Introduction

Singapore consistently ranks among the world's most competitive business hubs. Ranked #2 globally in the IMD World Competitiveness Ranking 2025, the city-state offers international businesses low regulatory friction, direct access to Asian markets, and efficient tax administration. For companies operating in or selling into Singapore, GST compliance is a core requirement — and getting it wrong carries real consequences.

In 2026, businesses face several specific compliance challenges:

- Correctly categorizing supplies to determine applicable GST treatment

- Identifying when registration thresholds are triggered

- Implementing mandatory InvoiceNow e-invoicing for voluntary GST registrants

- Understanding Overseas Vendor Registration (OVR) rules for cross-border sellers

Misclassification or late registration can trigger backdated assessments, penalties, and IRAS audits.

This guide covers the key areas for 2026 compliance:

- The current 9% GST rate and when it applies

- Four supply categories and their distinct tax treatment

- Registration thresholds under retrospective and prospective tests

- Foreign business obligations under OVR

- Quarterly filing requirements through IRAS's myTax Portal

TLDR: Key Facts About Singapore GST in 2026

- The current Singapore GST rate is 9%, effective since 1 January 2024; no rate change is expected in 2026 or the foreseeable future

- Businesses must register when taxable turnover exceeds SGD 1 million in any 12-month period; voluntary registration is permitted with a 2-year minimum commitment

- Four supply categories—standard-rated (9%), zero-rated (0%), exempt, and out-of-scope—each carry different GST treatment and input tax recovery rights

- Foreign businesses selling digital services or low-value goods to Singapore consumers trigger OVR registration above SGD 1M global turnover and SGD 100K in Singapore sales

- From 1 April 2026, new voluntary registrants must use InvoiceNow-compatible e-invoicing; full compliance for all GST registrants is required by 2031

Singapore's GST Rate in 2026: Current Rate and Historical Context

The prevailing Singapore GST rate is 9%, which took effect on 1 January 2024. This completed a two-stage increase from 7% announced in Budget 2022: the first increase to 8% occurred on 1 January 2023, followed by the second increase to 9% on 1 January 2024.

Budget 2026 confirmed that there is no change to the GST rate—it remains at 9%. No further rate increases are planned, and the 9% rate is now the settled standard for businesses to plan around.

Historical GST Rate Timeline

| Period | GST Rate |

|---|---|

| 1 Apr 1994 - 31 Dec 2002 | 3% |

| 1 Jan 2003 - 31 Dec 2003 | 4% |

| 1 Jan 2004 - 30 Jun 2007 | 5% |

| 1 Jul 2007 - 31 Dec 2022 | 7% |

| 1 Jan 2023 - 31 Dec 2023 | 8% |

| 1 Jan 2024 - present | 9% |

GST was introduced in Singapore on 1 April 1994 at 3% and has been adjusted six times over 30 years. The deliberate, gradual approach to rate increases reflects Singapore's preference for policy predictability. That predictability matters for compliance planning — and it becomes clearer when you set Singapore's rate against what other major economies charge.

How Singapore's Rate Compares Globally

Singapore's 9% GST is among the lowest consumption tax rates worldwide. By comparison:

- United Kingdom VAT: 20%

- EU average VAT: Approximately 21-22%

- Australia GST: 10%

- Japan Consumption Tax: 10%

- Canada GST (federal): 5%

Singapore applies a low rate broadly, with limited exemptions, rather than layering in the reduced-rate categories common in Europe. For businesses operating across multiple jurisdictions, this makes Singapore one of the more straightforward GST regimes to navigate.

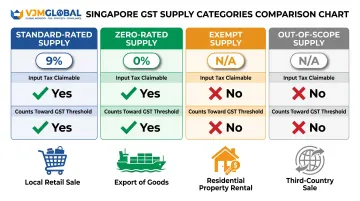

What Singapore GST Applies To: The 4 Supply Categories

Under Singapore's Goods and Services Tax Act, all supplies fall into one of four categories. Correct classification determines the GST rate, input tax recovery eligibility, and whether the supply counts toward the SGD 1 million registration threshold.

Supply Category Overview

| Category | GST Rate | Input Tax Claimable? | Counts Toward Threshold? |

|---|---|---|---|

| Standard-rated | 9% | Yes | Yes |

| Zero-rated | 0% | Yes | Yes |

| Exempt | N/A | No | No |

| Out-of-scope | N/A | No | No |

Standard-Rated Supplies (9%)

This covers the majority of goods and services supplied in Singapore:

- Retail goods and consumer products

- Professional and consulting services

- Food and beverage sales

- Accommodation services

- Digital subscriptions sold to local customers

- Commercial property transactions

Businesses charge 9% GST and remit the net amount (output tax minus input tax) to IRAS quarterly.

Zero-Rated Supplies (0% GST)

Zero-rated supplies are technically taxable but charged at 0%. Two main types qualify:

- Exports of goods shipped outside Singapore

- Qualifying international services: international flights, freight, and services provided to overseas persons where the benefit is received outside Singapore

The key advantage: suppliers charge no GST but retain full entitlement to claim input tax on business expenses. This makes zero-rating highly favorable for export-heavy businesses, as it creates a net refund position.

Exempt Supplies

Unlike zero-rated supplies, exempt supplies carry a real cost: no GST is charged, but input tax on related expenses cannot be claimed. Examples include:

- Most financial services: bank account fees, loans, insurance policies, currency exchange

- Sale and lease of residential properties

- Investment-grade precious metals: gold, silver, platinum

- Digital payment tokens

Because input tax cannot be recovered, exempt supplies increase the overall tax burden on businesses making them.

Out-of-Scope Supplies

These transactions occur wholly outside Singapore and do not attract GST. They do not count toward the registration threshold. Examples:

- Goods sold and delivered from one foreign country to another (never entering Singapore)

- Sales of goods within Free Trade Zones or Zero GST Warehouses

- Private (non-business) transactions

Why Classification Matters

Misclassification is a top IRAS audit finding — and the consequences stack up fast. Getting it wrong affects:

- The GST rate charged (9%, 0%, or none)

- Input tax recovery eligibility

- Sales counted toward the SGD 1M registration threshold

Misclassifying zero-rated exports as out-of-scope, for example, can cause a business to miss its registration obligation and forfeit input tax recovery rights at the same time.

GST Registration Requirements: Thresholds, Tests, and Process

Compulsory Registration Threshold

A business must register for GST when its taxable turnover exceeds SGD 1 million in any 12-month period. Taxable turnover includes standard-rated and zero-rated supplies only—not exempt or out-of-scope supplies.

IRAS applies two tests to determine liability:

Retrospective Test:

- If taxable turnover for the calendar year (1 January to 31 December) exceeds SGD 1M

- The business must apply between 1 January and 30 January of the following year

- Effective registration date: 1 March of that year

Prospective Test:

- At any point, the business reasonably expects taxable turnover to exceed SGD 1M in the next 12 months

- Must apply within 30 days of forming that expectation

- For forecasts made on or after 1 July 2025, the effective date is 2 months from the forecast date (extended grace period)

Voluntary Registration

Businesses below the SGD 1M threshold may register voluntarily. Key considerations:

Voluntary registration offers tangible advantages for B2B-focused businesses:

- Recover input tax on business expenses

- Enhance credibility with larger corporate clients

- Level the playing field when competing with GST-registered suppliers

Before registering voluntarily, note these binding conditions:

- Must remain registered for a minimum of 2 years

- Must fulfill all GST obligations: charging GST, filing returns, maintaining records

- From 1 April 2026, new voluntary registrants must transmit invoice data via the InvoiceNow network (Peppol standard) by the earlier of the filing date or filing due date

Consequences of Failing to Register on Time

IRAS has authority to:

- Backdate registration to the date the business was originally liable

- Require payment of GST on all sales from the backdated date, even if GST was not collected from customers

- Impose a fine of up to SGD 10,000

- Impose a penalty of 10% of the GST due

- Pursue prosecution

IRAS waives the fine and 10% penalty for businesses that voluntarily disclose late registration — though backdated GST remains payable regardless. Tracking turnover against the SGD 1M threshold monthly, rather than annually, gives businesses enough lead time to register before liability kicks in.

GST Rules for Foreign and Overseas Businesses in Singapore

Overseas Vendor Registration (OVR) Regime

Foreign businesses with no physical presence in Singapore must register under OVR when both thresholds are met:

- Global annual turnover exceeds SGD 1 million, AND

- B2C supplies to Singapore customers (non-GST-registered persons) exceed SGD 100,000 annually

Scope of OVR

Remote Services (effective 1 January 2020):

- Digital services: streaming subscriptions, downloadable software, online courses, e-books

- Non-digital services supplied remotely: online counseling, telemedicine, consultancy

- Travel arranging services

Low-Value Goods (LVG) (effective 1 January 2023):

- Goods located outside Singapore at point of sale

- Customs value at or below SGD 400

- Delivered via air or post

- Must not be GST-exempt or dutiable goods

Pay-Only Registration Scheme

OVR vendors operate under a simplified "pay-only" regime:

- Reduced registration and reporting requirements

- Must charge and remit GST on B2C supplies to Singapore customers

- Cannot claim input tax credits

This keeps compliance lighter but limits cost recovery — an important trade-off to factor in before choosing how to structure overseas sales channels.

Electronic Marketplace Deemed Supplier Rules

When overseas suppliers sell through digital platforms such as app stores or online marketplaces, IRAS may designate the platform operator as the deemed supplier, making them responsible for GST accounting. Key implications for overseas sellers include:

- The platform — not the seller — may be required to register and remit GST

- Sellers must confirm with each platform who holds the GST obligation

- Misaligned assumptions can result in double-charging or under-reporting

Reverse Charge Mechanism

GST-registered Singapore businesses that procure imported services or low-value goods from overseas suppliers not registered under OVR must self-account for GST under the reverse charge. This ensures tax is collected even when the overseas supplier has no registration obligation.

For USA, UK, and Australian businesses that also operate in or through India, understanding how Singapore's OVR obligations interact with Indian GST and transfer pricing rules is a separate — and often overlooked — compliance layer.

GST Filing, Invoicing, and Ongoing Compliance Obligations

GST Return Filing Process

Standard frequency: Quarterly returns (Form GST F5) via IRAS's myTax Portal

Accounting periods:

- January–March

- April–June

- July–September

- October–December

Filing and payment deadline: One month after the end of the accounting period (for example, 30 April for the January–March quarter)

GIRO enrollment: Provides an additional 15 days of payment credit

Refund processing: Over 95% of GST refunds are paid within 7 days. Businesses can receive faster refunds by enrolling in GIRO or PayNow linked to their UEN.

Tax Invoice Requirements

A tax invoice must be issued within 30 days from the time of supply when the customer is GST-registered. The time of supply is determined by whichever comes first:

- Date of payment

- Date the invoice is issued

12 mandatory fields on a standard tax invoice:

- The words "Tax Invoice" (prominently displayed)

- Supplier's name and address

- Supplier's GST registration number

- Invoice date

- Unique invoice serial number

- Customer's name

- Customer's address

- Description of goods and services

- GST rate (9%)

- Total amount payable excluding GST

- Total GST amount

- Total amount payable including GST

Simplified tax invoice: May be issued when total amount (including GST) does not exceed SGD 1,000. Requires fewer fields and does not require customer name and address.

Record-Keeping and Compliance Best Practices

Proper documentation is as important as accurate filing — IRAS expects a complete audit trail at every stage. Retain all of the following for at least 5 years:

- Tax invoices issued and received

- Receipts, credit notes, and debit notes

- Import/export permits and customs documentation

- Accounting records and bank statements supporting GST returns

Common GST Compliance Errors

In FY2024/2025, IRAS completed more than 2,800 GST audits, recovering SGD 205 million (including penalties). Common errors include:

- Incorrect supply classification — for example, treating zero-rated exports as out-of-scope

- Charging GST before registration is effective

- Failing to account for GST on imported services (reverse charge omissions)

- Input tax claims without valid tax invoices

- Poor record management and failure to maintain documentation for 5 years

- Accounting system errors leading to automated reporting mistakes

IRAS offers lower or no penalties for voluntary disclosure of errors. Errors must be corrected within 5 years from the end of the relevant accounting period.

Frequently Asked Questions

What is the sales tax (GST) rate in Singapore and will it change in the coming years?

The current GST rate is 9%, effective since 1 January 2024. Budget 2026 confirmed no rate change, and no further increases have been officially announced for 2026 or the near term.

Does Singapore use GST or VAT?

Singapore uses GST (Goods and Services Tax), not VAT — though the two are functionally equivalent. It's a value-added consumption tax charged at each stage of the supply chain, so businesses familiar with VAT will find the compliance logic nearly identical.

Is sales tax (GST) included in retail prices in Singapore?

Yes, GST-registered businesses must display and quote GST-inclusive prices to consumers. When filing returns, businesses separate out the GST component from the total price collected.

Do tourists and foreign visitors have to pay sales tax (GST) in Singapore?

Tourists purchasing goods or services from GST-registered businesses pay GST as part of the price. Eligible tourists can reclaim that GST on qualifying purchases when departing through the Tourist Refund Scheme (TRS).

Can tourists get sales tax (GST) refunds in Singapore?

Eligible tourists can claim GST refunds on qualifying purchases through the Tourist Refund Scheme (TRS), with a minimum spend of SGD 100 (including GST). Refunds are processed at eTRS kiosks at Changi and Seletar airports — credit card refunds arrive within 10 days, while Alipay payments are immediate.