Introduction

UK businesses expanding into Singapore or selling goods and services to Singapore customers face GST obligations under Singapore law — regardless of where they are based. Unlike domestic VAT compliance, Singapore's overseas entity rules differ significantly from the UK's framework, particularly in agent appointment requirements, registration triggers, and ongoing obligations.

This complexity creates real compliance risk. Common scenarios where UK businesses are caught off-guard include:

- A SaaS company selling subscriptions to Singapore consumers, already liable under the Overseas Vendor Registration (OVR) regime without realising it

- A manufacturer importing goods into Singapore for local distribution, required to appoint a local agent before registration

- A business tracking revenue in GBP, crossing the SGD 1 million threshold without triggering internal alerts

This guide covers the full picture: when UK businesses must register, how the registration process works, what overseas entity requirements apply, and what ongoing compliance looks like once you're registered.

Key Takeaways

- Mandatory GST registration kicks in once Singapore sales exceed SGD 1 million, either retrospectively at year-end or prospectively within 30 days of forecasting the threshold

- Selling digital services or low-value goods (SGD 400 or below) to Singapore consumers triggers OVR registration, even without a local presence

- Unlike local businesses, UK businesses registering as overseas entities must appoint a local Section 33(1) agent responsible for GST accounting and payment

- Voluntary registration below SGD 1 million is possible and financially advantageous, but requires GIRO setup, e-learning completion, and a two-year minimum commitment

- Non-compliance carries serious consequences: backdated GST liability, fines up to SGD 10,000, and a 10% penalty on GST owed

What Is Singapore GST and Why Does It Matter for UK Businesses?

Singapore's Goods and Services Tax (GST) is a consumption tax currently set at 9% (effective from 1 January 2024), administered by the Inland Revenue Authority of Singapore (IRAS). The tax applies to most goods and services sold in Singapore, including imports.

The system operates through an output tax/input tax mechanism. Registered businesses collect GST on sales (output tax) and offset it against GST paid on business purchases (input tax). IRAS describes the mechanism as taxing only "the value-add at each stage of a supply chain."

How Singapore GST Differs from UK VAT

Both are value-added consumption taxes collected by businesses on behalf of the government. However, key structural differences exist:

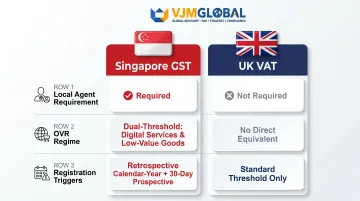

- Local agent requirement: Overseas entities registering under standard GST must appoint a Section 33(1) agent resident in Singapore, who becomes personally responsible for GST accounting and payment. The UK has no equivalent requirement for overseas traders.

- Separate OVR regime: Digital service providers and low-value goods sellers fall under the Overseas Vendor Registration regime, with a dual-threshold trigger — global turnover exceeding SGD 1 million AND Singapore B2C supplies exceeding SGD 100,000 annually.

- Dual registration triggers: Singapore applies both a retrospective basis (calendar-year review) and a prospective basis (forward-looking forecast) to determine when registration liability kicks in.

Why UK Businesses Must Understand Singapore GST Before Market Entry

Failing to register on time creates backdated liability. IRAS backdates registration to when the business ought to have registered, meaning you're liable for GST on past sales — even if you never collected it from customers.

Registration isn't only a compliance obligation, though — it can work in your favour. Key financial implications include:

- Backdated liability risk: GST owed on past sales if registration is delayed, regardless of whether it was charged

- Input tax recovery: Businesses with significant Singapore-side costs can offset GST paid on purchases, reducing net expenses

- Cash flow benefit: UK exporters supplying zero-rated international services can reclaim input tax on related costs

Do UK Businesses Need to Register for GST in Singapore?

Mandatory Registration — Retrospective Basis

A UK business with taxable turnover from Singapore sales exceeding SGD 1 million in a calendar year (1 January to 31 December) must apply for registration between 1–30 January of the following year, with an effective registration date of 1 March.

Taxable turnover includes:

- Standard-rated supplies (local supply of goods or services)

- Zero-rated supplies (export of goods or international services)

Taxable turnover excludes:

- Exempt supplies

- Out-of-scope supplies

- Sale of capital assets (machinery, equipment, office buildings)

Mandatory Registration — Prospective Basis

If a UK business can reasonably expect its Singapore taxable turnover to exceed SGD 1 million in the next 12 months, it must apply within 30 days of the forecast date.

IRAS requires supporting evidence: signed contracts, accepted quotations, confirmed purchase orders, or invoices showing fixed monthly fees.

2025 update: For liability arising on or after 1 July 2025, businesses receive a two-month grace period (extended from one month) before they must begin charging GST. The 30-day application deadline still applies.

Voluntary Registration

UK businesses below the SGD 1 million threshold may register voluntarily. This makes strategic sense when:

- Singapore-side operating costs are significant (allowing input tax recovery)

- UK exporters supplying zero-rated international services want to reclaim input tax on related costs

- The business expects to cross the threshold within 12 months and wants to establish compliance infrastructure early

Voluntary registration comes with several mandatory conditions:

- Minimum two-year registration commitment

- GIRO arrangement required before registration

- E-learning course completion and quiz pass required (director, partner, or return preparer)

- InvoiceNow compliance required from 1 April 2026 for new voluntary registrants

The Overseas Vendor Registration (OVR) Regime

UK businesses selling digital services (software, streaming, online consultancy) or low-value goods (SGD 400 or below) directly to Singapore consumers or non-GST-registered businesses may fall under the OVR regime. This applies even without a Singapore office or any physical presence in the country.

OVR registration thresholds (both must be met):

- Annual global turnover exceeding SGD 1 million, AND

- B2C supplies of remote services and/or low-value goods to Singapore exceeding SGD 100,000 annually

Once those thresholds are met, the OVR regime operates differently from standard GST registration in several important ways:

How OVR registration differs from standard GST:

- Separate OVR application form (not standard GST F1)

- No Section 33(1) local agent requirement

- Simplified pay-only regime (no input tax claims)

- Guarantee may be required for voluntary OVR registrants

UK business types most likely to trigger OVR:

- SaaS providers (subscription software)

- Streaming services (media, music, video)

- Online marketplaces (deemed suppliers under the regime)

- E-commerce retailers (physical goods valued at SGD 400 or less)

- Online consultancy and advisory firms (data analysis, research, telemedicine)

How UK Businesses Register for GST in Singapore: Step-by-Step

GST registration is conducted through the IRAS myTax Portal. UK businesses registering as overseas entities follow the same online process as local registrants, but with additional requirements. Because UK businesses cannot access Corppass directly without a local representative, appointing a local agent is a required first step.

Step 1: Determine Your Registration Type

Assess whether you are registering compulsorily (retrospective or prospective basis), voluntarily, or under the OVR regime. Use the IRAS GST registration calculator to check liability.

Step 2: Complete the GST E-Learning Course (Voluntary Registrants Only)

Voluntary registrants must have the company director, partner, trustee, or the person preparing GST returns complete IRAS's free "Overview of GST" e-learning course and pass the quiz before submitting the application.

Exemptions:

- Director/partner has experience managing other existing GST-registered businesses

- Preparer of GST returns is an Accredited Tax Adviser (ATA) or Accredited Tax Practitioner (ATP)

- Applying under OVR Simplified Pay-Only Regime

This step does not apply to compulsory registrants.

Step 3: Prepare the Required Supporting Documents

Prepare the following documents in PDF format for upload:

- Certificate of Incorporation in English (UK businesses will not have an ACRA business profile)

- Recent sales invoices or financial records evidencing turnover or projected turnover

- Letter appointing a local Singapore agent (Section 33(1) agent)

- For voluntary registrants: completed GIRO application form and e-learning acknowledgement

Refer to the IRAS Document Checklist for the full list.

Step 4: Submit the Application via myTax Portal

UK businesses log in through the portal via their local agent's Corppass credentials, complete the GST F1 registration form, and upload all supporting documents. IRAS will not process incomplete applications — ensure all documents are uploaded before submitting.

For voluntary registrants:

- Set up GIRO — either via eGIRO (near-instant) or paper form (up to 21 working days)

- GIRO approval must be secured before registration is processed

- If the GIRO application form is not submitted within 10 working days, the registration application is treated as cancelled

Step 5: Await Approval and Receive GST Registration Number

IRAS processes 60% of applications within 10 working days and the remainder within 30 days. Once approved, a letter is sent to the registered address confirming the GST registration number and the effective date of registration.

Critical: Do not charge GST before the confirmed effective date. For late compulsory registrations, the effective date is backdated.

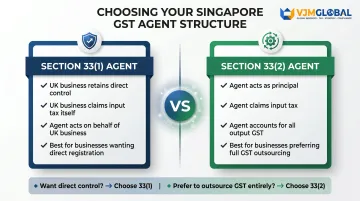

Appointing a Local Singapore Agent: Section 33(1) vs Section 33(2)

Section 33(1) Requirement

Under Section 33(1) of the GST Act, an overseas entity — one with no business establishment, fixed establishment, or usual place of residence in Singapore — that imports goods for supply in Singapore must appoint a local agent. This agent is personally responsible for accounting and payment of GST to IRAS on the overseas business's behalf.

For UK businesses registering under the standard GST regime, this appointment is a legal requirement — not a discretionary step.

What the Section 33(1) agent does:

- Submits GST returns (Form F5) quarterly

- Makes GST payments on behalf of the UK business

- Maintains records and coordinates with the UK business

- Liaises with IRAS on behalf of the UK business

Eligible agents include Singapore-based accounting firms, tax advisers, or other trusted entities with a Singapore presence. Appointment must be formalised via a letter included in the registration documents.

Section 33(2) Alternative

Under Section 33(2), a UK business may instead appoint a GST-registered Singapore agent who imports and supplies goods on the UK business's behalf in its own name. Under this arrangement, the agent claims input tax on imports and accounts for GST on subsequent sales as if it were the principal. This route means the UK business itself does not need to register for GST.

How the Section 33(2) arrangement works:

- Agent imports and sells goods under its own name

- Agent claims input tax on imports directly

- Agent accounts for output GST on all subsequent sales

- UK business avoids direct GST registration entirely

When to use Section 33(1) vs 33(2):

| Factor | Section 33(1) | Section 33(2) |

|---|---|---|

| Direct control | UK business retains control | Agent acts as principal |

| Input tax recovery | UK business claims | Agent claims |

| Commercial relationship | Agent acts on behalf of UK business | Agent supplies as principal |

| Best for | UK businesses wanting direct registration and control | UK businesses preferring to outsource GST entirely |

VJM Global's Cross-Border Tax Compliance Support

VJM Global brings 30+ years of experience helping UK businesses navigate cross-border tax compliance and international regulatory requirements. Working with a specialist adviser familiar with UK business structures and overseas compliance obligations helps UK businesses identify the right agent structure, prepare compliant documentation, and avoid registration delays.

For guidance on overseas entity GST registration in Singapore or coordinating agent appointments, contact VJM Global for a consultation.

Ongoing GST Obligations After Registration

Filing Requirements

Once registered, UK businesses (via their local agent) must file quarterly GST returns (Form F5) through the myTax Portal within one month after each accounting period ends.

| Accounting Period | Filing and Payment Due Date |

|---|---|

| January - March | 30 April |

| April - June | 31 July |

| July - September | 31 October |

| October - December | 31 January |

NIL returns must be filed even in quarters with no transactions. No extensions are granted. GST payment is due on the same deadline as the return.

Record-Keeping

All business and accounting records must be retained for a minimum of five years — even after GST registration is cancelled. Required records include:

- Sales invoices and purchase receipts

- Import and export documents

- Contracts and agreements

The UK business holds this obligation and should coordinate with the local agent to ensure records remain accessible for IRAS audits.

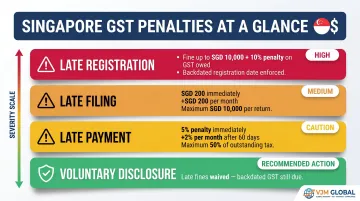

Penalties for Non-Compliance

| Offence | Penalty |

|---|---|

| Late registration | Fine up to SGD 10,000 + penalty equal to 10% of GST due; registration date backdated |

| Late filing of GST return | SGD 200 immediately + SGD 200 for every completed month outstanding; maximum SGD 10,000 per return |

| Late payment of GST | 5% late payment penalty imposed immediately; additional 2% per completed month unpaid after 60 days; maximum 50% of outstanding tax |

Voluntary disclosure: If you submit an application for GST registration and voluntarily disclose that you are late, IRAS waives the late notification fine and penalties. However, backdated GST on past sales must still be paid.

Common Mistakes UK Businesses Make with Singapore GST

Applying UK VAT Logic to Singapore GST

UK businesses often assume Singapore GST rules mirror UK VAT treatment for overseas traders. Key differences include:

- Mandatory local agent requirement: No equivalent exists in UK VAT

- OVR regime threshold and mechanics: Singapore's dual-threshold trigger and simplified pay-only regime have no direct UK VAT parallel

- Retrospective/prospective registration triggers: The calendar-year retrospective basis and 30-day prospective application deadline differ from UK VAT thresholds

Consider a UK SaaS company selling subscriptions to Singapore consumers. It triggers OVR obligations based solely on supply thresholds — no Singapore office required, no physical presence needed.

Missing Registration Deadlines Due to Currency and Threshold Tracking

UK businesses typically track revenue in GBP, not SGD. Turnover can cross the SGD 1 million threshold without the business realising it.

The practical fix: track Singapore-sourced revenue in SGD separately from your GBP accounts. Set a quarterly internal review to assess whether the threshold has been crossed — or is on track to be crossed within the next 12 months.

Overlooking OVR Obligations for Digital or E-Commerce Businesses

Many UK businesses selling digital products, SaaS, or low-value physical goods to Singapore customers assume GST does not apply because they have no physical presence there. The OVR regime applies regardless of physical presence, and the penalties for missing that registration are the same as for any other late registrant — no leniency for remote sellers.

Business types most exposed to this oversight include:

- Subscription software providers

- Streaming media services

- Online course or e-learning platforms

- E-commerce retailers selling goods valued at SGD 400 or less

Frequently Asked Questions

When should a company register for GST in Singapore?

A company must register when taxable turnover exceeds SGD 1 million. Under the retrospective basis, registration applies at the end of the calendar year (application due 1–30 January). Under the prospective basis, it applies when turnover is reasonably expected to exceed SGD 1 million within the next 12 months, with the application due within 30 days of that forecast.

How do I register for GST in Singapore?

Registration is completed via the IRAS myTax Portal. UK businesses as overseas entities must appoint a local Singapore agent before or during the application process and prepare supporting documents including a Certificate of Incorporation in English.

How long does it take to register for GST in Singapore?

IRAS processes most applications within 10 working days and the remainder within 30 days. Voluntary registrants face additional processing time if GIRO approval is pending (up to 21 working days for paper GIRO).

Who is required to register for GST in Singapore?

Local businesses exceeding the SGD 1 million taxable turnover threshold must register. Overseas businesses — including UK companies — that supply taxable goods or services in Singapore, or fall under the OVR regime for digital services and low-value goods, are also required to register.

Who is not required to register for GST?

The following businesses are not required to register:

- Businesses below SGD 1 million turnover (voluntary registration is still available)

- Businesses whose turnover is wholly or mainly from zero-rated (export) supplies — exemption can be applied for

- Businesses making only exempt or out-of-scope supplies

How to get a GST registration number in Singapore?

IRAS issues a GST registration number automatically once your application is approved. You'll receive it by letter to your registered address and can also view it on the myTax Portal. Print this number on all tax invoices from your effective registration date.