Introduction

For Singapore-incorporated groups and multinationals with Singapore entities, a qualified audit opinion can surface at the worst possible moment: before a funding round, a banking review, or a regulatory filing. The root cause is often a group audit process that wasn't well understood until something went wrong.

A group audit is the structured examination of consolidated financial statements covering a parent company and all its subsidiaries, producing a single unified audit opinion. It sits at the intersection of Singapore's Companies Act requirements and ACRA's oversight — and errors or omissions at this level can damage lender relationships, trigger regulatory scrutiny, and erode investor confidence.

Despite how frequently the term appears in Singapore's corporate governance conversations, the division of responsibilities between the group auditor and component auditors — and the sequence in which work actually happens — is rarely explained clearly. This guide walks through who does what, under which standards, and where the common pressure points arise.

Key Takeaways

- Group audits cover consolidated financial statements of parent companies and subsidiaries treated as a single economic entity

- Triggered when SFRS 10 requires consolidation; governed by SSA 600 (Revised)

- Structured across five phases: planning, risk assessment, component coordination, fieldwork, and consolidation review

- Key complexity drivers include materiality thresholds, component auditor competence, intercompany eliminations, and cross-border operations

- Small company exemptions may apply to individual entities, but don't eliminate the parent's group audit obligation

What Is the Group Audit Process and When Does It Apply in Singapore?

A group audit is the process by which a group auditor (typically the parent company's auditor) examines consolidated financial statements and issues an opinion reflecting the financial position of the entire group as a single economic entity. It's not simply multiple standalone audits combined; the group auditor must account for intercompany eliminations, component-level risks, and work performed by component auditors across multiple entities.

How a Group Audit Differs from a Statutory Audit

- A statutory audit covers one legal entity's standalone financials

- A group audit addresses consolidation adjustments, cross-entity risks, and reliance on other auditors

- The group auditor directs the entire engagement and bears full professional responsibility

Legal Triggers Under Singapore Law

When a parent company controls one or more subsidiaries — through majority ownership or the ability to direct financial and operational policies — it must prepare consolidated financial statements under SFRS 10 (Consolidated Financial Statements). Control exists when the parent has:

- Power over the subsidiary

- Exposure or rights to variable returns

- The ability to use that power to affect returns

Once consolidation is required, a group audit follows in accordance with SSA 600 (Revised), effective for periods beginning on or after 15 December 2023.

Scoping: How Auditors Identify Significant Components

Under the existing SSA 600, group auditors identify "significant components" — subsidiaries that are either financially material (typically using a 15% benchmark of chosen metrics like assets or revenue) or carry higher audit risk due to operational complexity.

SSA 600 (Revised) moves away from this binary classification toward a risk-based scoping approach. Significant components receive intensive audit procedures, while lower-risk entities may undergo limited analytical review — allowing teams to allocate resources where they matter most.

Why Group Audits Are Critical in Singapore's Regulatory Environment

Singapore ranked 4th globally in the 2025 Global Financial Centres Index, a position built on regulatory transparency, strict enforcement, and capital security. ACRA regulates 732 Accounting Entities and 1,232 Public Accountants, with listed and Public Interest Entity (PIE) audits subject to particularly intense scrutiny.

Consolidated financial statements of listed companies and large groups are governance requirements — enforced through practice monitoring inspections, not optional compliance exercises.

Consequences of deficient group audits:

Without proper execution, risks compound:

- Incomplete eliminations inflate revenue or assets through intercompany transaction errors

- Undetected subsidiary risks remain invisible to boards and investors

- Breaches of SFRS or SSA 600 trigger qualified opinions, regulatory action, and reputational damage

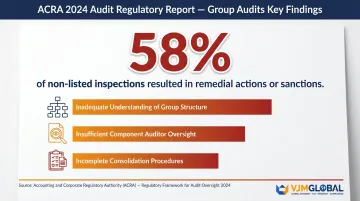

ACRA's 2024 Audit Regulatory Report identifies group audits as one of the five top deficiency themes. In the non-listed segment, 58% of inspections resulted in remedial actions or sanctions, with common failures including inadequate understanding of the group structure, insufficient component auditor oversight, and incomplete consolidation procedures.

Regulatory framework:

Group audits must comply with SSA 600, which mirrors ISA 600 and governs the group auditor's responsibilities for planning, component oversight, and consolidated reporting. ACRA oversees public accountants conducting these audits under the Accountants Act 2004, and breaches can result in suspension, PIE restrictions, or registration cancellation. Enforcement orders issued in recent years confirm the regulator acts on these standards.

How the Group Audit Process Works: Step-by-Step

The group audit unfolds simultaneously across entities, geographies, and auditor teams. The group auditor remains ultimately responsible for the entire opinion, while component auditors execute subsidiary-level work under detailed instructions from the centre.

Step 1: Planning and Scope Definition

The group auditor maps the full group structure—all subsidiaries, joint ventures, and associated entities—and determines which are in scope. Decisions are based on:

- Financial materiality

- Risk profile

- Regulatory requirements

- Prior-year findings

The output is a documented audit strategy setting overall group materiality and defining the nature, timing, and extent of procedures required at each component.

Step 2: Risk Assessment

Risk assessment operates at two levels:

Group-level risks:

- Accuracy of consolidation adjustments

- Related-party transactions

- Foreign currency translation

Component-level risks:

- Internal control weaknesses

- Local regulatory compliance gaps

- Fraud indicators

Auditors use quantitative analysis (financial impact modelling) and qualitative analysis (governance quality, management credibility) to prioritize high-risk areas and allocate resources accordingly.

Step 3: Coordination with Component Auditors

For groups with overseas subsidiaries or entities audited by different firms, the group auditor issues formal instructions detailing:

- Scope of work

- Materiality thresholds

- Timelines

- Specific risk areas

Critical requirement: The group auditor must assess component auditor competence and independence before relying on their work. SSA 600 requires evaluation of:

- Professional competence

- Understanding of SSAs

- Independence compliance

- Willingness to cooperate

Effective communication channels—written instructions, status calls, structured responses—are essential because the group auditor remains responsible for the overall opinion even when delegating component work.

Step 4: Fieldwork and Testing

Component auditors conduct fieldwork at their respective entities, performing:

- Substantive testing: Verifying transactions, balances, disclosures

- Controls testing: Evaluating design and operating effectiveness of internal controls

- Analytical procedures: Identifying unusual trends or anomalies

The group auditor reviews component work papers to confirm they meet required standards and sufficiently address identified risks before incorporating findings into the group-level assessment.

Step 5: Consolidation, Reporting, and Follow-Up

The group auditor consolidates findings from all components, covering:

- Elimination of intercompany balances and transactions

- Review of consolidated financial statements for completeness and SFRS compliance

- Preparation of the auditor's opinion for presentation to the board or audit committee

A thorough group audit also includes follow-up reviews in subsequent periods to verify that management has implemented recommended remedial actions—tracking whether control weaknesses identified in one cycle are resolved before the next.

Key Factors That Affect the Group Audit Process in Singapore

Materiality Thresholds

Group materiality is set at the consolidated level, but component materiality must be lower to ensure aggregated errors across entities don't exceed the group threshold. SSA 600 requires consideration of aggregation risk when setting component performance materiality—the lower the component materiality, the more extensive the testing required, directly affecting timelines and cost.

The ACRA 2024 report specifically cites failure to determine group and component materiality during planning as a common deficiency.

Component Auditor Quality and Jurisdiction

When subsidiaries are located in countries with weaker auditing infrastructure or different local standards, the group auditor must perform additional procedures. SSA 600 permits:

- Direct testing of components by the group auditor

- Additional review of component auditor work papers

- Site visits to component locations

- Expanding the scope of procedures communicated to component auditors

If the group engagement team concludes component auditor work is insufficient, it must determine what additional procedures are needed, who will perform them, and evaluate the impact on the group audit opinion if evidence remains inadequate.

Complexity of Intercompany Transactions

Groups with frequent, high-volume intercompany sales, loans, cost-sharing arrangements, or management fee structures require rigorous elimination procedures. SSA 600 mandates that the group auditor evaluate the appropriateness, completeness, and accuracy of consolidation adjustments and reclassifications, including intercompany eliminations.

Errors in intercompany reconciliations are a leading cause of consolidated statement misstatements, particularly for Singapore holding companies with regional operating subsidiaries. ACRA inspections specifically examine whether group auditors have performed sufficient work on these consolidation adjustments.

Cross-Border Regulatory and Reporting Differences

Subsidiaries operating under IFRS, US GAAP, or other local GAAPs require conversion to SFRS for consolidation purposes. The group auditor must verify these conversion adjustments. SFRS 110 requires uniform accounting policies across all entities in the group for like transactions and events in similar circumstances.

For multinational groups with Singapore as the holding jurisdiction, this adds technical complexity that extends audit timelines. Firms with access to international accounting networks—such as EAI International member firms—can coordinate directly with local auditors in each jurisdiction, reducing conversion errors and keeping the audit on schedule. VJM Global's EAI International membership supports exactly this kind of cross-border coordination.

Common Misconceptions About Group Audits in Singapore

Misconception: Group audits are just multiple standalone audits combined

In reality, the group auditor cannot simply add up component audit opinions. SSA 600 requires active direction, oversight, and integration of component work under a single audit strategy — the group auditor retains full professional responsibility for the consolidated opinion, regardless of how much work was delegated to components.

Misconception: Once component auditors are engaged, the group auditor's role becomes passive

Reality: The group auditor must continuously assess whether component work is sufficient, whether additional procedures are required, and whether the combined evidence supports the opinion being issued. ACRA inspection findings specifically flag cases where group auditors failed to verify that component auditors obtained sufficient appropriate evidence.

Misconception: Audit materiality thresholds are the same across all group entities

Reality: Each component requires its own materiality threshold, set lower than the group-level figure. Components with higher risk profiles may warrant even tighter thresholds. Applying a single uniform materiality figure across the entire group is one of the audit quality failures most frequently cited in ACRA inspections.

When a Group Audit May Not Be Required

Not every company within a group structure automatically requires a full audit. Under Section 205C of the Companies Act, a subsidiary qualifying as a "small company" may be exempt from statutory audit at the entity level if it meets at least two of three criteria for the two preceding financial years:

- Annual revenue ≤ S$10 million

- Total assets ≤ S$10 million

- ≤ 50 employees

One important distinction: component-level exemptions don't eliminate the parent's obligations. The group audit at the parent level remains required if the group as a whole exceeds the small group thresholds (measured on a consolidated basis) — regardless of individual subsidiary sizes.

That said, not every component within an audited group receives the same level of scrutiny. Non-significant components with low financial materiality and minimal risk exposure may be subject to reduced procedures:

- Analytical review only (ratio analysis, trend comparisons)

- Limited specified procedures targeting high-risk balances

- No full component audit required

The group auditor must document the rationale for any reduced scope and confirm that the evidence gathered remains sufficient and reliable at the consolidated level.

Frequently Asked Questions

What qualifies as a group audit in Singapore?

A group audit is required when a parent company must prepare consolidated financial statements under SFRS 10—when it controls one or more subsidiaries. The audit must comply with SSA 600 and results in a single opinion covering the consolidated group financials.

What are the audit requirements in Singapore?

Singapore companies must have financial statements audited annually under the Companies Act, unless they qualify for small company or small group audit exemption. Audits must be conducted by a public accountant registered with ACRA and comply with Singapore Standards on Auditing.

What is the process of a group audit in Singapore?

The process follows five phases: planning and scope definition, risk assessment, coordination with component auditors, fieldwork and testing, and consolidation and reporting—all conducted under the group auditor's overall direction in accordance with SSA 600.

What is the difference between a group auditor and a component auditor?

The group auditor directs the entire engagement and holds full professional responsibility for the opinion on consolidated financial statements. Component auditors perform work on individual subsidiaries, but the group auditor evaluates and integrates their findings before issuing the final report.

Can a Singapore company be exempt from a group audit?

A parent company qualifies for group audit exemption if the entire group meets "small group" criteria under the Companies Act—satisfying at least two of these three consolidated thresholds:

- Revenue ≤ S$10 million

- Total assets ≤ S$10 million

- 50 or fewer employees

If any two thresholds are exceeded, a group audit is required regardless of individual subsidiary sizes.