Introduction

The UAE has transformed into a dual tax compliance jurisdiction over the past seven years. VAT took effect on 1 January 2018, followed by Corporate Tax for periods commencing on or after 1 June 2023. For Singapore businesses managing UAE subsidiaries or branches, both entities now fall within the Federal Tax Authority's (FTA) audit scope.

Unlike Singapore's IRAS system, the UAE's tax audit framework operates on a risk-driven model with distinct procedural requirements — covering everything from audit selection criteria to record-keeping mandates and penalty structures.

This guide covers what Singapore finance teams need to know before an FTA audit arrives:

- What a UAE tax audit involves and who triggers one

- How the FTA selects businesses for review

- The step-by-step audit process

- Mandatory record retention periods

- Practical preparation strategies for Singapore-headquartered operations

Key Takeaways

- The FTA can audit any VAT or Corporate Tax-registered business at any time using risk-based selection models

- Minimum audit notice is 10 business days under current law — shorter notice applies only in suspected tax evasion cases

- UAE revenue above AED 50 million requires audited financial statements from a UAE-licensed auditor

- Corporate Tax records require 7-year retention; VAT records require 5 years (10 years for capital assets)

- Non-compliance triggers formal tax assessments plus administrative penalties calculated on underpaid tax

What Is a UAE Tax Audit?

A UAE tax audit is a formal examination of business records, tax returns, and financial documents conducted by the FTA to verify compliance with Federal Decree-Law No. 28 of 2022 (Tax Procedures Law), the VAT Law, and the Corporate Tax Law. This is distinct from voluntary financial audits or statutory audits required under UAE Companies Law.

Singapore businesses may face two distinct audit types:

- VAT Audits: Cover whether your business correctly charged and remitted VAT at 5%, classified zero-rated and exempt supplies accurately, and calculated input tax credits correctly.

- Corporate Tax Audits: Review profit declarations, transfer pricing documentation for intercompany transactions, allowable deductions, and return accuracy under the CT regime effective June 2023.

These audits aren't limited to your registered office. Under Article 16 of the Tax Procedures Law, the FTA can conduct audits at:

- FTA headquarters

- The business's registered premises

- Any location where records, goods, or inventory are maintained

- Warehouses and branch offices

What Triggers a UAE Tax Audit?

The FTA does not require a specific reason to initiate an audit. The FTA's 2023-2026 Strategy confirms audits are risk-driven using ISO 31000-certified risk management frameworks, not random selection.

Key risk indicators include:

- Turnover discrepancies between VAT returns and Corporate Tax filings

- Large transaction volumes or complex cross-border structures

- Late or incorrect return submissions

- Transfer pricing adjustments not reflected in VAT valuations

- Significant acquisitions or unusual financial patterns

- Reverse-charge mechanism inconsistencies

The FTA conducted 93,000 inspection visits in 2024 — a 135% year-on-year increase — signaling heightened enforcement across both tax types.

How the UAE Tax Audit Process Works

The FTA conducts audits in four defined stages — from issuing formal notice to delivering a tax assessment. Each stage carries specific obligations, and missteps at any point can extend the audit or trigger penalties.

Audit Stage 1: Notice of Audit

The FTA must issue written notice at least 10 business days before the scheduled audit, specifying:

- Audit scope and tax type (VAT, Corporate Tax, or both)

- Scheduled date and location

- Required documents and personnel

Critical exception: No advance notice is required if the FTA suspects tax evasion or believes prior notification would hinder the investigation. In such cases, the FTA may conduct unannounced inspections and temporarily close premises for up to 72 hours.

Audit Stage 2: Document Request and On-Site Review

FTA auditors request original records and certified copies across all relevant tax periods, including:

- Tax invoices issued and received

- VAT and Corporate Tax returns

- Financial statements and general ledgers

- Customs declarations for imports

- Transfer pricing documentation

- Bank statements and payment records

Auditors may also inspect physical inventory and assets, and interview relevant staff. The audited party — including appointed tax agents or legal representatives — must provide full access and assistance throughout. Failure to cooperate carries an AED 20,000 administrative penalty.

Audit Stage 3: Data Analysis and Clarifications

Auditors analyze submitted records to identify discrepancies between reported figures and actual transactions. For Singapore businesses with cross-border supply chains or intercompany arrangements, the FTA pays particular attention to:

- Input tax credit claims without proper supporting invoices

- Incorrect VAT classification of supplies

- Transfer pricing alignment with arm's length principles

- Deductions claimed without adequate documentation

The FTA may raise queries requiring written responses and additional documentation. If suspicious findings emerge, the FTA holds authority to order a re-audit.

Audit Stage 4: Findings and Outcome

Upon completion, the FTA communicates results. If non-compliance is identified — such as VAT underpayment, incorrect return filing, or Corporate Tax calculation errors — the FTA issues a formal tax assessment detailing:

- Outstanding tax amounts

- Applicable administrative penalties

- Payment deadlines

Businesses receive formal notification within 10 business days of assessment issuance. If you disagree with the outcome, a multi-step appeal process is available — starting with a reconsideration request to the FTA before escalating to the Tax Disputes Resolution Committee.

Key Records and Documents Singapore Businesses Must Maintain in the UAE

Record retention obligations differ significantly from Singapore's requirements.

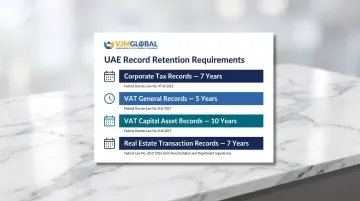

Retention Periods:

- Corporate Tax records: 7 years after the end of the relevant tax period (Article 56, Federal Decree-Law No. 47 of 2022)

- VAT records (general): 5 years

- VAT capital asset records: 10 years

- Real estate transaction records: 7 years

Core VAT Records (Article 78, VAT Law):

- Records of all supplies and imports

- Tax invoices issued and received (including alternative documents)

- Tax credit notes issued and received

- Records of zero-rated and exempt supplies

- Customs declarations and supplier invoices for imports

- Records of adjustments to accounts or tax invoices

- Documentation of goods/services used for non-business purposes

- Reverse-charge mechanism declarations

Corporate Tax Financial Statement Requirements

Key thresholds under Ministerial Decision No. 84 of 2025:

- Revenue above AED 50 million: Audited financial statements required, prepared by a UAE-licensed auditor under IFRS standards

- Free Zone subsidiaries (QFZPs): Audited IFRS financial statements are mandatory regardless of revenue level to maintain the 0% Corporate Tax rate

FTA Audit File (FAF)

The FAF is a structured digital format containing transactional-level VAT data that the FTA may request during a VAT audit. It is not a mandatory periodic filing, but VAT-registered businesses — including Singapore-owned UAE branches — must be ready to export accounting data in the FTA's prescribed CSV format on demand.

The FAF specification is supported by major accounting platforms including Microsoft Dynamics and Oracle NetSuite.

How Singapore Businesses Can Prepare for a UAE Tax Audit

Effective preparation begins long before an audit notice arrives. UAE tax compliance works best as an ongoing operational function — not something you scramble to address when the FTA comes calling.

Internal Review Steps:

Conduct periodic compliance health checks covering:

- Accounting System Verification: Confirm VAT and Corporate Tax calculations are automated and consistently accurate across all transactions

- VAT Classification Review: Check that standard-rated (5%), zero-rated, and exempt supplies are correctly applied — misclassification is one of the most common audit triggers

- Corporate Tax Return Accuracy: Reconcile profit calculations, deductions, and loss carry-forwards against your financial statements

- Filing Deadline Compliance: VAT returns follow FTA-assigned cycles; Corporate Tax returns are due 9 months after the tax period ends

Transfer Pricing Compliance:

Transfer pricing is a specific audit focus for Singapore businesses with UAE subsidiaries. The FTA examines whether intercompany transactions — management fees, IP licensing, shared services, or loans between the UAE entity and Singapore parent — are conducted at arm's length.

Singapore businesses should:

- Maintain contemporaneous transfer pricing documentation before transactions occur

- Prepare master files covering global operations

- Develop local files detailing UAE subsidiary-specific intercompany transactions

- Conduct benchmarking studies using comparable market data

- Document the rationale for selected transfer pricing methodologies

Professional Advisory Support:

Working with qualified tax advisors who understand both UAE and Singapore regulatory frameworks reduces audit risk significantly. Businesses can appoint a registered Tax Agent with the FTA who liaises directly with auditors on their behalf — a practical step for any Singapore entity without dedicated UAE in-house tax staff.

Practical Preparation Tips:

- Implement a formal document retention policy aligned with UAE's 7-year requirement

- Maintain open communication with FTA auditors during the audit process

- Ensure relevant staff are available for interviews on short notice

- Keep original documents accessible in both physical and digital formats

- Conduct mock audit exercises to identify gaps before actual FTA review

- Translate key documents to Arabic if requested (failure to comply carries AED 20,000 penalty)

Taken together, these steps shift audit preparation from a last-minute scramble into a manageable compliance routine — one that reduces both exposure and disruption when the FTA does make contact.

Consequences of Non-Compliance and Post-Audit Outcomes

Tax assessments issued after audits trigger both tax collection and administrative penalties. The most common scenarios that lead to assessments include:

- VAT underpayment or over-claimed input tax

- Failure to register for VAT within the required timeframe

- Late filing or non-filing of returns

- Incorrect Corporate Tax calculations

- Missing or inadequate transfer pricing documentation

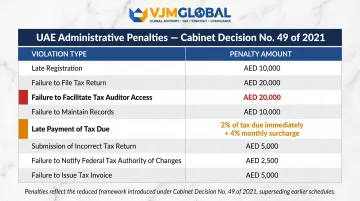

Administrative Penalties (Cabinet Decision No. 49 of 2021):

| Violation | Penalty |

|---|---|

| Failure to register for VAT on time | AED 10,000 |

| Late submission of tax return (first offense) | AED 1,000 |

| Late submission of tax return (repeat within 24 months) | AED 2,000 |

| Submitting incorrect tax return (first offense) | AED 1,000 |

| Late payment of declared tax | 2% immediately + 4% monthly (capped at 300%) |

| Failure to voluntarily disclose error before audit | 50% of error amount + 4% monthly |

| Failure to maintain required records (first offense) | AED 10,000 |

| Failure to facilitate tax auditor | AED 20,000 |

These penalties were considerably reduced from the original 2017 framework — for example, the previous 1% daily late payment penalty was eliminated in favour of the current 2% + 4% monthly structure.

Administrative penalties, however, are separate from criminal liability for deliberate misconduct.

Tax Evasion Penalties:

Tax evasion — covering deliberate misrepresentation, document destruction, or intentional non-payment — is treated as a criminal matter. Penalties include imprisonment and fines up to five times the evaded tax amount. The FTA treats cooperation during audits as a mitigating factor.

Dispute Resolution Process:

Singapore businesses can challenge FTA tax assessments through a formal multi-step process:

- Tax Assessment Review (Article 28) — Submit within 40 business days of assessment notification

- Reconsideration Request (Article 29) — File within 40 business days of Review decision

- Objection to Tax Disputes Resolution Committee (Articles 30-35) — Lodge within 40 business days of Reconsideration decision

- Appeal to Competent Court — File within 40 business days of TDRC decision

Missing any of these 40-business-day windows forfeits that stage of appeal. Extensions are available under specific conditions outlined in Executive Regulation Article 25, so Singapore businesses should act promptly once an assessment is received.

Frequently Asked Questions

Is a tax audit mandatory in the UAE?

An FTA tax audit is not mandatory on a fixed schedule — it is initiated at the FTA's discretion based on risk assessment. However, businesses with revenue exceeding AED 50 million or those classified as Qualifying Free Zone Persons must have their financial statements independently audited by a UAE-licensed auditor annually.

What is the turnover limit for a tax audit in the UAE?

There is no minimum turnover threshold for the FTA to initiate a compliance audit — any VAT or Corporate Tax-registered business can be selected regardless of revenue. The AED 50 million threshold specifically triggers the mandatory audited financial statement requirement under Corporate Tax Law, not FTA audit selection.

How much does a tax audit cost in the UAE?

The FTA does not charge businesses a fee for conducting tax audits. However, businesses typically incur costs engaging tax agents or advisors to assist with preparation and representation. Audits that uncover non-compliance can result in substantial tax assessments and penalties.

Who is required to have a tax audit in the UAE?

Any VAT or Corporate Tax-registered business can be subject to an FTA audit at any time. Businesses above the AED 50 million revenue threshold and Qualifying Free Zone Persons face the additional requirement of annual audited financial statements — as outlined above.

What records must Singapore businesses maintain for a UAE tax audit?

VAT records — tax invoices, returns, and customs declarations — must be retained for at least 5 years (10 years for capital assets); Corporate Tax records require 7 years. Documentation should cover financial statements, general ledgers, and transfer pricing records for intercompany transactions with the Singapore parent.

How does a UAE Corporate Tax audit differ from a VAT audit?

A VAT audit examines the accuracy of VAT charged, collected, and remitted — covering invoice compliance and input tax credit claims. A Corporate Tax audit reviews financial records, profit calculations, deductions, and transfer pricing under the CT Law introduced in June 2023. Singapore businesses with UAE entities may face both.