Introduction: US Corporate Tax — What UK Businesses Expanding Into America Need to Know

Introduction: What UK Businesses Need to Know Before Expanding Into the US Tax System

The UK held a foreign direct investment position of $636 billion in the US at end-2023, ranking as the 4th largest source of FDI — yet many UK companies entering this market underestimate the tax complexity awaiting them. The US corporate tax system differs fundamentally from the UK's single-rate corporation tax in structure, layering, and compliance requirements, creating a steep learning curve for foreign businesses.

This guide covers the federal 21% rate, state-level taxes, special rules for foreign companies, the US-UK double taxation treaty, and key filing obligations.

One critical misconception to address upfront: the effective rate UK businesses face in the US is consistently higher than 21% once state taxes are included. Combined federal and state rates typically reach 25–30%, making it essential to understand the full picture before committing capital.

TLDR: Key Takeaways for UK Businesses

- Federal rate is 21%, but combined federal and state rates typically reach 25–30%

- Tax applies to income "effectively connected" with US business activities — whether branch or subsidiary

- The US-UK Treaty reduces withholding rates but does not eliminate US tax obligations

- Branch vs. C corporation structures carry very different tax consequences — the choice matters

- Quarterly estimated payments, filing deadlines, and transfer pricing rules require proactive compliance planning

How the US Corporate Tax System Works

The US levies corporate income tax at two levels—federal and state—creating a layered system unlike the UK's single-rate corporation tax. The federal rate is a flat 21% on all taxable income for C corporations, introduced under the Tax Cuts and Jobs Act (TCJA) on December 22, 2017, effective January 1, 2018.

Taxable income for US purposes starts with gross receipts minus allowable deductions — cost of goods sold, wages, interest, depreciation, and R&D expenses. The net income approach mirrors the UK concept, but several deductions work differently. Key differences include:

- Interest expense limited to 30% of adjusted taxable income under IRC Section 163(j)

- Charitable contributions capped at 10% of taxable income

- Dividends-received deduction of 50–65% depending on ownership percentage

Entity Types UK Businesses Must Understand

C corporations are the standard taxable entity and the most common structure for foreign-owned US businesses. Profits are taxed at the corporate level, then again when distributed as dividends—creating double taxation.

S corporations cannot have foreign shareholders. IRC Section 1361(b)(1)(C) states an S corporation must "not have a nonresident alien as a shareholder," making this structure unavailable to UK parent companies.

Given that restriction, pass-through entities (LLCs, partnerships) are often the next option to consider. They flow income directly to owners, making them relevant where a UK individual is involved — though less common for UK corporate structures entering the US.

Special Rules for Large Corporations

The Corporate Alternative Minimum Tax (CAMT) imposes a 15% minimum tax on adjusted financial statement income for companies with average annual income exceeding $1 billion. Most UK SMEs entering the US won't hit this threshold, but UK multinationals with US operations at scale should confirm their exposure before filing.

GILTI (Global Intangible Low-Taxed Income) applies to US shareholders of controlled foreign corporations. The applicable rate depends on when your tax year falls:

| Tax Year | Deduction | Effective GILTI Rate |

|---|---|---|

| Before 1 January 2026 | 50% | ~10.5% |

| From 1 January 2026 | 37.5% | ~13.125% |

UK businesses with mixed US-UK structures should model GILTI exposure against both scenarios before the 2026 change takes effect.

Federal vs. State Corporate Tax: Understanding the Real Combined Rate

44 US states levy their own corporate income tax on top of the federal 21%, with rates ranging from 2.0% to 11.5%. Four states—Nevada, Ohio, Texas, and Washington—impose gross receipts taxes instead. South Dakota and Wyoming have no corporate income or gross receipts tax.

The combined effective rate matters most for UK businesses choosing where to incorporate or operate. The United States has a combined federal and state statutory corporate tax rate of 25.57%, ranking as the 82nd-highest globally. This means the realistic planning figure for most UK businesses is 25–30%, not just 21%.

State choice has a direct impact on that combined rate. At the high end:

Highest state corporate tax rates:

- New Jersey: 11.5% (income over $10 million)

- Minnesota: 9.8%

- Illinois: 9.5% (combined)

- Alaska: 9.4%

- California: 8.84%

At the other end of the spectrum, several states actively compete for business incorporation:

Business-friendly states:

- South Dakota and Wyoming: No corporate income or gross receipts tax

- North Carolina: 2.0% flat rate (reduced from 2.25% in 2026)

- Missouri and Oklahoma: 4.0% flat rate

State tax rules are not uniform. Some states start from federal taxable income and apply modifications; others use entirely separate calculations.

Apportionment formulas (based on sales, payroll, and property in-state) determine how much income each state can tax. 34 states use single-sales-factor apportionment, which benefits companies with in-state operations but customers elsewhere.

Nexus: When Does a UK Business Owe State Tax?

Nexus is the threshold of connection a business must have with a state before that state can tax its income. Physical presence (office, warehouse, employees) traditionally establishes nexus. Many states now apply economic nexus based on revenue levels from customers in the state, even without physical presence.

The Multistate Tax Commission's Factor Presence Nexus Standards set the following trigger thresholds:

- $50,000 in in-state property or payroll

- $500,000 in in-state sales

UK businesses selling into the US remotely may already have state tax obligations they have not accounted for. Reviewing nexus exposure early is one of the most overlooked steps in US market entry planning.

How UK Businesses Are Taxed in the US: Key Rules for Foreign Companies

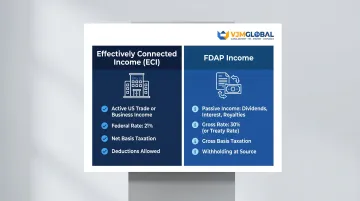

A UK company is considered a "foreign corporation" for US tax purposes. Foreign corporations face two distinct income tax regimes depending on how their US income is generated:

| Income Type | What It Covers | Tax Rate | How It's Applied |

|---|---|---|---|

| Effectively Connected Income (ECI) | Income tied to active US trade or business | 21% federal | Net basis (deductions allowed) |

| FDAP Income | Passive income: dividends, interest, royalties from US sources | 30% (unless treaty reduces it) | Gross basis via withholding |

Understanding which category applies to your UK company's US income is the first step in determining your tax obligations.

Branch Profits Tax: An Additional Layer

When a UK company operates through a US branch (rather than a US subsidiary), it faces an additional 30% branch profits tax on earnings deemed remitted to the UK parent. The US-UK treaty reduces this to 5% for qualifying UK companies, but UK businesses must be aware that the branch route carries this extra tax layer — replicating the effect of dividend withholding.

Permanent Establishment (PE): The Critical Threshold

A UK business may trigger US corporate tax obligations if it has a permanent establishment in the US. Under the US-UK treaty, a PE includes:

- A fixed place of business (office, branch, factory, workshop)

- A building site or construction project lasting more than 12 months

- A dependent agent acting on the company's behalf

Below the PE threshold, income may not be taxable in the US at all. UK businesses in early-stage US market entry can often avoid US tax entirely by keeping activities below the PE threshold. Activities that are purely preparatory or auxiliary — storage, display, purchasing — generally don't create a PE.

Subsidiary vs. Branch: The Structural Decision

US subsidiary (C corporation):

- Provides liability separation from the UK parent

- Profits distributed to the UK parent are subject to withholding tax (reduced under treaty)

- Cleaner structure for US operations and future fundraising

US branch:

- Simpler to set up initially

- Subject to branch profits tax (5% under treaty)

- Raises PE complications

- Less attractive for long-term operations

The right structure depends on your stage of US entry. A branch may suit early exploration; a subsidiary typically makes more sense once operations are established and profits are flowing. Either way, the structural choice has lasting consequences for tax, liability, and exit planning — so it warrants professional advice before committing.

US Corporate Tax vs. UK Corporation Tax: Key Differences

Understanding how US corporate tax compares to the UK system helps you anticipate costs and avoid structural mistakes before entering the American market.

Rate comparison:

- UK corporation tax is 25% for profits over £250,000 (with a small profits rate of 19% for profits of £50,000 or less)

- US federal rate is 21%

- The effective combined US rate — federal plus state taxes — generally lands between 25–30%, matching or exceeding the UK rate

Structural differences:

- The UK operates a single national rate; the US has 44+ separate state tax systems

- Both countries tax C corporations as separate legal entities with double taxation on dividends

- US S corporations (pass-through taxation) are unavailable to UK parent companies

Interest deduction limits:

The US limits interest expense deductions to 30% of adjusted taxable income (ATI). For tax years 2022–2024, ATI was computed on an EBIT basis (excluding depreciation and amortisation). From tax year 2025 onwards, ATI reverts to an EBITDA basis under recent US tax legislation, which increases the deductible amount. For UK companies funding US operations through intercompany loans, this cap directly limits how much interest cost can be offset against US taxable income — a key consideration when modelling your financing structure.

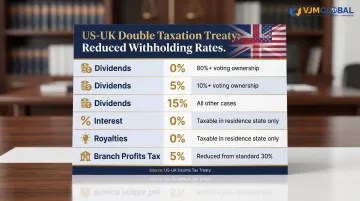

The US-UK Double Taxation Treaty and What It Means for UK Businesses

The US-UK Double Taxation Convention, signed July 24, 2001, and effective from March 31, 2003, prevents the same income from being taxed twice and provides important protections for UK businesses.

Key treaty benefits:

| Income Type | Treaty Rate | Conditions |

|---|---|---|

| Dividends | 0% | Beneficial owner holds 80%+ voting power for 12 months |

| Dividends | 5% | Beneficial owner holds 10%+ voting power |

| Dividends | 15% | All other cases |

| Interest | 0% | Taxable only in residence state |

| Royalties | 0% | Taxable only in residence state |

| Branch profits tax | 5% | Reduced from 30% domestic rate |

Treaty Benefits Are Not Automatic

UK businesses must actively claim treaty benefits by filing the relevant IRS forms. Form W-8BEN-E (Certificate of Status of Beneficial Owner for United States Tax Withholding and Reporting — Entities) is the primary document used to certify your status and claim reduced withholding rates.

The treaty also includes a Limitation on Benefits (LOB) clause — UK companies must pass at least one of the following tests to qualify:

- Publicly traded company test

- Ownership and base erosion test

- Active trade or business test

- Derivative benefits test

This anti-treaty-shopping provision (which blocks non-UK entities from routing income through UK structures just to access lower rates) is increasingly enforced by the IRS.

Transfer Pricing: A Separate Obligation

Even where the treaty reduces withholding rates, it does not affect how intercompany transactions are priced. UK-US related-party dealings remain subject to IRC Section 482, which requires arm's length terms regardless of treaty status. Key obligations include:

- Pricing all intercompany transactions (loans, services, IP licences) at market rates

- Maintaining contemporaneous transfer pricing documentation to defend positions on audit

- Facing penalties of 20–40% of any underpayment on substantial valuation misstatements

US Corporate Tax Filing Requirements and Key Deadlines

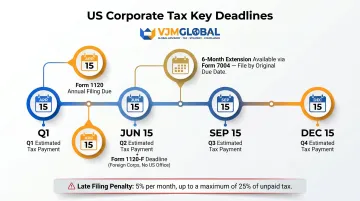

Form 1120 (US Corporation Income Tax Return):

- Due by the 15th day of the 4th month after the tax year ends (April 15 for calendar-year companies)

- 6-month extension available on request via Form 7004

- Late filing penalty: 5% of unpaid tax per month (maximum 25%)

Form 1120-F (Foreign Corporation):

- Filed by foreign corporations with US income

- April 15 deadline for those with a US office

- June 15 for foreign corporations without a US office

Estimated tax payments:

- C corporations must make quarterly estimated tax installments by the 15th day of the 4th, 6th, 9th, and 12th months of the tax year

- For calendar-year corporations: April 15, June 15, September 15, December 15

- Underpayment penalty applies if tax liability is $500 or more and estimates were insufficient

UK businesses used to a single annual payment should pay close attention to this quarterly cadence — missing instalments triggers underpayment penalties, calculated on Form 2220.

Transfer Pricing Documentation: A High-Risk Area

Beyond deadlines, transfer pricing is another area where UK businesses with a US subsidiary or branch face significant exposure. The IRS requires contemporaneous transfer pricing documentation for intercompany transactions. The IRS expects documentation on:

- Business overview and organizational structure

- Detailed description of transactions

- Method selection and analysis

- Comparables and benchmarking

- Economic projections and assumptions

Documentation must exist when the return is filed and be provided to the IRS within 30 days of a request. Penalties for transfer pricing adjustments are steep:

- 20% for substantial valuation misstatement — where the reported price is 200% or more, or 50% or less, of the correct arm's length price

- 40% for gross valuation misstatement — where the reported price is 400% or more, or 25% or less

Frequently Asked Questions

What are US corporate tax rates?

The US federal corporate tax rate is a flat 21% for C corporations. However, most businesses face a combined federal and state effective rate of approximately 25–30%, depending on the state where they operate and their apportionment formula.

How does corporate tax work in the USA?

US corporate tax is levied on net taxable income (revenue minus allowable deductions) at the federal level by the IRS and separately at the state level by each state's revenue authority. C corporations are taxed at the entity level, with shareholders also taxed on any dividends received.

How much corporation tax do you pay on $100,000?

At the 21% federal rate, a C corporation with $100,000 of taxable income would owe $21,000 in federal tax. State corporate tax adds a further $2,000–$11,500 on top, varying by state rate and apportionment formula.

Is the 21% corporate tax rate permanent?

The 21% rate established by the 2017 TCJA has no scheduled sunset date, making it technically permanent. That said, it has faced proposed changes under different administrations — UK businesses should track legislative developments, particularly proposals discussed through 2025–2026.

What are the tax changes coming in 2026?

The One Big Beautiful Bill Act (OBBBA) introduced BEAT and Section 163(j) changes, setting the BEAT rate at 10.5% and restoring the EBITDA basis for interest limitation calculations for tax years beginning after December 31, 2024. The 21% corporate rate remains unchanged. UK businesses should consult a tax adviser for guidance on how these changes affect their specific structure.

When did the US corporate tax rate change to 21%?

The Tax Cuts and Jobs Act (TCJA), signed into law on December 22, 2017, reduced the federal corporate income tax rate from 35% to a flat 21%, effective for tax years beginning on or after January 1, 2018.