Introduction

For UK businesses operating in India — whether through a subsidiary, branch office, or direct hiring — payroll accounting is one of the most operationally complex functions to manage. The challenge is structural: UK employers work primarily with HMRC for PAYE and National Insurance, while Indian employers must register with and report to multiple central and state-level authorities, each with separate deadlines, forms, and penalty regimes.

India's payroll framework involves four distinct compliance layers that have no direct equivalent in the UK:

- Tax Deducted at Source (TDS) — income tax withheld at source by the employer

- Provident Fund (PF) — mandatory retirement contribution managed by the EPFO

- Employees' State Insurance (ESI) — health and social security for eligible employees

- Professional Tax — a state-level levy that varies by location

Attempting to replicate UK payroll practices without understanding these differences leads to compliance failures, financial penalties, and operational disruption.

This guide breaks down how Indian payroll accounting works, the obligations it creates, and where UK businesses most commonly go wrong when managing it for the first time.

Key Takeaways

- Indian payroll covers gross salary calculation, statutory deductions (PF, ESI, TDS, Professional Tax), disbursement, and government filings — all monthly.

- India's CTC model differs structurally from UK salary packages; misreading it leads to budget shortfalls.

- Compliance spans central laws (EPF, ESI, Income Tax Act) and state-level Professional Tax — with penalties for non-compliance.

- India's April–March tax year and Form 16 (equivalent to a UK P60) follow different deadlines than UK businesses expect.

- UK businesses can manage payroll via a registered Indian entity, outsource to a local payroll partner, or use an Employer of Record (EOR) for full compliance support.

What Is Payroll Accounting in India?

Indian payroll accounting is the end-to-end process of calculating employee compensation, applying statutory deductions, disbursing salaries, and maintaining compliance filings. It covers far more than just monthly salary transfers: it requires managing multiple government registrations, coordinating monthly remittances to separate authorities, and filing annual employee tax certificates.

How India Differs From UK PAYE

In the UK, employers primarily deal with HMRC for income tax and National Insurance contributions through a single PAYE system. Indian employers navigate a fundamentally different landscape:

| UK PAYE System | Indian Payroll System |

|---|---|

| Single authority (HMRC) | Multiple authorities (EPFO, ESIC, Income Tax Dept, state PT bodies) |

| One consolidated filing | Separate monthly deposits and filings for each authority |

| National Insurance contributions | PF (12% each side), ESI (4% total), Professional Tax (varies by state) |

| Tax year: April to April | Financial year: April to March |

Indian payroll accounting is governed by both central legislation (applicable nationwide) and state-level rules that vary significantly by location. A business operating in Mumbai faces different Professional Tax obligations than one in Bangalore or Delhi, where Professional Tax does not apply at all.

Understanding this patchwork of rules starts with knowing which laws apply to your operations.

Key Legislation

- Employees' Provident Funds & Miscellaneous Provisions Act, 1952: covers mandatory retirement savings under EPFO

- Employees' State Insurance Act, 1948: covers health and social insurance under ESIC

- Income Tax Act, 1961 (Section 192): covers tax deduction at source on salaries

- Payment of Wages Act, 1936: sets salary disbursement deadlines

- State Professional Tax Acts: levy employment taxes capped at ₹2,500/year by the Constitution

How Indian Payroll Accounting Works: The Step-by-Step Process

Indian payroll follows a structured monthly cycle with three phases: pre-payroll setup, payroll calculation, and post-payroll compliance. Understanding each phase helps UK businesses avoid compliance gaps from day one.

Step 1: Pre-Payroll Setup and Data Collection

Before payroll can run, UK businesses must ensure their Indian entity is registered with:

- EPFO (Employees' Provident Fund Organisation) – for PF contributions

- ESIC (Employees' State Insurance Corporation) – for ESI contributions

- State Professional Tax authority – for state-level employment tax

Each employee's records must be collected, including:

- PAN (Permanent Account Number – India's equivalent of a National Insurance number)

- Aadhaar (biometric identity number)

- Bank account details for salary transfer

- Salary structure breakdown (basic, HRA, allowances)

- Tax regime declaration (employees in India choose between the old and new income tax regime each year, which directly affects TDS calculations)

Step 2: Payroll Calculation

The payroll team (or software) calculates each employee's gross salary based on their CTC structure, adjusts for attendance, leaves, and variable pay, then applies statutory deductions:

Statutory Deductions:

- Provident Fund (PF): 12% of basic salary (employee contribution)

- Employees' State Insurance (ESI): 0.75% of gross wages (if applicable)

- Professional Tax: varies by state and salary slab

- Tax Deducted at Source (TDS): based on the employee's declared tax regime and projected annual income

Formula: Net Salary = Gross Salary − Total Deductions

Step 3: Salary Disbursement and Payslip Issuance

Once calculated, salaries are credited directly to employee bank accounts (typically via NEFT/bulk transfer through the company's Indian bank). Payslips are issued and must clearly itemise all earnings and deductions — Indian payslips are used by employees when filing their own annual income tax returns.

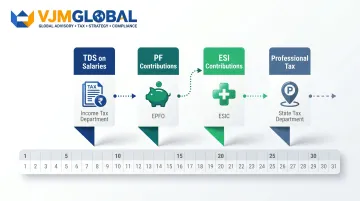

Step 4: Statutory Deposits and Monthly Filings

After disbursement, the employer must deposit:

| Obligation | Deadline | Authority |

|---|---|---|

| TDS on salaries | 7th of the following month | Income Tax Department |

| PF contributions | 15th of the following month | EPFO |

| ESI contributions | 15th of the following month | ESIC |

| Professional Tax | Varies by state | State tax department |

Each deposit must be accompanied by the correct government form or electronic filing.

Key Components of Indian Payroll Every UK Business Must Understand

Cost to Company (CTC)

CTC is the total annual cost an employer bears for an employee — a broader figure than the "gross salary" used in UK employment contracts. CTC includes:

- Basic salary (typically 40–50% of CTC)

- House Rent Allowance (HRA)

- Leave Travel Allowance (LTA)

- Special allowances

- Employer PF contributions (12% of basic)

- Employer ESI contributions (3.25% if applicable)

- Gratuity provisions

- Any other benefits

The employee's actual take-home is considerably less than the CTC figure — something that catches many UK employers off guard when reviewing offer letters. Basic salary forms the foundation on which PF, gratuity, and TDS are calculated, making its proportion within CTC critical.

Tax Deducted at Source (TDS)

TDS is the Indian equivalent of PAYE income tax withholding. Employers must:

- Calculate projected annual income for each employee

- Apply the applicable slab rates based on the employee's chosen tax regime (old or new)

- Deduct TDS evenly across each month

Income Tax Slabs for FY 2025-26:

| Income Slab (₹) | New Regime Rate | Old Regime Rate |

|---|---|---|

| Up to 2,50,000 | Nil | Nil |

| 2,50,001 – 4,00,000 | Nil | 5% |

| 4,00,001 – 8,00,000 | 5% | 5%–20% |

| 8,00,001 – 12,00,000 | 10% | 30% |

| 12,00,001 – 16,00,000 | 15% | 30% |

| 16,00,001 – 20,00,000 | 20% | 30% |

| 20,00,001 – 24,00,000 | 25% | 30% |

| Above 24,00,000 | 30% | 30% |

The new regime offers lower headline rates but eliminates most deductions (80C, 80D) and exemptions (HRA, LTA).

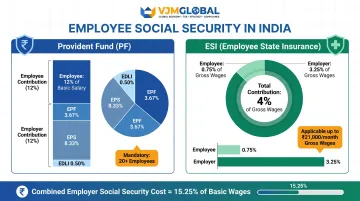

Provident Fund (PF)

Beyond income tax, employers must also manage social security contributions — starting with the Provident Fund. Both employer and employee contribute 12% of basic salary to the Employee Provident Fund (EPF). The employee contribution is deducted from salary; the employer's share is an additional cost on top of CTC.

Key Parameters:

- Mandatory for companies with 20 or more employees

- Wage ceiling of ₹15,000/month governs mandatory coverage

- Employer's 12% is split: EPF (3.67%), EPS – Pension (8.33%), EDLI – Insurance (0.50%)

- EPF interest rate for FY 2024-25: 8.25%

Unlike UK National Insurance — which applies to total earnings — PF is calculated on basic salary only. For UK employers structuring packages with a high basic component, this means PF costs can be higher than initially expected.

Employees' State Insurance (ESI)

ESI is applicable to employees earning gross salary up to ₹21,000/month, with:

- Employee contributing 0.75% of wages

- Employer contributing 3.25% of wages

Mandatory for companies with 10 or more employees. Combined, the total employer social security cost (PF + ESI) can reach approximately 15.25% of basic wages.

Statutory Compliance Obligations UK Businesses Must Meet

Running payroll in India means navigating multiple regulatory bodies simultaneously — each with its own portal, deadline, and penalty framework. Here's what UK businesses need to have in place before the first salary runs.

Employer Registration Requirements

Before hiring in India, a UK business operating through an Indian entity must register as an employer with:

- EPFO – via the OLRE (Online Registration of Establishments) portal

- ESIC – via the ESIC online portal

- State Professional Tax authority – via the respective state tax department

Without these registrations, statutory deductions cannot be remitted and penalties accumulate immediately.

Monthly Compliance Deadlines

| Obligation | Deadline |

|---|---|

| TDS deposit | 7th of the following month |

| PF and ESI contributions | 15th of the following month |

| Professional Tax deposit | Varies by state |

Annual Compliance Obligations

- Quarterly TDS returns: Filed in Form 24Q with the Income Tax Department

- Form 16: Annual TDS certificate issued to all employees by 15th June each year for the financial year ending 31st March (the Indian equivalent of a P60) — missing this deadline triggers employee complaints and potential regulatory scrutiny

- ESI returns: Filed half-yearly — covers both contribution periods (April–September and October–March) with a consolidated annual return also required

Payment of Wages Act and Minimum Wages Act

Salary Disbursement Deadlines:

| Establishment Size | Payment Deadline |

|---|---|

| Fewer than 1,000 employees | 7th of the following month |

| 1,000 or more employees | 10th of the following month |

Employers must pay at least the applicable state minimum wage for each employee's role category. Minimum wages vary by state, industry, and zone — Maharashtra skilled workers earn approximately ₹14,650–18,065/month depending on zone and industry (as of January 2025).

Consequences of Non-Compliance

Missing any of the above deadlines isn't just an administrative inconvenience — penalties are automatic and non-negotiable:

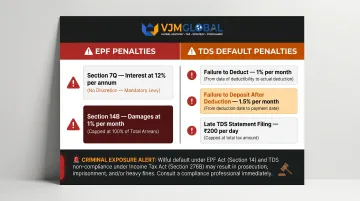

EPF Penalties (Two-Part Framework):

| Penalty Type | Rate/Amount |

|---|---|

| Section 7Q – Interest | 12% per annum on overdue contributions (no discretion to reduce) |

| Section 14B – Damages | 1% per month (capped at 100% of arrears) under new regime from June 2024 |

TDS Default Interest:

| Default Type | Rate |

|---|---|

| Failure to deduct TDS | 1% per month |

| Failure to deposit TDS after deduction | 1.5% per month |

| Late filing of TDS statement | ₹200 per day (capped at tax amount) |

Wilful default carries criminal exposure — up to 1 year imprisonment under the EPF Act and up to 3 years under the ESI Act.

Common Mistakes UK Businesses Make with Indian Payroll

Treating Indian Salary Offers Like UK Packages

The most common structural mistake is offering a "gross salary" without accounting for employer-side PF, ESI, and gratuity provisions. This means the actual cost to the company is higher than the figure stated in the offer letter, leading to budget miscalculations. CTC must be modelled correctly from the start.

For example, offering an employee ₹12,00,000 CTC means:

- Basic salary: ₹4,80,000–6,00,000 (40–50% of CTC)

- Employer PF: 12% of basic = ₹57,600–72,000

- Employer ESI: 3.25% if applicable

- Gratuity accrual, admin charges, etc.

The employee's net take-home will be substantially lower than ₹12,00,000 after statutory deductions.

Missing India's Monthly Deposit Deadlines

UK businesses accustomed to quarterly PAYE settlements often miss India's monthly deposit deadlines for TDS (7th), PF and ESI (15th), resulting in interest and penalty accruals that could have been avoided entirely with a proper payroll calendar. State-level Professional Tax deadlines vary further, compounding compliance risk for businesses operating across multiple states.

Applying One-Size-Fits-All Payroll Structures

A third common error is applying the same salary structure and deductions across all Indian employees without accounting for:

- State-level Professional Tax slabs (₹0 in Delhi vs. ₹2,500/year in Maharashtra)

- Employees' individual tax regime choices (old vs. new)

- ESI eligibility thresholds (₹21,000/month)

Each employee's payroll calculation must be individually managed based on location, salary level, and personal tax elections.

Many UK businesses find it practical to engage a specialised local payroll partner to manage these variables. VJM Global has supported over 250 UK businesses with Indian payroll and compliance, helping them avoid penalties and stay on the right side of statutory requirements.

Frequently Asked Questions

How does payroll work in India?

Indian payroll is a monthly process involving salary calculation based on the CTC structure, deduction of statutory contributions (TDS, PF, ESI, Professional Tax), salary disbursement to employee bank accounts, and filing of returns with the relevant government departments.

What is CTC in India payroll?

CTC (Cost to Company) is the total annual expenditure an employer incurs for an employee, including basic salary, allowances, employer PF contributions, gratuity accrual, and other benefits. After statutory deductions, the employee's actual take-home pay will always be lower than the CTC figure.

What are the 4 types of payroll systems?

The four main approaches are:

- Manual or spreadsheet-based payroll

- Dedicated payroll software

- Fully outsourced payroll (third-party provider)

- Employer of Record (EOR) model

For UK businesses new to India, outsourcing or an EOR arrangement is typically the practical choice for managing compliance complexity.

Which payroll software is used in India?

Popular platforms include Keka, greytHR, RazorpayX Payroll, Zoho Payroll, and ADP. Software alone does not ensure compliance, though — most foreign businesses pair it with local accountants or outsourced payroll specialists familiar with Indian labour law.

How is Indian payroll different from UK PAYE?

Unlike UK PAYE, which routes all employer tax obligations through a single HMRC system, Indian payroll requires separate registrations and filings with multiple authorities (EPFO, ESIC, Income Tax Department, state Professional Tax body), has a different financial year (April–March), and uses the CTC structure rather than a simple gross salary model.

Do UK businesses need to register separately in India to run payroll?

Yes — a UK business must have a legally recognised Indian entity (such as a private limited company, branch office, or liaison office) or use an EOR before it can employ staff in India. Once that entity exists, it must separately register with EPFO, ESIC, and the relevant state Professional Tax authority before processing any payroll.