Introduction

UK businesses looking to establish a commercial presence in Asia face a straightforward yet strategic choice: Singapore's subsidiary structure offers the most accessible and tax-efficient route to regional expansion. Despite post-Brexit headwinds redirecting European trade, the numbers are hard to ignore. Singapore ranked 2nd globally in the IMD World Competitiveness Ranking 2025 and scored 94 out of 100 in the World Bank's B-READY Business Entry index — both reflect how deliberately this city-state has been built for foreign investment.

Yet many UK decision-makers underestimate how quickly this process moves. Incorporation is typically measured in days, not months, and Singapore's compliance framework, whilst structured, avoids the bureaucratic drag common across much of Asia.

The real friction points are not procedural complexity but unfamiliarity: ACRA's registration portal, director residency requirements, and the nuances of post-Brexit tax planning when profits span three time zones.

This guide covers every stage — eligibility, statutory requirements, the registration process, and ongoing compliance — so UK businesses have a clear picture of what to expect before filing a single document.

Key Takeaways

- A Singapore subsidiary is a separate legal entity with limited liability, a 17% corporate tax rate, and start-up exemptions saving up to SGD 21,250/year for three years

- UK businesses can own 100% of shares—no local equity partner required

- You'll need one Singapore-resident director, one shareholder, a registered local address, and a qualified company secretary

- Incorporation via ACRA's BizFile+ typically completes in 1–3 days once documents are ready

- Post-incorporation duties cover Annual Returns, corporate tax filing, and (where applicable) GST registration and CPF contributions

What Is a Singapore Subsidiary Company?

A Singapore subsidiary is a locally incorporated private limited company (Pte. Ltd.) that is wholly or partially owned by a foreign parent company. It operates as a separate legal entity with its own rights, obligations, and liabilities—distinct from the UK parent in every legal and operational sense.

What "separate legal entity" means in practice:

- The UK parent company is not liable for the subsidiary's debts, contractual claims, or regulatory penalties

- The subsidiary can own assets, enter contracts, sue and be sued independently

- Business activities align with the parent's strategy but execute under Singapore law

- The subsidiary qualifies as a Singapore tax resident, accessing local incentives and treaty benefits

That last point matters more than it might appear. Singapore's tax residency status opens access to over 80 double taxation agreements — including the UK-Singapore DTA — which directly affects how profits are repatriated. Here's how the subsidiary compares to the two other structures UK businesses commonly consider:

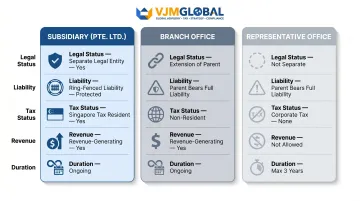

How it differs from other entry structures:

| Feature | Subsidiary (Pte. Ltd.) | Branch Office | Representative Office |

|---|---|---|---|

| Legal status | Separate legal entity | Extension of parent | Not separate entity |

| Liability | Ring-fenced to subsidiary | Flows to UK parent | Flows to UK parent |

| Tax residency | Singapore tax resident | Non-resident unless managed in SG | No corporate tax |

| Revenue generation | Yes | Yes | No |

| Duration | Ongoing | Ongoing | Maximum 3 years |

Source: ACRA - Ways to Set Up

For UK businesses with long-term commercial ambitions in Southeast Asia, the subsidiary structure is the practical default. The branch route exposes the UK parent to Singapore liabilities directly — a significant risk if the Asia operation is still being tested. The representative office, meanwhile, cannot generate revenue at all, making it unsuitable for anything beyond preliminary market research.

Why UK Businesses Prefer a Singapore Subsidiary Over Other Entry Structures

Liability Protection

Unlike a branch office where liabilities flow back to the UK parent, a subsidiary isolates risk at the Singapore entity level. If the subsidiary faces a contractual dispute or regulatory penalty, the UK parent's exposure is limited to its equity investment. This matters especially when operating in unfamiliar regulatory environments or testing new market ideas where downside risk must be contained.

Tax Residency and Incentives

A Singapore subsidiary qualifies as a tax-resident entity, making it eligible for the Start-Up Tax Exemption (SUTE) scheme:

| Income Band | Exemption Rate | Tax Saved (at 17%) |

|---|---|---|

| First SGD 100,000 | 75% exempt | Up to SGD 12,750 |

| Next SGD 100,000 | 50% exempt | Up to SGD 8,500 |

| Maximum annual saving | — | Up to SGD 21,250 |

The exemption applies for the first three consecutive Years of Assessment. Eligibility requires:

- Singapore incorporation and tax residency

- No more than 20 shareholders (all individuals), or at least one individual holding 10%+ of shares

- Principal activity cannot be investment holding or property development

Source: IRAS - Corporate Income Tax Rates

By contrast, a branch office is taxed as a non-resident entity and cannot access SUTE or other resident-only incentives, which raises the effective tax burden from day one.

UK-Singapore Double Taxation Agreement

The UK-Singapore DTA (2012 protocol) significantly reduces withholding tax on cross-border payments:

| Income Type | Treaty WHT Rate |

|---|---|

| Dividends | 0% |

| Interest | 5% |

| Royalties | 8% |

Source: GOV.UK - Singapore Tax Treaties

The 0% dividend withholding means UK parent companies can repatriate Singapore subsidiary profits with minimal treaty friction, a clear advantage when structuring regional cashflows.

Strategic Market Access

Singapore's position as Southeast Asia's financial hub makes it the natural Asian base for UK businesses. Its English-language legal system (modelled on common law), proximity to India, Indonesia, and Malaysia, and a corporate tax rate of 17% all contribute to this appeal.

The city-state hosts over 7,000 multinational corporations and nearly half of all Asian regional headquarters, according to EDB data. That concentration of talent, capital, and infrastructure cuts the time and cost of building local networks when expanding beyond Europe.

Operational Flexibility

A branch office must mirror the UK parent's business activities and carry the same name. A subsidiary, by contrast, can operate under its own brand, pursue different business lines, and build an independent credit and commercial profile in Singapore.

This flexibility is particularly useful when testing service offerings or partnership models that sit outside the parent's UK operations.

Key Requirements to Set Up a Singapore Subsidiary Company

Core statutory requirements:

- Company name: Must be unique and approved by ACRA; need not match the UK parent's name, but cannot infringe existing trademarks

- Resident director: At least one director must be ordinarily resident in Singapore (citizen, PR, or EntrePass holder). UK directors alone do not fulfil this requirement — nominee director services are the standard solution for foreign-owned subsidiaries

- Shareholders: Minimum one, maximum 50; can be individual or corporate entity with no nationality restrictions — the UK parent can be the sole shareholder

- Company secretary: Must be appointed within six months of incorporation; must be Singapore-resident and suitably qualified

- Registered office address: A valid physical Singapore address (not a P.O. box); virtual office addresses at commercial locations are accepted

- Paid-up capital: Minimum SGD 1; no maximum; additional capital can be injected post-incorporation

Source: ACRA — Appointing Company Directors & Other Officers

Once you've confirmed the structure, the UK parent company needs to prepare the following documents before incorporation can proceed:

- UK Certificate of Incorporation

- Board resolution authorising incorporation of the Singapore subsidiary

- Passport details and residential addresses of proposed directors

- Signed Consent to Act as Director

- Company's proposed Constitution (Articles of Association)

- All documents must be in English or officially translated

These documents feed directly into the filing process — which has one critical constraint for UK applicants.

Critical filing requirement:

UK businesses without a SingPass ID cannot self-register through BizFile+. All foreign businesses must engage an ACRA-approved corporate service provider (CSP) to submit the incorporation application. For UK applicants, engaging a CSP is mandatory, not optional.

Step-by-Step: How to Register Your Singapore Subsidiary

Registration is handled through ACRA's BizFile+ platform. When documents are ready and a filing agent is engaged, incorporation typically completes within 1–3 working days.

Registration is handled through ACRA's BizFile+ platform. When documents are ready and a filing agent is engaged, incorporation typically completes within 1–3 working days.

Here's a quick overview of what each step involves:

| Step | Action | Fee | Timeline |

|---|---|---|---|

| 1 | Reserve company name | SGD 15 | Same day |

| 2 | Prepare documents & engage filing agent | Varies | 3–5 days |

| 3 | Submit incorporation application | SGD 300 | Same day |

| 4 | Receive Certificate of Incorporation & UEN | — | 1–3 working days |

| 5 | Open corporate bank account | Varies | 1–4 weeks |

Step 1: Reserve and Approve Your Company Name

Submit the proposed company name to ACRA for approval via BizFile+. ACRA checks for conflicts with existing registered names and trademarks. Name reservation costs SGD 15 (non-refundable) and holds the name for 120 days.

Before finalising a name, cross-check ACRA's business name register and the Intellectual Property Office of Singapore (IPOS) trademark database. This prevents rejection at submission and protects against future infringement claims.

Source: ACRA - Reserving a Business Name

Step 2: Prepare Incorporation Documents and Engage a Filing Agent

Compile all required documents from the UK parent: Certificate of Incorporation, board resolution, director details, and Constitution. Engage an ACRA-approved filing agent or CSP to handle the BizFile+ submission.

This is the stage where an experienced advisory firm makes the biggest difference. VJM Global has supported over 250 UK businesses through cross-border setups, with direct experience handling UK parent company documentation and Singapore compliance requirements — reducing errors and turnaround time.

Step 3: Submit the Incorporation Application to ACRA

Your filing agent submits the incorporation application via BizFile+, including:

- All supporting documents

- Registered address

- Director and shareholder information

- Chosen SSIC code (Singapore Standard Industrial Classification) for business activity

Pay the registration fee of SGD 300.

Source: ACRA - Registering via Bizfile

Step 4: Receive the Certificate of Incorporation and UEN

Standard applications are approved within 1–3 working days. Applications referred for additional review (for example, those involving regulated activities) can take longer. Once approved, your company receives:

- Certificate of Incorporation

- Unique Entity Number (UEN) — your company's official identifier for all government and regulatory transactions

The subsidiary is now legally incorporated and can commence operations.

Step 5: Open a Corporate Bank Account

Use the Certificate of Incorporation and UEN to open a Singapore corporate bank account. Most major banks require in-person KYC or physical presence, so UK businesses should plan for potential travel.

If travel isn't feasible, licensed digital banks in Singapore offer remote account opening — though due diligence requirements are equally stringent. Factor this into your setup timeline.

Post-Incorporation Obligations and Common Pitfalls for UK Businesses

Key Ongoing Compliance Requirements

Annual Returns with ACRA: Private companies must file Annual Returns within 7 months after the financial year-end. Late filing penalties start at SGD 300 and can reach SGD 600.

Annual General Meeting: Must be held within 6 months after FYE (or dispensed with via written resolution if all members agree).

Source: ACRA - Deadline & Requirements for Annual Returns

Corporate Tax Filing with IRAS:

| Filing | Deadline |

|---|---|

| Estimated Chargeable Income (ECI) | Within 3 months from FY end |

| Form C-S / Form C | 30 November annually |

Source: IRAS - ECI Filing

GST Registration: Compulsory when annual taxable turnover exceeds SGD 1 million—either retrospectively at year-end or prospectively when the threshold is expected within the next 12 months.

CPF Contributions: UK businesses hiring Singapore citizens or PRs must register with the Central Provident Fund Board before the first payroll run. Employer contributions are 17% of monthly wages for employees aged 55 and below earning above SGD 750.

Source: CPF Board - How Much to Pay

Common Pitfall: Nominee Director Governance

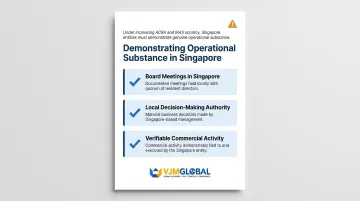

The most frequent mistake UK businesses make is appointing a nominee resident director as a formality without establishing proper governance documentation. Whilst nominee directors are legally permissible, ACRA and IRAS may scrutinise tax residency claims if Singapore-based management and control cannot be demonstrated.

To support tax residency status and withstand scrutiny during audits or treaty relief applications, the subsidiary needs genuine operational substance in Singapore. This means:

- Documented board meetings held in Singapore

- Local decision-making authority on material matters

- Verifiable commercial activity tied to the Singapore entity

Recommendation

UK parent companies often underestimate how granular Singapore's compliance calendar is. Each obligation—ACRA filings, IRAS tax returns, CPF registrations—runs on its own timeline and involves a separate regulatory body. Working with an adviser experienced in cross-border compliance structures helps UK teams stay on top of these deadlines without building in-house expertise in Singapore's regulatory framework from scratch.

Frequently Asked Questions

How to set up a subsidiary company in Singapore?

Reserve your company name with ACRA (SGD 15), prepare incorporation documents including UK parent records, engage an ACRA-approved filing agent, submit via BizFile+ (SGD 300 fee), and receive your Certificate of Incorporation and UEN—typically within 1–3 working days.

What is a subsidiary in Singapore?

A Singapore subsidiary is a locally incorporated private limited company (Pte. Ltd.) fully or partially owned by a foreign parent. It operates as a separate legal entity and qualifies for Singapore's resident tax regime, including access to the SUTE scheme and DTA benefits.

What qualifies a company as a subsidiary?

Under Singapore's Companies Act, a company is a subsidiary when another company (the holding company) controls the composition of its board of directors or holds more than half of its voting shares.

What is the difference between a branch and a subsidiary in Singapore?

The key differences come down to liability and tax status:

- Branch: Extension of the parent company; parent bears full liability; taxed as a non-resident entity; ineligible for SUTE or DTA benefits

- Subsidiary: Separate legal entity with ring-fenced liabilities; qualifies as tax resident; can access SUTE incentives and double tax treaty benefits

Can foreigners incorporate and own shares in a Singapore company?

Yes — both incorporation and full ownership are open to foreigners. A UK individual or UK parent company can hold 100% of shares with no requirement for a local equity partner. You must engage an ACRA-approved filing agent to submit the application and appoint at least one Singapore-resident director.