Introduction

Many companies with Singapore-listed entities or subsidiaries are still navigating a question that carries real compliance risk: what exactly does your auditor now have to disclose — and to whom?

Singapore's SSA 701 (aligned with ISA 701) replaced the binary pass/fail audit opinion with something far more detailed. Audit reports must now surface the most significant risks identified and addressed during the audit. Effective for financial statements covering periods ending on or after December 15, 2016, this reflects Singapore's broader push toward investor transparency.

Yet many organizations — particularly foreign multinationals — remain unclear on what Key Audit Matters (KAMs) are, what must be disclosed, and what these obligations mean in practice. That ambiguity creates compliance exposure and squanders an opportunity to build genuine investor confidence.

Key Takeaways

- KAMs are the matters auditors judge most significant when auditing financial statements — each must explain why it mattered and how the auditor responded

- Mandatory for audits of listed entities in Singapore; also applies to certain public interest entities and voluntary adopters

- Enhanced KAM reporting improves transparency and helps investors make better-informed decisions

- Audit reports must describe the auditor's approach for each KAM, not just flag that it exists

- Average 2.3 KAMs per entity were reported in Singapore during the first year of implementation

What Are Key Audit Matters (KAMs)?

Key Audit Matters are precisely defined by SSA 701, Paragraph 8 as "those matters that, in the auditor's professional judgement, were of most significance in the audit of the financial statements of the current period. Key audit matters are selected from matters communicated with those charged with governance."

The origin of KAMs traces back to the IAASB's 2015 revised auditor reporting standards. Singapore adopted these through the Singapore Standards on Auditing (SSA), issued by the Institute of Singapore Chartered Accountants (ISCA) under the oversight of ACRA.

The standards became effective for periods ending on or after December 15, 2016, making Singapore one of the early adopters globally, alongside the UK, Australia, and the Netherlands.

That adoption was driven by a clear need. The purpose of KAMs, according to SSA 701, is to "enhance the communicative value of the auditor's report by providing greater transparency about the audit that was performed." In the aftermath of the financial crisis, investor demands for more informative auditor's reports increased, prompting the profession to raise its reporting standards.

Criteria for Determining KAMs

Auditors use three specific criteria outlined in SSA 701, Paragraph 9 to identify KAMs:

- Higher assessed risk of material misstatement: includes significant risks identified under SSA 315 (Revised 2021) that required heightened audit attention

- Significant management judgment: areas where financial statements involved complex estimates or high estimation uncertainty, requiring the auditor to evaluate judgment calls carefully

- Significant events or transactions: matters arising during the period whose scale or nature materially affected the direction of audit work

KAMs are not a separate audit opinion on individual matters, nor a substitute for required disclosures in the financial statements. They are insights into the audit process itself, intended to provide transparency to report users.

The auditor selects from a broader pool of matters communicated to those charged with governance (TCWG) and determines which were of "most significance" — a judgment call that means the number and nature of KAMs will naturally vary by company and year.

Singapore's Regulatory Framework for Enhanced Auditor Reporting

Singapore's Accounting and Corporate Regulatory Authority (ACRA) adopted the revised auditor reporting standards with SSA 701 on "Communicating Key Audit Matters in the Independent Auditor's Report" becoming effective for financial periods ending on or after December 15, 2016. This early adoption positioned Singapore alongside the UK, Australia, and the Netherlands as global leaders in enhanced auditor reporting.

SGX Listing Rules reinforce the obligation. Rule 211A(3) requires that annual financial statements of SGX Mainboard and Catalist-listed companies must be audited in accordance with Singapore Standards on Auditing. Since SSA 701 is part of that framework, KAM reporting is mandatory for all SGX-listed issuers. This means companies are expected to:

- Address relevant KAMs in their financial statement disclosures

- Reference KAMs within their annual report where appropriate

- Align KAM disclosures with the auditor's findings — not issue generic, templated language

Beyond the compliance scope, there is a direct technical link between SSA 701 and SSA 315 (Revised). KAM identification is grounded in the risk assessment process — the auditor's procedures for identifying and assessing risks of material misstatement under SSA 315 directly feed into which matters get elevated to KAM status.

ACRA's practice monitoring reviews have put KAM quality under increasing scrutiny. The 2024 Audit Regulatory Report flagged "Auditor's report" as one of the top recurring inspection finding themes — showing that regulators want substantive KAM disclosures, not generic language.

The Audit Quality Indicators (AQI) disclosure framework adds another layer. It requires audit firms to publish measurable data on audit quality — such as partner-to-staff ratios, training hours, and inspection results — making it easier for investors and boards to assess whether the auditor behind a KAM disclosure has the capacity to support it.

What Must Be Included in a KAM Disclosure

SSA 701, Paragraph 13 specifies two mandatory components for every KAM description:

- Why the matter was significant — why it was considered one of the most significant matters in the audit and therefore determined to be a key audit matter

- How the matter was addressed — the key procedures performed and the auditor's response to the identified risk or judgment area

Each KAM must also include a cross-reference to the related disclosure(s) in the financial statements, ensuring report users can locate the corresponding management disclosures for context.

Drafting Considerations for Quality KAM Disclosures

A high-quality KAM disclosure is specific and tailored — not generic or boilerplate. SSA 701 Paragraph A44 states that "relating a matter directly to the specific circumstances of the entity may also help to minimize the potential that such descriptions become overly standardized and less useful over time."

Paragraph A47 reinforces this, directing auditors to relate the matter "directly to the specific circumstances of the entity, while avoiding generic or standardized language."

Regulators globally have flagged low-specificity disclosures as a quality concern. The UK FRC criticized "KAMs that are generic rather than specific," particularly regarding fraud in revenue recognition. An analysis by Germany's Institut der Wirtschaftsprüfer (IDW) of UK and Dutch reports found there was "less 'boiler plate' language than anticipated."

Achieving that specificity depends on effective internal coordination. The engagement partner, component auditors (in group audits), and TCWG must align during KAM drafting. The group engagement team must communicate potential KAMs to component auditors so that audit responses are adequately documented and reflected in the report.

KAMs cannot substitute for:

- The auditor's opinion

- Emphasis of matter paragraphs

- The going concern section

- Other required communications

Each serves a distinct purpose in the auditor's report.

Who Is Required to Report KAMs in Singapore?

SSA 701, Paragraph 5 states: "This SSA applies to audits of complete sets of general purpose financial statements of listed entities and circumstances when the auditor otherwise decides to communicate key audit matters in the auditor's report. This SSA also applies when the auditor is required by law or regulation to communicate key audit matters in the auditor's report."

In practice, this means:

- Mandatory for all SGX-listed companies — both Mainboard and Catalist issuers must have their auditors communicate KAMs

- Voluntary for non-listed entities — unlisted companies may elect to include KAMs

- Required when mandated by law or regulation — certain sectors or public interest entities beyond listed companies may have specific requirements

Foreign multinationals with Singapore-listed subsidiaries or statutory audit requirements in Singapore are subject to SSA 701. Their appointed Singapore-based auditors must comply, a point worth noting for overseas parent companies that may be unfamiliar with Singapore auditing standards. In these cases, coordinating between parent-level and subsidiary-level audit teams is essential to ensure proper alignment with local frameworks like SSA 701.

Common Key Audit Matters in Singapore Companies

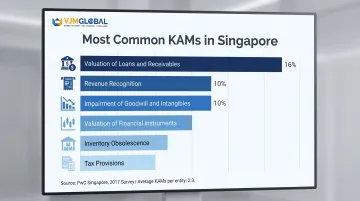

PwC Singapore's 2017 survey found an average of 2.3 KAMs per entity in Singapore during the first year of implementation, closely comparable to Hong Kong's average of 2.2. The most frequently reported KAM categories were:

Most Common KAMs in Singapore:

- Valuation of loans and receivables — reported in 16% of audits, most common in financial sector companies

- Revenue recognition (10%) — especially for companies with complex multi-element contracts or long-term contracts

- Impairment of goodwill and intangible assets (10%) — requiring significant management judgment in cash flow projections and discount rate assumptions

Other Common KAMs:

- Valuation of financial instruments — especially for financial sector and investment holding companies

- Inventory obsolescence — as illustrated by Singapore-listed companies like MegaChem, where inventory impairment methodology was flagged as a KAM across multiple years

- Tax provisions and uncertain tax positions

- Acquisition accounting and purchase price allocation

Financial sector companies in Singapore (banks, insurance firms) tend to disclose a higher volume and more complex KAMs due to regulatory complexity, asset opacity, and the judgment-intensive nature of financial reporting. United Overseas Bank (UOB)'s FY2016 audit report, for example, covered three KAMs: goodwill impairment, impairment of loans to customers, and valuation of illiquid or complex financial instruments.

KAMs are not fixed — they shift year to year as a company's circumstances change. Audit committees and management should engage with auditors early in the audit cycle to understand which areas auditors are likely to flag before fieldwork begins.

Benefits of Enhanced KAM Reporting for Stakeholders

Investor Perspective

KAMs reduce information asymmetry by giving shareholders and investors direct insight into where significant risks or judgments lie in the financial statements. Research confirms that KAM disclosure can effectively reduce information asymmetry and improve the information environment.

The Securities Investors Association Singapore (SIAS) welcomed KAMs as a direct response to investor demand for greater transparency. SIAS's guide highlights that KAMs "provide investors with deeper understanding of the significant risk areas in the financial statements" — giving shareholders more targeted questions to raise with directors, management, and auditors at AGMs.

Governance Ripple Effect

The investor benefits are only part of the picture. ACCA's research on the first year of KAM implementation globally — including Singapore — identified three benefits that extend well beyond investor information:

- Audit committees gain a structured new focus for discussions with auditors, strengthening corporate governance at the board level

- Audit quality improves because supervisors expect documented responses in working papers for every identified KAM, reducing the risk of superficial work in high-risk areas

- Financial reporting quality rises as companies proactively expand disclosures to align with the KAMs their auditors flag

Taken together, these effects mean KAMs do more than inform investors — they raise the standard of the entire audit and reporting cycle.

Frequently Asked Questions

Are key audit matters only for listed companies?

KAMs are mandatory for listed entities under SSA 701 in Singapore, but the standard also applies when required by law or regulation, or when the auditor elects to include KAMs for non-listed entities. KAMs are not exclusively for listed companies.

What should be included in key audit matters?

Each KAM must cover three elements:

- Why the matter was of most significance in the audit

- How the matter was addressed during the audit

- A cross-reference to the related financial statement disclosure

How does the auditor determine which matters qualify as KAMs?

Auditors select KAMs from matters communicated to those charged with governance. Key selection criteria include higher assessed risk of material misstatement, significant management judgment, and significant events or transactions during the period.

What are some common examples of key audit matters in Singapore?

Common examples include revenue recognition, goodwill and intangible asset impairment, inventory valuation, tax provisions, and financial instrument valuations. Financial services firms, for instance, tend to see more KAMs around instrument valuations, while manufacturers more often flag inventory and impairment.

How many KAMs should be included in an audit report?

SSA 701 sets no fixed number: the quantity reflects the auditor's judgment about which matters were most significant. Singapore companies averaged 2.3 KAMs in the first year of implementation, though regulators caution against both boilerplate over-listing and artificially restricting the count.

What is the difference between KAMs and an emphasis of matter paragraph?

An emphasis of matter paragraph draws attention to a matter already properly disclosed in the financial statements that is fundamental to users' understanding, while KAMs are a broader mechanism for communicating the most significant audit matters. The two serve different purposes and are governed by separate standards (SSA 706 vs SSA 701).