Introduction

India is the world's fastest-growing major economy — and Singapore entrepreneurs are increasingly first in line to benefit. GDP grew 7.4% in FY2025-26 (Ministry of Statistics' First Advance Estimate), while FDI hit $81.04 billion in FY2024-25, a 14% year-on-year increase and a three-year high.

The India-Singapore corridor is particularly active. Singapore contributed $14.94 billion in FY2024-25, making it India's top FDI source country. Bilateral trade under the Comprehensive Economic Cooperation Agreement (CECA) grew from $6.7 billion in FY2004-05 to $35.6 billion in FY2023-24, driven by geographic proximity, established trade ties, and aligned economic priorities.

That trade corridor is now drawing entrepreneurs from across the spectrum: established SME owners expanding regionally, NRIs and OCIs reconnecting with the Indian market, and investors targeting opportunities in technology services, fintech, manufacturing, and logistics.

The consumer opportunity is substantial. By 2036, middle class and affluent consumers will account for 93% of all spending, with 499 "consumer cities" projected by 2035, most of them outside India's five largest metros.

This guide covers what Singapore entrepreneurs need to act on: choosing the right business structure, understanding FDI routes, completing registration, and staying compliant once operations begin.

Key Takeaways

- Singapore citizens can legally start a business in India, primarily through a Private Limited Company or LLP structure

- India's FDI policy allows 100% foreign ownership in most sectors under the automatic route — no prior government approval needed

- Setup requires choosing a business structure, completing MCA registration, and obtaining PAN, TAN, GST, and FEMA compliance clearances

- Ongoing obligations include GST filings, annual MCA returns, and RBI reporting — all mandatory for foreign-owned entities

- Partnering with an India-based firm like VJM Global cuts setup time and keeps you compliant from day one

Why Singapore Entrepreneurs Are Entering the Indian Market

For Singapore entrepreneurs, "entering the Indian market" means incorporating an Indian legal entity — not operating remotely from Singapore. This typically involves registering a Private Limited Company or LLP to conduct business, hire staff, sign contracts, and serve Indian customers legally.

Singapore's Position as Top FDI Source

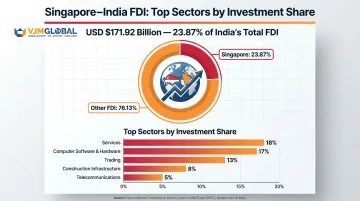

The numbers demonstrate a well-established investment corridor. Singapore contributed USD $171.92 billion in cumulative FDI to India (January 2000 to December 2024), representing 23.87% of India's total FDI and ranking second overall. Top sectors for Singapore FDI include Services (18%), Computer Software & Hardware (17%), Trading (13%), Construction Infrastructure (8%), and Telecommunications (5%).

Strategic Advantages for Singapore Entrepreneurs

Several factors make India strategically compelling from Singapore:

- CECA framework benefits — The Comprehensive Economic Cooperation Agreement reduces trade barriers and facilitates investment flows

- Geographic proximity — Time zone overlap and direct connectivity enable efficient coordination between Singapore HQ and Indian operations

- Large, fast-growing consumer base — India's consumer market is expanding beyond metros, with 93% of urban consumer growth through 2040 occurring outside the five largest cities

- Fintech growth trajectory — The sector is projected to grow from $51.3 billion (2026) to $109 billion by 2031 at a 16.27% CAGR

- E-commerce expansion — The market is expected to reach ~$380 billion by 2032, up from ~$125 billion in 2024 (14.9% CAGR)

- Comparatively low operating costs — Labour costs, office space, and operational expenses are substantially lower than Singapore, improving unit economics

Regulatory Complexity Requires Planning

India's market potential is significant, but the regulatory environment is more complex than Singapore's. Compliance layers vary by sector and state, timelines are longer, and setup requires careful planning. Singapore entrepreneurs who succeed here invest in proper legal setup, realistic timelines, and ongoing compliance from day one. Without that groundwork, the opportunity rarely delivers.

What Singapore Entrepreneurs Should Know Before Starting

India operates differently from Singapore's regulatory environment. Setting realistic expectations upfront helps Singapore entrepreneurs plan properly and avoid costly mistakes.

Three Critical Realities for Singapore Entrepreneurs

1. Plan for a 4–8 Week Incorporation Timeline

Company incorporation in India takes 4 to 8 weeks for foreign nationals, compared to approximately 2 weeks for domestic founders. The timeline includes:

| Phase | Activity | Timeline |

|---|---|---|

| Phase 1 | Digital Signature Certificate (DSC) and Director Identification Number (DIN) | 7-10 days |

| Phase 2 | Name approval via RUN service | 3-5 days |

| Phase 3 | SPICe+ filing and Certificate of Incorporation | 10-15 days |

| Phase 4 | RBI & FEMA compliance (post-incorporation) | Ongoing |

The longer timeline is primarily due to apostille and document validation requirements for documents originating outside India. All identity and address proof documents of foreign directors must be notarised by a Public Notary and apostilled (or consularised) in the director's country of residence.

2. Expect Hands-On Oversight Early On

In the early stages, decisions about local hiring, banking, and compliance often require founder oversight from Singapore. This creates real coordination challenges across time zones and jurisdictions.

Many successful Singapore entrepreneurs address this by appointing a trusted local team member early — or partnering with an India-based compliance firm like VJM Global to manage documentation and regulatory coordination.

3. Set Realistic Revenue Expectations

B2B services, tech products, and manufacturing tend to have longer sales cycles in India. Early-stage income should not be expected within the first 1–2 quarters without a local team and pipeline already in place. Indian buyer behaviour differs from Singapore — relationship-building, local references, and a local presence significantly impact deal closure timelines.

Beyond these operational realities, there's one structural limitation that catches many foreign founders off guard.

One Person Company Structure Unavailable to Foreign Nationals

A common misconception among foreign entrepreneurs is eligibility for India's One Person Company (OPC) structure. Foreign nationals, including Singapore citizens, cannot form an OPC in India. Only Indian citizens who are also residents of India (having stayed in India for at least 120 days during the immediately preceding financial year) can use this structure.

The most practical options for Singapore entrepreneurs are:

- Private Limited Company — the most common choice; allows 100% foreign ownership in most sectors and supports future fundraising

- Limited Liability Partnership (LLP) — suitable for professional services or joint ventures with an Indian partner

- Branch or Liaison Office — appropriate for companies that want a presence in India before committing to full incorporation

Choosing the Right Business Structure as a Foreign Investor

The choice of business structure affects tax rates, liability protection, FDI eligibility, fundraising ability, and ongoing compliance burden.

Sole Proprietorship and Partnership Firm

These structures are generally unsuitable for Singapore entrepreneurs. They do not offer limited liability protection, cannot easily accommodate foreign ownership, and are not recognised as separate legal entities. They also complicate repatriation of profits and create personal liability exposure.

Limited Liability Partnership (LLP)

An LLP is a valid option for foreign nationals under specific conditions:

Requirements:

- At least two designated partners, with at least one Indian resident

- FDI in LLPs permitted only in sectors where 100% FDI is allowed under the automatic route with no FDI-linked performance conditions

- Offers limited liability protection to all partners

When to Choose an LLP:

- Professional services or consulting businesses

- Smaller ventures prioritising operational flexibility over fundraising

- Businesses seeking lower compliance costs than a Private Limited Company

One hard constraint: LLPs cannot issue equity instruments to investors, which rules them out for any startup planning to raise venture capital or institutional funding.

Private Limited Company (Pvt Ltd)

For Singapore entrepreneurs, a Private Limited Company is the right default — it combines full foreign ownership, fundraising capability, and limited liability in a single structure.

Key Advantages:

- Separate legal entity with limited liability

- Allows 100% foreign ownership under the FDI automatic route in most sectors

- Can issue equity shares to raise institutional capital

- Continues operating through ownership transfers or director changes

- Eligible for government tenders, bank loans, and investor term sheets

Requirements:

- Minimum two directors (at least one must be an Indian resident — someone who has stayed in India for 182+ days in the preceding financial year)

- Minimum two shareholders (can be individuals or entities, foreign or Indian)

- No minimum paid-up capital requirement (removed by Companies Amendment Act 2015)

- Foreign directors must obtain Director Identification Number (DIN) and Class 3 Digital Signature Certificate (DSC)

Once you've settled on a Pvt Ltd structure, the next question is which FDI route applies to your sector.

FDI Automatic Route vs. Government Approval Route

Automatic Route: No prior approval from the Indian government or Reserve Bank of India (RBI) is needed to invest. This applies to over 90% of India's sectors, including:

| Sector | FDI Cap | Route |

|---|---|---|

| IT and Software | 100% | Automatic |

| Manufacturing | 100% | Automatic |

| E-commerce (Marketplace Model) | 100% | Automatic |

| Professional Services | 100% | Automatic |

| Logistics | 100% | Automatic |

Government Approval Route: Required for sensitive sectors including:

- Defence: 100% allowed, but government approval required beyond 74%

- Multi-Brand Retail: 51% cap, government approval required

- Print Media (news & current affairs): 26% cap, government approval required

- Private Banking: 74% cap, with government approval for 49-74% bracket

Prohibited Sectors: Lottery, gambling/betting, chit funds, real estate dealing, tobacco manufacturing, inventory-based e-commerce, and atomic energy.

Key Registration Documents Required

Singapore entrepreneurs need to prepare:

For Directors:

- Passport copy (notarised and apostilled)

- Address proof not older than 2 months (utility bill or bank statement, notarised and apostilled)

- Digital Signature Certificate (DSC)

- Director Identification Number (DIN)

- Passport-sized photograph

For the Company:

- Proof of Indian registered office address (utility bill not older than 2 months)

- If premises are rented: rent agreement and No Objection Certificate (NOC) from landlord

- Memorandum of Association (MoA) and Articles of Association (AoA)

- Declaration and affidavits from directors

Apostille is mandatory. The process authenticates Singapore-issued documents for use in India. Documents not in English need a certified translation. Photocopies without proper authentication are rejected by the Registrar of Companies.

How to Start a Small Business in India: A Step-by-Step Guide

Skipping steps — especially compliance steps — creates costly problems later. Here's the practical execution path from validation to launch.

Step 1 – Research the Market and Define Your Opportunity

Identify the specific problem your business solves in the Indian market and who the paying customer is. Indian consumer behaviour and B2B buying patterns differ significantly from Singapore.

Key Questions:

- Who is your target customer segment in India (geography, industry, size)?

- What pain point are you solving that Indian competitors are not?

- What is the competitive landscape in your target segment?

- Are there regulatory or sector-specific requirements that affect go-to-market?

Conduct primary research (customer interviews, pilot projects) or secondary research (industry reports, market studies) on the target segment before committing to a structure or budget.

Step 2 – Validate Demand and Pricing Viability

Test willingness to pay, not just interest. Pricing that works in Singapore may need recalibration for Indian market realities.

Pricing Considerations:

- Labour costs are substantially lower in India, but customer price sensitivity varies widely by segment

- B2B enterprise customers expect localised pricing, payment terms (30-90 days are common), and Indian invoicing

- B2C customers are highly price-sensitive; premium positioning requires strong brand differentiation

- Validate that unit economics can support sustainable margins at Indian price points

Run pricing experiments or pilot contracts before finalising your business model.

Step 3 – Decide on Your Entry Route and Business Model

Determine whether you will serve India through:

- Wholly-owned Indian subsidiary (most common for Singapore entrepreneurs)

- Joint venture with a local partner (useful in regulated sectors or for local market access)

- LLP structure (for professional services without fundraising needs)

Also decide whether the business model is product-led, service-led, or hybrid. The entry route affects:

- Tax treatment and effective tax rate

- Profit repatriation mechanics and timeline

- Ongoing compliance burden

- Ability to raise capital from Indian or international investors

Step 4 – Incorporate the Company and Complete Legal Setup

The company registration process occurs through India's Ministry of Corporate Affairs (MCA) using the SPICe+ (Simplified Proforma for Incorporating Company Electronically Plus) system.

Standard Incorporation Process:

- Obtain Digital Signature Certificate (DSC) for all directors (2 days)

- Obtain Director Identification Number (DIN) for all directors (1-2 days)

- Reserve company name via RUN (Reserve Unique Name) service (3-5 days)

- File SPICe+ incorporation documents including MoA and AoA (10-15 days)

- Receive Certificate of Incorporation (CoI) and auto-generated PAN (Permanent Account Number) and TAN (Tax Deduction and Collection Account Number)

Post-Incorporation: GST Registration

GST (Goods and Services Tax) registration is required if your annual turnover will exceed applicable thresholds:

| Category | Threshold | States |

|---|---|---|

| Goods suppliers | ₹40 lakh | Most states |

| Goods suppliers (special category states) | ₹20 lakh | Northeast states |

| Service providers | ₹20 lakh | Most states |

| Service providers (special category states) | ₹10 lakh | Northeast states |

Working with a Setup Partner

Singapore entrepreneurs should consider engaging a local compliance partner to manage the documentation and filing process accurately. VJM Global handles company setup for foreign entrepreneurs in India — from document apostille verification to SPICe+ filing, PAN/TAN generation, and GST registration. Working with a specialist reduces filing errors and frees up your time for the business itself.

Step 5 – Open a Business Bank Account and Set Up Financial Operations

A current account with an Indian bank is required to receive FDI remittances and operate the business.

Banking Requirements:

- Certificate of Incorporation

- PAN and TAN

- MoA and AoA

- Board resolution authorising bank account opening

- Identity and address proof of all directors (apostilled)

Critical FEMA Compliance: FC-GPR Filing

The first remittance from Singapore into the Indian company's account must be reported to the RBI under FEMA (Foreign Exchange Management Act) regulations.

Form FC-GPR (Foreign Currency - Gross Provisional Return) must be filed within 30 days of share allotment to foreign investors. This applies to equity shares, compulsorily convertible preference shares, convertible debentures, share warrants, or convertible notes.

Key Details:

- Filed by the Indian company (not the investor) on the RBI FIRMS portal

- Late submission attracts a minimum penalty of ₹7,500

- Details must exactly match the FIRC (Foreign Inward Remittance Certificate), KYC report, valuation certificate, board resolution, and share subscription documents

This is a non-negotiable compliance step that many first-time foreign entrepreneurs miss — resulting in penalties and compliance notices from the RBI.

Step 6 – Build Your Operations, Hire Locally, and Set Up Delivery

Decide what roles need to be filled locally in India versus what can be managed remotely from Singapore.

Recommended Local Hires:

- Operations manager or business head (critical for day-to-day execution)

- Accounts/finance person familiar with Indian GST and tax compliance

- Sales or customer success (for B2B businesses)

Hiring even one trusted local team member early improves execution speed and regulatory coordination. They also bring market knowledge that no amount of remote management replaces — vendor networks, buyer relationships, and an instinct for how things actually get done on the ground.

Step 7 – Launch and Build Market Presence

Define how customers will discover, evaluate, and engage with your business in India.

For B2B:

- Local referrals and introductions carry significant weight

- LinkedIn and industry-specific platforms (e.g., IndiaMART for manufacturing/trading)

- Trade associations and industry events

- Localised content marketing and case studies

For B2C:

- Digital channels dominate: Google Ads, Facebook/Instagram, SEO

- Marketplaces (Amazon India, Flipkart) for product businesses

- Influencer marketing and regional language content for mass market

Set up basic tracking (Google Analytics, CRM, conversion funnels) to understand which acquisition channels are working and iterate quickly.

Step 8 – Monitor Performance, Stay Compliant, and Stabilise Before Scaling

Track financials, customer feedback, and compliance deadlines consistently.

Key Metrics to Monitor:

- Monthly revenue and growth rate

- Customer acquisition cost (CAC) and lifetime value (LTV)

- Gross margin and operating expenses

- Cash runway and burn rate

- Compliance calendar adherence (GST filings, TDS deposits, ROC filings)

Fix operational gaps before expanding. Scaling into new Indian cities or segments with shaky unit economics or unresolved compliance issues will cost far more to unwind than to address now.

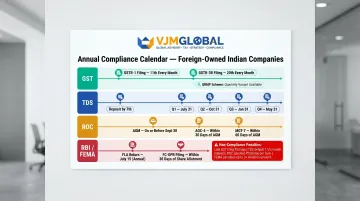

Ongoing Compliance Obligations for Foreign-Owned Businesses in India

Compliance obligations don't end at incorporation. Singapore entrepreneurs must actively manage multiple filings across different authorities on an ongoing basis.

GST Return Filing

| Return | Frequency (Turnover > ₹5 Crore) | Frequency (Turnover ≤ ₹5 Crore - QRMP) | Due Date |

|---|---|---|---|

| GSTR-1 (outward supplies) | Monthly | Quarterly | 11th of following month (monthly) / 13th of month after quarter (quarterly) |

| GSTR-3B (summary + tax payment) | Monthly | Quarterly | 20th of following month (monthly) / 22nd-24th of month after quarter (quarterly) |

QRMP (Quarterly Return Monthly Payment) Scheme: Available for businesses with aggregate annual turnover up to ₹5 crore. Even under QRMP, tax must be paid monthly via Form PMT-06 by the 25th of the following month.

TDS (Tax Deducted at Source) Compliance

TDS Deposit: By the 7th of the following month (except March, which is April 30)

TDS Quarterly Return Filing:

| Quarter | Period | Return Due Date |

|---|---|---|

| Q1 | April - June | July 31 |

| Q2 | July - September | October 31 |

| Q3 | October - December | January 31 |

| Q4 | January - March | May 31 (next FY) |

Forms include 24Q (salary TDS), 26Q (non-salary TDS), and 27Q (TDS on payments to non-residents).

ROC (Registrar of Companies) Annual Filings

| Filing | Form | Deadline |

|---|---|---|

| Annual General Meeting (AGM) | N/A | Within 6 months of FY end (September 30 for March FY-end companies) |

| Financial Statements | AOC-4 | Within 30 days of the AGM |

| Annual Return | MGT-7 / MGT-7A | Within 60 days of the AGM |

Non-compliance attracts additional fees of ₹100 per day of delay, plus potential legal consequences.

RBI/FEMA Reporting

Annual FLA Return (Foreign Liabilities and Assets):

- Mandatory for all Indian entities that have received FDI in any previous or current year

- Due date: July 15 each year

- Filed on the FLAIR portal (flair.rbi.org.in)

FC-GPR Filing:

- Required within 30 days of each share allotment to foreign investors

- Transaction-based filing, not annual

Why Compliance Matters

Unlike Singapore's relatively automated compliance environment, India requires active management of multiple filings across different authorities. Non-compliance carries real consequences:

- Late fees and daily penalties accumulating from the missed deadline

- Interest charges on unpaid tax obligations

- Legal notices from MCA, GSTN, or the Income Tax Department

- Complications in future fundraising rounds or business exits

Many Singapore entrepreneurs outsource India compliance entirely to a local specialist. VJM Global provides compliance support specifically for foreign-owned entities in India, covering:

- Bookkeeping and GST return filing

- TDS compliance and ROC annual filings

- Payroll management and RBI/FEMA reporting

This lets founders stay focused on growth rather than chasing filing deadlines.

Conclusion

Starting a small business in India as a Singapore entrepreneur is achievable, but it requires the right structure, a realistic timeline, and consistent compliance from day one.

The India-Singapore corridor is active and growing. Singapore's position as India's top FDI source country — supported by the CECA framework and sectoral demand in technology, fintech, services, and manufacturing — creates a real structural advantage for entrepreneurs making this move.

Capturing that opportunity comes down to three decisions you make early:

- Choose the right legal structure: Private Limited Company for most businesses, LLP for specific professional services

- Set realistic timelines: 4-8 weeks for incorporation, 3-6 months to initial revenue traction

- Build compliance infrastructure from day one: GST filings, TDS deposits, ROC filings, and RBI reporting are non-negotiable

Singapore entrepreneurs who get the legal and operational foundation right from the start will be far better positioned to scale. The businesses that struggle in India aren't usually underfunded — they're under-compliant. Treat your first ROC annual filing or GST reconciliation as a signal that your India operations are genuinely up and running.

Frequently Asked Questions

Frequently Asked Questions

How do I start a business in India?

Choose a business structure (Private Limited Company or LLP for foreign nationals), register via MCA's SPICe+ portal, obtain PAN/TAN and GST registration, open a business bank account, and report foreign investment to the RBI under FEMA within 30 days of share allotment.

Can a Singapore citizen start a business in India?

Yes, Singapore citizens can start a business in India — most commonly as a director/shareholder of a Private Limited Company under the FDI automatic route. At least one director must be an Indian resident, and the OPC (One Person Company) structure is not available to foreign nationals.

How do I open an IT company in India?

IT/software businesses qualify under 100% FDI via the automatic route and can be registered as a Private Limited Company. The process requires standard incorporation documents plus DSC, DIN, registered office address, and apostilled identity/address proofs for foreign directors.

What is the best business to start in India?

Sectors with strong FDI traction and market demand for Singapore entrepreneurs include technology services, fintech, education technology, logistics, and manufacturing. The best choice depends on your expertise and the specific market gap you're addressing.

Which businesses have the highest success rates in India?

Service-based businesses (IT, consulting, education, logistics) and digital-first ventures carry lower capital risk and faster validation cycles. Success rates rise sharply when founders secure local partnerships, hire Indian team members early, and build compliance infrastructure from day one.

Can I apply for the ₹20 lakh Startup India Seed Fund as a Singapore entrepreneur?

The Startup India Seed Fund Scheme (SISFS) provides up to ₹20 lakh as a grant for validation of proof-of-concept, prototype development, or product trials. However, foreign-majority entities are ineligible — the scheme requires 51% Indian promoter shareholding at the time of application. Foreign-owned startups should rely on private funding sources instead.