Introduction

Singapore ranks as India's #1 FDI source country, contributing USD 14.9 billion (29.87% share) of India's total FDI equity inflows in FY2024-25. The bilateral relationship is anchored by the Comprehensive Economic Cooperation Agreement (CECA) and a robust Double Taxation Avoidance Agreement (DTAA), creating a regulatory and tax framework that structurally favors Singapore capital over competitors.

For Singapore-based companies, entrepreneurs, and investors evaluating India as their next growth market in 2025-26, this is a genuine structural advantage. Capturing it requires navigating India's FDI entry routes, business structures, and compliance requirements correctly from the start.

Many Singapore investors run into the same preventable problems:

- Delayed regulatory approvals that stall market entry timelines

- FEMA penalty exposure from missed or incorrect filing deadlines

- Costly restructuring after choosing the wrong entry structure upfront

This guide explains what an FDI entry strategy involves, which routes and structures apply to Singapore investors, and what to plan for before committing capital.

Key Takeaways

- 100% FDI is permitted under the automatic route across most sectors, including IT, manufacturing, e-commerce, renewables, and infrastructure — no prior government approval needed

- Singapore investors gain measurable tax advantages through the India-Singapore DTAA (10-15% dividend withholding vs. 20% standard rate) and streamlined market access via CECA

- Two primary FDI routes exist: Automatic Route (no approval needed) and Government Route (ministry clearance required for sensitive sectors like defence beyond 74% and media)

- Each entry structure (Wholly Owned Subsidiary, Joint Venture, Branch Office, Liaison Office) carries distinct legal, tax, and operational trade-offs that affect long-term scalability

- Full market entry from incorporation to operational readiness spans 12–18 months across multiple Indian regulatory bodies

Why Singapore Investors Are Choosing India

The Bilateral Advantage: CECA and DTAA

The India-Singapore relationship is built on two foundational agreements that create preferential conditions for capital flows. The Comprehensive Economic Cooperation Agreement (CECA), in force since 2005, was India's first comprehensive economic pact with a South Asian partner. It covers trade in goods, services, investment protection, and movement of professionals — reducing friction for Singapore companies establishing Indian operations.

The Double Taxation Avoidance Agreement (DTAA) delivers concrete tax benefits. Under Article 10, dividends paid from an Indian subsidiary to a Singapore parent are taxed at:

- 10% if the beneficial owner holds at least 25% of shares

- 15% in all other cases

India's standard withholding tax on dividends to non-residents is 20%, meaning the DTAA provides a 5–10 percentage point saving. The Third Protocol (December 2016) removed capital gains exemptions for shares acquired after April 1, 2017, aligning Singapore with Mauritius. Dividend benefits remain intact, provided investors meet Limitation of Benefits (LOB) conditions — specifically, a minimum SGD 200,000 annual expenditure in Singapore.

Non-Land-Border Status: Automatic Route Access

Singapore's geographic position delivers a second structural advantage. Under Press Note 3 (2020) and Press Note 2 (2026), FDI from countries sharing a land border with India — China, Pakistan, Bangladesh, Myanmar, Nepal, Bhutan, Afghanistan — requires mandatory Government Route approval regardless of sector. Singapore investors are exempt from this restriction and qualify for the Automatic Route in all eligible sectors, accelerating entry timelines and reducing bureaucratic exposure.

Demand-Side Pull: India's USD 4.3 Trillion Consumer Market

India's GDP grew 6.5% in FY2024-25, confirmed by both the IMF and India's Press Information Bureau. Consumer spending is projected to reach USD 4.3 trillion by 2030 (up 46% from USD 2.4 trillion in 2024), with the middle class driving 53% of incremental consumption. For Singapore companies with strengths in fintech, electronics manufacturing, renewable energy, and logistics, this growth curve translates directly into addressable market opportunity.

The Production-Linked Incentive (PLI) scheme for Large Scale Electronics Manufacturing illustrates how quickly this is converting into industrial scale:

- Attracted INR 17,519 crore in investment — 250% of the original target

- Created 1.85 lakh direct jobs since launch

- Smartphones became India's top exported commodity in CY 2025, valued at INR 2.62 lakh crore

- Sectors including electronics, solar PV, and specialty chemicals carry active PLI windows

Singapore investors in electronics and renewables should assess PLI eligibility as part of the initial market-entry evaluation.

FDI Entry Routes in India: What Singapore Investors Need to Know

Automatic Route vs. Government Route

India's FDI framework operates on two pathways defined by sector and ownership percentage:

Automatic Route: Investment proceeds subject to FEMA compliance and RBI reporting only. No prior government approval required. Singapore investors file post-investment notifications (Form FC-GPR within 30 days of share allotment) but do not wait for ministry clearance before transferring capital.

Government Route: Prior approval required through the Department for Promotion of Industry and Internal Trade (DPIIT) via the Foreign Investment Facilitation Portal (fifp.gov.in). Approval timelines vary but typically add 8-12 weeks to the entry process.

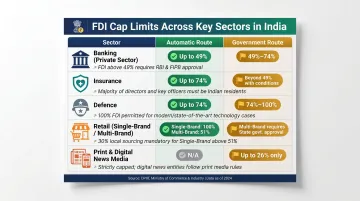

Sector-Specific FDI Caps and Routes

100% FDI Under Automatic Route (No Approval Required):

- Manufacturing, IT services, computer software & hardware

- E-commerce (B2B/wholesale model only)

- Renewable energy and infrastructure

- Industrial parks and townships

- Telecom services

- Coal and mineral mining

- Airports (greenfield and brownfield)

- Railway infrastructure

FDI Caps and Government Route Requirements:

| Sector | FDI Cap | Route | Notes |

|---|---|---|---|

| Banking (Private Sector) | 74% | Automatic up to 49%; Government beyond 49% | -- |

| Insurance | 74% | Automatic | Raised from 49% in 2021 |

| Defence | 100% | Automatic up to 74%; Government beyond 74% | Government route where modern technology access involved |

| Single/Multi-Brand Retail | 100%/51% | Government | Subject to local sourcing and other conditions |

| Print/Digital News Media | 26% | Government | -- |

Prohibited Sectors (FDI Not Permitted):

- Lottery, gambling, betting (including casinos)

- Chit funds and Nidhi companies

- Real estate speculation and farmhouse construction

- Tobacco manufacturing

- Atomic energy and railway operations (except metro rail)

Business Structures: Choosing the Right Entry Vehicle

Once you've confirmed your sector's FDI route, the next decision is which legal structure to establish in India. Each option carries distinct regulatory, operational, and tax implications.

Wholly Owned Subsidiary (WOS) — Private Limited Company

The most practical starting structure for Singapore investors seeking full control and profit repatriation. Incorporated under the Companies Act 2013 with the Singapore parent holding 100% share capital.

Key advantages:

- Full operational and financial control

- Perpetual legal existence

- Eligibility for all sectoral FDI benefits

- Straightforward dividend repatriation under RBI guidelines

- Limited liability protection

When to use: Long-term market commitment, revenue generation in India, need for an independent legal entity.

Joint Venture (JV)

A partnership structure where the Singapore investor holds equity alongside an Indian partner. Suitable when local market knowledge, distribution networks, or regulatory navigation require domestic participation.

Critical considerations:

- Thorough partner due diligence (financial, legal, reputational)

- Explicit governance and exit clauses in shareholders' agreement

- IP protection mechanisms and profit-sharing alignment

When to use: Sectors requiring local partnerships, access to established distribution, or shared capital investment.

Branch Office

Established under FEMA 1999 with RBI approval. Permitted activities are restricted to:

- Export/import operations

- Professional or consultancy services

- Research in the parent company's field

- IT services and software development

- Technical support for parent/group products

Cannot engage in manufacturing or retail. Ongoing RBI reporting requirements apply.

When to use: Service delivery or project execution without full subsidiary commitment.

Liaison Office

Strictly for market exploration and relationship building. Cannot generate any revenue in India. All expenses must be funded through inward remittances from the head office. Validity is limited to 3 years (extendable). Applications from China, Pakistan, Bangladesh, and other sensitive jurisdictions require additional government consultation.

When to use: Pre-entry market research only.

For most first-time Singapore investors, a Private Limited Company (WOS) offers the best balance of control, tax efficiency, and scalability. VJM Global's India entry team handles company formation, structure advisory, and full regulatory compliance for investors at this stage.

How to Register Your FDI in India: Step-by-Step

For Singapore investors, registering FDI in India involves four distinct phases spanning multiple regulatory authorities. The full process — from incorporation to operational readiness — typically takes 12–18 months and is best treated as a phased compliance plan, not a single event.

Step 1: Incorporate the Indian Entity (2-4 Weeks)

Registration occurs through the Ministry of Corporate Affairs (MCA) using the SPICe+ (Simplified Proforma for Incorporating Company Electronically Plus) integrated system.

Required steps:

- Obtain Digital Signature Certificates (DSC) for proposed directors

- Apply for Director Identification Numbers (DIN) — integrated within SPICe+

- Name reservation via SPICe+ Part A (RUN — Reserve Unique Name)

- File SPICe+ Part B with Memorandum and Articles of Association

- SPICe+ consolidates PAN, TAN, EPFO, ESIC, and bank account opening in one form

VJM Global manages the full incorporation process for foreign clients — DIN, DSC, name reservation, MoA/AoA filing, and Certificate of Incorporation — within the 2-4 week window.

Step 2: Open Bank Account and Transfer Capital (4-6 Weeks)

Key requirements:

- Open an account with an AD Category-I bank (RBI-authorised dealer for foreign exchange transactions)

- Transfer share subscription funds from Singapore through formal banking channels

- Price shares in line with RBI's FDI valuation guidelines

- Allot shares within 60 days of receiving funds — missing this window creates downstream FEMA exposure

Step 3: File RBI Compliance Reports (Critical 30-Day Window)

Form FC-GPR (Foreign Currency - Gross Provisional Return): Must be filed within 30 days of share allotment via RBI's FIRMS portal. Supporting documents include board resolution, FIRC (Foreign Inward Remittance Certificate), investor KYC, and valuation certificate.

Form FC-TRS (Foreign Currency - Transfer of Shares): Filed within 60 days when shares transfer between resident and non-resident.

FEMA Penalty Exposure: Delayed FC-GPR filing attracts compounding penalties ranging from INR 10,000 to INR 5 lakh depending on delay length. Under FEMA Section 13, penalties can reach three times the transaction value or INR 2 lakh, whichever is higher. Compounding applications require a non-refundable INR 5,000 fee and typically resolve within 180 days.

FC-GPR non-compliance is the single most common failure point for first-time foreign investors in India. Missing the 30-day deadline compounds quickly — both financially and in terms of RBI relationship. VJM Global handles FC-GPR and FC-TRS filing as part of post-incorporation compliance, ensuring the deadline is met.

Step 4: Complete Statutory Registrations for Operations

Mandatory registrations before commencing operations:

- GST registration: Required if aggregate turnover exceeds INR 20 lakh (INR 10 lakh in special category states); mandatory for interstate supply regardless of turnover

- PAN and TAN: Tax identification numbers for the entity

- EPFO registration: Employee provident fund (if hiring employees)

- State-specific licenses: Trade licenses, factory registrations, professional tax registration

- Sector-specific approvals: FSSAI for food, BIS for electronics, financial services licenses for fintech

Requirements vary significantly by state. Gujarat, Tamil Nadu, Maharashtra, and Telangana each maintain distinct industrial policies, incentive schemes, and licensing frameworks — the right state choice can meaningfully affect your cost structure and approval timelines. VJM Global's India entry service covers state selection advisory, GST registration, PAN/TAN, and sector-specific license applications.

Key Factors That Shape Your India FDI Strategy

DTAA Advantage: Quantifying the Tax Benefit

The India-Singapore DTAA's 10-15% dividend withholding rate versus India's standard 20% rate translates to meaningful savings at scale. For a Singapore parent receiving INR 10 crore in annual dividends, the DTAA saves INR 50 lakh to INR 1 crore annually (depending on shareholding percentage).

Critical compliance requirements:

- Obtain Tax Residency Certificate (TRC) from Singapore tax authorities

- File Form 10F with Indian tax authorities

- Meet LOB substance test: SGD 200,000 minimum annual expenditure in Singapore

- Maintain documentation proving genuine Singapore operations, not shell entity

Sector Selection and FDI Caps

FDI caps vary significantly by sector — financial services investors face different constraints than manufacturing or retail entrants. Key sectors with partial caps include:

- Insurance: 74% FDI permitted under automatic route

- Private sector banking: 74% under automatic route; beyond 49% requires RBI approval

- Defense manufacturing: 74% automatic route; beyond that requires government approval

- Multi-brand retail: 51% with government route and strict local sourcing conditions

DPIIT's Consolidated FDI Policy Circular 2020 covers all current sectoral limits — confirm your specific cap and route before finalizing structure.

State-Level Variation: Where to Incorporate Matters

India is not a uniform regulatory market. State choice determines incentive access, compliance complexity, and operational costs. Three states illustrate the range of options available to Singapore investors:

Gujarat — GIFT City IFSC: For financial services, GIFT City offers:

- 100% income tax exemption for 10 consecutive years out of 15

- No Securities Transaction Tax (STT) or stamp duty on IFSC transactions

- Reduced Minimum Alternate Tax (MAT) at 9% vs. standard 15%

- Unified regulator (IFSCA) collapsing RBI, SEBI, IRDAI, PFRDA into one window

Tamil Nadu — Electronics Manufacturing Hub: Foxconn invested approximately INR 150 billion (USD 1.69 billion) in Tamil Nadu for AI-led electronics manufacturing. The state's established supply chains and direct PLI scheme participation make it ideal for electronics and hardware companies.

Telangana — Life Sciences Policy 2026-2030: Targets USD 25 billion investment and 5 lakh jobs. Features include 10 pharma villages (1,000-3,000 acres each), Clinical Innovation Sandbox, 24x7 operations in designated parks, and a consultation committee to simplify clearances.

Post-Investment Compliance Obligations

Once structure and location are set, compliance obligations begin immediately. FDI registration is not a one-time event — ongoing requirements include:

- Annual RBI filings: Annual Return on Foreign Liabilities and Assets (FLA Return)

- Statutory audits: Mandatory under Companies Act 2013

- GST return filings: Monthly/quarterly depending on turnover

- Transfer pricing documentation: For related-party transactions between Indian subsidiary and Singapore parent (Sections 92-92F of Income Tax Act)

- FEMA compliance for repatriation: Dividend repatriation is freely permitted under RBI guidelines but requires proper documentation

VJM Global supports Singapore investors across all four areas — DTAA treaty compliance, sector cap analysis, state selection, and post-incorporation filings — as part of a single India entry engagement.

Common Mistakes Singapore Investors Make When Entering India

Choosing the Wrong Entry Structure for Short-Term Cost Savings

Many Singapore companies opt for a Liaison Office or Branch Office to avoid incorporation complexity, then discover these structures cannot generate revenue or scale without costly restructuring. A Liaison Office cannot earn any income in India. A Branch Office is restricted to specific service activities and cannot engage in manufacturing or retail.

The hidden cost: Converting from Liaison/Branch to WOS requires:

- Closing the original entity with RBI approval

- Full incorporation process for new WOS

- Capital repatriation and re-injection

- 6-12 months of regulatory downtime

If your market entry plan includes revenue generation within 18-24 months, start with a WOS. Based on restructuring cases handled across first-time entrants, a Wholly Owned Subsidiary almost always proves more cost-effective from day one than converting later.

Ignoring State-Level Regulatory Differences

Investors who treat India as a single regulatory environment face unexpected licensing delays and higher compliance costs. A manufacturing company incorporated in one state may wait 6-8 months for factory approvals that would take 2-3 months in another state with dedicated single-window clearance.

Due diligence must go beyond national FDI policy. State-level review should cover:

- Industrial policy and sector-specific incentives

- Single-window clearance availability and average timelines

- Infrastructure maturity relevant to your operations

- Labor law enforcement and compliance environment

VJM Global's location analysis compares these factors across states before recommending an incorporation jurisdiction.

Underestimating Post-Incorporation Compliance Complexity

The 60-day share allotment deadline followed by the 30-day FC-GPR window creates a 90-day critical compliance path from fund receipt to RBI reporting. Missing these deadlines triggers FEMA penalties and signals broader compliance gaps that can attract Directorate of Enforcement scrutiny.

Most Singapore investors lack in-house India compliance expertise, and filings slip. VJM Global handles FC-GPR, FC-TRS, and ongoing RBI reporting as standard post-incorporation services — so deadlines are met and penalties are avoided.

Frequently Asked Questions

Can Singapore companies invest in India under the automatic FDI route?

Yes. Singapore investors qualify for the automatic route in most sectors because Singapore is not a land-border country with India. Investments proceed subject to FEMA compliance and post-investment RBI reporting (Form FC-GPR), with no prior government approval required.

What is the India-Singapore DTAA and how does it benefit investors?

The India-Singapore Double Taxation Avoidance Agreement prevents double taxation on income earned in India by Singapore residents. Key benefits include reduced withholding tax on dividends (10-15% vs. the standard 20% rate) and favorable capital gains provisions — both subject to Limitation of Benefits (LoB) conditions.

How long does it take to incorporate a company in India as a Singapore investor?

Company incorporation through MCA takes approximately 2-4 weeks. Full operational readiness including RBI reporting, GST registration, and sector-specific licenses typically takes 12-18 months.

Which business structure is best for a Singapore company entering India for the first time?

A Private Limited Company (Wholly Owned Subsidiary) is the most practical choice for Singapore investors seeking full control, scalability, and profit repatriation eligibility. Joint Ventures are suited when local partnerships are strategically necessary for market access or regulatory navigation.

Which sectors offer the most FDI opportunity for Singapore investors in India?

High-opportunity sectors where 100% automatic route FDI is permitted include technology, financial services, manufacturing, renewable energy, and logistics. Singapore companies in electronics manufacturing should evaluate PLI scheme eligibility. Always confirm current DPIIT sectoral caps before finalizing your entry structure.

Is it mandatory to have a local Indian partner to invest in India from Singapore?

No. A local partner is not required in most sectors where 100% FDI is permitted under the automatic route. Strategic partners can accelerate market access, distribution reach, and regulatory navigation in certain industries, but are not legally mandatory for entry.

Ready to enter the Indian market? VJM Global supports Singapore investors at every stage of India market entry — from FDI route selection and company incorporation to ongoing compliance, transfer pricing documentation, and DTAA optimization. With 30+ years serving international clients across the USA, UK, Australia, and Asia-Pacific, VJM Global helps you enter India with the right structure in place.

Contact VJM Global:

📧 info@vjmglobal.com

📞 +91 9213397070 | +91 9891576441

🏢 Corporate Office: 601, 6th Floor, GMIT Park, Sector 142, Noida Expressway, Noida – 201305