Introduction

Many Singapore businesses arrive at a UAE bank's doorstep with a folder full of documents — and still get turned away. Opening an offshore bank account in Dubai is entirely achievable, but the process is more demanding than most business owners expect when they first look into it.

Dubai's banking system operates differently from traditional offshore jurisdictions. UAE banks require physical presence for KYC verification, residency documents for certain account types, and extensive business documentation that catches many applicants off guard.

Unlike the British Virgin Islands or Cayman Islands — which historically allowed remote onboarding — Dubai banks enforce strict in-person verification protocols under Central Bank of the UAE (CBUAE) guidance. Preparation is not optional here; it's what separates approvals from rejections.

This guide walks through what Dubai offshore banking actually means for Singapore companies, why they use it, how to open an account step by step, and which compliance obligations you must satisfy before submitting your first application.

Key Takeaways

- UAE residency (Emirates ID) is required for standard corporate accounts — non-residents typically need a UAE offshore entity (JAFZA/RAK ICC)

- Minimum balances range from AED 10,000 to AED 50,000, with non-resident corporate accounts often facing higher thresholds

- Onboarding takes 2–8 weeks and typically requires in-person KYC at a UAE branch

- Dubai is fully CRS-compliant—Singapore's IRAS receives automatic reporting on your UAE accounts annually

- Offshore accounts are legal for Singapore businesses, provided all foreign income is declared to IRAS

What "Offshore Banking in Dubai" Actually Means for Singapore Companies

For a Singapore business, "offshore banking in Dubai" typically refers to either a non-resident corporate account at a UAE-licensed bank, or an account held by a UAE offshore entity such as JAFZA Offshore or RAK ICC. It does not imply secrecy or tax evasion.

Singapore companies have three structural paths to consider:

- Personal non-resident account – Limited scope, harder to open without high net-worth relationship tiers

- UAE Free Zone LLC – Operationally active entity (IFZA, RAKEZ, DMCC) with stronger bank acceptance for transactional banking

- UAE offshore company – JAFZA Offshore or RAK ICC for holding structures or investment vehicles, subject to stricter due diligence

Your choice of structure directly affects how — and whether — you can access UAE banking at all.

How Dubai Differs from Other Offshore Jurisdictions

Unlike BVI or Cayman Islands, Dubai bank accounts cannot typically be opened remotely without UAE residency or physical presence. The CBUAE's November 2025 guidance permits non-face-to-face verification but imposes significantly higher compliance burdens. As a result, most major UAE banks continue to require in-person KYC.

What "Offshore" Does Not Mean Here

UAE banks apply full AML/KYC protocols, CRS automatic exchange of information, and UBO disclosure requirements. Singapore business owners should not expect privacy from IRAS. The UAE began automatic CRS exchanges in September 2018, and Singapore lists the UAE as a CRS participating jurisdiction.

| Feature | Free Zone LLC | Offshore IBC (JAFZA/RAK ICC) |

|---|---|---|

| Legal form | Limited Liability Company | International Business Company |

| Physical presence | Office/facility lease required in free zone | No physical office required |

| Banking acceptance | Generally stronger | Stricter due diligence; some banks decline |

| UAE corporate tax | 0% on qualifying income if substance met; 9% otherwise | Subject to CT if managed in UAE |

Why Singapore Businesses Open Offshore Bank Accounts in Dubai

Singapore and the UAE are significant trade partners — bilateral merchandise trade reached S$24 billion in 2024. For businesses with Middle East, Africa, or South Asian supply chains, a UAE account allows direct processing of AED, USD, and regional currencies, cutting out double conversion costs entirely.

The tax case is straightforward on paper, but requires careful reading:

- Dubai charges no personal income tax, and Free Zone entities qualify for 0% corporate tax on eligible income

- Singapore's corporate rate sits at 17%

- UAE corporate tax of 9% applies to taxable income above AED 375,000 for financial years from 1 June 2023 onward

- Free Zone status preserves the 0% rate, but only with genuine economic substance in the UAE

Beyond tax, Dubai operates as a politically stable, internationally recognized financial hub. It ranked 7th globally in the GFCI 39 (March 2026) — its highest-ever position — with strong correspondent banking networks that support reliable international wire transfers.

UAE banks also offer multi-currency accounts covering AED, USD, EUR, and GBP, useful for businesses collecting revenue across regions. Holding funds across jurisdictions further reduces exposure to any single country's financial or regulatory disruptions.

Step-by-Step: How to Open a Dubai Offshore Bank Account as a Singapore Business

High-level sequence:

- Entity structure selection

- Document preparation

- Bank pre-screening

- In-person KYC in Dubai

- Account activation and go-live

Skipping or rushing any step significantly increases rejection risk.

Step 1: Choose the Right Entity Structure

Three structure options and when each suits a Singapore business:

- Free Zone LLC (IFZA, RAKEZ, DMCC): Best for operational accounts with active suppliers or clients. Requires a physical office, trade license, and employees — but carries the strongest bank acceptance of the three options.

- JAFZA Offshore or RAK ICC: Best for holding structures or investment vehicles. No physical office required, but expect heightened scrutiny and slower onboarding due to the limited operating footprint.

- Personal non-resident accounts: Limited in scope and difficult to open without high-net-worth relationship tiers.

Free Zone LLCs have significantly stronger bank acceptance than offshore IBCs. Banks compensate for IBCs' limited operating footprint by applying deeper due diligence — which translates to longer timelines and higher rejection rates.

Step 2: Assemble Your KYC and Business Documentation

Core documents UAE banks require from Singapore corporate applicants:

- Valid passports of all shareholders and signatories

- Proof of address (utility bill or bank statement, recent)

- Company incorporation documents: ACRA BizFile business profile, Constitution, share certificates

- 6-12 months of business bank statements

- Source of funds evidence: invoices, contracts, purchase orders

- UBO declaration and ownership chart (tracing individuals with 25%+ ownership)

- Business plan with expected transaction flows and account purpose

A complete document pack at submission reduces back-and-forth delays by several weeks.

Step 3: Select a Bank and Conduct a Pre-Screening Call

UAE banks that commonly accept non-resident or offshore corporate clients:

| Bank | Confirmed Minimum Balance | Key Notes |

|---|---|---|

| FAB (First Abu Dhabi Bank) | AED 10,000 | Multi-currency capability; competitive tariff structure |

| Emirates NBD | AED 50,000 (sole proprietor) | Fall-below fee AED 250+VAT/month |

| Mashreq Bank | Not publicly listed | Offers dedicated non-resident account product |

| ADCB | Not publicly listed | Business banking services available |

| HSBC UAE | Not publicly listed | International account; can open in 20+ destinations |

| Standard Chartered UAE | Not publicly listed | Focus on international commercial banking |

| Wio Bank | No minimum deposit | Fully digital onboarding; Emirates ID required |

Critical: Conduct pre-screening calls with relationship managers before committing, as bank risk appetite changes frequently. Non-resident corporate accounts may carry higher undisclosed minimums than published retail/SME thresholds.

Step 4: Travel to Dubai for In-Person KYC

Once a bank confirms preliminary eligibility, final KYC almost always requires the authorized signatory or shareholder to appear in person at a UAE branch. Pre-screening can be done remotely, but identity verification cannot.

The CBUAE's November 2025 guidance permits non-face-to-face verification, but it imposes additional controls. In practice, most major banks still require or strongly prefer physical presence.

Strategic tip: Obtaining a UAE residency visa (Emirates ID) during this visit unlocks more banking options, including Wio Bank, which can subsequently be managed remotely.

Step 5: Account Activation and Go-Live

After in-person KYC approval, accounts typically activate within 2-8 weeks. Start with predictable, documented transactions that match the narrative submitted during onboarding. Sudden deviations in transaction patterns trigger manual reviews and can freeze payments.

Documents, Entity Structures, and Minimum Balance Requirements

Documents, Entity Structures, and Minimum Balance Requirements

KYC Documents for Singapore Corporate Applicants

Dubai banks require a consistent set of KYC documents from Singapore-registered companies. Prepare these before you begin the application:

- ACRA BizFile business profile

- Certificate of Incorporation

- Audited financial statements (if available)

- Valid passports and proof of address for all UBOs

- 6-12 months of business bank statements

- Source of funds evidence

- UBO declaration and ownership chart

- Business plan with transaction flows

Minimum Balance Requirements

With documents in order, your next planning consideration is the minimum balance each bank expects. Confirmed minimums range from AED 10,000 (FAB) to AED 50,000 (Emirates NBD). The AED 100,000–500,000 range cited in industry commentary is not uniformly confirmed by official bank sources, and non-resident corporate profiles may face higher undisclosed thresholds. Banks charge monthly fall-below fees whenever your balance dips under the required minimum.

Entity Structure and Due Diligence Timelines

The type of entity you operate through also affects how banks assess your application. JAFZA Offshore and RAK ICC companies face stricter due diligence and slower onboarding compared to Free Zone LLCs. Singapore businesses using offshore IBC structures should build extra lead time into their banking timeline from the outset.

Singapore Tax and Compliance Obligations Before You Open

Singapore Tax and Compliance Obligations Before You Open

CRS Reporting: What IRAS Already Knows

Singapore is a CRS participant. UAE banks have exchanged financial information under CRS since September 2018. IRAS receives automatic reporting on accounts held by Singapore tax residents.

Singapore business owners must declare foreign accounts and any income earned — the data is already flowing whether you report it or not.

Singapore's Legal Requirements for Offshore Accounts

Holding an offshore bank account is legal for Singapore businesses. However, foreign-sourced income is generally taxable when remitted to Singapore.

Key rules to know:

- Tax reliefs are available under Section 13(8) of the Income Tax Act 1947 for qualifying foreign-sourced dividends, branch profits, and service income

- Failure to declare income earned in foreign accounts is illegal

Interaction with UAE Corporate Tax

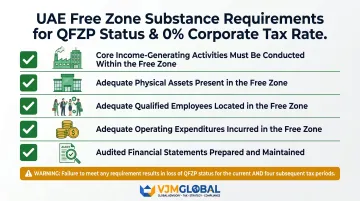

As of financial years starting June 2023, UAE corporate tax at 9% applies to profits above AED 375,000. Free Zone entities can access 0% on qualifying income but must meet substance requirements:

- Performing Core Income-Generating Activities (CIGA) within the Free Zone

- Maintaining adequate physical assets and employees

- Incurring adequate operating expenditures

- Preparing audited financial statements (mandatory regardless of revenue)

- Complying with the arm's length principle for related-party transactions

Failure to meet these conditions results in loss of QFZP status for that tax period and the subsequent four tax periods.

Getting Professional Advice

Singapore businesses using UAE entities for tax planning should seek qualified cross-border tax advice to ensure both Singapore and UAE obligations are met. An international tax advisory firm with cross-border compliance expertise can help structure your UAE presence and reporting obligations correctly before problems arise.

Common Mistakes and Misconceptions Singapore Businesses Make

Assuming Dubai Works Like BVI or Cayman Islands

The most common misconception is that Dubai accounts can be opened remotely without physical presence or residency. UAE banking is operationally oriented and requires in-person KYC — which catches many Singapore business owners off guard, especially those used to fully remote account opening.

Under-Documented Applications

Submitting an incomplete KYC pack is the leading cause of rejection or extended delays. Banks routinely flag applications missing:

- UBO (Ultimate Beneficial Owner) charts

- Source-of-funds documentation

- A clear written business rationale

Treat the bank application like a formal due diligence exercise, not a routine account opening.

Choosing the Wrong Entity Structure

Incorporating a JAFZA offshore company when you actually need active transactional banking will attract slower onboarding and heavier scrutiny compared to a Free Zone LLC. Match your structure to your banking needs before you incorporate — reversing this after the fact is costly.

No Genuine Economic Nexus

If your Singapore business has no real trade, investment, or operational connection to the UAE or Middle East, banks will likely decline the application. Economic rationale must be demonstrable, not constructed after the fact.

CBUAE guidance requires banks to identify the "intended purpose and nature of the relationship" and confirm that actual account activity matches the stated purpose. Weak or vague answers here are a fast route to rejection.

Frequently Asked Questions

Frequently Asked Questions

Is Dubai good for offshore banking?

Dubai is a strong offshore banking hub for businesses with genuine Middle East, Africa, or South Asia trade links. It offers multi-currency accounts, a stable regulatory environment, and 0% personal income tax. However, it is not a secrecy jurisdiction and requires full AML/KYC compliance with CRS reporting to Singapore's IRAS.

Can offshore companies open a bank account in Dubai?

UAE offshore companies (JAFZA Offshore, RAK ICC) can open UAE bank accounts on a selective basis, subject to clear business purpose, transparent UBO disclosure, and documented source of funds. Acceptance rates are lower than for operational Free Zone LLCs due to stricter due diligence requirements.

Can a foreigner open a bank account in Dubai?

Foreigners and non-residents can open accounts at select UAE banks under premium or corporate relationship tiers. In-person KYC is almost always required, and minimum balance thresholds are significantly higher than for residents, with non-resident corporate profiles typically carrying higher undisclosed minimums beyond standard published ranges.

What's the minimum deposit for an offshore account?

UAE banks typically require minimum balances of AED 10,000 to AED 50,000, though non-resident corporate accounts often carry higher undisclosed thresholds. Monthly fall-below fees apply if the balance drops below the minimum, so confirm exact requirements directly with your target bank.

Is it illegal to have offshore bank accounts?

Holding an offshore bank account is entirely legal for Singapore businesses, provided all foreign accounts and income earned are properly declared to Singapore's IRAS and comply with CRS reporting obligations. The illegality arises only from non-disclosure or tax evasion, not from the account itself.