Introduction

Picture this: a US-based technology company pays a software consultant in India ₹5,00,000 for services rendered. Before the money lands in the consultant's account, a slice of that payment — 10% — must be withheld and sent directly to the Indian government. That's Tax Deducted at Source (TDS) in action.

TDS touches virtually every significant financial transaction in India: salary payments, bank interest, rent, contractor fees, royalties, and cross-border payments to foreign companies. For businesses new to India, the system can feel opaque — which sections apply, at what rates, when tax must be deposited, and what happens when something is missed.

Those gaps carry real cost. Non-compliance under TDS can trigger:

- Interest charges on late deposits

- Fees of ₹200 per day for missed return filings

- Penalties equal to the entire undeducted amount, plus disallowance of business expenses

This guide covers the full picture: how TDS works, current rate charts, return forms, certificates, due dates, NRI-specific rules, refunds, and the cost of non-compliance — so you can navigate the system with confidence.

Key Takeaways

- TDS is deducted by the payer (deductor) at payment or credit — whichever comes first — and deposited with the government on behalf of the recipient

- Rates vary by payment type; NRIs and foreign companies face higher withholding rates unless a DTAA benefit applies with proper documentation

- TDS must be deposited by the 7th of the following month (30th April for March deductions)

- Excess TDS beyond actual tax liability is refundable via ITR filing

- Non-compliance triggers interest, penalties, late fees, and potential 30% expense disallowance

What Is TDS and How Does It Work in India?

The Core Mechanism

Tax Deducted at Source is a withholding tax mechanism under Chapter XVII of the Income Tax Act, 1961. The person making a specified payment — an employer, bank, company, or tenant — deducts a prescribed percentage of tax before remitting the balance to the recipient, then deposits that deducted amount directly with the Central Government.

Two roles define the system:

- Deductor — the payer (employer, bank, company, tenant) who deducts and deposits the tax

- Deductee — the recipient (employee, contractor, landlord, professional) who receives the net payment and claims the deducted amount as credit against their total tax liability

Note on the Income-tax Act, 2025: The new Act came into force on 1 April 2026. For FY 2024–25 transactions, the Income-tax Act, 1961 and applicable Finance Act amendments govern. Rates and thresholds are largely similar under the new Act, but section numbers differ post-April 2026.

When Does TDS Apply?

TDS must be deducted at credit or payment, whichever is earlier. If a company books professional fees as a payable in March but physically pays in April, the March credit triggers the obligation — not the April payment.

Salary TDS under Section 192 works differently: it applies at the time of actual payment, not when the salary is accrued.

A Practical Example

A company engages a consultant for ₹1,00,000 in professional fees:

| Step | Amount |

|---|---|

| Gross invoice raised by consultant | ₹1,00,000 |

| TDS deducted at 10% (Section 194J) | ₹10,000 |

| Net payment to consultant | ₹90,000 |

| Amount deposited to government by company | ₹10,000 |

The consultant then reports ₹1,00,000 as gross income and claims ₹10,000 TDS credit when filing their return — reducing their net tax payable accordingly.

Why TDS Exists

This mechanism serves the government's tax administration goals in three direct ways:

- Ensures advance tax collection spread across the year, rather than a lump-sum at filing

- Reduces evasion by collecting tax at the transaction level before funds reach the recipient

- Widens the tax net by capturing income that would otherwise go unreported

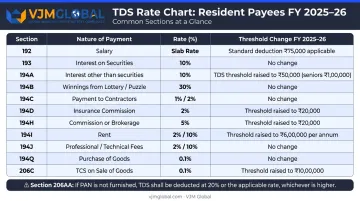

TDS Rate Chart: FY 2024–25 and FY 2025–26

Common TDS Rates (Resident Payees)

TDS rates are prescribed section-by-section under the Income Tax Act, and deduction only applies when the payment exceeds a specified threshold. The table below covers the most common payment categories for resident payees who have furnished their PAN.

| Section | Payment Type | Rate | Threshold (FY 2024–25) | FY 2025–26 Change |

|---|---|---|---|---|

| 192 | Salary | Applicable slab rate | N/A | Based on Finance Act slab rates |

| 194 | Dividend | 10% | ₹5,000 (non-cash) | No change |

| 194A | FD/Bank Interest | 10% | ₹40,000 (others); ₹50,000 (senior citizens) | ₹50,000 (others); ₹1,00,000 (senior citizens) |

| 194C | Contractor payments | 1% (individual/HUF); 2% (others) | Single payment ₹30,000; aggregate ₹1,00,000 | No verified change |

| 194H | Commission/Brokerage | 2% | ₹15,000 | No change |

| 194I | Rent — Land/Building | 10% | ₹2.40 lakh p.a. | Increased to ₹6 lakh p.a. |

| 194I | Rent — Plant/Machinery | 2% | ₹2.40 lakh p.a. | Increased to ₹6 lakh p.a. |

| 194IA | Immovable property sale | 1% | ₹50 lakh (consideration) | No verified change |

| 194IB | Rent by individual/HUF | 2% | ₹50,000/month | No verified change |

| 194J | Professional fees | 10% | ₹30,000 | Threshold increased to ₹50,000 |

| 194J | Technical services/call centre | 2% | ₹30,000 | Threshold increased to ₹50,000 |

The PAN Rule: Section 206AA

If the deductee fails to furnish their PAN, TDS must be deducted at the higher of the prescribed rate, the rate in force, or 20% under Section 206AA. This catches many foreign vendors off guard. Validating PAN before onboarding any vendor or payee is a baseline compliance requirement, not an optional step.

The rates above apply to resident individuals. NRI and foreign company rates are addressed in the next section.

TDS Compliance Roadmap: Returns, Certificates, and Due Dates

TDS Return Forms

Deductors file quarterly TDS returns with the Income Tax Department, reporting TAN, PAN of deductees, amounts deducted, and payment types. The key forms:

| Form | Purpose |

|---|---|

| Form 24Q | TDS on salary payments |

| Form 26Q | TDS on all non-salary payments to residents |

| Form 27Q | TDS on payments to non-residents (other than salary) |

| Form 26QB | TDS on sale of immovable property (Section 194IA) |

| Form 26QC | TDS on rent by individuals/HUF (Section 194IB) |

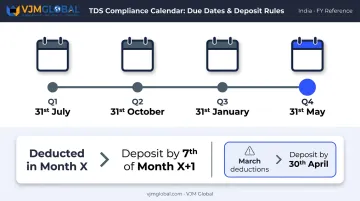

Quarterly return due dates:

| Quarter | Period | Due Date |

|---|---|---|

| Q1 | April – June | 31st July |

| Q2 | July – September | 31st October |

| Q3 | October – December | 31st January |

| Q4 | January – March | 31st May |

Forms 26QB and 26QC must be filed within 30 days from the end of the month in which TDS is deducted.

TDS Certificates

After filing returns, deductors must issue certificates to deductees as proof of deduction:

| Certificate | Covers | Due Date |

|---|---|---|

| Form 16 | Salary TDS (annual) | 15th June (not 31st May — a common misconception) |

| Form 16A | Non-salary TDS (quarterly) | Within 15 days of the TDS return due date |

| Form 16B | TDS on property purchase | Within 15 days after Form 26QB filing |

| Form 16C | TDS on rent | Within 15 days of Form 26QC due date |

Monthly TDS Deposit Deadlines

TDS deducted in any month must be deposited by the 7th of the following month, with one exception: TDS deducted in March can be deposited by 30th April. Payment is made online via the Income Tax e-Pay Tax portal using Challan ITNS 281 under the TAN of the deductor.

Tracking TDS via Form 26AS and AIS

Form 26AS is a consolidated tax credit statement linked to the deductee's PAN. It shows every rupee of TDS deducted and deposited on their behalf by various deductors. The Annual Information Statement (AIS) supplements this with broader transaction data.

TDS credit can only be claimed for amounts reflected in Form 26AS. If a deductor deducts tax but files an incorrect return, or deposits to the wrong PAN, the credit won't appear and the deductee cannot claim it. Always reconcile Form 26AS before filing your ITR to avoid credit mismatches and departmental notices.

TDS for NRIs and Foreign Companies

Section 195: The Non-Resident Withholding Rule

Payments made to non-residents (whether NRIs or foreign companies) fall under Section 195. The payer must deduct TDS on any sum chargeable to tax under the Act, at the rates in force, triggered at credit or payment — whichever is earlier.

Domestic TDS rates for non-residents are higher than those for residents:

| Income Type | Typical Domestic Rate |

|---|---|

| Interest income | 20% |

| Royalty | 20% |

| Fees for technical services (FTS) | 20% |

| Short-term capital gains (listed equity) | 20% |

| Long-term capital gains | 12.5% |

These rates apply before surcharge and cess, and the final effective rate can be higher depending on the payee's income level.

Claiming DTAA Benefits

India has DTAAs with 80+ countries, including the USA, UK, Australia, UAE, Canada, and Germany. A non-resident payee can claim a lower withholding rate under the applicable treaty — but documentation must be in place before the payment is made, not during refund season.

Documents required to claim DTAA benefits:

- Tax Residency Certificate (TRC): issued by the tax authority of the payee's country of residence

- Form 10F: required as a self-declaration when the TRC doesn't contain all prescribed details

- PAN: the Indian payer needs this to apply the reduced treaty rate

- Self-attested passport and visa copies confirming residency status

The treaty rate applies only when the payee is the beneficial owner of the income and the documentation trail is complete. Without TRC and Form 10F, the Indian payer must deduct at the higher domestic rate.

Foreign Company Compliance Obligations

A foreign company making payments that attract TDS in India must:

- Obtain a TAN — the 10-digit Tax Deduction and Collection Account Number issued by the Income Tax Department, required for all TDS-related filings

- File Form 27Q — quarterly returns for all payments made to non-residents

- Issue Form 16A — quarterly TDS certificates to non-resident payees

Non-compliance has a direct commercial cost: payments may be disallowed as business expenses, and the company faces interest and penalties on top of that.

VJM Global's Chartered Accountants assist foreign businesses across the full TDS compliance process: TAN registration, DTAA documentation, Form 27Q filing, and lower deduction certificate applications.

TDS Refunds and the Cost of Non-Compliance

How TDS Refunds Work

If total TDS deducted during the financial year exceeds actual tax liability — after applying deductions and exemptions — the excess is refundable, recovered by filing an ITR. For non-audit individuals, the normal deadline is 31st July (extended to 15th September 2025 for AY 2025–26).

Two points that often catch people off guard:

- TDS is not automatically 100% refundable — only the amount exceeding actual tax liability comes back

- If TDS equals tax due, there is no refund; if TDS falls short, the balance is owed by the individual

Getting the refund right matters — but avoiding penalties in the first place matters more.

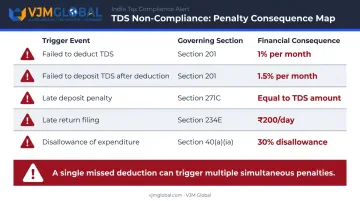

Penalties and Interest for Non-Compliance

| Consequence | Rate/Amount | Applicable When |

|---|---|---|

| Interest under Section 201 | 1% per month | From date tax was deductible to date of actual deduction |

| Interest under Section 201 | 1.5% per month | From date of deduction to date of actual deposit |

| Penalty under Section 271C | Equal to TDS not deducted | Failure to deduct TDS |

| Late filing fee under Section 234E | ₹200 per day (capped at TDS amount) | Delay in filing TDS returns |

| Business expense disallowance | 30% of the payment | TDS not deducted or not deposited on time |

Non-compliance rarely results in a single penalty. A missed deduction can simultaneously trigger interest from the deductible date, a penalty equal to the full TDS amount, and a 30% disallowance of the related expense — turning one oversight into three separate financial consequences.

Frequently Asked Questions

What is the TDS rate in India?

TDS rates vary by payment type: 10% on professional fees and FD interest, 1–2% on contractor payments, 2% on technical services and rent for plant/machinery, and the applicable slab rate on salary. The governing section of the Income Tax Act and whether the payee is a resident or non-resident both affect the applicable rate.

What is the TDS rate for NRIs in India?

Under Section 195, NRIs face TDS at 20% on interest and royalties, and 12.5–20% on capital gains depending on the asset type. To claim a reduced rate under an applicable DTAA, the NRI must provide a Tax Residency Certificate and Form 10F to the Indian payer before payment.

Is TDS 100% refundable?

Not always. Only the portion of TDS that exceeds actual tax liability for the year is refunded. If TDS deducted equals the tax owed, there is no refund. If TDS is less than the tax due, the individual must pay the shortfall.

Who is responsible for deducting TDS in India?

The deductor — the entity making the specified payment, whether an employer, company, bank, or tenant — is responsible for deducting TDS before making the payment and depositing it with the government within prescribed due dates.

What happens if TDS is not deducted or deposited on time?

Failure to deduct attracts interest at 1% per month from the due date; failure to deposit after deduction attracts 1.5% per month. A penalty equal to the undeducted TDS applies under Section 271C, and 30% of the related business expenditure may be disallowed when computing taxable income.

What is Form 26AS and why does it matter?

Form 26AS is a consolidated tax credit statement linked to the taxpayer's PAN, showing all TDS deducted and deposited on their behalf. TDS credit is only claimable for amounts that appear in Form 26AS, so reconciling it before filing any ITR is essential to avoid credit mismatches.