Introduction

Singapore businesses expanding into the UAE — whether through mainland companies, free zone entities, or branch offices — face audit and compliance obligations that differ significantly from what they're used to back home. While 67% of Singapore SMEs qualify for audit exemptions under the Companies Act, the UAE takes a fundamentally different approach.

Here, mandatory audit requirements are driven by entity type, licensing authority, and regulatory environment — not company size alone.

Many Singapore business owners assume their existing audit practices will transfer seamlessly to the UAE. They don't. With Singapore-UAE bilateral trade reaching S$27.94 billion in 2025 — and the UAE ranked as Singapore's largest trading partner in MENA — getting these obligations right from day one matters.

This article covers when audits are mandatory, how mainland and free zone obligations differ, what the UAE's Corporate Tax rules require, and how Singapore accounting standards compare to UAE expectations.

Key Takeaways

- Mainland UAE companies must undergo annual external audit under Commercial Companies Federal Law No. 32 of 2021 — no exemptions

- Free zone rules differ: DMCC, JAFZA, and DAFZA mandate annual audits, while ADGM and DIFC offer limited exemptions

- UAE Corporate Tax requires audited financials for revenue above AED 50 million and all Qualifying Free Zone Persons

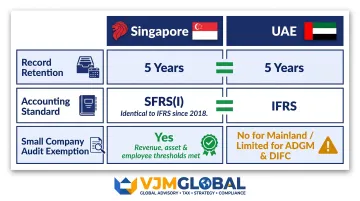

- Singapore SFRS(I) and UAE IFRS have been identical since 2018, meaning no accounting conversion is required

- Non-compliance triggers license renewal delays, penalties, and up to five years' loss of the 0% Corporate Tax rate

Why UAE Audit Requirements Are a Priority for Singapore Businesses

The UAE has become the top destination for Singapore businesses expanding into the Middle East. Singapore-UAE bilateral trade in goods reached S$27.94 billion in 2025, with the UAE ranking as Singapore's largest trading partner in MENA. That scale of commercial activity means UAE compliance frameworks — including audit obligations — directly affect a growing number of Singapore companies.

The Audit Exemption Gap

Here's the critical difference: Singapore's Companies Act provides audit exemptions for "small companies" meeting size thresholds:

- Annual revenue below SGD 10 million

- Total assets below SGD 10 million

- Fewer than 50 employees

Many Singapore SMEs have never undergone a statutory audit. The UAE offers no comparable broad exemption for mainland entities, and free zone exemptions depend entirely on which authority governs your license.

Double Taxation Agreement Considerations

The Singapore-UAE Double Taxation Agreement (DTAA), in force since September 2019, provides reduced withholding tax rates on dividends and interest. While the treaty text doesn't explicitly mandate audited financials, audited financials are practically necessary to substantiate tax residency claims, income characterization, and treaty benefit eligibility.

Understanding where Singapore exemptions end and UAE obligations begin is the first step for any business managing entities across both jurisdictions.

Is Audit Mandatory in the UAE? Understanding the Legal Framework

What an Audit Means Under UAE Law

A UAE audit is an independent examination of a company's financial statements by a licensed external auditor, producing an audit report that verifies the accuracy of reported revenues, expenses, assets, and liabilities. Unlike an internal review, it carries legal consequences for non-compliance.

The Legal Foundation

Federal Decree-Law No. 32 of 2021, Articles 26-27, establishes the mandatory audit framework:

- Article 26 requires companies to maintain accounting records that give a clear picture of financial position

- Article 27 mandates every Joint Stock Company and Limited Liability Company to appoint one or more auditors for annual account audits

- Record retention: Five-year minimum — matching Singapore's requirement

There is no revenue or size exemption for mainland LLCs or JSCs. If you're incorporated as a mainland entity, you're subject to annual audit regardless of turnover.

Statutory vs. Internal Audits

- Statutory (external) audit: Legally mandated, conducted by independent UAE-licensed auditors, reviews financial statements for regulatory compliance

- Internal audit: Voluntary management tool focused on operational efficiency and internal controls (does not replace external audit obligations)

Who Qualifies as an Auditor in the UAE

Under Ministerial Resolution 111-2 of 2022, auditors must meet one of two qualification paths:

- Pass three mandatory exams: IFRS, International Standards on Auditing (ISAs), and UAE Tax & Regulation (70 questions each, 60% pass mark)

- Hold a recognized qualification — ACCA, ICAEW, AICPA, CPA Australia, CPA Canada, or SOCPA — and pass only the UAE Tax & Regulation exam

- Obtain UAE Fellowship certificate through the ACCA, Ministry of Economy, and Emirates Association for Accountants and Auditors partnership

- Maintain 30 hours CPE/CPD annually

Singapore-qualified ACCA and ICAEW members qualify under the second path, meaning they need to pass only one exam to practice as UAE auditors.

The "It Depends" Reality

Audit obligations in the UAE are not one-size-fits-all. They vary by:

- Legal form (mainland LLC vs. free zone entity)

- Licensing authority (each free zone sets its own rules)

- Sector regulation (financial services face stricter requirements)

- Triggering events — including bank financing, government tenders, and visa applications

Singapore businesses should verify their specific obligations based on entity type and jurisdiction, rather than assuming they match a peer company's setup.

UAE Audit Requirements by Business Structure: Mainland vs. Free Zone

Mainland Entities

Companies registered under the UAE Commercial Companies framework face annual audit requirements with no exceptions. Shareholders expect audited financial statements, and licensing authorities require them for license renewal — this applies whether you've incorporated a mainland LLC or registered a branch in the UAE.

Free Zone Entities — The Variable Landscape

Audit requirements are governed by the specific free zone authority and license conditions. Here's the breakdown:

Always Require Annual Audit:

- DMCC: Submit audited accounts within 180 days of financial year-end (5 days post-AGM to portal)

- JAFZA: 90-day submission deadline from financial year-end

- DAFZA: 90-day submission deadline from financial year-end

- RAKEZ: 6-month submission deadline

Offer Small Entity Exemptions:

- ADGM: Exemption available if turnover up to USD 13.5 million AND up to 35 employees; 9-month filing deadline for private companies

- DIFC: Exemption available if fewer than 20 shareholders AND turnover below USD 5 million; 7-month filing deadline

Since Singapore entrepreneurs typically choose free zones for tax benefits and 100% ownership, verify your specific free zone's audit obligations at incorporation — not after. Assuming no requirement exists is one of the most common compliance gaps.

Regulated Sectors

Beyond structure-based rules, the sector you operate in adds another layer. Financial services firms face additional audit obligations — defined timelines, approved auditor criteria, and regulatory reporting standards set by the relevant UAE authority. Singapore fintech companies in particular should confirm these requirements before selecting their UAE entity type, as the choice of structure can affect which regulator governs your audit.

Event-Driven Audit Triggers

Even where no standing audit obligation exists, audited financials may be required for:

- Banking facility applications

- Investor due diligence

- Government tender participation

- Immigration purposes (visa applications)

- Upon request by competent authorities

Recommendation: Maintain audit-ready records at all times, regardless of your entity's standing audit obligation.

Corporate Tax and Audit Compliance in the UAE

The Corporate Tax Framework

Federal Decree-Law No. 47 of 2022, effective for financial years starting on or after June 2023, introduced UAE Corporate Tax at a 9% rate on taxable income exceeding AED 375,000. Corporate Tax doesn't automatically require every business to undergo statutory external audit — but it introduces specific circumstances where audited financial statements become mandatory.

Who Must Maintain Audited Financial Statements

Ministerial Decision No. 82 of 2023, updated by MD 84 of 2025, mandates audited financial statements for:

- Any Taxable Person with revenue exceeding AED 50 million during the relevant tax period

- All Qualifying Free Zone Persons (QFZPs) — regardless of revenue

The QFZP Compliance Risk

This is the most overlooked obligation for Singapore-owned free zone companies. To qualify for the 0% preferential Corporate Tax rate on qualifying income, a Qualifying Free Zone Person must:

- Be registered in a free zone

- Maintain adequate substance in the UAE

- Derive qualifying income

- Ensure non-qualifying revenue doesn't exceed 5% of total revenue or AED 5 million (whichever is lower)

- Comply with transfer pricing rules

- Prepare audited IFRS financial statements

Penalty for non-compliance: Loss of QFZP status, subject to 9% Corporate Tax on entire income for the current year, and disqualification from the 0% rate for the next four years (total five-year penalty period). For a free zone company generating AED 10 million in annual income, losing QFZP status could mean AED 900,000 in additional tax — every year for five years.

Broader Tax Compliance Benefits

Beyond the QFZP obligation, audited financial statements reduce the risk of disputes in Corporate Tax filings — tax returns are only as reliable as the underlying financials. Weak record-keeping creates direct exposure to Federal Tax Authority inquiries and penalties that are entirely avoidable.

VJM Global's chartered accountants help Singapore-owned UAE businesses maintain audit-ready records year-round, ensuring accurate Corporate Tax filings and protecting QFZP eligibility.

How Singapore Audit Standards Compare to UAE Requirements

The IFRS Alignment Advantage

Singapore's SFRS(I) standards are "identical to IFRS" since 1 January 2018. The UAE mandates IFRS for financial reporting. This means Singapore businesses using SFRS(I) can make an explicit statement of compliance with IFRS, satisfying UAE requirements without restating financials.

In practice, this eliminates any accounting standards transition — no conversion burden, no dual reporting frameworks to manage.

The Audit Exemption Framework Difference

Singapore: A private company qualifies for audit exemption if it meets two of three criteria for the immediate past two consecutive financial years:

- Annual revenue ≤ SGD 10 million

- Total assets ≤ SGD 10 million

- Number of employees ≤ 50

The UAE takes a significantly stricter approach.

UAE: No comparable broadly available small company exemption exists for mainland entities. Audits are effectively mandatory for most operational mainland businesses. ADGM and DIFC offer limited exemptions, but Corporate Tax requirements may override them.

Where both jurisdictions do align is on record-keeping obligations.

Record Retention Parity

Both Singapore (IRAS) and UAE (Commercial Companies Law, Article 26) mandate a minimum five-year record retention period. Singapore businesses can apply familiar documentation habits, but must ensure records are structured and accessible for UAE-licensed auditors operating under ISA standards.

| Requirement | Singapore | UAE |

|---|---|---|

| Retention period | 5 years | 5 years |

| Accounting standard | SFRS(I) (identical to IFRS) | IFRS |

| Small company exemption | Yes (revenue/asset/employee thresholds) | No (mainland); limited (ADGM/DIFC) |

Key Documents and Practical Steps for Audit Readiness

Core Documents for UAE Statutory Audit

- Draft trial balance and general ledger

- Bank statements and reconciliations

- Fixed asset register with depreciation calculations

- Contracts and agreements (customers, suppliers, leases, loans)

- Payroll records and employee documentation

- Revenue and receivables support (invoices, ageing reports)

- Payables support and supplier documentation

- VAT and Corporate Tax filings

Year-Round Preparation Habits

- Reconcile accounts monthly — don't leave it until year-end

- Categorise and file expense documentation in real-time

- Document inter-company transfers and related-party transactions as they occur

- Align record-keeping with your free zone licensing authority's requirements

- Confirm that accounting policies reflect current IFRS standards

Cross-Border Compliance Support

Keeping these habits consistent across two regulatory environments — Singapore and UAE — adds a layer of complexity that catches many businesses off guard. Working with advisors who understand both frameworks reduces that risk considerably.

VJM Global's chartered accountants help Singapore businesses structure their accounts and compliance processes for multi-jurisdiction requirements. The team handles audit checklists, responds to auditor queries, and ensures documents reach the right parties on time.

Frequently Asked Questions

Is audit mandatory in the UAE?

Yes, audit is mandatory for all mainland companies under Commercial Companies Federal Law No. 32 of 2021. Free zone requirements vary by authority — DMCC, JAFZA, DAFZA, and RAKEZ mandate annual audits; ADGM and DIFC offer limited exemptions. Corporate Tax rules require audited financials for Qualifying Free Zone Persons and businesses with revenue above AED 50 million.

What is audit in UAE?

A UAE audit is an independent examination of financial statements conducted by a licensed external auditor, producing a report that verifies accuracy and gives stakeholders confidence in the company's reported financial position. Unlike an internal management review, it is a formal statutory requirement under UAE law.

What is the qualification for audit in UAE?

Under Ministerial Resolution 111-2 of 2022, auditors must hold qualifying professional certifications (ACCA, ICAEW, or CPA Australia). They must also pass UAE-specific exams in IFRS, International Standards on Auditing, and UAE tax and regulation through the UAE Fellowship Programme. Singapore-qualified ACCA/ICAEW members need only pass the Tax and Regulation exam.

How much is audit fee in UAE?

Audit fees vary based on company size, entity type, transaction volume, and jurisdiction. Small free zone companies typically pay less than larger mainland entities, with first-year engagements often costing more due to setup work. Request quotes from UAE-licensed audit firms for accurate estimates.

Does the UAE use IFRS or GAAP?

The UAE mandates IFRS (International Financial Reporting Standards) for financial reporting. This is an advantage for Singapore businesses since Singapore's SFRS(I) is closely aligned with IFRS since 2018, reducing accounting transition complexity.

Do Singapore businesses in UAE free zones still need an audit?

It depends on the specific free zone's regulations. DMCC, JAFZA, DAFZA, and RAKEZ require annual audited financial statements for license renewal. Even if your free zone offers an exemption, Singapore businesses structured as Qualifying Free Zone Persons for Corporate Tax purposes must maintain audited financial statements to retain the 0% preferential tax rate.