Introduction

Spain remains one of the most attractive destinations for UK entrepreneurs looking to access European markets post-Brexit. The numbers support this: Spain received €28.2 billion in foreign investment in 2023, with the UK ranking as the second-largest source of inflows at 13.1%, confirming that British capital continues to flow south despite the changed political relationship.

The core challenge is that Brexit fundamentally altered the personal status of UK nationals in Spain. Before 31 December 2020, British citizens had EU freedom of establishment — no visas, no special ID requirements, no unusual tax complexities.

That changed on 1 January 2021. UK nationals are now third-country nationals, meaning the process involves visa decisions, NIE applications, and cross-border tax considerations that didn't exist before 2021.

Understanding these requirements upfront saves significant time and cost. This guide walks through the post-Brexit landscape, the right business structure for your situation, the incorporation process, and the tax obligations you'll need to manage from day one.

Key Takeaways

- UK nationals can own 100% of a Spanish company after Brexit — no nationality restrictions on shareholding

- Brexit changed immigration status only: those physically relocating to Spain need a visa; remote owners do not

- A Spanish NIE is mandatory for all business activity — apply via the Spanish Consulate in London, Edinburgh, or Manchester

- The Sociedad Limitada (S.L.) is the standard structure for UK entrepreneurs entering Spain

- The full incorporation can be completed remotely from the UK using a notarial Power of Attorney

What Changed for UK Nationals After Brexit

Before 31 December 2020, UK citizens had exactly the same right to set up a business in Spain as any EU national — no visa, no restrictions, no extra steps. That ended when the Brexit transition period closed.

What Is Different Now

UK nationals are classified as third-country nationals for all Spanish legal purposes as of 1 January 2021. The practical consequences:

- Physical relocation requires a visa — UK nationals who want to live and run their business in Spain must now work through Spanish immigration requirements

- NIE applications go through the Spanish Consulate rather than a simpler domestic process, with processing times of 2–4 weeks

- Corporate structures involving a UK Ltd as shareholder require a Spanish corporate NIF (obtained via Form 036 with the Agencia Tributaria), adding a step that EU-resident shareholders don't face

What Has Not Changed

Not everything shifted, though:

- UK nationals can still own 100% of a Spanish S.L. with no local partner requirement

- The UK-Spain Double Taxation Treaty remains fully in force

- UK companies can still establish Spanish subsidiaries or branch offices

- The entire incorporation process can still be completed remotely from the UK

Why Spain Is Worth Considering

For UK entrepreneurs looking to re-establish a European presence post-Brexit, Spain offers a practical and well-supported entry point.

The numbers:

- Spain is the 4th largest economy in the EU, according to Invest in Spain/ICEX

- Spanish goods exports reached €384.5 billion in 2024 — the second-best year in the historical series

- Spain's population stands at 49.7 million with average household expenditure rising 4.4% in 2024 to €34,044

Beyond raw market size, several structural factors favour foreign entrepreneurs specifically:

- Startup Law (Ley de Startups, Law 28/2022) — cuts corporate tax to 15% for certified emerging companies, expands Beckham Law eligibility, and simplifies conditions for founders

- Entrepreneurship Service Points (PAEs) — government-run offices offering free incorporation guidance and fee-free CIRCE processing

- Growing foreign self-employed base — foreign RETA affiliates grew from 405,178 in January 2023 to 471,559 in February 2025, an 8.2% annual growth rate

- Geographic reach — Spain's position connects Western Europe, North Africa, and Latin America, giving UK businesses a broader distribution footprint than most single-country EU bases

Business Structures Available to UK Nationals

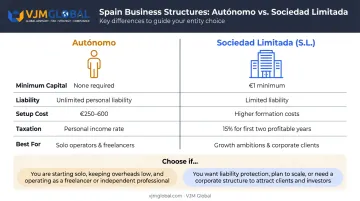

The first real decision is structural, and it matters more than most people expect. Choosing between Autónomo and Sociedad Limitada affects liability, tax efficiency, and how Spanish banks, clients, and suppliers perceive the business.

Autónomo (Self-Employed)

The Autónomo route means registering as a self-employed professional with the Agencia Tributaria and the Social Security system.

Best for: Freelancers, solo professionals, or those testing the market before committing to full incorporation.

| Feature | Detail |

|---|---|

| Setup cost | Approximately €250–600 |

| Minimum capital | None |

| Setup time | 1–2 weeks |

| Liability | Unlimited personal liability |

| Tax | IRPF progressive scale — becomes inefficient above approximately €50,000–60,000 net annual profit |

The unlimited liability exposure is the key limitation. Everything you own personally is at risk if the business falls into debt.

Sociedad Limitada (S.L.)

The S.L. is the go-to structure for UK entrepreneurs with growth plans, employees, or commercial relationships with Spanish corporates.

Best for: Anyone with meaningful revenue expectations, employees, or client contracts requiring a corporate counterparty.

| Feature | Detail |

|---|---|

| Minimum share capital | €1 (special reserve rules apply until €3,000 threshold is reached) |

| Liability | Limited to capital contribution |

| Corporate income tax | 25% general rate; 15% for first two profitable tax years |

| Tax efficiency vs. Autónomo | More efficient above approximately €50,000–60,000 annual net profit |

Other Structures to Know

Beyond Autónomo and S.L., three additional structures are worth understanding before ruling them out:

- Sociedad Anónima (S.A.) — Requires €60,000 minimum capital; used for large-scale operations or external fundraising

- Branch Office (Sucursal) — Extension of the UK parent company; the UK parent is fully liable for Spanish debts

- Representative Office — Cannot conduct commercial activity; limited to market research only

Most UK entrepreneurs starting out will default to the S.L. — it limits personal liability, scales with the business, and is immediately recognizable to Spanish banks and corporate clients.

Visas, NIE, and Legal Prerequisites

The NIE: Non-Negotiable First Step

The NIE (Número de Identificación de Extranjero) is Spain's foreigner tax identification number. Without one, no incorporation can proceed — it is the single hardest prerequisite to skip.

UK nationals apply at the Spanish Consulate in London, Edinburgh, or Manchester. Processing typically takes 2–4 weeks, so build this wait into your project timeline before booking notaries or advisers.

Corporate shareholders: If the shareholder is a UK Ltd rather than an individual, the company itself must obtain a Spanish corporate NIF via Form 036, filed with the Agencia Tributaria. This requires a local representative with an active NIE and is one of the most common sources of timeline delays.

Visa Options for UK Nationals Relocating to Spain

A visa is only required if you intend to physically live and work in Spain. Three main routes apply:

- Entrepreneur Visa — For innovative or technology-driven projects; requires a favourable report from ENISA (Spain's National Innovation Company) before the residence permit is granted. The bar is high, but the pathway suits founders with a scalable concept.

- Self-Employed (Autónomo) Visa — Standard pathway for traditional businesses: consultancies, retail, professional services. Requires a business plan validated by a recognised Spanish trade body.

- Digital Nomad Visa — Available to UK nationals working remotely for non-Spanish clients. Can provide access to the Beckham Law flat-rate tax regime, which is particularly relevant for UK professionals keeping an existing client base.

Note: The Golden Visa route via €500,000 real estate investment was discontinued in April 2025 under LO 1/2025 and is no longer a viable pathway.

Remote Incorporation from the UK

UK nationals who want to own and operate a Spanish company without relocating need no visa at any stage. The entire S.L. incorporation is completed through a notarial Power of Attorney (PoA):

- Drafted bilingually (English/Spanish)

- Signed before a UK Notary Public

- Legalised with an FCDO apostille (standard GOV.UK postal service typically takes 2–3 weeks)

- Accompanied by a sworn Spanish translation

From the point of receiving the completed PoA, a Spanish representative can handle all remaining steps without you travelling.

How to Set Up a Business in Spain from the UK: Step by Step

The steps below cover standard S.L. incorporation for a UK national completing the process remotely — the most common route. Realistic total timeline: 4–7 weeks from decision to a registered, operational company. The Spanish-side process moves quickly once UK documentation is received; the UK-side preparation is usually where delays occur.

Step 1 – Obtain Your NIE or Corporate NIF

Individual UK nationals apply at the Spanish Consulate (London, Edinburgh, or Manchester). UK Ltd shareholders must obtain a separate corporate NIF via Form 036 through the Agencia Tributaria, using a local representative with an active NIE.

Both identification numbers must be in place before the incorporation deed can be executed. Allow 2–4 weeks for NIE processing.

Step 2 – Prepare the Power of Attorney and UK Documentation

A bilingual PoA is prepared authorising a Spanish representative to act on your behalf at the notary. You sign before a UK Notary Public, submit for an FCDO apostille, and attach a sworn Spanish translation. Once the completed PoA is received in Spain, no further travel is required.

Step 3 – Reserve the Company Name

The proposed name is submitted to the Registro Mercantil Central for availability confirmation. Once approved, the Registry issues a name certificate with a limited validity period — move quickly to avoid reapplying.

Step 4 – Draft Articles of Association and Deposit Share Capital

Two tasks run in parallel here:

- Draft the estatutos (articles of association) covering the company's purpose, governance, share capital, and management structure

- Deposit the minimum share capital into a Spanish bank account in the company's name — the bank issues a deposit certificate required for the notarial deed

Step 5 – Execute the Notarial Deed

The deed of incorporation is signed at a Spanish notary by the authorised representative acting under the PoA. A provisional NIF is issued, and the company can begin operating commercially from this point.

Step 6 – Register with the Mercantile Registry and Activate Tax Obligations

The signed deed is filed with the provincial Mercantile Registry. While the company can trade from Step 5, full legal personality is only confirmed upon registration — which takes approximately 3 weeks. Following registration:

- Modelo 036 is filed with the Agencia Tributaria to obtain the definitive NIF and activate VAT (IVA) registration

- A digital certificate is activated for remote management of Spanish tax filings from the UK

- Where applicable, VIES/ROI registration is completed for intra-EU VAT operations

Tax and Compliance Essentials

Core Tax Obligations by Structure

| Tax | S.L. | Autónomo |

|---|---|---|

| Corporate/Income Tax | IS at 25% (or 15% for first two profitable tax years) | IRPF progressive scale |

| VAT (IVA) | Standard 21% | Standard 21% |

| Filing | Modelo 303 (VAT), annual IS return | Modelo 303, quarterly/annual IRPF |

UK companies importing or exporting goods to Spain need an EU EORI number — GB-prefixed EORI numbers are no longer valid for EU customs declarations after Brexit.

The 183-Day Rule: Critical for UK Entrepreneurs

Spending 183 or more days in Spain in a calendar year triggers Spanish tax residency. The consequences are significant:

- Worldwide income becomes taxable in Spain — including salary and dividends from a UK company — at IRPF rates up to 47%

- If a UK company's sole director manages the business from Spain, the Agencia Tributaria may treat Spain as the place of effective management and apply Spanish corporate tax to the UK entity's worldwide profits

Structure this before you relocate. Unwinding a poorly planned cross-border position — once the Agencia Tributaria has identified Spain as your place of effective management — can trigger back-taxes, penalties, and dual corporate exposure that far exceeds the cost of setting it up correctly from the start.

The Beckham Law (Article 93)

UK nationals relocating to Spain who qualify can elect a special tax regime offering:

- A flat 24% income tax rate on Spanish-source income up to €600,000

- Foreign-sourced income largely excluded from Spanish taxation

- Applies for the year of relocation plus five subsequent tax periods (up to six years total)

Eligibility conditions:

- Must not have been a Spanish tax resident in the five previous years (reduced from ten years under the Startup Law)

- Must meet employment or business activity conditions

- Applies directly to UK executives and entrepreneurs formally relocating to run Spanish operations, and to Digital Nomad Visa holders maintaining a UK client base

Conclusion

Starting a business in Spain from the UK is achievable, and for many entrepreneurs it's a genuinely strong strategic move. Brexit has made the process more structured, though. The NIE, visa decision, structure choice, and tax position all require careful planning that simply wasn't necessary before 2021.

The most common and costly mistakes — choosing the wrong structure, triggering unexpected tax residency, or encountering documentation errors on the Power of Attorney — are avoidable when the legal and compliance foundations are in place from the start. The practical next step is straightforward: get qualified cross-border legal and tax advice before you file anything, not after the first rejection letter arrives.

Frequently Asked Questions

Can a British citizen start a business in Spain?

Yes. British citizens can own 100% of a Spanish S.L. after Brexit with no nationality restrictions on shareholding. Brexit only changed immigration status — UK nationals who want to physically live and work in Spain need a visa, but those managing a Spanish company remotely from the UK do not.

How much money do I need to start a business in Spain?

For an S.L., the minimum share capital is €1 (though special reserve rules apply until €3,000 is reached). Setup costs include notary fees (€300–500), Mercantile Registry fees (€100–200), a company name certificate (~€20), plus UK-side notary and FCDO apostille costs. Autónomo registration costs far less (€250–600) but offers no limited liability protection.

Do I need a visa to start a business in Spain from the UK?

Only if you intend to physically live and work in Spain. Owning and incorporating a Spanish S.L. while remaining UK-based requires no visa. For those relocating, the three main routes are the Entrepreneur Visa, Self-Employed (Autónomo) Visa, and Digital Nomad Visa.

Can I run my UK company from Spain?

Yes, but it carries material risks. Spending 183+ days in Spain creates Spanish tax residency, making worldwide income — including UK dividends — taxable in Spain. Managing a UK company from Spain may also trigger a place of effective management assessment, exposing the UK entity to Spanish corporate tax. Get professional tax advice before relocating.

What is the 2-year rule in Spain?

In the Spanish business context, it refers to two things. First, newly incorporated S.L. companies pay a reduced 15% corporate income tax rate for their first two profitable fiscal years. Second, the Self-Employed Visa is granted for one year initially, with a two-year renewal available after demonstrating continued business activity.

Can I live in Spain on €4,000 a month?

€4,000/month comfortably covers living costs in most Spanish cities outside of central Madrid or Barcelona. According to Numbeo's 2026 data, a single person's monthly costs excluding rent in Madrid are approximately €826, with a city-centre one-bedroom flat averaging €1,417/month. Seville and Valencia are notably more affordable for those watching their budget.