Introduction

Miss a single RBI filing deadline as a Singapore investor in India and you're looking at penalties up to three times your investment amount. Yet Singapore has poured USD 186.8 billion cumulatively into India, commanding a 34% share of total FDI inflows in H1 FY2025-26 — a scale that makes getting the compliance architecture right non-negotiable.

India's Foreign Exchange Management Act (FEMA) governs every stage of foreign investment, from entry route selection to post-transaction reporting.

Singapore investors benefit from bilateral treaties (the Comprehensive Economic Cooperation Agreement (CECA) and the Double Taxation Avoidance Agreement (DTAA)), but those advantages dissolve quickly when compliance gaps emerge. Incorrect share pricing or misclassification of business activities carries the same penalty exposure as missed filings.

This guide covers India's FDI regulatory architecture, including automatic versus government approval routes, sector-specific caps, mandatory reporting requirements, and recent policy changes. Each section is structured to answer the questions that typically arise at the deal-structuring stage — before capital is committed.

Key Takeaways

- Singapore ranks 1st among all FDI source countries, contributing USD 186.8 billion cumulatively to India

- India's FDI framework operates through Automatic Route (no prior approval) and Government Route (12-week standard timeline)

- Insurance sector opened to 100% FDI in December 2025; defence and brownfield pharma retain sector-specific caps

- All FDI requires Form FC-GPR filing within 30 days of share allotment; annual FLA returns due July 15

- Entity structure choice (subsidiary, LLP, or branch office) directly shapes tax treatment and compliance burden

Why Singapore Businesses Are Targeting India for FDI

Bilateral Investment Architecture and CECA Advantages

The India-Singapore CECA delivered USD 34.26 billion in bilateral trade in FY2024-25, making Singapore India's largest trading partner within ASEAN. This treaty framework extends beyond tariff preferences to investment promotion, creating a treaty foundation no other ASEAN source country matches.

The India-Singapore DTAA, as amended by the Third Protocol (2016), reduces withholding tax on:

- Dividends: 10-15% (depending on shareholding percentage)

- Interest: 10-15% (depending on financial institution type)

- Royalties and technical fees: 10%

Capital gains treatment shifted under the 2016 Protocol: shares acquired on or after April 1, 2017 are taxed in India at domestic rates. This eliminates Singapore's historic advantage as a tax-efficient holding jurisdiction, meaning investors must now factor Indian capital gains tax into exit modeling.

Singapore's cumulative FDI position—USD 186.8 billion from January 2000 to September 2025, overtaking Mauritius—reflects the structural advantage of this bilateral architecture. In FY2024-25, Singapore commanded a 30% share of India's total FDI equity inflows; in April-September 2025, that share rose to 34%.

India's Macroeconomic Fundamentals

India's gross FDI inflows crossed the USD 1 trillion milestone in December 2024, with FY2024-25 recording USD 81.04 billion, a 14% year-on-year increase. The IMF raised India's FY2025-26 GDP growth forecast to 6.6%, while India's own revised estimates place real GDP growth at 7.6% for the same period.

Three macroeconomic factors drive Singapore investor interest:

- Consumer market scale: An expanding middle class is generating demand across financial services, technology, consumer goods, and infrastructure — sectors that align directly with Singapore companies' strengths in fintech, logistics, and professional services.

- Digital economy growth: India Stack, UPI, and national digital identity infrastructure have created a platform for fintech innovation, making India a strategic fit for Singapore's technology and financial services firms.

- Workforce demographics: India's working-age population provides cost-efficient, skilled labor across IT, engineering, and back-office operations — positioning it as a natural destination for outsourcing and captive center operations.

Sectoral Concentration: Where Singapore Capital Flows

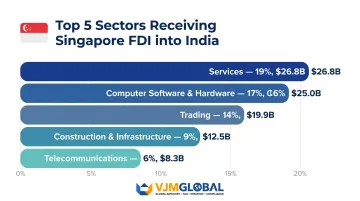

Based on DPIIT data from January 2000 to December 2022, the top five sectors attracting Singapore FDI equity into India are:

| Sector | Share of Singapore FDI | USD (Millions) |

|---|---|---|

| Services | 19% | 26,795 |

| Computer Software & Hardware | 17% | 25,035 |

| Trading | 14% | 19,915 |

| Construction (Infrastructure) | 9% | 12,453 |

| Telecommunications | 6% | 8,263 |

This sectoral distribution reflects Singapore's strengths in IT services, logistics, infrastructure development, and telecom: precisely the sectors where CECA trade facilitation and India's regulatory openness create the most favorable entry conditions.

India's FDI Routes: Automatic vs. Government Approval

Defining the Two Routes

India's Consolidated FDI Policy establishes two pathways:

Automatic Route: No prior approval from the Government of India or Reserve Bank of India (RBI) is required. The investor files post-transaction reports with the RBI and complies with sectoral conditions.

Government Approval Route: Prior approval from the relevant ministry is mandatory before the investment can proceed. Proposals are filed through the Foreign Investment Facilitation Portal (FIFP) and processed by the Department for Promotion of Industry and Internal Trade (DPIIT).

Which route applies depends on three factors:

- Sector of the investee company (e.g., defence, insurance, broadcasting)

- Percentage of equity being acquired (e.g., above 74% in defence requires government approval)

- Investor origin (e.g., investors from land-border countries require government approval regardless of sector)

Singapore investors typically fall under the Automatic Route in most sectors, bypassing the multi-month approval process. Singapore investors typically fall under the Automatic Route in most sectors, bypassing the multi-month approval process. That said, one significant exception can override this default — particularly relevant for Singapore entities with Chinese ownership.

Press Note 3 (2020): The Land-Border Country Restriction

Press Note 3 (2020), issued April 17, 2020, mandates government approval for any FDI from countries sharing a land border with India—China, Pakistan, Bangladesh, Nepal, Myanmar, Bhutan, and Afghanistan. This applies to both direct investments and cases where the beneficial owner is a citizen or entity of these countries.

Why this matters for Singapore investors: If a Singapore-incorporated entity has Chinese beneficial ownership, Press Note 3 applies, triggering the Government Route even for sectors otherwise open under the Automatic Route.

A 2026 revision introduces a 10% beneficial ownership threshold, allowing investments with less than 10% non-controlling ownership from land-border countries to potentially use the Automatic Route. As of March 2026, the RBI had not yet issued the final FEMA notification to implement this threshold. Singapore investors with Chinese minority shareholders should monitor this development closely.

Government Approval Process: FIFP Portal and Timeline

Proposals under the Government Route are filed through the FIFP portal, accessible via the National Single Window System (NSWS). Required documents include:

- Letter of authorization for the filing person

- FDI proposal summary (background, business model, beneficial ownership)

- Pre- and post-transaction shareholding patterns

- Fund flow and group structure diagrams

- Beneficial ownership details (especially for land-border country investors)

- Investee company documents: Certificate of Incorporation, MoA, AoA, Board Resolution, Audited Financials

- Investor documents (authenticated per FEMA rules)

- Valuation certificate per FEMA pricing guidelines

- Undertaking that entities/directors are not on negative/sanction lists

- Notarized affidavit on INR 100 stamp paper

- Security Clearance Form (for specified sectors)

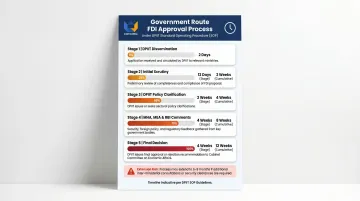

The DPIIT Standard Operating Procedure (SOP), dated May 4, 2026, sets a 12-week standard processing timeline:

| Stage | Duration | Cumulative |

|---|---|---|

| DPIIT dissemination | 2 days | 2 days |

| Initial scrutiny | 12 days | 2 weeks |

| DPIIT policy clarification | 2 weeks | 4 weeks |

| Comments from MHA, MEA, RBI, regulators | 4 weeks | 8 weeks |

| Final decision | 4 weeks | 12 weeks |

In practice, applications involving clarifications, supplementary documents, or security clearances can extend to 6-9 months. Proposals exceeding INR 5,000 crore require Cabinet Committee on Economic Affairs (CCEA) clearance. For Singapore businesses, this means building government approval milestones directly into term sheets and SPA conditions precedent — treating the 12-week standard as a floor, not a guarantee.

Sector-by-Sector FDI Limits: Permitted, Restricted, and Prohibited

Three-Tier Sector Classification

India's FDI policy classifies sectors into three tiers:

- Fully open: 100% FDI under Automatic Route

- Conditionally permitted: Sectoral caps or government approval required above a threshold

- Fully prohibited: No FDI allowed under any route

This classification determines the approval route, timeline, and compliance obligations — so identifying the right tier before choosing a sector is the first step for any Singapore investor.

Sectors Open to 100% FDI Under Automatic Route

Key sectors include:

- Manufacturing (general): No conditions

- IT and technology services: No conditions

- Construction and real estate development: Minimum area and capitalization conditions; no repatriation before 3 years

- Logistics: No conditions

- Railways infrastructure: Covers infrastructure projects, not train operations

- Telecommunications: Subject to security conditions

Full foreign ownership with no prior approvals makes these the fastest entry points for Singapore businesses.

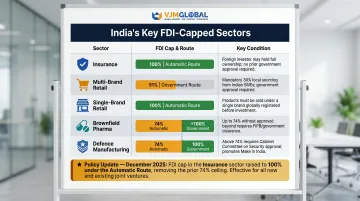

Sectors With FDI Caps or Conditions

| Sector | FDI Cap | Route | Key Conditions |

|---|---|---|---|

| Insurance | 100% (as of Dec 2025) | Automatic | Indian management required; entire premium must be invested in India |

| Multi-brand retail | 51% | Government | State approval required; 30% sourcing from Indian MSMEs |

| Single-brand retail | 100% | Automatic (beyond 49% requires local sourcing) | 30% local sourcing from India; e-commerce permitted for brick-and-mortar SBRT |

| Brownfield pharmaceuticals | 74% Automatic / 100% Government | Automatic up to 74%; Government beyond | Non-compete clause restrictions apply |

| Defence manufacturing | 74% Automatic / 100% Government | Automatic up to 74%; Government beyond | Beyond 74% permitted where it brings modern technology |

The insurance sector's opening to 100% FDI in December 2025 represents a major opportunity for Singapore financial services firms, particularly those with insurance operations.

Fully Prohibited Sectors

FDI is not permitted under any route in:

- Lottery and gambling (including casinos)

- Chit funds

- Real estate speculation (excluding development)

- Tobacco product manufacturing

- Atomic energy

- Railway operations (train operations, distinct from infrastructure)

Some prohibited categories have close permitted equivalents — real estate development is allowed, for instance, while real estate speculation is not. Verifying the specific activity matters.

Sector Classification Nuances

Several sectors have permitted and prohibited sub-categories that look similar on the surface:

- E-commerce (B2B marketplace): 100% FDI under Automatic Route

- E-commerce (B2C inventory model): Prohibited

- Pharma (brownfield): Up to 74% Automatic; beyond that requires Government approval

- Defence: Same dual-threshold structure as pharma, with the added condition that the higher tranche must introduce modern technology

A sector-specific assessment — reviewing the exact business activity, not just the industry label — is essential before finalizing any investment structure.

Compliance and Reporting Requirements for Singapore Investors

FEMA and NDI Rules: The Foundational Framework

All FDI in India is governed by the Foreign Exchange Management Act, 1999 (FEMA) and the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019 (NDI Rules). Singapore businesses must ensure every stage complies with entry route norms, sectoral caps, and pricing guidelines.

Key Reporting Obligations

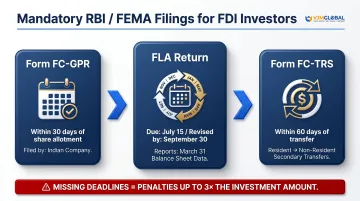

Three filings apply to most Singapore investors:

- Form FC-GPR — Filed by the Indian company with the RBI within 30 days of allotment of shares, convertible debentures, or other eligible instruments to a non-resident.

- FLA Return (Foreign Liabilities and Assets) — Annual filing due by July 15, reporting data as of March 31. If audited accounts aren't ready, file provisional figures and submit revised figures by September 30.

- Form FC-TRS — Required for secondary share transfers between residents and non-residents within 60 days of transfer. Transfers between two non-residents are exempt from FC-TRS but must still meet reporting norms.

Missing any deadline triggers FEMA contravention proceedings with penalties up to three times the amount involved.

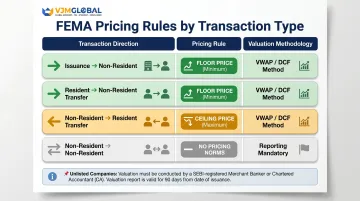

Deadlines are just one piece of the compliance picture. Pricing on every cross-border equity transaction must also meet FEMA's fair market value (FMV) norms.

Pricing Guidelines Under FEMA

| Transaction Type | Pricing Rule | Methodology |

|---|---|---|

| Issuance to non-resident (inbound FDI) | Price must not be less than FMV (floor price) | Listed: SEBI-prescribed VWAP; Unlisted: DCF or internationally accepted methodology on arm's length basis |

| Transfer: Resident to non-resident | Price must not be less than FMV (floor price) | Same as above |

| Transfer: Non-resident to resident | Price must not exceed FMV (ceiling price) | Same as above |

| Transfer: Non-resident to non-resident | No pricing norms | Must still be reported |

For unlisted companies, a SEBI-registered Merchant Banker or Chartered Accountant must certify the valuation. The valuation report is valid for 90 days.

Sectors Requiring Security Clearance

The following sectors require prior security clearance from the Ministry of Home Affairs (MHA) as part of the FDI approval process:

- Broadcasting

- Telecommunications

- Defence

- Civil aviation

- Private security agencies

- Space

- Mining of titanium-bearing minerals

Security clearance adds time and documentation requirements to the investment timeline. Singapore businesses investing in these sectors should factor MHA clearance into their project timelines from the outset.

How to Structure Your India Investment: Entry Vehicles

Main Entity Types

| Structure | FDI Eligibility | Key Features | Key Restrictions |

|---|---|---|---|

| Wholly Owned Subsidiary (Private Limited Company) | Full FDI eligible in all permitted sectors | Registered under Companies Act 2013; minimum 2 directors (1 resident in India), 2 shareholders; full commercial operations; profit repatriation allowed | Annual ROC filings; audit requirements; corporate governance compliance |

| Limited Liability Partnership (LLP) | Restricted | FDI permitted only via Government approval route and only in sectors where 100% FDI is allowed under Automatic Route | Cannot operate in sectors with partial FDI caps; must comply with LLP Act 2008 |

| Branch Office (BO) | Not FDI (extension of foreign parent) | Permitted for export/import, professional/consultancy services, research, IT services, technical support | Cannot undertake retail trading or manufacturing (except in SEZs); requires RBI approval |

| Liaison Office (LO) | Not FDI (representative office) | Permitted only for representing parent, promoting export/import, facilitating technical/financial collaboration | Cannot undertake any commercial/trading/industrial activity or earn income in India; funded entirely by parent; initial approval typically 3 years |

| Project Office (PO) | Not FDI (project-specific) | Permitted to execute a specific project in India; can be set up with RBI general permission if project is funded by inward remittance or bilateral/multilateral financing | Limited to the specific project; must close upon completion |

Choosing the Right Structure

- Operational presence: Wholly owned subsidiaries and LLPs are the most common choices for Singapore businesses wanting full commercial activity in India.

- Market exploration: Liaison offices provide a cost-efficient foothold without triggering commercial activity restrictions.

- One-time projects: Project offices suit infrastructure or manufacturing engagements with a defined endpoint.

The structure you choose also shapes your tax position under the India-Singapore DTAA. Singapore companies investing through an Indian subsidiary are well-positioned to access reduced dividend withholding tax rates under the treaty. However, capital gains on Indian shares acquired post-April 2017 are taxable in India at domestic rates, regardless of which structure you use — making professional tax advice an important part of the setup process.

Recent FDI Policy Updates Singapore Businesses Must Track

Insurance Sector Opening to 100% FDI

In December 2025, Parliament passed the Insurance Laws (Amendment) Bill, raising the FDI cap from 74% to 100%. Key conditions under IRDAI oversight include:

- Indian management control must be maintained

- Domestic reinvestment of premiums is required

- Full compliance with IRDAI licensing and reporting norms

For Singapore financial services companies with insurance operations, this opens the door to full ownership in a market where insurance penetration remains low — a significant structural opportunity.

High-Level Committee on Ease of Doing Business

In February 2025, the Union Budget announced formation of a high-level committee for regulatory reforms to "strengthen trust-based economic governance and enhance ease of doing business." The DPIIT's Business Reforms Action Plan (BRAP) 2024 and the Regulatory Compliance Burden (RCB) initiative have already delivered over 42,000 compliance reductions under 670 acts nationally — fewer filings, faster approvals, and lower administrative overhead for incoming investors. Singapore businesses should monitor DPIIT press notes directly for updated compliance procedures as these reforms roll out.

Ongoing Policy Evolution

Singapore investors should track:

- DPIIT's consolidated FDI policy document (updated periodically)

- RBI's Master Directions on Foreign Investment in India

- Press Note 3 revisions (final FEMA notification for the 10% beneficial ownership threshold pending as of March 2026)

Changes to sectoral caps and conditions can take effect with short notice, directly affecting investment structuring decisions.

Frequently Asked Questions

Is Foreign Direct Investment allowed in India?

Yes, FDI is broadly allowed in India. Most sectors are open either under the Automatic Route (no prior approval needed) or the Government Approval Route (12-week standard timeline). Only a small set of sectors—lottery, gambling, chit funds, atomic energy, and railway operations—are fully prohibited.

Where is FDI not allowed in India?

FDI is fully prohibited in lottery and gambling businesses, chit funds, speculative real estate, tobacco product manufacturing, atomic energy, and railway operations.

What are the 4 types of FDI?

The four types are:

- Horizontal FDI — same industry replicated in another country

- Vertical FDI — different stage of the supply chain abroad

- Conglomerate FDI — unrelated business entered in a foreign country

- Platform FDI — production in one country, sales to a third

What are the top 5 FDI sources in India?

As of September 2025, the top five cumulative FDI source countries are:

- Singapore — USD 186.8 billion

- Mauritius — USD 183.8 billion

- USA — USD 77.4 billion

- Netherlands — USD 55.0 billion

- Japan — USD 45.7 billion

Singapore overtook Mauritius in 2025 to claim the top position.

How long does it take to get FDI approval in India?

Automatic Route investments require no prior approval. Government Route approvals carry a 12-week DPIIT indicative timeline, though complex proposals with sector-specific clearances can take 6–9 months depending on documentation completeness.