Introduction

The UK pharmaceutical industry invested £9.3bn in R&D in 2024—representing £1 in every £6 of private sector R&D investment. With the average cost to develop a new drug reaching $2.23bn per asset (USD) according to Deloitte's 2024 analysis, tax relief is essential for sustaining innovation at scale. Yet many UK pharmaceutical companies, particularly SMEs and biotech firms, underestimate their eligibility or leave significant relief unclaimed.

The landscape changed fundamentally in April 2024. The old SME and RDEC dual-scheme system merged into a single regime, overseas R&D restrictions tightened, and the interaction with grant funding simplified. For pharma companies running clinical trials, developing novel therapies, or innovating manufacturing processes, these changes create both opportunities and compliance risks.

This article covers:

- What qualifies as pharmaceutical R&D under HMRC's definition

- Who can claim and under which scheme (merged regime vs. ERIS)

- Which costs are eligible — and which are excluded

- How each clinical trial phase is treated for relief purposes

- How to submit a claim that withstands HMRC scrutiny

TLDR: Key Takeaways

- UK pharmaceutical companies subject to corporation tax can claim R&D tax relief on qualifying scientific or technological work

- The merged scheme delivers approximately 15–16.2% net benefit; loss-making R&D-intensive SMEs access ERIS at roughly 27% net benefit

- Qualifying activities include drug discovery, preclinical work, Phase I–III clinical trials, computational drug discovery, and manufacturing innovation

- Companies can now claim relief alongside Innovate UK and NIHR grants, which was not possible under the old SME scheme

- Overseas clinical trial costs are tightly restricted, with narrow exceptions for unique patient populations or regulatory requirements

What Counts as Pharmaceutical R&D Under UK Tax Rules

The Core Test

HMRC's definition is precise: qualifying work must seek an advance in overall knowledge or capability in a field of science or technology by resolving scientific or technological uncertainty. That means a competent professional in the field could not readily determine whether the outcome was achievable, or how to achieve it.

For pharmaceutical companies, this standard covers:

- Drug discovery and synthesis: Developing new chemical entities (NCEs) or novel biologics where the therapeutic effect or synthesis pathway is uncertain

- Preclinical development: Toxicology studies, pharmacokinetic modelling, and formulation work where outcomes cannot be predicted from existing knowledge

- Phase I–III clinical trials: Establishing safety, efficacy, dosing, and patient response where medical uncertainties exist

- Biopharmaceutical technologies: Monoclonal antibodies, gene therapies, mRNA platforms, and cell therapies involving unresolved technical challenges

- AI and digital health applications: Machine learning models for drug target identification, clinical trial patient selection, or efficacy prediction

- Manufacturing process innovation: Developing new synthesis routes, improving yield, reducing impurities, or scaling production where technical uncertainties must be resolved

What Doesn't Qualify

Not all pharma activity meets the test. Excluded work includes:

- Generic drug bio-equivalence testing where no new scientific uncertainty exists

- Phase IV post-marketing surveillance (unless genuine unresolved scientific questions remain)

- Brand development, logo design, and marketing activities—even if conducted during clinical trials

- Routine quality assurance testing and regulatory compliance filing

- Standard scale-up of proven processes without technical innovation

Failed Experiments Still Count

R&D tax relief rewards the attempt to resolve uncertainty, not success—a distinction many companies overlook. HMRC guidance (CIRD81510) confirms that failed projects qualify if they genuinely sought to advance scientific knowledge. For early-stage biotech companies running unsuccessful preclinical programmes, this distinction can preserve significant relief entitlement.

HMRC's Four-Stage Framework

CIRD81920 identifies four stages in pharmaceutical R&D:

- Drug Discovery – generally qualifies

- Preclinical Development – generally qualifies

- Clinical Trials (Phase I–III) – qualifies in most cases

- Regulatory Review/Post-Marketing Surveillance – does not qualify unless specific scientific uncertainties persist

The first three stages constitute accepted starting points for qualifying R&D. Phase IV requires closer scrutiny, as work typically shifts from resolving scientific uncertainty to monitoring known drugs in routine use.

Who Qualifies for UK Pharmaceutical R&D Tax Relief

Core Eligibility

To claim UK R&D tax relief, a pharmaceutical company must satisfy three conditions:

- Incorporated in the UK and subject to UK corporation tax

- Actively engaged in R&D — directly involved in scientific or technological innovation within pharma or life sciences

- Bearing financial risk — the company that commissions and funds the work holds claim entitlement, even if CROs or subcontractors conduct it

SME vs. Large Company Thresholds

Under the merged scheme, both SMEs and large companies claim through the same RDEC mechanism, but ERIS creates a more generous route for qualifying SMEs.

SME definition:

- Fewer than 500 employees

- Either turnover under €100m or balance sheet total under €86m

Loss-making SMEs spending at least 30% of total expenditure on qualifying R&D can access ERIS instead of the standard merged scheme, roughly doubling their benefit.

Overseas R&D Restrictions (Critical for Clinical Trials)

From April 2024, relief is generally restricted to UK-based activity. Subcontracted R&D and externally provided workers must be UK-based unless specific exemptions apply:

Valid exemptions:

- Specific patient population: Trials requiring patients not available in sufficient numbers in the UK (e.g., tropical disease studies)

- Geographical or environmental conditions: Drug stability testing in extreme climates not replicable in the UK

- Legal or regulatory requirements: Activities mandated by foreign regulators to take place in specific jurisdictions

Cost savings or workforce availability are not valid exceptions. Pharma companies running international multi-centre trials must carefully document why overseas costs meet exemption criteria.

Note for Northern Ireland: Companies registered in Northern Ireland claiming ERIS are exempt from overseas restrictions, but face a de minimis state aid cap.

Subcontracting Entitlement

If a pharma company acts as a CRO carrying out R&D under direction for a UK client, it generally cannot claim relief on that work—the commissioning company holds entitlement. CROs should verify their position before submitting claims to avoid HMRC challenges. Understanding where entitlement sits is the first step toward building a compliant, well-documented claim.

How Much Relief Can Pharmaceutical Companies Claim

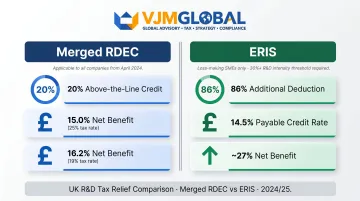

Merged RDEC Scheme

From April 2024, the merged scheme provides a 20% above-the-line taxable credit on qualifying R&D expenditure.

Net benefit by tax rate:

| Corporation Tax Rate | Gross Credit | Net Benefit After Tax |

|---|---|---|

| 25% (main rate) | 20% | 15.0% |

| 19% (small profits rate) | 20% | 16.2% |

Example: A pharmaceutical company spends £500,000 on qualifying R&D.

- Gross credit: £500,000 × 20% = £100,000

- Corporation tax on credit (25% rate): £100,000 × 25% = £25,000

- Net benefit: £75,000 (15% of qualifying spend)

ERIS (Enhanced R&D Intensive Support)

Loss-making SMEs meeting the 30% R&D intensity threshold access significantly higher relief:

- 86% additional deduction (total 186% deduction on qualifying spend)

- 14.5% payable credit on surrenderable losses

- Approximate net benefit: 26.97% of qualifying expenditure

For a biotech SME spending £1m on qualifying R&D (representing 35% of its £2.86m total expenditure), ERIS delivers roughly £270,000 benefit vs. £150,000 under merged RDEC—an 80% uplift over merged RDEC.

Northern Ireland cap: NI-registered SMEs claiming ERIS face a €300,000 de minimis state aid cap over three years (denominated in euros under retained UK state aid rules), applied to the additional benefit above merged RDEC.

Grant Funding Interaction—A Major Change

Under the old SME scheme, receiving notified state aid grants blocked R&D tax claims. This restriction was not carried into the merged scheme.

Per HMRC's merged scheme guidance, companies can now claim full merged RDEC relief alongside:

- Innovate UK grants

- NIHR funding

- Biomedical Catalyst awards (up to £2m per project, up to 70% for SMEs)

This removes a significant funding barrier for grant-dependent pharma SMEs — previously, a single Innovate UK award could disqualify an entire R&D tax claim.

Contractor Costs—New Inclusion

Previously, large company RDEC claims faced limits on subcontractor costs. The merged scheme now allows 65% of payments to unconnected subcontractors to count as qualifying expenditure (subject to UK location rules).

For pharma companies using specialist CROs, bioinformatics firms, or contract laboratories — where outsourced work can represent 40–60% of total R&D spend — this inclusion can substantially increase the qualifying expenditure base and the resulting credit.

What Costs Qualify for Pharmaceutical R&D Tax Claims

UK pharmaceutical R&D claims can cover a broader range of costs than most companies initially realise. The categories below reflect the current merged R&D scheme rules, including updates effective from 1 April 2023.

Main Qualifying Categories

Staff costs:

- Salaries, employer Class 1 NICs, and employer pension contributions for employees directly engaged in R&D

- No cap applies; costs must be genuinely attributable to qualifying R&D activities

Subcontractor and EPW costs:

- 65% of payments to unconnected subcontractors and externally provided workers (EPWs)

- Actual relevant expenditure for connected parties

- Subject to UK location restrictions

Consumables and materials:

- Chemicals, reagents, biological samples, and lab materials consumed or transformed during R&D

- Power, water, and fuel used directly by R&D activities

Software and data licences:

- AI tools, bioinformatics platforms, and cloud computing used directly in R&D

- Eligible for periods from 1 April 2023

Clinical trial volunteer payments:

- Payments to human trial subjects — both healthy volunteers and patients

- A pharma-specific qualifying cost with no direct equivalent in other sectors

- Requires thorough documentation to withstand HMRC scrutiny

Costs Pharmaceutical Companies Frequently Miss

Even experienced R&D teams leave money on the table. These are the most common oversights specific to pharmaceutical claims:

- CRO-routed volunteer payments – payments made to trial subjects via contract research organisations qualify, not just direct payments

- Biostatistician fees – pure mathematical and statistical analysis of trial data counts as qualifying R&D expenditure

- Agency staff under EPW rules – contractors and agency workers qualify at 65%, but many companies fail to identify them correctly

- Data licence renewals – annual licence costs for genomic databases, clinical registries, and bioinformatics platforms are eligible from April 2023

What Doesn't Qualify

Not every pharma-related cost makes the cut. Common exclusions include:

- Capital expenditure on equipment (though this may qualify separately under R&D Allowances)

- Costs tied to routine testing, post-approval monitoring, or marketing activities

- Overseas subcontractor costs that don't meet the permitted overseas expenditure exemptions

Clinical Trial Phases: What Qualifies and What Doesn't

Phase I, II, and III: Generally Qualify

According to guidance published by Buzzacott, Phase I–III clinical trials generally qualify because they resolve scientific uncertainty about:

- Phase I: Safety, tolerability, pharmacokinetics in healthy volunteers or small patient groups

- Phase II: Efficacy signals, dose ranging, adverse effects in larger patient cohorts

- Phase III: Confirmatory efficacy, safety monitoring, optimal treatment protocols in diverse populations

These phases inherently involve technological uncertainty that competent professionals cannot readily resolve without empirical testing.

Phase IV: Generally Excluded

Phase IV post-marketing surveillance typically does not qualify. Once a drug is licensed, Phase IV work usually involves:

- Ongoing safety monitoring of known drugs

- Commercial positioning and market expansion

- Routine compliance with regulatory obligations

These activities don't seek to resolve scientific uncertainty—they monitor established products in routine use.

Exceptions: Phase IV work can qualify where genuine unresolved scientific questions persist:

- Investigating previously unknown drug interactions

- Studying effects in patient subgroups not covered in Phase I–III

- Researching new indications requiring new efficacy evidence

Before including Phase IV costs in a claim, companies should document the specific scientific uncertainty being investigated and be prepared to defend that position to HMRC.

Grey Areas Within Qualifying Phases

The boundary between qualifying and non-qualifying work doesn't fall neatly at phase boundaries. Even within Phase I–III, certain activities must be excluded:

- Brand development and logo design conducted during trials

- Market research and commercial positioning

- Standard quality control testing

- Routine regulatory compliance filing (e.g., Form 12 submissions)

In practice, this means maintaining a clear cost allocation methodology — separating staff time, contractor costs, and consumables by activity type from the outset of each trial programme, rather than attempting to reconstruct the split at year-end.

How to Claim Pharmaceutical R&D Tax Relief

Preparation Steps

1. Identify and document qualifying projects

Maintain contemporaneous records throughout the year:

- Lab notebooks and experimental protocols

- Clinical trial designs and patient recruitment records

- Project plans linking activities to scientific uncertainties

- Technical summaries explaining what was unknown and what the project sought to resolve

2. Calculate eligible expenditure by category

Separate costs into qualifying categories (staff, subcontractors, consumables, etc.) and apply appropriate caps (e.g., 65% for unconnected subcontractors).

3. Prepare the technical narrative

Explain how each project sought an advance in science or technology by resolving uncertainty a competent professional couldn't readily answer. Link activities to HMRC's definition.

4. Complete the Additional Information Form (AIF)

The mandatory online AIF must be submitted before or alongside the tax return. Introduced in August 2023, it continues under the merged scheme.

Formal Submission Process

CT600 Corporation Tax Return:

- Claims are made through the company's CT600 for the relevant accounting period

- The merged RDEC is an above-the-line taxable credit reported in the return

- Two-year deadline from the end of the accounting period—there are no extensions

Claim Notification (for new claimants):

- Companies claiming for the first time, or that haven't claimed in the previous three periods, must submit a Claim Notification to HMRC in advance

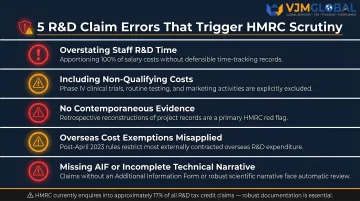

Common errors that trigger HMRC checks:

- Overstating staff time attributable to R&D

- Including non-qualifying Phase IV or marketing costs

- Failing to retain contemporaneous evidence

- Incorrectly applying overseas cost exemptions

- Missing AIF or incomplete technical narratives

With an HMRC enquiry rate of approximately 17% in 2023/24, robust documentation is essential. That risk makes specialist support worth serious consideration.

Expert Support Makes the Difference

Navigating the merged scheme, ERIS thresholds, overseas cost restrictions, and subcontracting rules goes well beyond a standard accountant's remit. Errors don't just reduce your claim — they invite extended HMRC scrutiny.

VJM Global has supported 250+ UK businesses across tax, audit, and advisory work. For pharmaceutical R&D claims specifically, the team helps with:

- Identifying which projects and activities qualify under HMRC's criteria

- Building well-supported technical reports that hold up under enquiry

- Applying the correct cost caps for staff, subcontractors, and consumables

- Submitting compliant claims through the CT600 and AIF process

With 30+ years of experience and direct familiarity with pharma R&D's scientific and regulatory context, VJM Global works alongside your existing advisors so no eligible expenditure is missed.

Frequently Asked Questions

What is UK R&D tax relief?

UK R&D tax relief is a government-backed incentive from HMRC that allows UK corporation tax-paying companies to reduce their tax liability or receive a cash credit for qualifying research and development expenditure.

What is the 86% R&D tax relief?

The "86%" figure relates to the Enhanced R&D Intensive Support (ERIS) scheme for qualifying loss-making SMEs that spend at least 30% of total costs on R&D. ERIS provides an 86% additional deduction (total 186% deduction) plus a 14.5% payable credit, delivering approximately 26.97% net benefit, which is significantly more generous than the standard merged RDEC rate.

What qualifies as R&D for tax relief in the UK?

A project must seek an advance in science or technology by resolving genuine scientific or technological uncertainty. That means a competent professional in the field could not readily determine whether the goal was achievable or how to achieve it. In pharma, qualifying work covers drug discovery, preclinical development, and Phase I–III clinical trials.

Can pharmaceutical companies claim R&D relief for clinical trials?

Phase I, II, and III clinical trials generally qualify because they resolve scientific uncertainty about a drug's safety, efficacy, dosing, and patient response. Phase IV post-marketing trials do not usually qualify unless genuine uncertainties remain, such as investigating new indications or previously unknown interactions.

Can a UK pharma company claim R&D tax relief and grant funding at the same time?

Yes — since April 2024, UK companies can generally claim R&D tax relief under the merged scheme or ERIS even when receiving grant funding (Innovate UK, NIHR, Biomedical Catalyst) for the same project. This reverses the old SME scheme restriction, where state aid grants could block claims.

What is the difference between the SME R&D scheme and RDEC for pharma companies?

The old SME and RDEC schemes were largely consolidated into the merged RDEC scheme from April 2024. All companies now claim through merged RDEC (20% credit, approximately 15% net benefit), except loss-making R&D-intensive SMEs meeting the 30% intensity threshold, who access the higher ERIS credit (approximately 27% net benefit) instead.