Introduction

Dubai's corporate tax regime — introduced in June 2023 via Federal Decree-Law No. 47 of 2022 — represents a fundamental shift for Singapore businesses operating in or expanding to the UAE. Unlike Singapore's long-established tax framework, UAE businesses now face mandatory annual filings, and missing deadlines carries steep financial penalties including AED 10,000 for late registration and AED 500–1,000 per month for late filing.

Many Singapore companies underestimate the compliance burden. The UAE regime involves several requirements that have no direct equivalent at home:

- Registering through the Federal Tax Authority's EmaraTax portal

- Maintaining audited financial statements (required for entities above AED 50 million in revenue)

- Navigating first-tax-period rules that can stretch up to 18 months for entities incorporated before June 2023

This guide covers everything Singapore businesses need to stay compliant:

- Who must file and registration requirements

- Key deadlines based on your financial year-end

- Step-by-step filing processes

- Penalties for non-compliance

- How the UAE-Singapore Double Tax Agreement affects cross-border planning

Whether you operate a mainland LLC, free zone company, or branch office, getting these deadlines right is the difference between smooth operations and avoidable fines.

TLDR: Key Takeaways for Singapore Businesses

- UAE corporate tax applies at 9% on taxable profits above AED 375,000 (0% below), covering mainland companies, free zone entities, and foreign businesses with a UAE presence

- Every UAE-registered business must file within 9 months of financial year-end — December 31 year-end = September 30 filing deadline

- Tax registration is mandatory before filing — late registration carries an AED 10,000 penalty

- Late filing costs AED 500/month for the first 12 months, rising to AED 1,000/month thereafter

- Free zone companies must file even if they qualify for 0% tax on qualifying income

- The UAE-Singapore DTA provides tax credits but does not eliminate UAE filing obligations for Singapore businesses

Does UAE Corporate Tax Apply to Your Singapore Business?

UAE corporate tax applies to any entity with a taxable presence in the UAE — including mainland LLCs, free zone companies, and branch offices — regardless of where the parent company is incorporated. A Singapore-headquartered business with a UAE subsidiary or branch office is subject to UAE corporate tax rules from the first financial year starting on or after June 1, 2023.

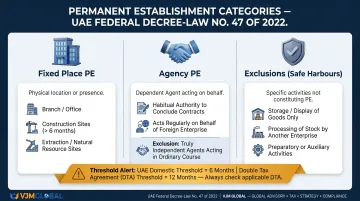

Understanding Permanent Establishment (PE)

If a Singapore company operates in the UAE without formally incorporating but has a fixed place of business, employees, or a dependent agent, it may still be treated as a taxable entity by the FTA. Under Article 14 of Federal Decree-Law No. 47 of 2022, a non-resident has a PE in the UAE if:

Fixed Place PE:

- Fixed or permanent place through which business is conducted (branch, office, factory, workshop)

- Building sites or construction projects lasting more than 6 months

- Mines, oil/gas wells, or natural resource extraction sites

Agency PE:

- A person habitually concludes or negotiates contracts on behalf of the non-resident

- Does not apply to independent agents acting in ordinary course of business

Exclusions:

- Facilities used solely for storage, display, or delivery

- Stock kept for processing by another person

- Activities that are purely preparatory or auxiliary

The 6-month construction threshold under domestic UAE law differs from the 12-month threshold in the UAE-Singapore DTA, meaning treaty protection may apply for shorter-duration projects. Understanding your PE exposure determines which registration pathway applies — the table below outlines the three structures Singapore businesses most commonly use in the UAE.

UAE Entity Structures Singapore Businesses Use

| Entity Type | Tax Registration Required | Notes |

|---|---|---|

| Mainland LLC | Yes | Full UAE corporate tax applies; must register within 3 months of incorporation (for entities established after March 1, 2024) |

| Free Zone Company | Yes | Must register and file even if qualifying for 0% rate on qualifying income; Ministerial Decision No. 84 of 2025 requires audited financials regardless of revenue |

| Branch of Foreign Company | Yes | Treated as resident juridical person; follows same registration and filing deadlines as mainland entities |

Exemptions and Registration Obligations

The following entities are exempt from UAE corporate tax registration:

- UAE government bodies conducting non-commercial activities

- Qualifying public benefit entities (listed in Cabinet Decision)

- Qualifying investment funds (FTA-approved)

- Extractive businesses (notified to Ministry of Finance)

Most Singapore commercial entities operating in the UAE will have registration obligations. Confirming whether any exemption applies to your specific structure requires a review of both your entity type and the nature of your UAE activities.

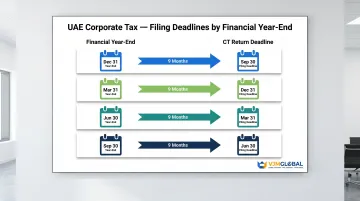

UAE Corporate Tax Filing Deadlines: What Singapore Businesses Need to Know

UAE corporate tax returns must be filed within 9 months after the end of the relevant tax period. The filing deadline and tax payment deadline coincide — both obligations fall on the same date.

Financial Year-End Deadline Calculator

Many Singapore companies follow an April–March or October–September financial year, not the UAE's common January–December calendar year. Here's how different financial year-ends translate to UAE CT filing deadlines:

| Financial Year-End | Filing & Payment Deadline | Example |

|---|---|---|

| 31 December | 30 September (following year) | FY ending 31 Dec 2024 → file by 30 Sep 2025 |

| 31 March | 31 December (same calendar year) | FY ending 31 Mar 2025 → file by 31 Dec 2025 |

| 30 June | 31 March (following year) | FY ending 30 Jun 2025 → file by 31 Mar 2026 |

| 30 September | 30 June (following year) | FY ending 30 Sep 2025 → file by 30 Jun 2026 |

The December 31 to September 30 deadline is explicitly confirmed by the FTA: "tax liabilities should be settled through the EmaraTax platform before the payment deadline, which corresponds to the end of September 2025" for a December 31, 2024 year-end.

Before filing, your UAE entity must be registered for corporate tax. Registration deadlines depend on when and how your entity was established.

Registration Deadlines

Established before March 1, 2024 (resident juridical persons): Deadlines depend on the trade licence issuance month per FTA Decision No. 3 of 2024. Licences issued January–February 2024 had a May 31, 2024 deadline; licences issued in December had a December 31, 2024 deadline.

Established on or after March 1, 2024 (resident juridical persons):

- UAE-incorporated entities (including Free Zone Persons): 3 months from date of incorporation

- Foreign entities effectively managed and controlled in UAE: 3 months from end of Financial Year

Non-resident juridical persons with a permanent establishment (PE):

- PE established before March 1, 2024: 9 months from date of PE existence

- PE established on or after March 1, 2024: 6 months from date of PE existence

First Tax Period Rules

For companies incorporated before June 1, 2023, the first tax period may be longer than 12 months (between 6–18 months). The FTA's Public Clarification on the First Tax Period states: "The first Tax Period of a newly established company... is determined by the first Financial Year."

Example for Singapore company: A Singapore parent established a UAE subsidiary on January 1, 2023, with a December 31 financial year-end. The first tax period runs from June 1, 2023 (when corporate tax took effect) to December 31, 2023, covering 7 months. The first filing deadline is September 30, 2024 (9 months after December 31, 2023).

For companies incorporated on or after June 1, 2023, the first tax period starts from the date of incorporation and runs until their chosen financial year-end.

Record-Keeping Requirement

Businesses must maintain financial records and supporting documents for 7 years from the end of the tax period, as the FTA can request these during audits. For Singapore businesses, this means ensuring UAE-entity records are stored and accessible independently of the Singapore parent's books.

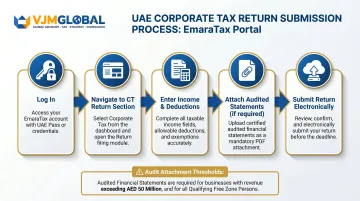

How Singapore Businesses File a UAE Corporate Tax Return

Step 1: Registration on EmaraTax

All UAE corporate taxpayers must register via the FTA's EmaraTax portal to receive a Tax Registration Number (TRN). Singapore businesses managing this remotely should:

- Set up UAE Pass authentication or create an account using email ID and phone number

- Prepare required documents: Certificate of Incorporation, Commercial Registration Certificate, valid Trade License, Emirates ID and passport of owners with 25%+ ownership, and proof of authorization for signatories

- Complete registration through the portal or via UAE Tas'heel Centres

- Alternatively, engage a registered UAE tax agent to handle registration

Step 2: Financial Record Preparation

Before filing, prepare:

Core Financial Statements:

- Income statement

- Balance sheet

- Cash flow statement

Tax Calculations:

- Calculation of taxable income after applying the AED 375,000 exemption

- Schedule of adjustments to accounting income

Transfer Pricing Documentation:

- For related-party transactions between Singapore parent and UAE entity

- Arm's-length pricing analysis consistent with OECD guidelines

- Master File and Local File (if applicable)

Foreign Tax Credit Documentation:

- Evidence of tax paid in Singapore on the same income

- Calculations supporting DTA relief claims

Audited Financial Statements (if required): Per Ministerial Decision No. 84 of 2025, required for:

- Taxable persons with revenue exceeding AED 50 million

- All Qualifying Free Zone Persons (regardless of revenue)

- Tax Groups

Step 3: Submitting the Corporate Tax Return

Via the EmaraTax portal:

- Log in using UAE Pass or registered credentials

- Navigate to Corporate Tax Return section

- Enter income, deductions, exemptions, and taxable income figures

- Cross-check all figures against financial statements; attach audited statements if revenue exceeds AED 50 million or the entity is a Qualifying Free Zone Person

- Submit return electronically

Step 4: Tax Payment

Pay tax on the same date you file the return. Accepted methods:

| Payment Method | Details |

|---|---|

| GIBAN (bank transfer) | Generate unique payment reference via EmaraTax; validated by UAE banks integrated with the platform |

| MagnatiPay | Visa or Mastercard prepaid, debit, or credit cards via online payment gateway |

Critical timing note: The FTA has discontinued e-Dirham. Payments made on the actual deadline day via bank transfer may not process instantly, potentially triggering late payment penalties. Singapore treasury teams should account for AED/SGD conversion and payment processing timelines when scheduling remittances.

Singapore businesses managing these filings remotely may benefit from working with a registered UAE tax agent or a cross-border compliance firm familiar with both jurisdictions — particularly for transfer pricing documentation and DTA relief claims, where errors carry the highest penalty risk.

Penalties for Late Filing or Non-Compliance

Late Registration Penalty

AED 10,000 for failing to register for corporate tax within the prescribed deadline. Per Cabinet Decision No. 75 of 2023 and amendments, Cabinet Decision No. 10 of 2024 added this penalty.

Temporary Waiver (Mostly Expired): The FTA offered a penalty waiver if businesses filed their first return within 7 months of the first tax period end. For calendar-year taxpayers, the deadline was July 31, 2025. Over 33,900 taxpayers benefited before the window closed. As of May 2026, most calendar-year entities can no longer access this waiver.

Late Filing Penalty

- AED 500 per month (or part month) for the first 12 months after the missed deadline

- AED 1,000 per month (or part month) from month 13 onward, continuing until the return is filed

Example: A Singapore business with a December 31, 2024 year-end misses the September 30, 2025 filing deadline. If the return is finally submitted on March 15, 2026:

- October 2025 (partial month): AED 500

- November 2025 – February 2026 (4 months): AED 500 × 4 = AED 2,000

- March 2026 (partial month): AED 500

- Total late filing penalty: AED 3,000

Late Payment Penalty

14% per annum (applied monthly) on unpaid corporate tax from the payment due date. This works out to approximately 1.17% per month, compounding separately from the late filing fine.

If the same business above owed AED 50,000 in tax and paid it on March 15, 2026 (approximately 5.5 months late):

- Late payment surcharge: AED 50,000 × 14% × (5.5/12) = AED 3,208

Combined exposure: AED 3,000 (late filing) + AED 3,208 (late payment) = AED 6,208 in penalties — plus the AED 10,000 late registration penalty if registration was also delayed.

Beyond the financial hit, persistent non-compliance puts your entity on the FTA's radar for audits — which means additional documentation demands, management time, and potential disruption to UAE operations. Getting filings right the first time is the cleaner path.

UAE-Singapore Double Tax Agreement: What Singapore Businesses Should Know

The UAE-Singapore Double Tax Agreement (DTA) prevents the same income from being taxed in both countries. Concluded in 1995 and subsequently updated by the 2014 Protocol and the MLI (effective September 1, 2019), this treaty directly shapes how Singapore businesses structure their UAE operations.

Key DTA Provisions

Withholding Tax Rates (Post-2014 Protocol):

| Income Type | WHT Rate | Treaty Article |

|---|---|---|

| Dividends | 0% | Article 10 (taxable only in recipient's state) |

| Interest | 0% | Article 11 (taxable only in recipient's state) |

| Royalties | 5% | Article 12 (source state may tax up to 5%) |

The 2014 Protocol removed "industrial, commercial or scientific equipment" from the royalties definition, meaning payments for equipment use are reclassified as business profits.

Critical Misconception Clarified

The DTA does not exempt a UAE-registered entity from UAE corporate tax. It provides relief mechanisms — tax credits or exemptions — at the Singapore level when the same income has already been taxed in the UAE.

How it works:

- UAE subsidiary earns AED 1,000,000 profit

- After AED 375,000 exemption, taxable income = AED 625,000

- UAE corporate tax at 9% = AED 56,250

- When dividends are repatriated to Singapore parent, Singapore grants a tax credit for the AED 56,250 UAE tax paid

- Since Singapore's corporate tax rate (17%) is higher than UAE's (9%), the Singapore parent pays the difference on the same income

The DTA uses the credit method from both perspectives. Article 23 specifies: "UAE tax payable... shall be allowed as a credit against Singapore tax payable in respect of that income." Dividends paid by a Singapore company to a UAE company are also exempt from UAE tax "to the extent that the dividends would have been exempt... if both companies had been residents of UAE."

Transfer Pricing Implications

Transactions between a Singapore parent and its UAE subsidiary must be priced at arm's length per OECD guidelines. Under Articles 34-35 of Federal Decree-Law No. 47 of 2022, taxable persons must maintain contemporaneous transfer pricing documentation including:

- Functional analysis (FAR: Functions, Assets, Risks)

- Economic analysis and benchmarking

- Intercompany agreements

- Pricing methodology justification

This applies even if the Singapore parent holds the UAE entity within a broader regional structure.

Preparing Master Files, Local Files, and Country-by-Country Reporting for cross-border structures like these is an area where VJM Global regularly supports clients navigating multi-jurisdiction compliance.

Frequently Asked Questions

What is the last date for corporate tax filing in the UAE?

The deadline is 9 months after the end of the company's financial year-end. For example, if the year ends December 31, the deadline is September 30 of the following year. This date applies to both tax filing and tax payment.

How often must businesses file corporate tax returns in the UAE?

Corporate tax returns must be filed once per year, covering the business's annual tax period (typically 12 months after the first tax period). Returns are submitted through the FTA's EmaraTax portal.

Is there corporate tax in Dubai?

Yes, the UAE — including Dubai — introduced federal corporate tax in June 2023. It applies at 9% on profits above AED 375,000 and is administered by the Federal Tax Authority, covering mainland and free zone businesses alike.

Do Singapore companies with a UAE free zone presence need to file corporate tax?

Yes, free zone entities must register and file corporate tax returns even if they qualify for the 0% rate on qualifying income. Failing to file triggers penalties regardless of whether any tax is owed.

Does the UAE-Singapore Double Tax Agreement affect corporate tax obligations in the UAE?

The DTA prevents double taxation on the same income, but UAE corporate tax filing obligations remain. Singapore businesses must still register and file in the UAE — the DTA's practical value is in claiming tax credits in Singapore for income already taxed in the UAE.

What happens if a Singapore company misses the UAE corporate tax filing deadline?

Late filing incurs AED 500 per month for the first 12 months and AED 1,000 per month thereafter, plus a 14% per annum surcharge on any unpaid tax. Repeated non-compliance can trigger formal FTA audits.