The challenge is that the process looks different depending on your business structure, residency status, and whether you're physically in the US. Many applicants show up at a bank with the wrong documents, or skip entity formation entirely, and wonder why they're turned away.

This guide covers everything you need: what documents to gather, how the application works step by step, which account types suit different businesses, and what foreign nationals specifically need to navigate the process successfully.

Key Takeaways

- A US business bank account separates personal and business finances, simplifies tax compliance, and helps build business credit

- You'll need a registered business entity, an EIN, government-issued ID, and entity-specific formation documents

- Foreign nationals can open a US business account, though expect additional requirements: ITIN or passport, notarized documents, and possibly an in-person branch visit

- Online applications are available at most banks and fintech platforms; some complete in under 15 minutes if documents are ready

- Business registration and EIN must come first; most banks won't open an account without them

What Is a Business Bank Account in the USA?

A US business bank account is a deposit account held in the name of a legally registered business entity, kept separate from the owner's personal finances. It's used to receive income, make payments, and manage business cash flow. The FDIC insures business deposits separately from personal deposits — up to $250,000 per ownership category — provided the entity is validly formed and engaged in independent activity.

The SBA identifies three primary account types most US businesses use:

| Account Type | Primary Use |

|---|---|

| Business checking | Daily transactions — payments in and out |

| Business savings | Cash reserves, earns interest |

| Merchant services | Accepts customer card payments; fees vary by transaction type |

Business accounts aren't reserved for large companies. Entities that commonly open one include:

- Sole proprietors managing client payments

- Single-member LLCs separating business and personal funds

- Startups establishing financial infrastructure early

- Foreign-owned US entities receiving domestic revenue

Most banks offer tiered account options scaled to transaction volume — so the right account depends on how your business is structured and how actively it operates.

What You Need Before Opening a US Business Bank Account

Incomplete documentation is the single most common reason business bank account applications get delayed or rejected. Getting your paperwork in order before you approach a bank saves significant time.

Most banks require your business to be legally registered before opening an account — meaning you'll need to choose a structure (LLC, corporation, sole proprietorship, or partnership) and file formation documents with the appropriate state authority.

The EIN Requirement

An Employer Identification Number (EIN) is a nine-digit tax ID issued by the IRS, required by nearly all banks for any entity other than a sole proprietor using their SSN. The IRS EIN application is free and takes minutes online — provided your principal place of business is in the US and you hold a valid US taxpayer identification number.

International applicants without an SSN must apply by fax, phone, or mail using IRS Form SS-4.

Personal Documents Required

Regardless of entity type, every applicant typically needs:

- Government-issued photo ID (passport or driver's license)

- SSN or ITIN (for non-US citizens without an SSN)

- Valid US business address

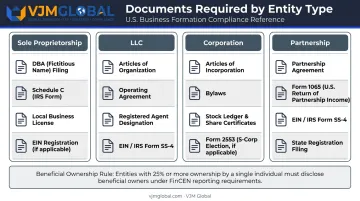

Entity-Specific Formation Documents

| Entity Type | Documents Required |

|---|---|

| Sole proprietorship | SSN or EIN; DBA/Assumed Name certificate if operating under a trade name |

| LLC | Articles of Organization, Operating Agreement, EIN, EIN Assignment Letter |

| Corporation | Articles/Certificate of Incorporation, corporate resolution authorizing account opening, EIN |

| Partnership | Partnership Agreement, Certificate of Limited Partnership or LLP registration, EIN, ID for all general partners |

KYC and Beneficial Ownership

Banks also require business details — estimated monthly transaction volume, number of employees, and business purpose — as part of their Know Your Customer (KYC) compliance process. Under 31 CFR 1010.230, any individual owning 25% or more of a legal entity must provide personal identification and complete a beneficial ownership certification form.

These requirements can be complex for international applicants. VJM Global works with foreign founders and multinationals to prepare accurate entity formation documents and KYC submissions — reducing the back-and-forth that typically delays account approvals.

Why Open a Business Bank Account in the USA?

A 2023 NFIB survey found 97% of small business owners maintain a separate business bank account. That near-universal adoption makes sense — the benefits span legal protection, day-to-day operations, and long-term credit-building.

Legal Protection

For LLCs and corporations, keeping business funds separate from personal funds is a legal expectation, not an optional best practice. Mixing the two risks "piercing the corporate veil" — a legal doctrine that can expose personal assets in lawsuits or audits. A dedicated account reinforces the separation that makes limited liability meaningful.

Operational Benefits

- Accept payments in the business name, not your personal name

- Delegate banking authority to employees or accountants

- Access business credit lines and financing

- Maintain cleaner books that simplify tax filing

Credit Building

A dedicated business account builds your company's independent financial identity. As Bank of America notes, business credit scores track how a company manages its accounts separately from personal borrowing history.

Lenders, suppliers, and insurers all rely on this business credit profile to assess risk. A strong profile opens doors to better loan terms, favorable vendor agreements, and smoother growth financing.

How to Open a US Business Bank Account: Step by Step

Step 1 – Register Your Business and Obtain Your EIN

Register your chosen business structure with the appropriate state authority, then apply for an EIN from the IRS. Both are required before most banks will process your application.

US-based applicants can complete the IRS online EIN application in minutes at no cost. International applicants without an SSN must use the Form SS-4 fax or phone route instead.

Step 2 – Choose the Right Account Type and Bank

Decide what you need before comparing options:

- Basic checking for daily operational transactions

- Savings account for maintaining cash reserves

- Merchant services if you'll accept card payments from customers

When comparing banks, evaluate these factors:

- Monthly maintenance fees and minimum balance requirements

- Transaction limits

- Online and mobile banking capabilities

- Integration with accounting software

- ATM access and cash deposit options

- Availability of business credit lines

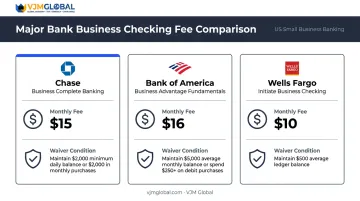

Fee examples from major banks:

| Bank | Account | Monthly Fee | Waiver Condition |

|---|---|---|---|

| Chase | Business Complete Banking | $15 | $2,000 minimum daily balance |

| Bank of America | Business Advantage Fundamentals | $16 | $5,000 combined average balance or $500 in debit purchases |

| Wells Fargo | Initiate Business Checking | $15 | $2,000 minimum daily balance |

Online-first platforms like Mercury, Relay, and Novo often have faster approval times and fewer branch requirements — useful if you're not near a US branch.

Step 3 – Gather All Required Documents

Compile your documents based on your entity type before starting any application. Common requirements across most banks include:

- Business formation documents (Articles of Incorporation, LLC Operating Agreement, or DBA certificate)

- EIN confirmation letter from the IRS

- Government-issued photo ID for all account signers

- Business license or proof of address, depending on your state

For entities with multiple owners, all individuals above the 25% beneficial ownership threshold must provide personal ID and complete ownership certification forms.

Incomplete documentation is the leading cause of delays — double-check your entity type requirements against the bank's specific checklist before submitting.

Step 4 – Submit Your Application

Two routes are available depending on your entity type and circumstances.

Most major banks and all fintech platforms accept online applications. Mercury advertises a 10-minute application, with debit cards typically arriving within 7–10 business days of approval. Chase allows online applications for sole proprietorships and single-member LLCs, but requires a branch visit for multi-member LLCs and more complex structures.

In-person branch visits are required by some banks for complex entity types, foreign applicants, or accounts needing cash deposit capabilities. Traditional banks generally offer broader services — credit lines and in-branch support — than digital-only platforms.

Step 5 – Make Your Initial Deposit and Activate the Account

Most banks require an initial deposit to activate the account. Wells Fargo's Initiate account requires a $25 opening deposit; some digital platforms have no minimum. Once active:

- Set up online and mobile banking access

- Authorize any additional users or accountants

- Connect the account to accounting software

- Configure payment processing integrations

Can Foreigners and Non-US Residents Open a US Business Bank Account?

Yes — foreign nationals and non-US residents can legally open a US business bank account. The path involves additional steps, but it's well-established.

The ITIN Alternative to an SSN

Foreign nationals without a Social Security Number need an Individual Taxpayer Identification Number (ITIN), obtained by filing IRS Form W-7. The IRS typically processes ITIN applications within 7 weeks (or 9–11 weeks during peak tax season). Some banks accept a valid passport directly instead of an ITIN; others specifically require one.

Additional Documentation for Foreign Applicants

Beyond the standard requirements, foreign applicants typically need:

- Proof of US business address (a registered agent address is acceptable at most banks, though fintech platforms like Mercury and Relay explicitly exclude PO boxes and virtual mailboxes)

- Certified or notarized copies of formation documents

- Certificate of Authority if the business was formed in a different state

In-Person Requirements

Many traditional US banks require non-US residents to appear in person at a US branch. Chase accepts passports and Matricula Consular cards as primary ID for non-US citizens. However, several fintech platforms handle foreign-owned businesses entirely online:

- Mercury: Accepts non-US citizens and non-residents; requires US-registered business with US operations

- Relay: Accepts non-US citizen and non-resident owners; requires US physical address (no virtual mailboxes)

- Brex: Requires US EIN, valid US incorporation, and US operations

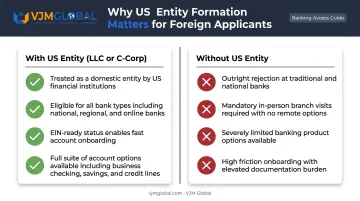

Why US Entity Formation Is the Critical First Step

A foreign-owned US LLC or C-Corp — properly formed under state law with a valid EIN — is treated as a domestic legal entity for banking purposes. Without that domestic entity, foreign businesses typically face outright rejection at traditional banks, mandatory in-person branch visits, and a much narrower set of account options. Entity formation remains the right first step for international entrepreneurs entering the American market.

VJM Global works with international business owners on the cross-border compliance groundwork — entity structure, EIN registration, and tax identification — that underpins a smooth US bank account application. Their New York office (447 Broadway, 2nd Floor, New York, NY 10013) supports clients at this stage of US market entry.

Conclusion

Opening a US business bank account is manageable once the foundation is in place: a registered business entity, a valid EIN, and the right documentation for your structure. Most delays come from skipping formation steps or arriving at the bank with an incomplete document set.

Foreign nationals have a clear path, but preparation matters more than in domestic cases. Getting entity registration and EIN right the first time removes most of the friction.

Once the account is open, it enables you to:

- Manage US finances through a dedicated, compliant structure

- Accept professional payments from American clients and platforms

- Build business credit under your registered entity

- Establish a professional presence with US customers and vendors

If you're navigating this process from outside the US — or setting up a US entity as part of a broader market entry strategy — VJM Global's business setup and advisory team can help you get the structure right before you walk into the bank.

Frequently Asked Questions

What is required to open a business bank account in the USA?

You need a registered business entity, an EIN (or SSN for sole proprietors), government-issued photo ID, entity-specific formation documents, and an initial deposit. Exact requirements vary by entity type and bank — LLCs and corporations require formation documents that sole proprietorships don't.

Can a foreigner open a business bank account in the USA?

Yes. Foreign nationals typically need a US-registered business entity with an EIN, a valid passport or ITIN, and notarized formation documents. Some traditional banks require an in-person branch visit; fintech platforms like Mercury and Relay often allow fully remote applications.

Is it safe to keep $500,000 in one US bank?

FDIC insurance covers up to $250,000 per depositor, per insured bank, per ownership category. For balances above that threshold, spread funds across multiple FDIC-insured institutions — separately chartered banks insure deposits independently.

Do I need an EIN to open a business bank account in the USA?

Most entity types — LLCs, corporations, partnerships — require an EIN. Sole proprietors may use their SSN, but an EIN is strongly recommended: it protects personal information and is required once you hire employees or work with vendors who need a tax ID.

Can I open a US business bank account online?

Many banks and fintech platforms allow fully online applications, often finished in 10–15 minutes. Traditional banks may still require a branch visit for complex entity types or foreign nationals, while digital-first platforms like Mercury, Relay, and Novo offer simpler remote processes.

How long does it take to open a US business bank account?

Timelines range from a few minutes (digital platforms with complete documents) to several business days for traditional banks requiring additional verification. Most online platforms complete the application in under 10 minutes; debit cards typically arrive within 7–10 business days after approval.