Introduction

Picture this: It's April 30th, three days before your corporate income tax filing deadline. You're digging through shoeboxes of faded receipts, trying to match transactions from nine months ago to cryptic bank statement entries.

Your accountant is asking for invoices you can't find. That supplier payment from August? Unrecorded. And IRAS just sent a compliance notice requesting documentation for the past five years.

This scenario plays out across Singapore every tax season, costing SME owners far more than stress. Between July 2020 and June 2023, IRAS recovered S$79 million in taxes and penalties from companies with erroneous Corporate Income Tax returns — two-thirds flagged by AI-powered analytics targeting poor record-keeping.

For Singapore SMEs, sound bookkeeping is a compliance obligation under IRAS and ACRA, a foundation for growth decisions, and your clearest defence against costly audits. This guide covers the essential tips, compliance requirements, and when outsourcing becomes the smarter call.

TLDR: Key Takeaways

- Separate business and personal finances immediately—IRAS scrutinizes co-mingled accounts during audits

- IRAS requires financial records retained for five years from the relevant Year of Assessment

- Monthly reconciliation and consistent recording prevent costly errors and audit exposure

- Outsourcing makes financial sense once monthly transactions exceed 50–100 or GST registration kicks in

- GST-registered businesses must maintain additional records once annual turnover crosses S$1 million

What is Bookkeeping for SMEs and Why It Matters

Bookkeeping is the systematic process of recording, organising, and maintaining every financial transaction flowing through your business—income, expenses, invoices, payments, refunds, and transfers. It differs from accounting: bookkeeping captures the daily transactions, while accounting analyses and interprets those records to prepare financial statements, compute taxes, and guide business decisions.

For Singapore SMEs, bookkeeping carries legal weight. ACRA requires all companies to maintain proper accounting records under Section 199 of the Companies Act, regardless of size or revenue. IRAS depends on these records to assess your tax obligations accurately.

Poor records create compounding risks:

- Inaccurate tax filings lead to penalties and surcharges

- Disallowed expense claims trigger best-judgement assessments (where IRAS estimates your tax liability based on incomplete data)

- Missing documentation raises audit red flags that are costly to resolve

Beyond compliance, accurate books give you real-time visibility into cash flow, profit margins, and spending patterns. You can spot cost overruns before they spiral and identify which products or services actually drive profitability.

That visibility matters more than ever right now. In the QBE SME Survey 2025, two-thirds of Singapore SMEs cited rising costs and shrinking margins as their biggest challenge. For businesses operating on tight margins, clean books aren't just a compliance requirement—they're how you find the dollars worth saving.

Singapore's Bookkeeping Compliance Requirements SMEs Must Know

IRAS Record-Keeping: The Five-Year Rule

IRAS mandates that all businesses—companies, sole proprietors, partnerships, and GST-registered entities—maintain proper records and retain them for at least five years from the relevant Year of Assessment (YA).

Note the five years starts from the YA, not the transaction date. A 2023 transaction assessed in YA 2024 must be retained until at least 2029.

What Records You Must Keep

IRAS defines "proper records" across three categories:

| Record Type | Required Documents |

|---|---|

| Income | Invoices issued, sales receipts, cash register tapes, rental agreements, tax invoices |

| Expenses | Supplier invoices, payment vouchers, receipts, contracts, import permits |

| Supporting Documents | Bank statements (business accounts only), general ledgers, financial statements, stock lists, payroll records |

Digital records are acceptable, but must be accurate and readily retrievable. IRAS explicitly states that keeping only bank statements is insufficient—you need source documents to prove every transaction. Estimates and incomplete records are not acceptable.

ACRA's Financial Statement Requirements

Under the Companies Act Section 199, every Singapore company must maintain accounting records that "sufficiently explain the transactions and financial position of the company." All companies must prepare and file annual financial statements with ACRA.

Audit exemption applies to small companies meeting at least two of these criteria for two consecutive years:

- Total annual revenue not exceeding S$10 million

- Total assets not exceeding S$10 million

- Employees not exceeding 50

Even audit-exempt companies must still prepare unaudited financial statements—which depends entirely on clean, organised bookkeeping records.

GST Bookkeeping for Registered Businesses

GST compliance adds another layer to your bookkeeping obligations. Singapore's GST rate is 9% (effective 1 January 2024), and businesses with taxable turnover exceeding S$1 million in the past 12 months—or expected to exceed that threshold in the next 12 months—must register within 30 days.

GST-registered businesses face additional record-keeping obligations:

- Tax invoices and simplified tax invoices (serially numbered)

- Export documents (bills of lading, air waybills, export permits)

- Import documents and permits

- GST account summarising output and input tax per period

- Records of due diligence checks for missing trader fraud

Set up your bookkeeping system to track GST transactions before you hit the registration threshold — retroactive reconciliation across months of records is time-consuming and error-prone.

Consequences of Non-Compliance

IRAS may impose penalties of up to S$5,000 and imprisonment of up to six months for inadequate record-keeping. Beyond criminal penalties, IRAS can exercise "best judgement" to estimate your revenue (typically unfavourably), disallow all expense claims lacking documentation, and trigger full audits.

The enforcement numbers make this concrete: between 2020–2023, IRAS recovered over S$270 million from approximately 7,000 businesses. Small businesses with cash transactions and family-owned companies were explicitly flagged as high-risk targets.

Essential Bookkeeping Tips for SMEs in Singapore

Tip 1: Separate Your Personal and Business Finances Immediately

Open a dedicated business bank account the day you incorporate. Every dollar of business income flows in; every business expense flows out. No exceptions.

IRAS explicitly requires business bank statements separate from personal accounts for GST-registered businesses. Mixing personal and business transactions creates reconciliation chaos, distorts profitability analysis, and raises red flags during audits.

IRAS enforcement reports consistently flag businesses that claim private expenses — personal travel, entertainment, family meals — as business deductions. Commingled accounts make those claims much harder to defend.

Tip 2: Set Up a Chart of Accounts Suited to Your Business

A chart of accounts is your financial filing system — a structured list of categories grouped under assets, liabilities, equity, income, and expenses. Customise it to reflect your actual operations:

- F&B businesses need detailed cost-of-goods-sold categories (ingredients, packaging, wastage)

- Consultancies need project-based revenue codes

- Retail businesses need inventory tracking accounts

A well-structured chart makes tax filing, financial reporting, and expense analysis easier. Most cloud accounting platforms offer industry-specific templates you can adapt.

Tip 3: Record Transactions Consistently—Don't Let Receipts Pile Up

Bookkeeping accuracy depends on frequency. Record transactions daily or at minimum weekly, at the point they occur. Use receipt-scanning apps to digitise paper receipts immediately — faded thermal paper becomes unreadable within months.

IRAS operates on a simple principle: no receipt = it didn't happen. Source documents are required proof for every expense claim. The "batch processing" trap (leaving bookkeeping for months until year-end) turns a manageable routine into an overwhelming backlog where documents go missing and errors multiply.

Tip 4: Reconcile Your Accounts Every Month

Monthly bank reconciliation means matching your internal transaction records against your bank statement, line by line. This process catches:

- Unrecorded bank charges or interest

- Duplicate entries

- Transactions you recorded but never cleared

- Deposits or withdrawals you forgot to log

Cloud accounting software can automate most of this through bank feeds that import transactions directly. Manual reconciliation for a month typically takes 30–60 minutes; catching a S$5,000 error three months later can take hours to trace and fix.

Tip 5: Stay on Top of Accounts Receivable

Outstanding invoices represent real money owed but not yet in your bank account. Set clear payment terms upfront (net 30 days is standard in Singapore), issue invoices promptly after delivery, and send automated reminders at 7, 14, and 30 days.

Late receivables create cash flow crunches that force SMEs to delay supplier payments, miss growth opportunities, or take on expensive short-term loans. An accounts receivable ageing report shows exactly who owes what and for how long — review it weekly.

Tip 6: Review Your Financial Reports—Not Just at Year-End

The two most important reports SMEs should review regularly:

| Report | What It Shows | Review Frequency |

|---|---|---|

| Profit & Loss (P&L) | Income vs. expenses over a period — reveals profitability and spending patterns | Monthly |

| Balance Sheet | Assets vs. liabilities on a specific date — shows net worth and financial health | Quarterly |

Review these monthly or at minimum quarterly. Spot cost overruns early, identify seasonal cash flow patterns, and catch emerging issues before they escalate into crises.

Common Bookkeeping Mistakes SMEs in Singapore Make

Three mistakes come up repeatedly in Singapore SME audits — and each one compounds the others.

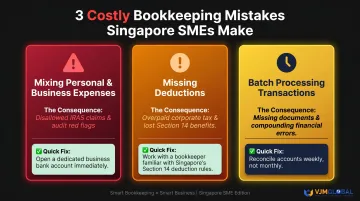

Mixing personal and business expenses tops the list of IRAS audit triggers. Beyond compliance risk, it distorts the true cost of running your business and results in disallowed expense claims. Separate bank accounts and credit cards for business use are the simplest fix.

Missed deductions are the second costly error. Under Section 14 of the Income Tax Act, expenses "wholly and exclusively incurred in the production of income" are deductible — yet many SMEs fail to track them consistently. Commonly overlooked categories include:

- Business travel (excluding private portions)

- Professional subscriptions (trade-related, not social clubs)

- Software subscriptions and SaaS tools

- Accounting, audit, and tax filing fees

- Employee training expenses (eligible for the enhanced 400% deduction under the Enterprise Innovation Scheme)

Batch processing syndrome—leaving bookkeeping updates for months—amplifies every other mistake. Errors become harder to trace, source documents disappear, and the risk of inaccurate filings increases dramatically. Preventive bookkeeping takes minutes per day versus painful days of catch-up work at year-end.

When to DIY vs. When to Outsource Your Bookkeeping

When DIY Makes Sense

DIY bookkeeping works for early-stage businesses with:

- Low transaction volumes (fewer than 50 transactions monthly)

- Founders with basic financial literacy

- Investment in quality cloud accounting software

Popular tools for Singapore SMEs include platforms listed on the IRAS Accounting Software Register Plus (ASR+):

| Platform | Starting Price | Key Singapore Features |

|---|---|---|

| Xero | S$39/month | Direct bank feeds (DBS, OCBC, UOB); GST F5 filing; receipt scanning |

| QuickBooks | S$31/month | Automated invoicing; multi-currency; mobile app |

| Zoho Books | Free tier available | Integrated ecosystem; automated workflows |

| Financio | S$20/month | Southeast Asia focus; PayNow QR integration |

All four support GST compliance and enable digital submission of GST returns to IRAS MyTaxPortal. The Productivity Solutions Grant covers up to 50% of software costs.

When Outsourcing Becomes Smarter

Outsourcing makes financial sense when:

- Transaction volumes exceed 50-100 monthly

- Your business becomes GST-registered

- Payroll complexity increases (CPF contributions, multiple employees)

- Year-end compliance creates stress and takes time from core operations

- Founder time is better spent on revenue-generating activities

Monthly outsourced bookkeeping for Singapore SMEs typically costs S$100-S$300 for small businesses (1-50 transactions), rising to S$300-S$800+ for higher volumes. Since accounting fees are fully tax-deductible under Section 14V, the net cost after 17% corporate tax is 17% lower.

For Singapore SMEs with cross-border operations or international investors, VJM Global provides outsourced bookkeeping and compliance support backed by 30+ years of accounting experience. Their team of Chartered Accountants and CPAs handles multi-entity structures, international transactions, and management reporting — useful when your business has ties to markets like India, the UK, or Australia.

Frequently Asked Questions

What is an SME company in Singapore?

Enterprise Singapore defines an SME as an enterprise with Group Annual Sales Turnover not exceeding S$100 million OR Group Employment Size not exceeding 200 employees. All SMEs must maintain proper financial records under Singapore law.

What is SME accounting?

SME accounting involves interpreting bookkeeping records to prepare financial statements, manage tax obligations, and support business decisions. Where bookkeeping records daily transactions, accounting analyses those records to produce compliance reports and financial insights.

How long must Singapore SMEs keep their financial records?

IRAS requires businesses to retain all records and supporting documents for at least five years from the relevant Year of Assessment. Both physical and digital records are acceptable, provided they're accurate and readily retrievable.

Is bookkeeping legally required for SMEs in Singapore?

Yes. Under the Companies Act and IRAS requirements, all Singapore companies must maintain proper accounting records and prepare annual financial statements, regardless of size or revenue. Non-compliance can result in fines up to S$5,000 and imprisonment up to six months.

What is the difference between bookkeeping and accounting?

Bookkeeping is the day-to-day recording of financial transactions — sales, expenses, and payments. Accounting takes those records further: analysing, summarising, and reporting them through tax computation, financial statements, and strategic financial advice.

When should an SME in Singapore outsource its bookkeeping?

Consider outsourcing when monthly transactions exceed 50-100, when GST registration adds complexity, when year-end compliance becomes stressful, or when founder time is better spent on core business growth rather than administrative tasks.