For foreign companies entering India, this fragmentation is a genuine compliance trap. PT is capped at ₹2,500 per year per individual under Article 276 of the Indian Constitution, but state-level variation in rates, exemptions, and deadlines means that a single national policy simply doesn't exist. Non-compliance penalties — interest, late fees, and potential legal exposure — can far exceed the tax amount itself for employers with large workforces.

This guide covers what PT is, who must pay it, state-wise slab rates for major business hubs, and what employers need to do to stay compliant.

Key Takeaways

- PT is a state-level direct tax under Article 276 of the Constitution — not collected by the central government

- The constitutional ceiling is ₹2,500 per person per year, regardless of income

- Not all states levy PT; compliance obligations only arise in states where employees actually work

- Employers need two certificates: a Registration Certificate (to deduct employee PT) and an Enrolment Certificate (for the company's own PT liability)

- PT paid is deductible from gross salary under Section 16 of the Income Tax Act, 1961 (applicable under the old tax regime)

What Is Professional Tax in India?

Despite its name, professional tax is not limited to doctors, lawyers, or chartered accountants. It applies to all salaried individuals above a minimum income threshold — as well as self-employed professionals, business owners, and trading entities operating in PT-applicable states.

Constitutional and Legal Basis

Article 276 of the Constitution grants state legislatures the power to levy PT on income earned through employment, profession, trade, or calling. The article caps the maximum annual levy at ₹2,500 per person — setting a national ceiling despite state-level variation.

Collection is handled by each state's Commercial Taxes Department or designated municipal authorities — not central government agencies. Revenue stays within the state and is not shared with the Centre.

How PT Is Calculated

PT uses a slab-based structure:

- Each state defines income brackets with corresponding monthly or annual tax amounts

- Liability is calculated on gross salary or professional income — not net income

- States with higher thresholds show zero liability below that bracket

Where PT Does Not Apply

Not every part of India imposes PT. This is particularly relevant for foreign companies deciding where to establish operations or hire employees:

- Union territories (except Puducherry) do not levy PT, as they are governed centrally

- Several states have chosen not to impose PT at all — meaning employer obligations vary significantly by location

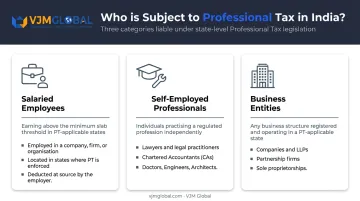

Who Must Pay Professional Tax in India?

PT applicability covers three broad categories:

- Salaried employees earning above the minimum slab threshold in PT-applicable states

- Self-employed professionals — lawyers, chartered accountants, doctors, engineers, and architects

- Business entities — companies, LLPs, partnerships, and sole proprietorships engaged in trade or profession

The Employer's Dual Obligation

Employers in PT-applicable states must obtain two separate certificates:

- PT Registration Certificate (PTRC) — authorises the employer to deduct and remit PT on behalf of employees

- PT Enrolment Certificate (PTEC) — covers the employer's own PT liability as a business entity

In states where a company has multiple offices, separate registration may be required per location. This is a frequently missed requirement for companies expanding across states.

Freelancers and Independent Contractors

Freelancers without employees are still required to register and pay PT directly if their income crosses the state's minimum threshold. This obligation is commonly overlooked, particularly by professionals working remotely for foreign clients.

Common Exemptions

Most states recognise exemptions for:

- Members of the armed forces

- Individuals with physical or mental disabilities (for example, Karnataka exempts those with at least 40% permanent disability)

- Salaried employees below the state's minimum income threshold (for example, below ₹25,000/month gross in Karnataka)

- Parents or guardians of differently-abled children (varies by state)

Each state publishes its own exemption schedule — check your state's PT authority directly for the current thresholds and qualifying conditions.

Foreign Companies Entering India

Applicability doesn't stop at domestic entities. Foreign companies hiring local employees must register for PT in each applicable state from day one — a requirement that applies regardless of whether the entity is a liaison office, branch, or wholly owned subsidiary. Multi-state operations mean multiple registrations, each with its own filing calendar and rates.

State-Wise Professional Tax Slab Rates in India

PT rates, income thresholds, and payment frequencies vary by state. States currently levying PT include: Karnataka, West Bengal, Maharashtra, Tamil Nadu, Andhra Pradesh, Telangana, Kerala, Gujarat, Assam, Bihar, Odisha, Meghalaya, Tripura, Madhya Pradesh, Jharkhand, Sikkim, Mizoram, and Puducherry.

Slab Rates for Key States

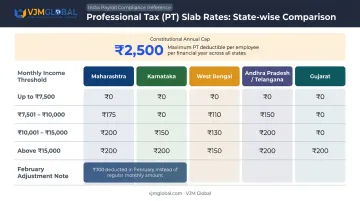

Maharashtra (Gender-differentiated slabs; source: MAHAGST PT Rate Schedule updated to 31 March 2025)

| Monthly Salary | PT — Men | PT — Women |

|---|---|---|

| Up to ₹7,500 | Nil | Nil |

| ₹7,501 – ₹10,000 | ₹175/month | Nil |

| Above ₹10,000 | ₹200/month (₹300 in February) | Nil below ₹25,000; ₹200/month (₹300 in February) above ₹25,000 |

The February adjustment keeps the annual total within the ₹2,500 constitutional cap.

Karnataka (Source: Karnataka PT FAQ, notification dated 15 April 2025)

| Monthly Gross Salary | Monthly PT |

|---|---|

| Below ₹25,000 | Nil |

| ₹25,000 and above | ₹200/month (₹300 in February) |

West Bengal

| Monthly Salary | Monthly PT |

|---|---|

| Up to ₹10,000 | Nil |

| ₹10,001 – ₹15,000 | ₹110 |

| ₹15,001 – ₹25,000 | ₹130 |

| ₹25,001 – ₹40,000 | ₹150 |

| Above ₹40,000 | ₹200 |

Andhra Pradesh and Telangana

| Monthly Salary | Monthly PT |

|---|---|

| Up to ₹15,000 | Nil |

| ₹15,001 – ₹20,000 | ₹150 |

| Above ₹20,000 | ₹200 |

For established professionals and companies in Telangana (more than 5 years standing): ₹2,500 per annum flat.

Tamil Nadu — Semi-annual basis. Maximum PT is ₹1,250 per half-year (₹2,500 annually), levied through local municipal and town panchayat bodies.

Kerala — Also collected on a half-yearly basis through the Local Self-Government Department. Rates were revised under GO (Sadha) No. 1149/2024/LSGD effective 1 October 2024.

Gujarat (Gandhinagar Municipal Corporation)

| Monthly Salary | Monthly PT |

|---|---|

| Below ₹12,000 | Nil |

| Above ₹12,000 | ₹200 |

Enrolment Certificate holders (traders and professionals): ₹2,000–₹2,500 per annum; EC payment due by 30 September.

States Where PT Is Not Applicable

Not every state levies PT. The following states impose no PT obligation — relevant if your India operations are concentrated in these regions:

Arunachal Pradesh, Goa, Haryana, Himachal Pradesh, Punjab, Rajasthan, Uttar Pradesh, and Uttarakhand.

A Note on Payment Frequency

Some states collect PT monthly (Maharashtra, Karnataka, West Bengal), while others use a semi-annual structure (Tamil Nadu, Kerala). The difference matters for payroll calendars — a missed semi-annual deadline in Tamil Nadu carries the same penalties as a missed monthly filing in Karnataka. Companies running multi-state payrolls need state-specific PT logic built into their payroll systems to avoid compliance gaps.

Professional Tax Compliance for Employers and Self-Employed Individuals

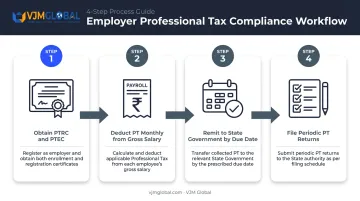

Employer Compliance Workflow

- Obtain PTRC and PTEC from the state tax authority — typically within 30 days of becoming liable (as required under states like Madhya Pradesh; verify your specific state's window)

- Deduct PT monthly from each employee's gross salary based on the applicable state slab

- Remit collected PT to the state government by the prescribed due date — commonly by the 20th of the following month in Karnataka, 15th in Maharashtra (for PTRC monthly returns)

- File periodic PT returns with payment proof as required by each state

Note that PTEC (enrolled person) payment deadlines differ from employer remittances. West Bengal enrolled persons must pay by 31 July each financial year; Gujarat's deadline is 30 September. Self-employed individuals follow the same enrolled-person schedule.

Self-Employed Professionals

Self-employed individuals must:

- Register independently with the state PT authority

- Compute their own liability based on income slab or occupational category

- Make direct payments — annually — through the state's online portal or designated bank

The Section 16 Income Tax Deduction

Under Section 16(iii) of the Income Tax Act, 1961 — confirmed by India Code — you can deduct PT paid during the financial year from your gross salary, reducing taxable income by up to ₹2,500 per year.

Important: This deduction applies under the old tax regime. Under the new tax regime (Section 115BAC), most deductions under Section 16 are not available unless specific provisions apply. Confirm your applicable regime before claiming the deduction.

Penalties for Non-Compliance with Professional Tax

Penalties are state-specific but follow a consistent pattern:

| Violation | Typical Penalty |

|---|---|

| Late registration | ₹20/day (Madhya Pradesh, verified); state-specific — check your state |

| Late payment interest | 1% per month (West Bengal); 2% per month (Madhya Pradesh) |

| Non-payment without cause | Up to 2% per month in some states |

| Late return filing | State-specific flat penalties; MP imposes ₹20/day for employer returns |

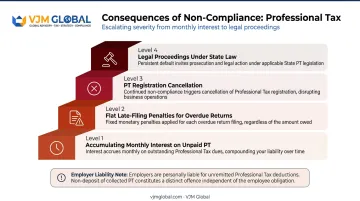

Escalating Consequences

Persistent non-compliance can result in:

- Accumulating interest on unpaid amounts (charged monthly)

- Flat late-filing penalties for returns submitted after due dates

- PT registration cancellation

- Potential legal proceedings under state law

Beyond penalties, there's a liability question that trips up many employers. If PT is not deducted from an employee's salary, the employer — not the employee — remains primarily liable to the state authority. PT deduction is a payroll control obligation, and state authorities will pursue the employer directly if it's missed.

Common Misconceptions About Professional Tax in India

Many businesses — especially foreign companies setting up Indian operations — carry incorrect assumptions about professional tax that lead to compliance gaps. Here are four misconceptions worth correcting:

PT Covers All Salaried Employees, Not Just Professionals

Professional tax applies to every salaried employee above the state's minimum income threshold — not just doctors, lawyers, or accountants. A factory worker, software engineer, and chartered accountant face the same PT obligation if their salary exceeds the applicable slab.

PT Rules Differ State by State

Rates, slabs, payment frequency, and applicability vary significantly across states. A company with offices in Mumbai, Bengaluru, and Chennai must comply with three independent sets of rules. There is no single national PT framework — each state legislates its own.

The ₹2,500 Cap Doesn't Make PT Low-Risk

The annual maximum of ₹2,500 per employee can mislead employers into treating PT as negligible. For companies with large workforces, cumulative non-compliance — across hundreds of employees, delayed remittances, and multi-state registrations — creates exposure that far exceeds the underlying tax amounts.

PTRC and PTEC Are Two Separate Requirements

These are commonly confused:

- PTRC (Registration Certificate): Authorises the employer to deduct PT from employees' salaries

- PTEC (Enrolment Certificate): Covers the business entity's own PT liability

Both certificates are required. Many first-time business registrants obtain only one and remain technically non-compliant for their entity's own PT obligation.

Frequently Asked Questions

How much is the professional tax in India?

PT varies by state and income slab. Monthly deductions for salaried employees typically range from nil to ₹200, with the constitutional cap at ₹2,500 per financial year per individual. Maharashtra and Karnataka both reach this annual maximum through a ₹300 February deduction.

How are professionals taxed in India?

Self-employed professionals pay PT directly to the state based on occupational standing or income tier — and separately pay income tax to the central government on their net professional income. These are two independent tax obligations under different legal frameworks.

Is professional tax applicable in all states in India?

No. PT is not levied in Arunachal Pradesh, Goa, Haryana, Himachal Pradesh, Punjab, Rajasthan, Uttar Pradesh, and Uttarakhand. Union territories (except Puducherry) are also exempt since they are governed centrally.

Can professional tax be claimed as a deduction in income tax returns?

Yes. PT paid is deductible from gross salary under Section 16(iii) of the Income Tax Act, 1961, reducing taxable income by the amount paid during the year. This deduction applies under the old tax regime only — it is not available under the new tax regime.

Who is responsible for deducting and paying professional tax — the employer or the employee?

Employers are legally responsible for deducting PT from employee salaries and remitting it to the state government. Employees do not pay PT directly unless they are self-employed or operate as independent contractors.

What are the penalties for not paying professional tax on time?

Late registration attracts daily penalties (₹20/day in Madhya Pradesh), while delayed payment draws interest of 1–2% per month depending on the state. Persistent non-payment can trigger additional penalties under state-specific PT legislation, so exact amounts vary by jurisdiction.