Introduction

Over 4.3 million Indians live and work in the UAE — roughly 35% of the country's population. Many earn well, pay no tax locally, and assume their financial life is clean. Then an Indian bank deducts 30% TDS on NRO account interest, or the income tax department sends a notice about income not declared in India.

The confusion is understandable. The UAE charges no personal income tax, so why does India still want a cut?

The answer lies in how the India-UAE Double Taxation Avoidance Agreement (DTAA) actually works. It doesn't create a tax-free zone for UAE NRIs — it allocates taxing rights between two countries and caps rates on specific income types.

Understanding the difference between what India can tax and what the DTAA limits is what separates smart tax planning from an unexpected bill.

This guide covers exactly that: how the treaty operates, the specific rates that apply, which Indian income remains taxable, and the precise steps to claim DTAA benefits.

Key Takeaways

- The India-UAE DTAA prevents double taxation but does not eliminate Indian tax on India-sourced income

- UAE salary income faces zero tax in both countries for qualifying NRIs

- India still taxes NRO interest, rental income, capital gains, and dividends earned from Indian sources — regardless of your UAE residency

- TDS on NRO interest drops from 30% to 12.5% under the DTAA — but only with a valid TRC and Form 10F

- Without both documents on file with your Indian payer, full domestic TDS rates apply

What Is the India-UAE DTAA and Who Qualifies?

The India-UAE DTAA is a comprehensive bilateral treaty signed on April 29, 1992, which entered into force on September 22, 1993. It has since been amended twice (in 2007 and 2013) to keep pace with evolving trade and investment flows. Its purpose is straightforward: prevent the same income from being taxed in full by both countries and encourage cross-border investment.

Who Can Use the Treaty?

Three groups qualify:

- UAE tax residents: individuals physically present in the UAE for 183 or more days in a consecutive 12-month period, holding a valid Tax Residency Certificate (TRC) from the UAE Federal Tax Authority

- NRIs in the UAE with India-sourced income: NRO account holders, rental property owners, shareholders in Indian companies

- UAE-based businesses: companies with investments or active operations in India

What Taxes Does the Treaty Cover?

| Country | Taxes Covered |

|---|---|

| India | Income tax, surcharge, surtax, and wealth tax |

| UAE | Corporation tax, income tax, and wealth tax under individual emirate tax laws |

The UAE currently levies no personal income tax on individuals. For most UAE NRIs, the treaty's practical value is entirely about reducing or eliminating Indian tax on India-sourced income. Protecting UAE income from Indian tax simply isn't a concern — there's no UAE personal tax to protect against.

How the India-UAE DTAA Works: Two Methods to Avoid Double Taxation

The treaty works by assigning taxing rights to one or both countries for each income type. Two mechanisms handle this.

Exemption Method

One country gets the exclusive right to tax a specific income — the other country exempts it entirely.

UAE salary income is the clearest example. The UAE holds the primary taxing right because the work is performed there — and since the UAE levies no personal income tax, the effective rate is zero. India does not tax this income again, provided the individual qualifies as a non-resident under Indian law.

Result: UAE employment income faces no tax in either country for qualifying NRIs.

Tax Credit Method

Both countries can tax the same income, but the tax paid in one country is credited against the liability in the other.

Example: An NRO fixed deposit earns ₹5,00,000 in interest. India deducts TDS at 12.5% under the DTAA (₹62,500). If the UAE were to tax this same income, the resident could claim a ₹62,500 credit against UAE tax owed. That credit eliminates the double taxation.

Which method applies depends entirely on the income type. NRO interest, for instance, falls under the credit method — not the exemption method. Misapplying this leads to incorrect ITR filing and potential notices from the Income Tax Department.

Tax Residency: The Gateway to DTAA Protection

DTAA benefits are only available to tax residents of one of the two contracting states. An individual must satisfy both tests:

- UAE side: 183+ days of physical presence in a consecutive 12-month period (UAE FTA standard)

- India side: Must qualify as a non-resident under Section 6 of the Indian Income Tax Act — generally, spending fewer than 182 days in India in a financial year

One exception: Indian citizens or PIOs with Indian income above ₹15 lakh must stay under 120 days in India to maintain non-resident status.

If a UAE-based Indian spends too many days in India, they become an Indian tax resident — and their global income becomes taxable in India. Day-counting is not a formality.

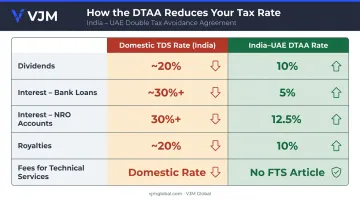

DTAA Rates Between India and UAE: What You Actually Pay

The treaty significantly reduces withholding tax rates compared to standard Indian domestic rates.

| Income Type | Domestic TDS Rate | India-UAE DTAA Rate |

|---|---|---|

| Dividends | ~20% | 10% (Article 10) |

| Interest — bank/financial institution loans | 30%+ (NRIs) | 5% (Article 11) |

| Interest — all other (incl. NRO accounts) | 30%+ (NRIs) | 12.5% (Article 11) |

| Royalties | ~20% | 10% (Article 12) |

| Fees for Technical Services | Domestic rate applies | No FTS article in DTAA |

A few important clarifications on each category:

Dividends (Article 10): India can tax dividends paid to UAE residents, but the rate is capped at 10% of the gross amount — half the standard domestic rate of around 20%.

Interest (Article 11): For NRO accounts — the most common scenario — domestic TDS runs at 30% plus surcharge and cess. The DTAA cuts this to 12.5% for most interest, or 5% on loans from a bank or financial institution. Claiming either rate requires a valid TRC and Form 10F.

Royalties (Article 12): Payments for use of copyrights, patents, trademarks, formulas, or industrial equipment are capped at 10%. Payments related to natural resource extraction are excluded from this definition.

Fees for Technical Services: The India-UAE DTAA contains no separate FTS article. Service payments typically fall under Article 7 (business profits) and are taxable in India only if the UAE entity has a permanent establishment there — not automatically at full domestic rates. UAE businesses providing services to Indian clients should review their PE exposure before assuming exemption applies.

Capital Gains: The Article 13 Rules

- Gains from Indian real estate → taxable in India regardless of the seller's UAE residency

- Gains from shares in companies whose assets are primarily Indian immovable property → taxable in India

- Gains from other property (movable assets) → taxable only in the seller's country of residence

On mutual fund gains: ITAT Delhi in Saket Kanoi v DCIT (ITA No. 3243/Del/2023, October 23, 2024) held that capital gains from Indian debt mutual funds held by a UAE resident were not taxable in India under Article 13(5). This ruling has not been overturned or appealed.

UAE NRIs holding Indian mutual funds should get current advice before filing.

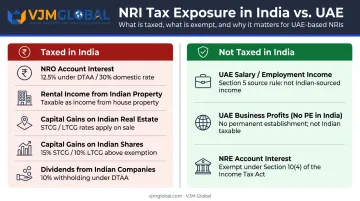

What India Still Taxes for UAE-Based NRIs

Living in a zero-tax country does not insulate India-sourced income from Indian tax. The DTAA prevents India from taxing UAE income — it doesn't prevent India from taxing income that originates within its own borders.

Taxed in India

| Income Type | Tax Treatment |

|---|---|

| NRO account interest | TDS at 30%+ under domestic law; reducible to 12.5% under DTAA with TRC + Form 10F |

| Rental income from Indian property | Taxable in India; standard deduction and expenses available |

| Capital gains on Indian real estate | Taxable in India at applicable rates |

| Capital gains on Indian company shares | Taxable in India (subject to treaty provisions) |

| Dividends from Indian companies | Taxable at 10% under DTAA (vs. ~20% under domestic law) |

Not Taxed in India

- UAE salary/employment income — not India-sourced, exempt for qualifying NRIs

- UAE business profits — not India-sourced (subject to PE analysis)

- NRE account interest — exempt under Section 10(4) of the Indian Income Tax Act for qualifying non-residents; DTAA is irrelevant here

The NRE/NRO distinction trips up many NRIs. NRE interest is already statutory-exempt under Indian law — no treaty documentation needed. NRO interest is where the DTAA applies directly: filing TRC and Form 10F can reduce your effective tax rate from 30%+ to 12.5%.

PE Exposure for Business Owners

Indian-origin entrepreneurs operating UAE companies need to understand Article 5. Business profits are only taxable in India if the UAE company has a permanent establishment (PE) there — but the India-UAE DTAA sets a lower bar than the OECD Model.

Common PE triggers to watch for:

- Fixed place PE: A branch, office, factory, or warehouse in India

- Construction/service PE: Projects lasting more than 9 months (vs. 12 months under OECD standard)

- Dependent-agent PE: A senior employee regularly travelling to India to conclude contracts on the company's behalf

Any UAE business with India-facing activity should run a PE risk assessment before treating its profits as India-tax-free.

How to Claim DTAA Benefits in India: Documents and Process

DTAA benefits are not automatic. Two documents are non-negotiable:

Tax Residency Certificate (TRC) — Issued by the UAE Federal Tax Authority, confirming UAE tax residency for the relevant year. Apply through the UAE FTA's tax residency service portal.

Form 10F — A self-declaration filed on the Indian income tax e-filing portal (required electronically since DGIT(Systems) Notification No. 03/2022 dated July 16, 2022). (Note: Non-residents without a PAN who are not required to obtain one can still file electronically.)

Without both documents, Indian payers — banks, tenants, companies — will deduct TDS at the full domestic rate.

The Claim Process

To get reduced TDS from the start:

- Obtain TRC from UAE FTA for the relevant financial year

- File Form 10F on the Indian income tax portal

- Submit both to your Indian bank, tenant, or company payer before income is received

If full TDS was already deducted:

- File an ITR (ITR-2 for most NRIs without business income; ITR-3 if business/profession income is involved)

- Cite the relevant DTAA article in the return

- Claim the excess TDS as a refund

Filing an ITR is often necessary even when TDS is withheld — it's how you recover over-deducted tax and formally apply treaty rates.

Common Errors to Avoid

- Treat DTAA claims as an annual task — documentation must be renewed each financial year

- Keep NRE and NRO accounts distinct: NRE interest is tax-free by law; DTAA relief applies to NRO interest

- Always file an ITR after TDS deduction — skipping it permanently forfeits any excess refund

- Track India visit days carefully; crossing residency thresholds inadvertently triggers Indian tax liability

VJM Global's NRI tax advisory team helps UAE-based clients navigate each step of this process — from residency status determination and Form 10F filing to TRC documentation and ITR-2/ITR-3 preparation under the India-UAE DTAA.

Frequently Asked Questions

Is there a DTAA between India and the UAE?

Yes. The India-UAE DTAA was signed on April 29, 1992, and entered into force on September 22, 1993. It is a comprehensive agreement covering income, wealth, and capital taxes in both countries, with formal amendments in 2007 and 2013.

Do I have to pay taxes in India if I earn in the UAE?

UAE salary is generally not taxable in India if you qualify as a non-resident under Indian tax law. However, any income that originates in India — NRO account interest, rental income, capital gains, and dividends from Indian companies — remains taxable in India regardless of UAE residency.

Who is eligible for DTAA benefits under the India-UAE treaty?

Individuals and companies who are tax residents of India or the UAE are eligible. For UAE residents, a valid TRC from the UAE Federal Tax Authority is the primary proof required to claim reduced withholding tax rates in India.

What documents are required to claim DTAA benefits in India?

Two mandatory documents: (1) a Tax Residency Certificate issued by the UAE FTA, and (2) Form 10F filed electronically on the Indian income tax portal. Both must be submitted to Indian payers or included with your ITR to apply DTAA-reduced rates.

What is the TDS rate on NRO interest for UAE NRIs under the DTAA?

Under domestic Indian law, TDS on NRO interest is 30% plus surcharge and cess. Under the India-UAE DTAA, this reduces to 12.5% for most interest income, or 5% for interest on loans from banking institutions — provided the NRI submits a valid TRC and Form 10F to their Indian bank.

Is the India-UAE DTAA relevant now that the UAE has introduced corporate tax?

Yes — and more so now. The UAE corporate tax (9% on income above AED 375,000, effective June 1, 2023) is covered under Article 2 of the DTAA. Businesses can offset UAE corporate tax against Indian tax liabilities via the treaty's credit mechanism, and apply PE rules to determine where profits are taxable.