Introduction

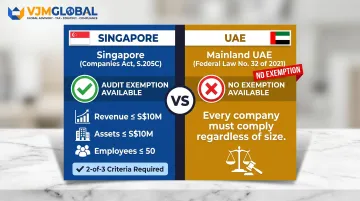

Singapore businesses expanding into the UAE mainland face a compliance obligation that operates differently from Singapore's framework: **every mainland UAE company must undergo a mandatory annual external audit**, regardless of size, revenue, or number of employees.

This catches many Singapore founders off guard. Under Singapore's Companies Act, small companies meeting specific thresholds can be audit-exempt — but no such exemption exists for UAE mainland entities.

From day one of operations, your UAE Limited Liability Company (LLC) or Public Joint Stock Company (PJSC) must appoint a UAE Ministry of Economy-licensed auditor and file audited financial statements annually.

This guide covers the legal framework, the audit process, what your finance team needs to prepare, and the consequences of non-compliance — so your UAE entity stays on the right side of the law.

Key Takeaways

- All mainland UAE companies face mandatory annual external audit under Article 27 of Federal Law No. 32 of 2021

- Revenue above AED 50 million triggers audited financial statement requirements for corporate tax compliance (Ministerial Decision No. 84 of 2025)

- Only UAE Ministry of Economy-licensed auditors can sign off on mainland audit reports; Singapore CA firms cannot sign mainland audit reports

- Retention periods differ: 7 years for corporate tax records, 10 years for VAT capital asset documentation

- Non-compliance triggers fines starting at AED 10,000, plus potential trade licence renewal complications

What Is a Mainland UAE Company Audit?

A mainland UAE company audit is an independent examination of your entity's financial statements, conducted by a third-party licensed auditor, to verify that accounts are accurate, complete, and comply with UAE laws and International Financial Reporting Standards (IFRS).

This is not the same as internal audit functions, routine bookkeeping reviews, or outsourced accounting. A statutory external audit carries legal weight and must produce a formal auditor's report — one that regulators and banks will actually rely on.

That report can be required by the Department of Economy and Tourism (DED), the Federal Tax Authority (FTA), and UAE banks at any point.

For Singapore-based businesses, this is where UAE rules diverge sharply from what you may be used to at home:

| Framework | Audit Exemption Available? | Threshold |

|---|---|---|

| Singapore (Companies Act, S.205C) | Yes | Revenue ≤ S$10M, assets ≤ S$10M, employees ≤ 50 (2 of 3) |

| Mainland UAE | No | Every company must comply, regardless of size |

In mainland UAE, every registered entity must undergo a statutory audit — there are no size-based carve-outs.

The Legal Framework: Who Needs an Audit and When

Universal Audit Mandate Under Article 27

The governing provision is Article 27(1) of Federal Law No. 32 of 2021 (UAE Commercial Companies Law), which states: "Every Joint Stock Company or Limited Liability Company shall have one or more auditors to audit the accounts of the Company on a yearly basis."

Key points:

- Applies to all mainland LLCs and PJSCs

- No minimum size, revenue, or shareholder threshold

- Auditor must be appointed annually by shareholders at the general assembly

Corporate Tax Audit Threshold: AED 50 Million

Under Ministerial Decision No. 84 of 2025 (effective for tax periods from 1 January 2025), businesses with annual revenue exceeding AED 50 million must maintain audited financial statements for corporate tax filing purposes.

This threshold applies independent of the Article 27 obligation — mainland companies below AED 50 million still require an annual audit under Commercial Companies Law, but those exceeding it face an additional corporate tax compliance layer.

Submission Timeline

| Entity Type | Financial Statement Preparation Deadline |

|---|---|

| LLC | 3 months from financial year-end (Article 87) |

| PJSC | 4 months from financial year-end (Article 238) |

Singapore parent companies with LLC subsidiaries face a tighter compliance window than PJSCs. Missing these deadlines can create cascading problems with licence renewals and tax filings.

Singapore Parent vs. UAE Subsidiary

These deadlines are the UAE subsidiary's responsibility alone — not the Singapore parent's. The audit obligation applies at the subsidiary level, meaning your UAE entity must be audited independently, separate from any group audit conducted in Singapore.

One practical advantage: Singapore's SFRS(I) framework has been identical to IFRS since 1 January 2018, so there are no standards-conversion issues when consolidating UAE financials into Singapore group accounts. However, the UAE audit itself must be conducted by a UAE-licensed professional — your Singapore auditor cannot sign off on it.

How the Mainland UAE Audit Process Works

The audit cycle runs from the close of the financial year through auditor appointment, document preparation, fieldwork, report issuance, and submission to relevant authorities.

Step 1: Appoint a UAE-Licensed Auditor

Critical requirement: The auditor must be registered with and licensed by the UAE Ministry of Economy under Federal Law No. 12 of 2014.

Article 3 states: "No natural person or legal entity may practice the profession in the State unless his name is registered in a record of practicing auditors at the Ministry."

Singapore-based CA firms or international Big 4 entities registered only in Singapore cannot legally sign UAE statutory audit reports. Your firm must either establish a UAE branch with a locally licensed representative or engage a separate UAE-registered audit firm.

Step 2: Prepare Financial Documentation

Your auditor will require a comprehensive document package. Use this checklist:

- Audited trial balance

- General ledger (all accounts)

- Bank reconciliation statements

- Accounts payable and receivable schedules

- Fixed asset register with depreciation schedules

- Payroll records and employment contracts

- VAT return filings (if registered)

- Sales and purchase contracts

- Board and shareholder resolutions

- Previous year's audit report (if applicable)

Step 3: Fieldwork and Testing

The auditor reviews financial documents, tests a sample of transactions, assesses internal controls, and verifies that financial statements are prepared in accordance with IFRS.

Fieldwork may be conducted on-site at your UAE premises or remotely, depending on the auditor's methodology. Cooperation from your local management team is essential. Delayed responses to auditor queries can push back your submission deadline and create compliance risk.

Step 4: Audit Report Issuance

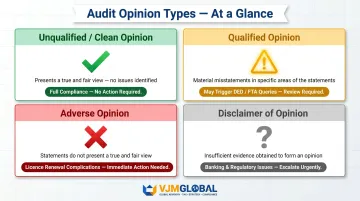

The auditor issues a formal opinion in one of four forms:

| Opinion Type | Meaning | Impact |

|---|---|---|

| Unqualified (Clean) | Statements present a true and fair view | No compliance issues |

| Qualified | Material misstatements in specific areas | May trigger DED/FTA questions |

| Adverse | Statements do not present a fair view | Licence renewal complications likely |

| Disclaimer | Auditor could not obtain sufficient evidence | Banking and regulatory issues |

For Singapore firms managing group reporting timelines, an unqualified opinion is particularly important — qualified or adverse opinions can delay parent-company consolidation and trigger queries from your Singapore auditors as well.

Step 5: Submission and Use of Audited Statements

Audited financial statements must be submitted to:

- DED for trade licence renewal (general Commercial Companies Law compliance)

- Federal Tax Authority for corporate tax returns (if revenue > AED 50 million)

- UAE banks for credit facilities or account maintenance

- Immigration authorities (sometimes required for visa processing)

Singapore parent companies will typically need UAE audited statements in IFRS format to support group consolidation under SFRS(I), so confirm formatting requirements with your Singapore auditors before fieldwork begins.

Key Requirements Singapore Firms Must Meet

Auditor Qualification and Appointment

The appointed auditor must hold a valid licence from the UAE Ministry of Economy. Singapore-qualified Chartered Accountants (CA Singapore) or international Big 4 affiliates operating only in Singapore cannot sign off on UAE statutory audit reports.

Before engaging a firm, verify their UAE licensing status through the Ministry of Economy's professional license register.

Accounting Standards: IFRS in the UAE vs. SFRS in Singapore

UAE mainland companies must prepare financial statements in accordance with IFRS. Singapore uses SFRS, which is substantially converged with IFRS but not identical — unless you've adopted SFRS(I).

Good news for Singapore firms: If your Singapore parent company uses SFRS(I) (mandatory for SGX-listed companies from 1 January 2018), your framework is identical to IFRS. This eliminates standards conversion burden when consolidating UAE subsidiary financials.

Companies still using the older SFRS framework should note it is "substantially aligned" but may contain minor differences in transition provisions and effective dates. A UAE-licensed accountant should review financials before audit to identify any gaps.

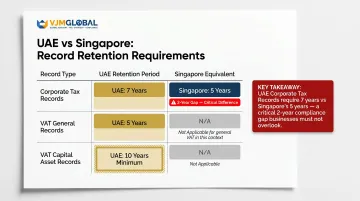

Record Retention Obligations

UAE law imposes layered retention requirements:

| Record Type | Retention Period |

|---|---|

| Corporate tax records | 7 years from end of tax period |

| VAT general records | 5 years from end of tax period |

| VAT capital asset records | 10 years minimum |

Critical difference: Singapore's general requirement is 5 years; UAE's is 7 years for corporate tax. Establish a compliant document retention policy for your UAE entity from the outset.

Electronic storage is permitted under Article 5(5) of the Tax Procedures Law, subject to FTA accessibility and integrity requirements. Cloud-based systems are acceptable if they maintain data integrity, prevent unauthorized alteration, and provide audit trails.

Cross-Border Coordination for Singapore Parent Companies

Singapore firms operating a UAE mainland subsidiary need to coordinate two separate compliance cycles:

- UAE entity's statutory audit (mandatory annually, no exemption)

- Singapore parent's own audit obligations (may be exempt if qualifying as a small company)

Synchronising these obligations requires careful planning. A cross-border advisory firm with experience across both jurisdictions can help align reporting timelines, manage consolidation requirements, and ensure your UAE subsidiary is audit-ready well before year-end.

Common Mistakes Singapore Firms Make (and the Penalties)

Mistake 1: Assuming Audit Exemption Applies

Singapore's Companies Act lets small companies skip the audit if they meet two of three size criteria. Many founders assume their UAE LLC qualifies for the same exemption — it doesn't.

No equivalent exemption exists for UAE mainland companies under Article 27 of Federal Law No. 32 of 2021. Delaying auditor appointment puts you out of compliance immediately, with no grace period.

Mistake 2: Engaging an Unlicensed Auditor

Any of the following auditors will produce a legally invalid report in the UAE:

- A Singapore CA firm without UAE licensure

- A Big 4 entity operating regionally but not registered with the UAE Ministry of Economy

- An accountant qualified under international standards but not UAE-licensed

DED, FTA, and UAE banks will all reject the report. You'll need to repeat the entire audit with a licensed auditor — doubling costs and likely missing submission deadlines in the process.

Penalties and Consequences

Both mistakes above expose your company to penalties across multiple authorities. Here's what non-compliance actually costs:

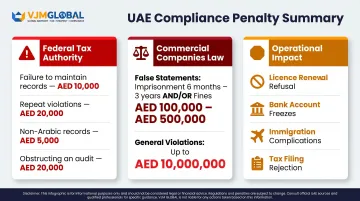

Federal Tax Authority (Corporate Tax):

- Failure to keep required records: AED 10,000 per violation

- Repeat violations within 24 months: AED 20,000

- Failure to submit records in Arabic when requested: AED 5,000

- Failure to facilitate tax audit: AED 20,000

Commercial Companies Law:

- False statements in financial reports: Imprisonment 6 months to 3 years and/or fine AED 100,000 to AED 500,000 (Article 349)

- General administrative violations: Fine AED 100 to AED 10,000,000 (Article 362)

Operational consequences:

- Trade licence renewal refusal or delays

- Bank account freezes or credit facility denials

- Immigration authority complications

- Corporate tax filing rejection

Singapore firms managing UAE subsidiaries remotely often miss deadlines because they're not tracking DED and FTA calendars from their home office. Set up automated compliance tracking from day one.

Frequently Asked Questions

What is an audit in mainland UAE?

A mainland UAE audit is an annual independent examination of a company's financial statements by a UAE-licensed external auditor, conducted to verify accuracy and compliance with Federal Law No. 32 of 2021 and IFRS standards. It produces a legally binding auditor's report required for licence renewals and tax filings.

Which mainland UAE companies are required to have an audit?

All companies registered in the UAE mainland — including LLCs and PJSCs — are legally required to have an annual external audit under Article 27 of Federal Law No. 32 of 2021. There is no exemption based on company size, revenue, or number of shareholders.

What financial thresholds require an audit in the UAE?

All mainland companies require an audit under Commercial Companies Law. Those with revenue exceeding AED 50 million face an additional requirement to maintain audited financial statements for corporate tax purposes under Ministerial Decision No. 84 of 2025 — but the baseline audit obligation applies regardless of revenue.

Is an audit report required for corporate tax in the UAE?

Yes. Companies with revenue above AED 50 million must maintain audited financial statements for corporate tax filings under Ministerial Decision No. 84 of 2025. Qualifying Free Zone Persons seeking the 0% tax rate face this requirement regardless of revenue level.

What qualifications are required to perform an audit in the UAE?

Auditors must be licensed by the UAE Ministry of Economy under Federal Law No. 12 of 2014. International qualifications — including CA Singapore, ACCA, or CPA — are not sufficient on their own; the auditor must also hold a valid UAE practising licence and appear in the Ministry's register of practising auditors.

What is Article 27 of the UAE Companies Law?

Article 27(1) of Federal Law No. 32 of 2021 mandates that every mainland UAE company (LLC or PJSC) appoint one or more licensed auditors approved by the shareholders to audit the company's financial accounts annually. This is the primary legal basis for the universal audit obligation.

Need help navigating UAE audit requirements and cross-border compliance? VJM Global advises Singapore-registered businesses on cross-border compliance, IFRS-aligned financial statement preparation, and multi-jurisdictional reporting obligations. Contact us at info@vjmglobal.com or call +91 98915 76441 to discuss your specific requirements.