Introduction: India Market Entry for Singapore Businesses

India's economy crossed USD 3.91 trillion in nominal GDP in 2024, growing at 6.5%—making it one of the few major markets still expanding at that pace. For Singapore businesses, the case for entry is stronger than it is for most: geographic proximity, decades of bilateral ties, and favourable trade agreements create structural advantages that competing nationalities don't have.

Those advantages don't eliminate the friction. Singapore businesses routinely struggle with India's regulatory complexity, state-level variation in rules and incentives, and compliance obligations that kick in long after incorporation is done.

This guide covers what Singapore businesses need to know before and during entry: the bilateral advantages worth activating, the sectors showing strong performance for foreign entrants, the entity structures available, and the compliance essentials that separate a successful launch from a costly false start.

Key Takeaways

- India is the 5th largest economy by nominal GDP (USD 3.91 trillion in 2024) and 3rd largest by purchasing power parity; IMF projects India to become the 3rd largest economy by nominal GDP by 2031

- The Comprehensive Economic Cooperation Agreement (CECA) eliminates tariffs on 81% of Singapore's exports to India, covering over 3,000 product categories

- 100% FDI under automatic route is permitted in most sectors for wholly owned subsidiaries; other common structures include joint ventures, liaison offices, and distributor arrangements

- Key compliance obligations include FC-GPR filing within 30 days of share allotment, GST registration for all inter-state suppliers, and transfer pricing documentation for related-party transactions

- Singapore is India's 2nd largest FDI source (USD 171.92 billion cumulative, 23.87% of total inflows), giving Singapore entrants a recognized regulatory track record

Why India Is a Smart Next Step for Singapore Businesses

India's macroeconomic fundamentals present a compelling case for expansion. The country's USD 3.91 trillion economy grew at 6.5% in 2024, significantly outpacing developed markets and most major emerging economies. The World Bank projects sustained growth, maintaining India's position as one of the fastest-growing large economies globally.

The real opportunity lies in India's demographic profile. A median age of approximately 29.8 years means over 1 billion working-age people — a productive consumer base that is only beginning to spend.

Consumer patterns are shifting fast: by 2036, India's middle class and affluent consumers will account for 93% of all spending, up from 80% in 2026. By 2035, India will have 499 "consumer cities" where 75%+ of the population qualifies as consumer class, distributing purchasing power well beyond the traditional metros.

Government-led reforms have systematically removed barriers that previously restricted foreign entry:

- Production-Linked Incentive (PLI) schemes across 14 strategic sectors with Rs 1.91 lakh crore outlay (approximately USD 22.5 billion) have generated cumulative investment exceeding Rs 2.16 lakh crore and created over 14.39 lakh jobs as of December 2025

- 100% FDI under automatic route now applies to most sectors, eliminating prior approval requirements for foreign companies in areas including IT, e-commerce, renewable energy, pharmaceuticals (greenfield), logistics, and food processing

- Over 47,000 compliance requirements reduced in the last five years through digitization, simplification, decriminalization, and elimination

These reforms directly lower the cost and complexity of entry — which matters most to Singapore businesses operating at the scale of a highly developed but geographically constrained domestic market. For companies already optimized for efficiency and export, India's 1.45 billion consumers and digitizing economy offer a scope of growth that simply isn't available at home.

The Singapore-India Bilateral Edge Other Competitors Don't Have

Singapore enjoys a unique set of bilateral advantages that materially reduce the cost and complexity of India entry compared to most other foreign investor nationalities.

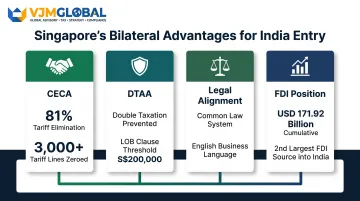

CECA: Tariff Elimination and Services Access

The Comprehensive Economic Cooperation Agreement between India and Singapore, which entered into force in 2005, eliminates tariffs on 81% of Singapore's exports to India. Over 3,000 tariff lines have been zeroed and another 2,000+ reduced, benefiting product categories including food, plastics, electronics, pharmaceuticals, and mechanical appliances. The 35% value content rule-of-origin requirement means Singapore companies can qualify for preferential tariffs even when sourcing some inputs regionally.

Beyond goods, CECA provides preferential access for Singapore service providers in engineering, banking, telecommunications, real estate development, finance, construction, logistics, R&D, and tourism—precisely the sectors where Singaporean companies have competitive strengths.

Double Taxation Avoidance Agreement (DTAA)

The India-Singapore DTAA prevents the same income from being taxed twice across jurisdictions. Following the Third Protocol signed in December 2016, the treaty shifted from residence-based to source-based taxation of capital gains on shares, with grandfathering provisions (protecting pre-existing investments from the new rules) for shares acquired before April 1, 2017. The treaty includes a Limitation of Benefits (LOB) clause requiring Singapore resident entities to have incurred expenditure of at least S$200,000 on operations in Singapore in the preceding 12 months—a threshold easily met by genuinely Singapore-based companies.

This framework provides predictability for dividend repatriation, royalty payments, and intercompany service fees between Singapore parents and Indian subsidiaries.

Shared Legal and Cultural Frameworks

Both India and Singapore operate under common law legal systems derived from British legal tradition. Singapore businesses entering India benefit from several structural familiarity advantages that companies from civil law jurisdictions simply don't have:

- Familiar legal concepts — company incorporation, shareholder agreements, contract structures, and dispute resolution all map closely to Singapore practice

- English as the business language — India's primary language for commerce and government eliminates the translation friction common in other Asian markets

- Active bilateral networks — the Singapore-resident Indian diaspora and chambers such as the Singapore Indian Chamber of Commerce and Industry reduce the information asymmetry that makes India difficult for Western entrants

FDI Position and Network Effects

Singapore's position as India's 2nd largest FDI source — with cumulative equity inflows of USD 171.92 billion (23.87% of total, January 2000–December 2024) — creates tangible operational benefits. Maharashtra receives 31% of Singaporean FDI and Karnataka 27%, meaning Singapore entrants in these states benefit from established professional services ecosystems, legal precedent, and regulatory familiarity that are absent for first-mover nationalities.

That investment concentration has produced a deep commercial relationship. Bilateral trade reached USD 34.26 billion in FY 2024-25, making Singapore India's largest trading partner in ASEAN. The September 2025 India-Singapore Joint Statement further committed to cooperation in digital finance, fintech, cybersecurity, and capital market linkages — giving Singapore businesses a policy tailwind that newer entrant nationalities will wait years to develop.

Top Sectors Where Singapore Companies Can Win in India

Fintech and Digital Financial Services

India's fintech market reached USD 44.12 billion in 2025 and is projected to reach USD 95.30 billion by 2030 at 16.65% CAGR. The opportunity is underpinned by digital infrastructure that Singapore companies can leverage rather than build from scratch.

UPI's scale is hard to overstate: 24,162 crore transactions worth approximately USD 3.7 trillion processed in FY 2025-26, covering 85% of India's digital payments and nearly 49% of global real-time payment transactions. UPI is already operational in 8 countries including Singapore, giving Singapore fintech firms a ready-made cross-border payment rail to build on.

The RBI Regulatory Sandbox framework enables fintech companies to test innovative solutions in a controlled environment for up to 6 months, with a minimum net worth requirement of just Rs 25 lakh (approximately USD 30,000). Five cohorts have been completed covering retail payments, cross-border payments, MSME lending, fraud prevention, and theme-neutral innovation.

Singapore fintech firms typically enter through one of three paths:

- Technology partnerships with Indian banks or NBFCs

- Startup investment in the Indian fintech ecosystem

- Direct entity setup to operate independently under RBI guidelines

Food and Beverage and Consumer Goods

Premium and health-conscious F&B is a strong fit for Singapore companies entering India. The urban middle class is expanding fast, and by 2035, over 20% of each key generation will spend USD 45+ per day, driving sustained demand for quality products that Singapore brands are well-positioned to supply.

The geography of this growth matters: 93% of urban consumer class growth through 2040 will occur outside the five largest cities. Singapore F&B companies that build Tier II and Tier III distribution from the start, rather than anchoring to Delhi and Mumbai, can capture disproportionate market share.

Many Singapore F&B businesses start with distribution agreements to test product-market fit before establishing direct operations, reducing upfront capital while building market knowledge.

Logistics, Supply Chain, and Smart Infrastructure

India reduced its logistics costs from 16% to 9% of GDP as of December 2025, according to a joint study by IIM Bangalore, IIT Madras, and IIT Kanpur. The National Logistics Policy targets further reduction to 8-9% of GDP, creating sustained demand for supply chain optimization services.

The PM Gati Shakti initiative represents a Rs 100 lakh crore (approximately USD 1.2 trillion) National Master Plan for holistic infrastructure development. This creates large-scale procurement opportunities in warehousing, cold chain logistics, and last-mile delivery — areas where Singapore logistics companies have proven expertise.

PLI-linked manufacturing growth across 14 sectors is generating sustained demand for supply chain services as production scales up and domestic sourcing increases.

Technology and SaaS

India hosts over 1,750 Global Capability Centers (GCCs) employing 1.9 million professionals, with revenue growing at 9.8% CAGR. By 2030, projections indicate 2,400+ GCCs, approximately USD 100 billion market size, and 4.5 million+ jobs.

Singapore tech companies typically pursue one or both of these models:

- Talent access: Establishing R&D or engineering centers in Bengaluru, Hyderabad, or Pune to build products at lower cost

- Market access: Selling SaaS solutions directly to Indian enterprises as a fast-growing customer base

Many Singapore firms run both in parallel — building in India while selling to Indian customers from day one.

The technology talent pool offers English-proficient engineers at costs significantly below Singapore levels, making India an attractive base for product development deployable globally.

Education and Professional Training Services

For Singapore's internationally accredited education providers, India's combination of a large youth population and strong demand for employability-linked credentials is a compelling entry case. Key parameters to note:

- FDI: 100% permitted under the automatic route

- Regulators: All India Council for Technical Education (AICTE) and University Grants Commission (UGC)

- Timeline: Factor regulatory consultation into your market entry schedule

The Viksit Bharat Shiksha Adhishthan Bill, 2025 will specify standards for select foreign universities operating in India, requiring prior Central Government approval for certain educational activities. Singapore providers entering this sector should plan for this regulatory layer early.

How to Structure Your India Entry: Business Entity Options

Wholly Owned Subsidiary (Private Limited Company)

The Wholly Owned Subsidiary—structured as a Private Limited Company under the Companies Act 2013—is the most common structure for foreign companies with long-term India ambitions. The parent company holds 100% equity, maintains full operational control, and creates a separate legal entity that limits liability exposure to the capital invested in the subsidiary.

100% FDI under automatic route applies in most sectors, meaning no prior government approval is required. Incorporation follows the SPICe+ process on the Ministry of Corporate Affairs portal, with government processing typically taking 7-12 working days from name reservation through Certificate of Incorporation.

Based on VJM Global's experience incorporating Indian subsidiaries for Singapore clients, the realistic timeline from document submission to Certificate of Incorporation is approximately 13-14 days, broken down as:

- Digital Signature Certificate (DSC): 2 days

- Director Identification Number (DIN): 1 day

- Name Approval: 5 days

- Company Registration and Certificate of Incorporation: 5 days

VJM Global's 30+ years of experience in Indian tax, audit, and compliance enables efficient handling of the full incorporation sequence, including document preparation, addressing Registrar of Companies queries, and ensuring all filings meet regulatory requirements.

Joint Venture with Local Indian Partner

A Joint Venture makes strategic sense when local market relationships, distribution networks, or government-sector access are critical to the business model. The JV structure allows risk-sharing and can provide faster market access through the Indian partner's existing infrastructure.

JV success depends entirely on partner selection and agreement quality. Thorough due diligence should verify financial standing, market reach in Tier II/III cities (where much of India's growth is occurring), and references from existing principals.

Clear JV agreements must cover profit sharing, IP ownership, decision-making authority, and exit provisions—misaligned incentives cause most JV failures in India.

VJM Global provides partner identification and negotiation support, helping foreign companies locate, initiate discussions, and formalize agreements with distributors, franchisees, or joint-venture partners.

Liaison Office

A Liaison Office allows a foreign company to maintain a representative presence in India for market research and relationship building, but cannot generate revenue or sign commercial contracts. Governed by RBI approval under the Foreign Exchange Management Act (FEMA), this structure is suited for early-stage market exploration.

The liaison office is expressly barred from undertaking any commercial, trading, or industrial activity. It cannot earn income, charge fees or commissions, or enter contracts for sale of goods/services. Funding must come 100% via inward remittances from the head office.

Annual compliance obligations include submitting an Annual Activity Certificate certified by a Chartered Accountant to the RBI, maintaining audited accounts, and obtaining a PAN and Unique Identification Number (UIN). VJM Global manages these ongoing compliance requirements for foreign companies operating liaison offices.

Branch Office

A Branch Office can conduct limited business activities (primarily for companies in specific sectors like banking, insurance, or trading), must be approved by RBI, and carries the full liability of the parent company since it is not a separate legal entity. This is the key distinction from a Liaison Office, and the primary reason most Singapore businesses avoid this structure.

If the branch incurs losses, the foreign parent must cover them by liquidating its own assets. A Private Limited Company subsidiary, by contrast, limits the parent's exposure to its shareholding amount. For most Singapore businesses, that unlimited liability profile makes the branch office a higher-risk option than a wholly owned subsidiary.

Distributor or Franchise Model

Distributor or franchise arrangements offer an asset-light entry point for Singapore businesses that want to test product-market fit before committing to full entity setup. This model provides faster market access and lower capital requirements, but comes with trade-offs: limited brand control and dependency on third-party performance.

Many Singapore companies use distributor arrangements as a bridge—validating demand and building market knowledge before establishing a wholly owned subsidiary. Once revenue thresholds justify the investment, transitioning to a subsidiary becomes straightforward.

VJM Global advises foreign clients on key issues at this stage, including:

- Legal and regulatory compliance obligations

- Contractual clarity and IP protection

- Taxation considerations for distributor arrangements

- Partner fit assessment and due diligence

Regulatory and Compliance Essentials for Singapore Companies

Core Registration Sequence

Getting your Indian entity fully operational requires coordination across multiple government agencies, each with distinct documentation requirements and timelines:

Company incorporation with the Ministry of Corporate Affairs (MCA): Includes name approval, DSC and DIN for directors, MOA and AOA preparation, and incorporation filing.

PAN and TAN: Permanent Account Number and Tax Deduction and Collection Account Number are required for all tax-related activities.

GST registration: Mandatory once annual turnover exceeds the prescribed threshold, but also required immediately for all inter-state suppliers regardless of turnover. Foreign-owned subsidiaries engaged in inter-state supply, imports/exports, or receiving services from their foreign parent under the Reverse Charge Mechanism must register for GST from day one.

EPFO registration: Required once employees are hired, covering Employees' Provident Fund and related labour law compliance.

This multi-agency process extends well beyond the 7-12 day incorporation window. Total operational readiness — including GST registration, bank account opening, and sector-specific licenses — typically takes several weeks to months. Singapore companies that underestimate these timelines face costly delays; VJM Global manages the end-to-end sequence to keep the process on track.

FEMA Compliance for Singapore Entities

Inbound FDI must be reported to RBI via Form FC-GPR within 30 days from the date of allotment of shares to the foreign investor. Allotment must occur within 60 days of receipt of funds; if it fails, refund is required within 15 days after the 60-day window. An annual Foreign Liabilities and Assets (FLA) Return is due by July 15.

Ongoing transactions between the Indian subsidiary and its Singapore parent — including management fees, royalties, intercompany loans, and service fees — are subject to transfer pricing regulations under Section 92E of the Income Tax Act. All entities involved in international transactions must obtain an audit report from a Chartered Accountant via Form 3CEB, filed by the income tax return due date.

VJM Global prepares the full suite of transfer pricing documentation required under Indian regulations:

- Master File — global group information and organisational structure

- Local File — specific intercompany transaction details and FAR analysis

- Country-by-Country Report (CbCR) — applicable for large multinational groups

Proper documentation significantly reduces exposure to penalties and transfer pricing disputes.

State-Level Regulatory Variation

Beyond central government registrations, state-specific licenses, labour law compliance (Shops and Establishments Act registration, Provident Fund/ESI requirements), and environmental clearances vary significantly by state. Singapore companies should choose their initial operating state strategically.

Gujarat and Tamil Nadu are frequently cited as top achievers in the DPIIT Business Reforms Action Plan (BRAP) for streamlined industrial clearance processes. Maharashtra offers the largest consumer market and receives 31% of Singaporean FDI into India, but typically involves higher operating costs. Karnataka (particularly Bengaluru) is the preferred location for technology and SaaS companies due to talent availability.

The right state choice depends on sector, customer location, talent requirements, and supply chain considerations — factors that often point away from the most obvious option.

Key Mistakes Singapore Businesses Make When Entering India

Treating India as a Single, Uniform Market

India operates as 28+ distinct business environments with different regulatory timelines, consumer preferences, infrastructure quality, and competitive dynamics. Companies that launch with a single national strategy often under-invest in regional adaptation and miss the growth occurring in Tier II and Tier III cities.

State-level feasibility analysis should precede location decisions, evaluating factors including regulatory environment, talent availability, logistics infrastructure, customer concentration, and operating costs.

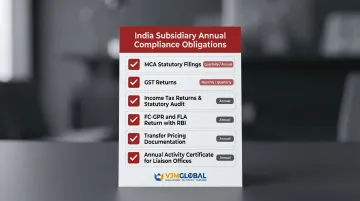

Underestimating Compliance Timelines and Costs

Company incorporation may take 13-14 days. But full operational readiness—GST registration, RBI approvals, sector-specific licenses, banking setup, and transfer pricing documentation—can take 12-18 months for complex businesses. Singapore companies that budget only for incorporation fees and ignore ongoing compliance costs are frequently caught off-guard.

Ongoing compliance obligations include:

- Quarterly and annual statutory filings with MCA

- Monthly/quarterly GST returns

- Annual income tax returns and statutory audits

- Annual FC-GPR and FLA Return filings with RBI

- Transfer pricing documentation (Master File, Local File, potentially CbCR)

- Annual Activity Certificate for liaison offices

Realistic total annual compliance costs for a Singapore company's Indian subsidiary in its first 1-2 years span statutory audit fees, GST filings, income tax preparation, transfer pricing documentation, and RBI reporting. Treat these as a substantial recurring cost, not a one-time setup line item.

Choosing the Wrong Local Partner or Skipping Due Diligence

A poorly vetted distribution or JV partner can damage brand reputation, create IP exposure, and waste 12-24 months of market time. Before signing any agreement, partner verification should confirm:

- Financial standing and credit history

- Market reach in Tier II/III cities relevant to your sector

- Operational capability and existing infrastructure

- Cultural fit and communication practices

- References from current principals

Contracts that clearly define profit sharing, IP ownership, decision authority, and exit terms prevent the disputes that derail otherwise promising market entries.

Frequently Asked Questions

What is the best market entry strategy for India?

The best strategy depends on your sector, scale, and timeline. Wholly Owned Subsidiary suits companies with long-term commitment and sectors with 100% FDI under automatic route. Distributor or franchise models work for initial market testing with lower capital requirements.

Can Singaporean companies legally start a business in India?

Yes, Singapore companies can establish 100% wholly owned subsidiaries in most sectors under India's automatic FDI route without prior government approval. The India-Singapore CECA further facilitates investment and professional service flows.

Which businesses in India have the highest success rates?

Technology/SaaS, fintech, consumer goods, and logistics have seen strong foreign entrant performance, particularly when companies localize their offering and invest in Tier II/III market distribution rather than limiting themselves to metro cities.

What are the advantages and disadvantages of entering the Indian market?

Key advantages: 1.45 billion consumers, 100% FDI automatic route in most sectors, a skilled English-speaking workforce, and CECA benefits specific to Singapore companies. Key challenges: multi-layer compliance requirements, state-level regulatory variation, and timelines to profitability that typically run longer than expected.

What are the visa and entry requirements for Singapore business owners operating in India?

Singapore citizens can visit India on a business visa or e-visa for exploratory meetings. Operating formally — hiring staff, signing contracts, conducting regulated activities — requires proper entity registration and employment documentation in India. For current visa categories, contact the Indian High Commission in Singapore directly.

Is outsourcing to India worth it for Singapore companies?

India's depth of English-speaking talent in IT, finance, and back-office functions makes it a strong outsourcing option for Singapore companies. You can structure this through a captive center (owned subsidiary) or a third-party provider — both deliver meaningful cost savings relative to Singapore-based operations.

VJM Global has helped 500+ American, 250+ UK, and 250+ Australian businesses set up and operate in India over 30+ years. We handle accounting outsourcing, tax compliance, FDI advisory, and full business setup — so Singapore companies enter India with the regulatory groundwork already done. Reach us at info@vjmglobal.com or +91 98915 76441 to discuss your market entry plan.