Introduction

The commercial case for Australian businesses entering India has never been stronger. Since the Australia-India Economic Cooperation and Trade Agreement (ECTA) entered into force on 29 December 2022, 90% of Australian goods exports to India by value became tariff-free—a shift that makes establishing a formal presence in India genuinely cost-competitive for the first time.

The opportunity sits on top of a market of 1.46 billion people. India's middle class is projected to reach 715 million by 2030-31, according to PRICE data via IBEF, and bilateral trade between the two countries already exceeds AUD $50 billion annually.

Setting up legally in India is a different process from what Australian founders are used to. It involves navigating FDI entry routes, Indian corporate law, FEMA compliance, and ongoing statutory obligations that don't map onto Australian business structures. This guide covers every key step: choosing the right entity type, understanding FDI regulations, completing MCA registration, registering for GST and tax, and meeting post-incorporation compliance requirements.

Key Takeaways

- Australian businesses can enter India through a Private Limited Company, LLP, or Branch Office—each carrying different FDI implications and compliance obligations.

- India's MCA portal handles the full incorporation process via the SPICe+ form—covering name reservation, digital signatures, director identification, and the incorporation filing itself.

- Post-incorporation essentials include PAN, TAN, GST registration, and FEMA compliance for cross-border fund flows.

- Under the India-Australia DTAA, withholding tax on dividends and interest is capped at 15% and royalties at 10–15%—reducing the tax burden on cross-border payments.

- Working with an India-based advisor significantly reduces setup time and prevents costly compliance errors.

Why Australian Businesses Are Setting Up in India

India's appeal as an expansion destination goes beyond headline population figures.

Market Scale and Consumer Growth

India's middle class stood at 432 million people (31% of the population) in 2020-21 and is projected to reach 1.02 billion by 2046-47. For Australian companies in technology, agribusiness, education, and professional services, that trajectory represents sustained, long-term demand.

DFAT's 2025 economic engagement roadmap identifies clean energy, education and skills, agribusiness, and technology as the priority sectors for Australian-Indian commercial partnerships—a useful filter for businesses evaluating which opportunities warrant a formal Indian entity.

Operational Advantages

Beyond market access, India offers meaningful cost advantages for back-office and service operations:

- Large English-speaking workforce across technology, finance, and professional services

- Significantly lower operational costs compared to Australian equivalents

- Established business hubs like Noida, Bengaluru, Hyderabad, and Pune purpose-built for foreign business operations

Government-Level Support

Three policy levers have made India's entry environment notably more favourable for Australian companies:

- Make in India (10+ years running) has simplified foreign entry across pharmaceuticals, electronics, renewable energy, and automobiles

- ECTA tariff reductions lower the cost of cross-border goods trade between Australia and India

- India-Australia DTAA reduces withholding tax on cross-border income flows, cutting the tax friction on dividends, royalties, and service fees

Together, these frameworks mean Australian businesses entering India today face fewer regulatory barriers and lower tax drag than at any point in the past two decades.

Choosing the Right Business Structure for Australian Companies

The structure you choose determines your FDI eligibility, liability exposure, compliance burden, and ability to raise funding. Make this decision before approaching India's Ministry of Corporate Affairs — each structure has different registration pathways, tax implications, and operational constraints.

Private Limited Company (Pvt Ltd)

The most common structure for foreign businesses entering India. Key features:

- Allows 100% FDI under the automatic route in most sectors (no prior government approval required)

- Offers limited liability to shareholders

- Suitable for businesses planning to scale, hire locally, or raise external funding

- Requires a minimum of two directors, with at least one resident in India for not less than 182 days per financial year

For Australian founders without Indian residency, a local professional can be appointed as the resident director. This is a standard arrangement that VJM Global facilitates for foreign clients.

Limited Liability Partnership (LLP)

A more flexible structure suited to professional services firms or SMEs:

- Simpler compliance requirements than a Pvt Ltd company

- Cannot raise equity funding from external investors

- FDI is permitted under the automatic route only where 100% automatic FDI applies and no FDI-linked performance conditions exist (such as minimum capitalization thresholds or export obligations)

Australian businesses should verify their sector's FDI eligibility before selecting this structure. LLP is not universally available under the automatic route.

Branch Office

An established Australian company can open a Branch Office in India without forming a new legal entity. However, there are strict limitations:

- Requires prior RBI approval and FEMA compliance

- Cannot undertake manufacturing, processing, or retail activities

- Taxed at a higher income tax rate than a domestic subsidiary

Branch Offices work best for exploratory or representative purposes before full incorporation. They are not suited as a long-term operating vehicle.

Decision Framework

| Goal | Recommended Structure |

|---|---|

| Full operations, scaling, hiring | Private Limited Company |

| Professional services, flexibility | LLP (verify FDI route first) |

| Market testing, representative presence | Branch Office / Liaison Office |

| Restricted sector with local partner | Joint Venture |

Note that sector-specific FDI rules can override structural preferences — a sector listed under the government approval route may restrict LLP or Branch Office eligibility regardless of your business goals. Confirm your sector's FDI classification first.

Step-by-Step: How to Register a Business in India from Australia

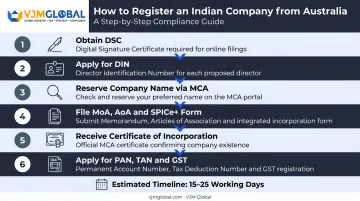

Registration is managed through India's MCA portal using the SPICe+ (Simplified Proforma for Incorporating a Company Electronically Plus) form. When documents are in order, the process typically takes 15–25 working days, though delays can occur at the apostille, FDI approval, or RBI authorization stages. Here's what each step involves.

Step 1: Obtain a Digital Signature Certificate (DSC)

All proposed directors must obtain a DSC from an authorized Certifying Authority. It is the mandatory electronic key for signing all digital submissions to the MCA.

For Australian directors, identity documents must be notarized and apostilled before submission. Australia's Department of Foreign Affairs and Trade (DFAT) issues Australian Apostilles, which authenticate the origin of public documents for use by foreign authorities.

Step 2: Apply for a Director Identification Number (DIN)

Every director must hold a DIN issued by the MCA. The DIN application is filed as part of the SPICe+ form itself — no separate process required. At least two directors are required, with one being an India-resident director—either an existing team member or an appointed local professional.

Step 3: Reserve a Company Name via the MCA Portal

The RUN (Reserve Unique Name) service on the MCA portal checks proposed names against existing registered entities and MCA naming guidelines. Key rules:

- Cannot be identical to any existing registered name

- Must not suggest government affiliation

- Cannot contain prohibited or offensive terms

SPICe+ Part A also handles name reservation as part of the integrated incorporation process.

Step 4: Prepare and File MoA, AoA, and the SPICe+ Form

The Memorandum of Association (MoA) defines the company's objectives; the Articles of Association (AoA) governs internal rules. Both are submitted digitally with the SPICe+ form to the Registrar of Companies (RoC).

Even minor errors in the MoA, AoA, or supporting documents trigger resubmissions and can add weeks to your timeline. VJM Global's incorporation team notes that "both MoA and AoA have to be made with total clarity and accuracy" — and manages all RoC queries that arise from the filing.

Step 5: Receive the Certificate of Incorporation

Following RoC approval, the Certificate of Incorporation (CoI) is issued—legally recognizing the company in India. The CoI includes the company's Corporate Identification Number (CIN). For public limited companies, a Certificate of Commencement of Business is also required before operations begin.

Step 6: Apply for PAN, TAN, and GST Registration

After incorporation, three registrations are needed:

- PAN (Permanent Account Number): required for all tax filings and banking

- TAN (Tax Deduction and Collection Account Number): required for managing withholding tax obligations

- GST Registration: mandatory when annual aggregate turnover exceeds ₹20 lakh (₹10 lakh in special category states), or for any company making inter-state taxable supplies

These are typically applied for through the AGILE-PRO-S form linked to SPICe+ Part B, or shortly after incorporation.

Documents Required to Register a Company in India from Australia

Core Documentation

| Document | Requirement |

|---|---|

| Valid passport | Notarized and apostilled for all Australian directors |

| Proof of Indian registered address | Physical or qualifying virtual address |

| DSC | Required for all directors |

| DIN | Applied through SPICe+ |

| MoA and AoA | Drafted and submitted digitally |

All foreign-origin documents must go through the apostille process. DFAT issues Australian Apostilles, which authenticate the signatures and seals of Australian officials for acceptance by Indian authorities.

FDI Compliance Documentation

Before filing, Australian businesses must confirm their investment complies with India's FDI policy for their specific sector:

| Route | Approval Required | Common Sectors |

|---|---|---|

| Automatic Route | No prior approval needed | Manufacturing, IT, most services |

| Government Route | Prior FIPB approval required | Multi-brand retail (51%), news media (26%), defence (above 74%) |

Misclassifying your sector's FDI route can trigger rejection or registration delays. Confirming this before filing prevents penalties and restarts.

Post-Incorporation Requirements

- Indian business current account (resident director typically required for account opening)

- PAN, TAN, and GST registration certificates

- Sector-specific licenses or permits where applicable

Post-Incorporation Obligations: Compliance, Tax, and Banking

Ongoing Statutory Compliance

Under the Companies Act 2013, Australian-owned Indian companies must maintain:

- First board meeting within 30 days of incorporation

- Minimum 4 board meetings per year, with no more than 120 days between meetings

- First auditor appointment by the board within 30 days of registration

- Annual return (Form MGT-7) filed within 60 days of the AGM

- Financial statements (Form AOC-4) filed within 30 days of the AGM

- GST return filings (GSTR-1, GSTR-3B) on a monthly or quarterly basis

Compliance costs add up quickly — statutory audit fees, company secretarial filings, GST returns, and transfer pricing documentation all require ongoing attention, especially once the Indian entity starts transacting with the Australian parent. VJM Global manages this full compliance stack for Australian clients, so nothing falls through the gaps.

Opening an Indian Business Current Account

A current account is required to operate in India. Typical documents needed:

- Certificate of Incorporation

- PAN card

- MoA and AoA

- Board resolution authorizing account opening

The resident Indian director is usually required to be present for account opening. Cross-border fund flows between the Indian entity and the Australian parent must comply with FEMA and RBI regulations — including proper reporting of capital inflows, dividend repatriation, and intercompany loan arrangements.

Tax Considerations for Australian Businesses

Key rates for AY 2026-27:

- Foreign company income tax rate: 35%, plus surcharge and 4% health and education cess

- Domestic subsidiary (Pvt Ltd) rate: 30% for most companies; concessional rates available (22% under Section 115BAA; 15% under Section 115BAB for new manufacturing companies)

Transfer pricing rules under Sections 92–92F apply when transacting with the Australian parent — intercompany pricing must be set at arm's length and documented accordingly.

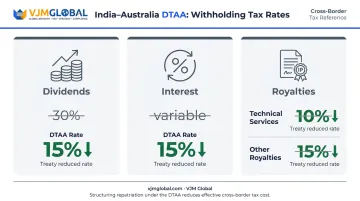

Beyond domestic rates, the India-Australia DTAA directly affects what you pay when moving profits home. The treaty reduces withholding tax on dividends to 15%, interest to 15%, and royalties to 10% (technical services) or 15% (other royalties). Structuring repatriation correctly under the DTAA can make a material difference to your effective tax cost.

Common Challenges Australian Businesses Face When Setting Up in India

Regulatory Complexity and FDI Nuances

India's regulatory framework spans the Companies Act, FEMA, RBI guidelines, and sector-specific rules—each with its own compliance calendar. Sectors including retail, media, defence, and financial services carry strict FDI caps and often require government-route approval. Misclassifying a sector's FDI route doesn't just slow registration; it can trigger penalties and require costly restructuring.

Cultural and Market Adaptation

What works commercially in Australia doesn't always translate to India's diverse, price-sensitive market. Australian businesses frequently underestimate:

- The importance of local relationship-building

- Regional market differences between cities and states

- The need to adapt product pricing against entrenched local competitors

Bureaucratic Timelines Without Local Representation

Without a resident director or on-the-ground support, approval timelines stretch—particularly for sectors requiring government FDI approval or RBI authorization for a Branch Office. Each of these stages moves faster with someone managing the process locally:

- DSC application and DIN registration

- ROC filings and incorporation documentation

- RBI notifications and bank account opening

These are precisely the friction points where local expertise makes a measurable difference. VJM Global has guided over 250 Australian businesses through India entry, covering FDI route assessment, entity selection, incorporation, FEMA compliance, and post-setup operations — structured to avoid the errors that trigger delays and resubmissions.

Conclusion

Setting up a business in India is manageable when approached systematically: confirm your FDI route, choose the right structure, complete MCA registration accurately, and build your compliance calendar from day one.

Before you move forward, make sure you've covered the essentials:

- Confirm whether your sector falls under automatic or government approval FDI routes

- Select a business structure that matches your operational model and liability requirements

- File MCA registration accurately to avoid delays at the incorporation stage

- Set up your GST, TDS, and annual compliance calendar before trading begins

India's market scale, ECTA trade access, skilled workforce, and government support for foreign investment make it one of the most strategically valuable entry points for Australian businesses right now. Getting the structure right from the start means spending your first two years growing — not untangling regulatory problems that could have been avoided.

Frequently Asked Questions

Can an Australian citizen start a business in India?

Yes. Australian citizens can establish a company in India, and India allows 100% FDI under the automatic route in most sectors. The most common structure is a Private Limited Company, which requires at least one India-resident director alongside the Australian founders.

What business structures are available to Australian companies registering in India?

The three main options are a Private Limited Company, a Limited Liability Partnership, and a Branch Office. Each suits a different purpose — full operations, professional services, or representative presence respectively. The right choice depends on your sector, FDI eligibility, and long-term goals.

Does Australia have a tax treaty with India?

Yes. The India-Australia Double Taxation Avoidance Agreement (DTAA) caps withholding tax on dividends and interest at 15%, and royalties at 10–15%. This reduces the tax cost of repatriating income from an Indian subsidiary to an Australian parent company.

How long does it take to register a company in India from Australia?

Registration typically takes 15–25 working days when all documents are in order. Delays occur most commonly when director documents are not properly apostilled, or when the sector requires RBI authorization or government FDI approval.

What is the minimum number of directors required for an Indian company set up by Australians?

A Private Limited Company requires a minimum of two directors. At least one must be resident in India for not less than 182 days during the financial year. Australian founders without Indian residency can appoint a local professional director to meet this requirement.

What are the ongoing compliance costs for running an Indian company?

Ongoing costs include statutory audit fees, annual RoC filings (Forms AOC-4 and MGT-7), GST return filing, and company secretarial services. For Australian-owned entities transacting with their parent company, transfer pricing documentation is mandatory for related-party transactions above prescribed thresholds . Costs vary by company size, turnover, and sector — a local compliance provider can quote based on your specific situation.