Introduction

The UK fintech sector ranks second globally, attracting £2.9 billion in investment across 534 deals in 2025 and accounting for 11% of the global industry. This makes it one of the most R&D-intensive sectors in the country, where constant innovation in payments, AI, blockchain, and regulatory compliance creates significant opportunities for government-backed tax relief.

Yet many fintech companies either underclaim or miss out entirely. Confusion around eligibility rules, recent scheme changes, and what HMRC looks for in a submission remains widespread. According to HMRC's R&D tax relief statistics, total R&D claims fell by 26% in 2023–24, reflecting both tighter compliance scrutiny and increased administrative burden.

This guide covers eligibility criteria, qualifying costs, the merged RDEC scheme, and how to build a submission that holds up under HMRC review.

Key Takeaways

- R&D tax credits reward UK fintech companies for developing innovative financial technology, even if the project fails

- Two schemes apply: Merged RDEC (for most companies) and ERIS (for qualifying loss-making, R&D-intensive SMEs)

- Qualifying work includes AI development, blockchain, payment infrastructure, and cybersecurity that resolves genuine technical uncertainty

- Recent changes include mandatory Claim Notification Forms, cloud computing cost eligibility, and tighter overseas subcontracting rules

- Specialist tax advisors reduce claim risk and increase how much your company recovers

What Counts as R&D in Fintech?

HMRC's core eligibility test is straightforward: a project must seek an advance in science or technology by resolving a technological uncertainty that a competent professional in the field could not readily resolve. This is distinct from simply building new software or launching a new product.

Qualifying Fintech R&D Activities

Activities that qualify tend to share one common thread: they tackle a technical problem that existing knowledge, tools, or methods cannot straightforwardly solve. Common examples in fintech include:

- Developing novel AI models for credit scoring or fraud detection that extend beyond applying existing techniques

- Building or extending blockchain systems for asset tokenisation, digital contracts, or secure settlement — particularly where performance or interoperability gaps remain unsolved

- Designing real-time payment architectures that overcome measurable constraints in processing speed, security, or cross-platform compatibility

- Creating biometric authentication or behavioural fraud analysis systems that go beyond configuring off-the-shelf tools

- Automating FCA regulatory reporting through custom-built processing logic that resolves genuine technical uncertainty

What Doesn't Qualify

Routine software development does not qualify. This includes building a website, integrating off-the-shelf APIs, or updating a user interface. The work must address a technical problem that isn't solvable using existing knowledge.

The difference becomes clear with a direct comparison:

| Qualifying R&D | Non-Qualifying Activity | |

|---|---|---|

| Scenario | Building a real-time fraud detection system using behavioural biometrics and ML to flag suspicious patterns within milliseconds of transaction initiation | Integrating Stripe's existing fraud detection API and customising the dashboard interface |

| Why it matters | Technical uncertainty exists: achieving sub-100ms processing at 95%+ accuracy across diverse transaction types is not solvable with existing methods | No technical uncertainty: the integration uses documented, readily available knowledge |

| HMRC verdict | Qualifies | Does not qualify |

HMRC has developed reasonable familiarity with fintech propositions. That said, a claim still needs to be tightly scoped — each qualifying project should identify the specific uncertainty being resolved and explain why existing methods were insufficient.

UK R&D Tax Relief Schemes: Merged RDEC and ERIS

Merged RDEC Scheme

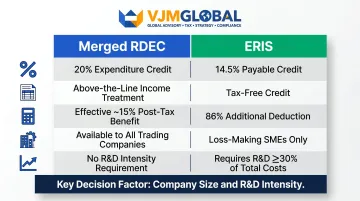

From April 2024, the Merged RDEC scheme replaced the previous two-track SME and large company system. All companies, regardless of size, now claim under a single framework unless qualifying for ERIS.

Key features:

- Delivers a 20% expenditure credit on qualifying R&D costs

- Treated as above-the-line income, which improves reported profitability before tax

- Yields an effective post-tax benefit of ~15% at the 25% Corporation Tax rate, or ~16.2% at the 19% small companies rate

- Caps payable credit at £20,000 plus 300% of relevant PAYE and National Insurance contributions

Note that the credit counts as taxable trading income — it is subject to Corporation Tax, which is factored into the effective benefit rates above. Loss-making R&D-intensive SMEs may find better value under ERIS, covered next.

Enhanced R&D Intensive Support (ERIS)

ERIS targets loss-making SMEs where R&D expenditure reaches 30% or more of total operational costs. Fintech startups building pre-revenue products frequently meet this threshold, making ERIS one of the most valuable reliefs available to early-stage companies. To qualify as an SME, a company must have fewer than 500 employees and either turnover under €100 million or a balance sheet under €86 million (thresholds retained from EU-origin UK company law).

Key features:

- Provides an 86% additional deduction (186% total) on qualifying expenditure

- Generates a payable credit of up to 14.5% of surrenderable loss — not subject to Corporation Tax

- R&D intensity threshold reduced from 40% to 30% from April 2024, widening eligibility

- Net benefit materially exceeds Merged RDEC for eligible loss-making companies

Companies qualifying for ERIS may elect to claim under Merged RDEC instead — but cannot claim under both schemes for the same expenditure.

| Scheme | Who it's for | Credit rate | Key condition |

|---|---|---|---|

| Merged RDEC | All trading companies | 20% expenditure credit | None |

| ERIS | Loss-making R&D-intensive SMEs | 14.5% payable credit | R&D ≥30% of total expenditure |

Qualifying Costs Fintech Companies Can Claim

Qualifying expenditure is broader than most fintech companies realise. Claims are frequently undervalued simply because eligible cost categories go unidentified.

Staffing and People Costs

Eligible staff costs include:

- Salaries, wages, and bonuses for employees directly working on R&D projects

- Employer National Insurance contributions

- Employer pension fund contributions

- Engineers, data scientists, and product developers engaged in qualifying work

For employees splitting time between R&D and non-R&D work, claims are proportionate based on actual duties performed — this is a question of fact, not job title.

Qualifying indirect activities also count toward the claim:

- Scientific or technological information services

- R&D equipment maintenance

- Recruitment for specific R&D projects

- Line management of R&D staff

Payroll is typically the largest single line item in any R&D claim.

Benefits in kind, redundancy payments, payments in lieu of notice, and gardening leave do not qualify.

Cloud Computing and Software

From accounting periods beginning on or after 1 April 2023, cloud computing costs used directly in R&D now qualify. Most fintech platforms rely on cloud infrastructure for ML training and data processing — these costs now qualify directly.

Eligible cloud and software costs include:

- Compute costs for training ML models

- Running test environments

- Processing large fintech datasets

- Data licence costs directly attributable to R&D

Subcontractors and Externally Provided Workers (EPWs)

Costs for UK-based subcontractors or EPWs engaged to perform qualifying R&D can be claimed. From April 2024, overseas subcontractor costs are generally excluded — a narrow exception applies where work cannot feasibly be conducted in the UK due to regulatory or technical conditions (for example, fintech projects requiring jurisdiction-specific FCA knowledge).

Other eligible categories include:

- Consumable materials used directly in R&D

- Payments to research participants (relevant in health-fintech crossovers)

Key Rule Changes Fintech Firms Must Know

Claim Notification Form (CNF)

For accounting periods beginning on or after 1 April 2023, companies claiming for the first time, returning after a 3-year gap, or following a prior rejection must notify HMRC of their intent to claim.

Submit the CNF within six months of your accounting period end — failure to do so can result in the entire claim being disallowed.

Expanded Cloud Computing Eligibility

From April 2023, cloud computing and data licence costs became qualifying expenditure. Fintech companies with significant cloud infrastructure spend should include those costs in claims.

Tightened Overseas Subcontracting Restriction

From April 2024, overseas subcontractor costs are generally excluded, with narrow exceptions. Getting specialist advice before filing helps identify which exceptions apply and prevents non-compliant inclusions from triggering HMRC challenges.

Contemporaneous Documentation Requirements

HMRC scrutiny has increased sharply. The estimated error and fraud rate was 9.9% (£759 million) in 2022-23, reduced to an illustrative 5.9% (£481 million) by 2024-25.

Maintain real-time records of R&D activities, project logs, and cost allocations throughout the year — not just at claim time. Contemporaneous documentation produces stronger, more defensible submissions when HMRC reviews your claim.

How to Make a Successful Fintech R&D Claim

Step-by-Step Process

1. Assess eligibility: Identify projects that meet HMRC's advance-in-technology and technological-uncertainty tests.

2. Identify qualifying costs: Capture all eligible expenditure categories including staffing, cloud computing, and subcontractors.

3. Submit CNF if required: First-time claimants, companies returning after 3 years, or those with prior rejections must submit within 6 months of accounting period end.

4. Prepare technical narrative: Your narrative must cover:

- The specific field of science or technology involved

- The baseline knowledge that existed at the start

- The advance being sought

- The technical uncertainties faced

- Why resolution wasn't readily deducible by a competent professional

- The steps taken to resolve those uncertainties

5. File alongside Corporation Tax return: Submit within two years of the end of the accounting period.

Who Needs to Be Involved

Two internal stakeholders are critical to a strong submission:

- Finance team — leads on cost identification, eligible expenditure mapping, and filing logistics

- Technical lead (CTO, VP Engineering, or Chief Product Officer) — articulates the R&D uncertainties addressed and the advance being sought; HMRC evaluates technical quality, not just financial calculations

Working with Specialist Advisors

Working with a specialist R&D tax advisor reduces the risk of HMRC enquiries and helps ensure no qualifying costs are missed. VJM Global's team of chartered accountants and tax professionals has supported over 250 UK businesses and can guide fintech companies from eligibility assessment through to final submission.

This support is especially relevant now. The introduction of CNF and Additional Information Form (AIF) requirements has raised the compliance bar — and contributed to a 26% drop in total claims between 2022–23 and 2023–24. Getting the process right from the outset is the most effective way to avoid that outcome.

Frequently Asked Questions

What is the R&D credit rate in the UK?

Under the Merged RDEC scheme (from April 2024), companies receive a 20% credit on qualifying R&D expenditure — an effective post-tax benefit of around 15% at the 25% Corporation Tax rate. ERIS-qualifying SMEs can access a higher 14.5% payable credit (not liable to tax).

Can fintech startups claim R&D tax credits if they are loss-making?

Yes. Loss-making fintech SMEs may qualify under the ERIS scheme if their R&D expenditure is 30% or more of total operational costs. This can result in a payable cash credit of 14.5% even when no corporation tax is owed.

What fintech activities qualify for R&D tax credits in the UK?

Qualifying activities include:

- Developing AI/ML models for fraud detection, credit scoring, or personalisation

- Building blockchain infrastructure or decentralised finance protocols

- Creating novel payment systems or open banking integrations

- Engineering cybersecurity or RegTech compliance solutions

Each activity must address a genuine technological uncertainty — one that a competent professional could not resolve using existing knowledge.

What is the Claim Notification Form (CNF) and when is it required?

The CNF is a mandatory pre-notification to HMRC. It must be filed within six months of the accounting period end — required for first-time claimants, those returning after a three-year gap, or companies whose prior claim was rejected. Missing this deadline disqualifies the entire claim.

Can I claim R&D tax credits for cloud computing costs in fintech?

Yes. Cloud computing costs directly attributable to R&D activity (such as compute for ML model training or R&D test environments) became eligible for accounting periods starting on or after 1 April 2023. For data-intensive fintech operations, this change meaningfully expands what can be claimed.

Can fintech companies claim R&D credits for work done by overseas contractors?

From April 2024, HMRC excludes most overseas subcontractor costs. A narrow exception applies where the R&D genuinely requires conditions unavailable in the UK — fintech companies with jurisdiction-specific regulatory development needs may qualify under this exception.