This guide covers the core deadlines every UK limited company must track: CT600 filing, Corporation Tax payment, Companies House accounts, VAT, and PAYE. It also covers the penalty structure for non-compliance and practical steps to stay on top of it all.

Key Takeaways

- The CT600 must be filed within 12 months of the accounting period end

- Corporation Tax must be paid by 9 months and 1 day — before the return is due

- Large companies (profits over £1.5 million) pay Corporation Tax in quarterly instalments

- Very large companies (profits over £20 million) follow an accelerated instalment schedule

- Missing CT600 deadlines triggers £200 penalties from day one, escalating to percentage-based charges at 6 and 12 months

- Companies House accounts, confirmation statements, and VAT/PAYE obligations each run on separate deadlines

Understanding the UK Corporation Tax Accounting Period

All CT deadlines flow from one date: the end of your company's accounting period. Get this wrong, and every subsequent deadline calculation is off.

What the Accounting Period Actually Is

For Corporation Tax purposes, the accounting period is the time covered by the Company Tax Return, as defined by HMRC. It cannot exceed 12 months and is usually the same as the financial year in your statutory accounts.

This is not the same as the UK tax year (April to April). A company with a 31 March year-end has different deadlines than one with a 31 December year-end — even though both file with the same HMRC.

When Two CT Returns Are Required

That 12-month cap becomes important when statutory accounts cover a longer period. Companies House permits accounting periods up to 18 months, but HMRC does not — so if your accounts span more than 12 months, two separate CT600 returns must be filed:

- The first return covers months 1–12

- The second return covers the remaining period

Each carries its own payment and filing deadlines. For a company with an 18-month first period, that means two sets of due dates to track simultaneously.

First-Year Considerations

New companies often have a first accounting period that doesn't fit the standard 12-month pattern — which shifts all subsequent CT deadlines. Key rules to know:

- Companies House sets the first accounting reference date as the last day of the month in which the anniversary of incorporation falls

- First accounts for private companies are generally due within 21 months of incorporation

- A first period shorter or longer than 12 months means your initial CT deadlines will differ from later years

- Companies can confirm exact dates on the Companies House register and opt in to email reminders through the service

UK Corporate Tax Filing and Payment Deadlines Explained

The Four Core Deadlines

| Obligation | Deadline |

|---|---|

| Register for Corporation Tax | Within 3 months of starting business activities |

| Pay Corporation Tax | 9 months and 1 day after the accounting period ends |

| File CT600 (Company Tax Return) | 12 months after the accounting period ends |

| File annual accounts with Companies House | 9 months after the financial year ends |

The critical sequencing point: you pay before you file. The payment deadline arrives three months before the CT600 is due. Companies that wait until the return is complete before paying will already be late.

The CT600 in Detail

The CT600 is the self-assessment form used to report taxable profits, calculate the Corporation Tax liability, and claim any reliefs or allowances. Filing requirements include:

- Online filing only — HMRC only permits paper filing in limited circumstances (reasonable excuse or filing in Welsh)

- iXBRL format required for accounts and computations (Inline eXtensible Business Reporting Language, a machine-readable tagging standard)

- Supporting calculations must accompany the return for the full accounting period

Current Corporation Tax Rates

Accuracy in the CT600 matters because rates vary by profit level:

| Profit Level | Rate |

|---|---|

| Up to £50,000 | 19% (Small Profits Rate) |

| £50,001 – £250,000 | Marginal Relief applies (standard fraction 3/200) |

| Over £250,000 | 25% (Main Rate) |

Companies in the marginal relief band face an effective rate between 19% and 25%, so calculating liability precisely — rather than estimating — can make a meaningful difference to the tax bill.

Payment Methods and Processing Times

Once you know your liability, the payment method you choose determines how much lead time you need. HMRC processing times vary:

| Payment Method | Processing Time |

|---|---|

| Faster Payments / online banking | Same or next day (including weekends) |

| CHAPS | Same working day (within bank processing times) |

| Debit or corporate credit card | Same day as payment made |

| Bacs transfer | Up to 3 working days |

| Direct Debit (existing) | Up to 3 working days |

| Direct Debit (new setup) | Up to 5 working days |

Note: HMRC does not accept personal credit cards for Corporation Tax payments.

Corporation Tax Payment Rules: Large and Very Large Companies

Standard 9-months-and-1-day payment rules only apply to smaller companies. Once profits cross certain thresholds, quarterly instalment payments become mandatory — and the schedule is earlier than most directors expect.

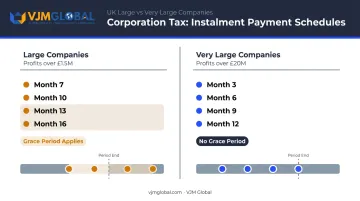

Large Companies (Profits Over £1.5 Million)

A company is "large" for instalment purposes if annual taxable profits exceed £1.5 million — but this threshold is divided by the number of associated companies, including the company itself. A group of four associated companies each has an effective threshold of £375,000.

For a standard 12-month accounting period, instalments fall on the 14th day of months 7, 10, 13, and 16, with the first instalment landing 6 months and 13 days after the period start.

Exceptions — a company can revert to the standard payment deadline if:

- Total CT liability is under £10,000

- The company was not large in the previous 12 months and profits do not exceed £10 million

Very Large Companies (Profits Over £20 Million)

The threshold rises to £20 million (divided by associated companies and reduced proportionally for short accounting periods). With 7 associated companies, for instance, the very large threshold drops to £20M ÷ 8 = £2.5 million per company.

Very large companies follow an accelerated schedule, with instalments due on the 14th day of months 3, 6, 9, and 12 of the accounting period. Unlike the large company rules, there is no first-year grace period when a company newly crosses this threshold.

Key differences from the large company regime:

- Instalments begin in month 3 (vs. month 7 for large companies)

- No grace period applies in the year a company first becomes very large

- Profit forecasting must be more current, as payments fall within the accounting period itself

Interest accrues on late or underpaid instalments from the due date. The current HMRC late payment rate is 7.75% (as of January 2026). For very large companies, this means an underpayment identified after the period ends could carry interest from month 3 — well before the final liability is known.

Penalties for Late Filing and Late Payment

CT600 Late Filing Penalties

HMRC's current penalty structure for late CT600 filing is:

| Lateness | Penalty |

|---|---|

| 1 day late | £200 |

| 3 months late | Another £200 |

| 6 months late | 10% of unpaid tax added |

| 12 months late | Another 10% of unpaid tax |

| 3 consecutive late returns | £200 flat penalties increase to £1,000 each |

These penalties stack on top of interest charges on unpaid tax — they are not an alternative to interest, they are in addition to it.

If You Cannot Pay on Time

If you cannot pay in full, act before the deadline — not after. HMRC offers Time to Pay (TTP) arrangements with structured repayment by instalment. Key steps:

- Contact HMRC's Business Payment Support Service before the due date

- Request a Time to Pay arrangement to agree a repayment schedule

- Early contact demonstrates good faith; ignoring the debt leads to enforcement action

More information on setting up a payment plan is available at HMRC's guidance on difficulties paying.

Companies House Penalties — A Separate Regime

Companies House imposes its own penalty structure for late annual accounts, entirely separate from HMRC:

| Lateness | Penalty (Private Company) |

|---|---|

| Up to 1 month | £150 |

| 1 to 3 months | £375 |

| 3 to 6 months | £750 |

| More than 6 months | £1,500 |

If accounts are filed late in two successive financial years, every penalty doubles. This means a company that misses deadlines two years running faces up to £3,000 from Companies House alone — on top of any HMRC penalties for the same periods.

Other Corporate Compliance Deadlines in the UK

Beyond corporation tax, UK companies must meet three other recurring compliance obligations: the confirmation statement, VAT returns, and PAYE reporting.

Confirmation Statement

Every limited company must file a confirmation statement (formerly the annual return) at least once every 12 months. Key requirements include:

- Filed within 14 days of the end of the confirmation period

- Confirms or updates details on directors, shareholders, and registered office

- Failure to file can result in Companies House striking the company off the register

VAT Obligations

For VAT-registered companies:

- VAT return and payment are due 1 month and 7 days after the end of each VAT quarter

- Registration is required if taxable turnover exceeds £90,000 in the last 12 months

- Under Making Tax Digital for VAT (live for all VAT-registered businesses since April 2022), digital records must be kept and returns submitted via MTD-compatible software

PAYE Obligations

For companies with employees:

- Full Payment Submission (FPS): Must be sent on or before each payday

- Monthly PAYE payments: Due by the 22nd of the following month for electronic payments; 19th if paying by post

- PAYE bills include employee income tax, Class 1 National Insurance, and any CIS deductions

- Late FPS submissions trigger in-year penalties from HMRC, scaled by the number of employees on payroll

How to Stay on Top of Your UK Corporate Tax Obligations

Practical Steps

- Record your accounting period end date — calculate and calendar every deadline from this single reference point

- Set tiered reminders at 90, 60, and 30 days before each key deadline

- Keep monthly bookkeeping current — last-minute rushes before CT600 deadlines are the primary cause of filing errors and late payments

- Keep contact details updated with both HMRC and Companies House to receive official correspondence

- Set up a Government Gateway account for the company (separate from the director's personal account) to monitor HMRC notices and correspondence

Working with a UK Tax Compliance Partner

These practical steps cover the essentials — but some businesses face significantly more complex CT obligations. Foreign-owned subsidiaries, group structures, and companies with cross-border operations typically contend with:

- Associated company threshold calculations

- Two-return requirements for long accounting periods

- Instalment payment forecasting across multiple entities

VJM Global has supported 250+ UK businesses across 15+ industries with accounting outsourcing and tax compliance services, maintaining a 95% client retention rate. The firm's Chartered Accountants and CPAs provide end-to-end compliance support suited to UK companies with cross-border operations, including those managing activities in India. For enquiries about UK corporate tax compliance support, contact info@vjmglobal.com.

A Note on Making Tax Digital for Corporation Tax

MTD for VAT is already live and mandatory for all VAT-registered businesses. MTD for Corporation Tax is a different matter: HMRC's 2025 Transformation Roadmap states that HMRC does not currently intend to introduce MTD for Corporation Tax. Earlier consultation proposals about quarterly CT reporting have been superseded by this position. No mandatory MTD for CT start date exists as of 2026.

Frequently Asked Questions

What is the deadline for a UK corporate tax return?

The CT600 must be filed within 12 months of the end of the accounting period (a date specific to each company, not a fixed calendar deadline). The Corporation Tax payment deadline is earlier: 9 months and 1 day after the period ends.

What happens if I don't do my tax return by October 31?

October 31 is the paper Self Assessment deadline for individuals — it has no relevance to Corporation Tax. For limited companies, the CT600 deadline is 12 months after the accounting period ends. Missing that deadline triggers an immediate £200 penalty, with further penalties at 3 months, 6 months, and 12 months.

When should a company register for Corporation Tax with HMRC?

New companies must register within 3 months of starting business activities (not the incorporation date). Registration is completed online via HMRC's Government Gateway. Late registration can itself attract penalties.

Can I get an extension on my corporation tax return filing deadline?

HMRC does not routinely grant extensions to the CT600 deadline. An extension to the Companies House accounts deadline (up to 3 months) can be applied for in exceptional circumstances, which may indirectly affect the CT return timeline — though it does not extend the Corporation Tax payment deadline.

Does a dormant company need to file a corporation tax return?

After notifying HMRC of dormancy, the company will not need to file further CT600 returns unless HMRC requests one or trading resumes. However, dormant Companies House filing obligations remain : private companies must still file dormant accounts 9 months after the financial year ends.

What is the quarterly instalment payment schedule for large companies?

Companies with profits over £1.5 million pay instalments on the 14th of months 7, 10, 13, and 16 of the accounting period. Very large companies (profits over £20 million) use months 3, 6, 9, and 12. Both thresholds are divided by the number of associated companies and scaled down for accounting periods shorter than 12 months.