Introduction

Singapore is India's 2nd largest source of foreign direct investment, contributing USD 171.92 billion — 23.87% of India's total cumulative FDI as of December 2024. That's not a coincidence. At under 4 hours by flight and a 2.5-hour time zone difference, Singapore companies can maintain hands-on operational oversight that Western competitors simply can't match.

Despite these advantages, expansion without preparation creates friction. India's regulatory environment — increasingly liberalized, but still layered — requires navigating:

- Company incorporation and MCA filings

- RBI reporting and FEMA compliance

- GST registration and ongoing returns

- Transfer pricing documentation

- State-level regulatory variations

Cultural nuances in business negotiations add a further dimension that catches many first-time entrants off-guard.

This guide gives Singapore companies a clear roadmap for India market entry. You'll find out which business structure delivers the best tax efficiency, how incorporation works step-by-step, what taxes apply, and which sectors offer the strongest growth potential right now.

TLDR

- CECA and DTAA treaty protections reduce withholding tax to 10-15% (vs. 20% standard rate)

- A wholly-owned subsidiary (Private Limited) offers ~25% effective tax vs. 42-44% for Branch Offices

- Incorporation via SPICe+ takes 2-4 weeks; full operational readiness (PAN, GST, bank account) takes 4-8 weeks

- Top sectors: fintech (87% adoption), renewable energy, SaaS, healthcare, and semiconductors (50% government co-investment)

Why Singapore Businesses Should Expand to India Right Now

India's economic momentum has created a narrow window for first-mover advantage. The World Bank projects India's GDP growth at 6.6% for FY27, maintaining its position among the world's fastest-growing major economies despite global headwinds. The IMF forecasts India will become the 3rd largest economy globally by 2031, reinforcing the structural growth trajectory.

That growth is being driven by a rapidly expanding consumer base. Nearly 80% of Indian households will be middle-income by 2030, up from roughly 50% today, according to the World Economic Forum. This shift will drive 75% of consumer spending — creating strong demand across technology, financial services, healthcare, and consumer goods, all sectors where Singapore companies have proven track records.

Policy reforms have also lowered the barriers to entry considerably. Singapore companies can now enter most sectors without a local partner, thanks to FDI liberalization allowing 100% foreign ownership via the automatic route. Key initiatives include:

- Make in India: Broad industrial policy push incentivizing foreign investment across manufacturing and services

- PLI Schemes: Production Linked Incentives across 14 strategic sectors, with Rs 1.91 lakh crore (USD 21 billion) in committed support

- Approved PLI applications: 836+ approvals to date, generating Rs 2.16 lakh crore in cumulative investment and 1.44 million jobs

For Singapore businesses evaluating entry timing, the combination of GDP growth, rising consumer spending, and accessible FDI rules makes the case difficult to ignore.

Singapore's Unique Advantages When Entering India

CECA Treaty Framework Delivers Measurable Market Access Benefits

The India-Singapore Comprehensive Economic Cooperation Agreement (CECA), signed in 2005, provides Singapore-registered businesses with preferential market access for goods, services, and investments. Key advantages unavailable to most other countries include:

- Reduced or zero tariffs on qualifying goods traded between both nations

- Simplified market entry procedures for services and investment

- Mutual recognition frameworks that speed up regulatory approvals

Singapore Dominates the FDI Corridor

Singapore's position as India's 2nd largest FDI source reflects a deeply established investment corridor. Key metrics demonstrate this dominance:

| FDI Metric | Value |

|---|---|

| Cumulative FDI Equity (Jan 2000 - Dec 2024) | USD 171.92 billion |

| Share of India's Total FDI | 23.87% |

| CY2024 FDI Inflow | USD 16.31 billion |

| Top Receiving Sectors | Services (18%), Computer Software & Hardware (17%), Trading (13%) |

| Top Indian States | Maharashtra (31%), Karnataka (27%), Delhi (14%) |

This established corridor means Singapore companies benefit from established regulatory precedents, banking relationships familiar with Singapore-India flows, and mature advisory ecosystems that lower setup risk.

DTAA Tax Efficiency Changes Repatriation Economics

The India-Singapore Double Taxation Avoidance Agreement delivers substantial tax savings compared to domestic withholding rates:

| Income Type | DTAA Rate | Domestic Rate | Condition |

|---|---|---|---|

| Dividends | 10% | 20% | Beneficial owner holds ≥25% equity |

| Dividends | 15% | 20% | All other cases |

| Interest | 10% | 5-20% | Bank or financial institution loan |

| Interest | 15% | 5-20% | All other cases |

| Royalties | 10% | 20% | - |

| Technical Services Fees | 10% | 20% | - |

For Singapore companies repatriating dividends, interest, or royalty income from Indian operations, these reduced rates directly improve after-tax returns — making Singapore a tax-efficient holding structure for India subsidiaries.

Cultural and Geographic Proximity Reduces Operational Friction

Singapore's Indian diaspora comprises 9% of the resident population, creating natural cultural bridges and business networks. Widespread English proficiency and a working familiarity with Indian business culture — relationship-driven, hierarchical, built on long-term trust — give Singapore-based founders real advantages in negotiations that Western competitors often lack.

The logistics reinforce this edge. A 2.5-hour time zone difference enables real-time collaboration, and flight times under 4 hours to Bengaluru, Mumbai, or Delhi make frequent site visits practical — especially valuable during early-stage expansions requiring hands-on management.

Business Structure Options for Singapore Companies Expanding to India

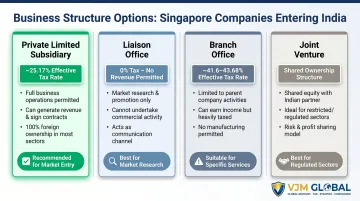

Private Limited Company (Wholly-Owned Subsidiary)

This is the most popular and tax-efficient structure for Singapore companies. Key characteristics:

- 100% FDI permitted via automatic route in most sectors

- Separate legal entity limiting parent company liability

- Full operational control without requiring a local Indian partner

- Taxed as a domestic company at approximately 25.17% effective rate (22% base + 10% surcharge + 4% cess)

- New manufacturing companies incorporated after October 1, 2019 qualify for 15% base rate (effective ~17.16%)

VJM Global assists Singapore companies in incorporating wholly-owned subsidiaries within 2-4 weeks, providing end-to-end support from DSC procurement through post-incorporation registrations including PAN, TAN, GST, and corporate bank account opening.

Liaison Office (LO)

A Liaison Office is the lowest-commitment entry point — useful for testing the market before deploying capital. Permitted activities include:

- Representing the parent company in India

- Conducting market research

- Promoting products and facilitating collaborations

One hard constraint: an LO cannot execute contracts, generate revenue, or conduct any commercial activities. All operating expenses must be funded through inward remittances from the parent company. This makes it suitable only for Singapore companies still evaluating market fit.

Recent RBI draft regulations eliminate prior USD 50,000 financial eligibility thresholds and remove three-year tenure caps, making LO establishment more accessible.

Branch Office

Branch Offices can carry out limited commercial activities:

- Import/export operations

- Research and development

- Professional/consulting services

- IT services and technical support

The tax position is the key drawback. Because a Branch Office is treated as an extension of the foreign parent, it faces an effective tax rate of 41.6-43.68% (40% base + surcharge + cess) — versus ~25% for a subsidiary. That 17-18 percentage point gap makes Branch Offices practical only for short-term, project-specific engagements where full subsidiary incorporation isn't worth the setup cost.

Joint Venture with Indian Partner

Joint Ventures make strategic sense when:

- 100% FDI is restricted in the target sector

- Local distribution networks and market relationships are critical

- Regulatory navigation requires an established Indian partner

VJM Global supports JV structuring end-to-end — covering partner due diligence, valuation based on financial statements and credit ratings, and shareholder agreement drafting with clause-level review to close common contractual gaps.

FDI Route Classification

Whichever structure you choose, its viability depends on the FDI route governing your target sector. The two classifications are:

- Automatic Route: No prior government approval required; applies to most sectors including manufacturing, IT services, and financial services

- Government Route: Prior approval required for sectors including defense, media, broadcasting, multi-brand retail (51% cap), and brownfield pharmaceuticals (above 74%)

Singapore entities are not subject to the mandatory government approval requirement imposed on investors from countries sharing land borders with India (China, Pakistan, Bangladesh, etc.).

How to Register Your Business in India from Singapore

Step 1: Obtain Digital Signature Certificate (DSC) and Director Identification Number (DIN)

Before any incorporation filing can proceed, at least one director of the proposed Indian entity must obtain a Director Identification Number (DIN) from the Ministry of Corporate Affairs. All authorized signatories require Digital Signature Certificates (DSC) for electronic filing authentication.

Required documents for Singapore company directors:

- Passport-size photograph

- Self-attested address proof (apostilled/notarized for foreign nationals)

- Self-attested identity proof (passport copy for foreign nationals)

- Self-attested PAN card (if applicable)

DSC procurement takes 1-2 days; DIN issuance follows within 1 business day.

Step 2: Name Reservation and Incorporation via MCA Portal

The SPICe+ (Simplified Proforma for Incorporating Company Electronically) process consolidates multiple registrations into two parts:

Part A — Reserve your company name through the RUN (Reserve Unique Name) service. Names must comply with Companies Act, 2013 conventions and cannot duplicate existing registered entities.

Part B — Submit incorporation documents including:

- Memorandum of Association (MoA) and Articles of Association (AoA)

- Proof of registered address (rental agreement or ownership documents)

- Passport copies and address proof for all foreign directors

- Digital signatures of subscribers and witnesses

MCA processing takes 5-7 days after submission, with the Certificate of Incorporation issued on the day of approval. VJM Global consistently achieves 13-15 day total incorporation timelines by ensuring documentation accuracy and resolving MCA queries before they cause delays.

Step 3: Post-Incorporation Registrations

After receiving the Certificate of Incorporation, four mandatory registrations follow:

- PAN (Permanent Account Number): Issued by the Income Tax Department; required for all tax filings and financial transactions

- TAN (Tax Deduction Account Number): Needed when the company deducts tax at source from employee salaries, contractor fees, or vendor payments

- GST Registration: Mandatory once aggregate annual turnover exceeds ₹20 lakh (₹10 lakh for northeastern and hill states). Must be completed before commencing taxable supplies

- Corporate Bank Account: Required for receiving FDI remittances. Banks typically ask for the Certificate of Incorporation, PAN, MoA, AoA, a board resolution for account opening, and identity/address proof for directors

Complete post-incorporation setup typically takes 2-4 weeks.

Step 4: RBI/FEMA Compliance for Inward FDI

Once your Singapore parent transfers capital into the Indian entity, a critical compliance clock starts. You must report the foreign investment to the Reserve Bank of India via the FIRMS portal within 30 days of receiving funds.

The FC-GPR (Foreign Currency – Gross Provisional Return) filing documents share issuance to your Singapore entity—in plain terms, it confirms that your Indian company has formally issued equity in exchange for the inbound capital. Missing this deadline attracts penalties and can complicate future capital raising or profit repatriation.

VJM Global manages FEMA compliance end-to-end, ensuring timely FIRMS portal reporting and maintaining audit-ready documentation for RBI reviews.

Step 5: Ongoing Compliance Obligations

Indian private limited companies carry recurring statutory obligations after incorporation. Key annual and periodic filings include:

- Annual return (Form MGT-7), financial statements (Form AOC-4), and director disclosures filed with MCA

- Corporate income tax returns, due by September 30 after fiscal year-end

- GST returns — monthly GSTR-1 (outward supplies) and GSTR-3B (summary return), with quarterly options for smaller taxpayers

- Transfer pricing documentation for all transactions with the Singapore parent, including the mandatory Form 3CEB Accountant's Report

- Quarterly TDS returns for tax deducted at source on salaries, contractor payments, and other applicable transactions

VJM Global provides ongoing compliance outsourcing — handling all statutory filings, maintaining statutory registers, and tracking deadlines to prevent penalties.

Tax Obligations and DTAA Benefits for Singapore Companies

Corporate Tax Rate Structure

Entity structure choice drives tax efficiency:

| Structure | Base Rate | Surcharge | Cess | Effective Rate |

|---|---|---|---|---|

| Domestic Company (Section 115BAA) | 22% | 10% | 4% | ~25.17% |

| New Manufacturing (Section 115BAB) | 15% | 10% | 4% | ~17.16% |

| Foreign Company (Branch Office) | 40% | 2-5% | 4% | 41.6–43.68% |

The 17–18 percentage point differential between wholly-owned subsidiaries and branch offices makes the subsidiary structure clearly preferable for any operation generating taxable income in India.

India-Singapore DTAA: Key Benefits

The India-Singapore Double Taxation Avoidance Agreement (DTAA) directly reduces the tax burden on cross-border income flows:

- Dividends: Withholding tax capped at 15% (versus the standard 20% for non-treaty countries)

- Interest income: Reduced withholding at 15%, covering intercompany loans from the Singapore parent

- Royalties and fees for technical services: Capped at 15%, relevant for IP licensing and management charge arrangements

- Capital gains: Gains from shares in Indian companies may be taxed only in Singapore under the treaty, subject to anti-avoidance conditions (Limitation of Benefits clause applies)

- Permanent Establishment threshold: The treaty defines PE carefully — a Singapore company providing services in India for fewer than 90 days in a 12-month period generally avoids triggering a PE

Singapore companies should obtain a Tax Residency Certificate (TRC) from the Inland Revenue Authority of Singapore and submit Form 10F to Indian payers to claim reduced withholding rates at source.

GST Framework Complexity

Beyond direct corporate taxes, India's indirect tax regime adds another compliance layer. The Goods and Services Tax operates across five primary slabs:

- 0% (Nil): Essential goods (grains, milk, eggs)

- 5%: Necessities (sugar, tea, coffee, edible oils)

- 12%: Processed foods, mobile phones

- 18%: Most goods and services (standard rate)

- 28%: Luxury goods, automobiles, tobacco

Additional rates apply: 0.25% for rough diamonds, 1.5% for certain precious stones, 3% for gold and silver. A Compensation Cess sits on top of the 28% rate for tobacco, aerated drinks, and luxury vehicles.

Singapore businesses familiar with Singapore's single-rate 9% GST will find India's multi-rate structure significantly more complex, requiring robust accounting systems and expert local compliance support. Monthly and quarterly filings — reconciling GSTR-1, GSTR-3B, and books of accounts — are mandatory, and accurate input tax credit availment depends on timely, error-free reconciliation.

Transfer Pricing Rules and Documentation

Any financial transactions between the Singapore parent and Indian subsidiary — including service fees, royalties, management charges, and intercompany loans — fall under India's strict Transfer Pricing regulations under the Income Tax Act.

Documentation requirements include:

- Contemporaneous transfer pricing documentation demonstrating arm's length pricing

- FAR (Functions, Assets, Risks) analysis covering each intercompany transaction type

- Benchmarking against industry comparables using recognized databases

- Form 3CEB (Accountant's Report) filed annually when international transactions exceed specified thresholds

Transfer pricing audits in India carry significant adjustment risk — penalties can reach 200% of underpaid tax in cases of concealment. VJM Global prepares transfer pricing studies aligned with both Indian regulations and OECD guidelines, and manages Form 3CEB filings to reduce audit exposure.

High-Growth Sectors and Common Challenges to Watch Out For

Top Sectors for Singapore Investors

Technology/SaaS — India's active internet user base reached 958 million in 2025, with rural users accounting for 548 million (57%) and growing faster than urban users. This digital-first population creates strong opportunities for cloud software, productivity tools, and B2B platforms.

Fintech — India leads global fintech adoption with an 87% adoption rate, well above the 64% world average. Government initiatives covering digital payments, simplified account opening, and regulatory sandboxes make this sector especially accessible. 100% FDI permitted via automatic route.

Healthcare/Pharmaceuticals: India's growing middle class drives healthcare spending growth. Government initiatives including Ayushman Bharat (world's largest health insurance scheme) and medical device manufacturing incentives under PLI schemes create favorable conditions. 100% FDI permitted via automatic route for most healthcare services.

Renewable Energy: India targets 500 GW of non-fossil fuel capacity by 2030. As of March 2026, total capacity stands at 283.46 GW, leaving a 217 GW gap to be filled over the next four years. Solar capacity reached 150.26 GW and wind reached 56.09 GW. India now ranks 3rd globally in renewable energy installed capacity. 100% FDI permitted via automatic route.

Semiconductors — The Semicon India programme provides fiscal support of up to 50% of project cost for semiconductor fabs, display fabs, compound semiconductors, and OSAT/ATMP facilities. Five approved projects with cumulative investment of Rs 1.52 lakh crore (~US$18 billion) create supply chain opportunities for component suppliers, testing services, and specialized materials.

Common Challenges Singapore Companies Face

Regulatory complexity varies by state. Federal policies set the framework, but each state applies labor laws, tax incentives, and industrial policies differently. Maharashtra, Karnataka, and Tamil Nadu are generally more business-friendly — local expertise is essential before choosing where to set up.

Talent attrition remains a real cost. IT sector attrition declined to 15.1% in 2024 (down from 19.3% in 2023), but still runs high by Singapore standards. Bengaluru, Mumbai, and Hyderabad face intense competition for skilled talent, pushing up compensation. Build retention strategies from day one: clear career paths, competitive pay, and a strong workplace culture.

Business culture moves at a different pace. Indian negotiations prioritize relationship-building, operate through hierarchical decision structures, and involve longer sales cycles than Singapore companies typically expect. Those who invest in face-to-face meetings and demonstrate long-term commitment consistently outperform those taking a purely transactional approach.

Risk Mitigation Strategy

Three practices consistently reduce market-entry risk for Singapore companies:

- Start lean via PEO. VJM Global's PEO services let you hire Indian employees and test product-market fit without the overhead of incorporating a subsidiary — validate the market before committing to permanent infrastructure.

- Vet Joint Venture partners carefully. VJM Global's partner evaluation covers financial analysis, credit rating assessment, and operational capability review to confirm strategic alignment before you commit.

- Bring in local advisors from day one. Going it alone commonly leads to delayed incorporation, missed RBI reporting deadlines, GST errors, and transfer pricing gaps — all of which attract penalties. VJM Global's 30+ years supporting 500+ American, 250+ UK, and 250+ Australian businesses entering India provides proven frameworks for efficient, compliant expansion.

Frequently Asked Questions

How to increase business in India?

Leverage digital channels (India has 958 million internet users) and localize pricing for regional markets rather than applying Singapore models directly. Building local partnerships is equally important — India's relationship-driven business culture means established Indian partners provide credibility that purely digital approaches cannot replicate.

Which business is most growing in India?

Technology/SaaS, fintech (87% adoption rate leading globally), e-commerce, healthcare/pharmaceuticals, and renewable energy currently demonstrate the fastest growth. These sectors benefit from government PLI incentives, a digitally active youth population exceeding 500 million, and rising consumer spending driven by middle-class expansion.

Which industry will boom in 2026 in India?

Semiconductors will see explosive growth with government subsidies covering up to 50% of project costs under the ₹76,000 crore Semicon India programme. Electric vehicles will accelerate under the PM E-DRIVE scheme (₹10,900 crore outlay). Green energy — particularly solar and wind — will expand rapidly to close the 217 GW gap between current 283 GW capacity and the 500 GW 2030 target.

Can a Singapore company own 100% of an Indian subsidiary?

Yes, 100% FDI is permitted under the automatic route in most sectors — no local Indian partner required. Exceptions include multi-brand retail (51% cap), certain media sectors, and brownfield pharmaceuticals above 74% (government approval required). Singapore entities must also file FC-GPR with RBI within 30 days of receiving FDI funds.

What is the DTAA benefit between India and Singapore?

The India-Singapore Double Taxation Avoidance Agreement prevents the same income from being taxed in both countries. Key benefits include reduced withholding tax rates: dividends at 10-15% versus domestic 20%, interest at 10-15% versus domestic 5-20%, and royalties/technical fees at 10% versus domestic 20%. This materially improves repatriation economics for qualifying Singapore-resident companies.

How long does it take to register a company in India from Singapore?

Incorporation through the MCA's SPICe+ process takes 2-4 weeks with accurate documentation. Post-incorporation steps (PAN, TAN, GST registration, bank account) add another 2-4 weeks, making 4-8 weeks the realistic timeline for full operational readiness. VJM Global typically achieves incorporation in 13-15 days through proactive MCA liaison.

Singapore companies enter India with real structural advantages: DTAA treaty benefits, established FDI corridors, cultural affinity, and geographic proximity. The economic case is concrete — 6.6% GDP growth, middle-class expansion to 80% of households by 2030, and USD 21 billion in government incentives across strategic sectors.

Navigating India's regulatory complexity requires expert guidance from the outset. VJM Global brings 30+ years of experience, a 95% client retention rate, and a dedicated team of chartered accountants and business setup professionals supporting Singapore companies from entity structure selection through ongoing compliance. Contact VJM Global at info@vjmglobal.com or +91 98915 76441 to begin your India expansion.