Introduction

Many Singapore businesses expanding into UK markets struggle with a deceptively simple compliance requirement: choosing the correct VAT code. These short identifiers determine how each transaction is taxed, reported to HMRC, and whether the business can reclaim input VAT. Choosing the wrong code creates real consequences: denied VAT reclaims, HMRC penalties that can reach 100% of tax due in severe cases, and costly corrections.

Singapore's GST framework differs significantly from the UK's VAT system, and applying Singapore GST logic directly to UK transactions can be costly. A transaction that is GST-exempt in Singapore might be zero-rated in the UK — a distinction that determines whether you can reclaim thousands of pounds in input VAT.

This guide covers:

- What each UK VAT code means and when it applies

- Which codes govern Singapore-UK cross-border trade

- What Singapore businesses must do to stay compliant with HMRC

Key Takeaways

- UK VAT codes classify transactions as standard rate (20%), zero rate (0%), reduced rate (5%), exempt, or outside scope — each maps to specific VAT return boxes

- Singapore businesses are Non-Established Taxable Persons (NETPs) and must register from the first taxable UK supply, with no £90,000 threshold

- Reverse charge codes transfer VAT accounting responsibility to you as the buyer in specific B2B transactions

- Misapplying codes (treating zero-rated as exempt, or confusing outside scope with zero-rated) triggers HMRC penalties and incorrect VAT reclaims

What Are UK VAT Codes?

UK VAT codes are two-to-five character identifiers used in accounting software (Xero, QuickBooks, Sage) and on VAT returns to indicate the VAT treatment of each transaction. They are distinct from your UK VAT registration number — that nine-digit identifier proves you're registered, while VAT codes classify individual transactions.

The key difference from Singapore GST: in the UK, VAT codes determine not just the rate but which boxes on the HMRC VAT return (Boxes 1–9) each transaction flows into. A zero-rated sale goes into Box 6 (total sales) but generates no Box 1 (output tax) entry. An exempt sale doesn't appear on your return at all.

Get the code wrong, and your entire VAT return is incorrect.

That distinction also explains why codes and rates are not the same thing:

VAT codes vs. VAT rates: Rates (20%, 5%, 0%) describe the tax percentage. Codes describe the full treatment — including whether the transaction is reported, how it's reported, and under which scheme. The same 0% rate applies to both zero-rated and some outside-scope transactions, but they use different codes and carry completely different compliance implications.

How VAT Codes Map to VAT Return Boxes

Understanding how codes flow into the VAT100 form is essential:

| Box | Description | What Gets Reported |

|---|---|---|

| Box 1 | VAT due on sales | Output VAT from standard, reduced, and reverse charge sales |

| Box 4 | VAT reclaimed on purchases | Input VAT on business purchases, imports, and reverse charge |

| Box 6 | Total sales excluding VAT | All outputs including zero-rated and exports (but not exempt) |

| Box 7 | Total purchases excluding VAT | All inputs including zero-rated and reverse charge values |

Source: HMRC VAT Notice 700/12

Accounting Software VAT Code Labels

VAT codes are platform-specific, not HMRC-standardised. Each software uses its own labels:

| Treatment | Sage | QuickBooks | Xero |

|---|---|---|---|

| Standard 20% | T1 | S (20.0%) | 20% (Standard) |

| Zero-rated 0% | T0 | Z (0.0%) | Zero Rated |

| Reduced 5% | T5 | R (5.0%) | 5% (Reduced) |

| Exempt | T2 | Exempt | Exempt |

| Outside scope | T9 | No VAT | No VAT |

| Reverse charge | T20 | RC SG (20%) | Reverse Charge Expenses (20%) |

All three platforms produce identical output for HMRC's VAT return boxes despite different labelling.

The Main UK VAT Codes Singapore Businesses Need to Know

Here's a quick reference across all six codes before the full breakdown:

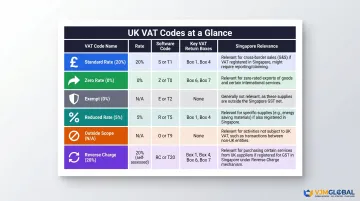

| VAT Code | Rate | Code | Key VAT Return Boxes | Singapore Relevance |

|---|---|---|---|---|

| Standard Rate | 20% | S / T1 | Box 1 (output), Box 6 (net) | Sales to UK customers |

| Zero Rate | 0% | Z / T0 | Box 6 (net only) | UK exports to Singapore |

| Exempt | 0% | E / T2 | Not reported | Financial/insurance services |

| Reduced Rate | 5% | R / T5 | Box 1 (output), Box 6 (net) | Specific goods only |

| Outside Scope | N/A | T9 | Not reported | Non-business transactions |

| Reverse Charge | 20% | RC SG / T20 | Boxes 1, 4, 6, 7 | B2B services from UK suppliers |

Standard Rate (20% — Code S or T1)

This is the default code for most goods and services sold in the UK. Output VAT goes to Box 1 and net sale to Box 6 on the VAT return. Singapore businesses selling standard-rated goods or services in the UK must apply this code and remit the VAT to HMRC.

Common use cases:

- Physical products sold to UK customers

- Consulting services delivered in the UK

- Software licences to UK businesses (note: B2B digital services may fall under reverse charge — covered below)

- Hospitality services

Zero Rate (0% — Code Z or T0)

Zero-rated transactions are still VAT-taxable and must be reported (net sale to Box 6), but no VAT is charged. This is not the same as exempt — zero-rated supplies allow you to reclaim input VAT on related costs.

Common examples:

- Most food for human consumption (excluding catering, confectionery, alcohol)

- Children's clothing and footwear

- Books, newspapers, magazines

- UK exports to countries outside the UK including Singapore

Source: HMRC VAT Rates Guidance

Critical for Singapore businesses: UK companies exporting goods to Singapore zero-rate those sales, provided they retain proof of export. You should expect zero-rated invoices, not 20% VAT.

Exempt (Code E or T2)

Exempt supplies are not reported on a VAT return at all and no VAT is charged or reclaimed. Businesses that only make exempt supplies cannot register for VAT and cannot reclaim input VAT.

Key categories:

- Insurance and financial services

- Certain education and vocational training

- Medical treatment by registered professionals

- Selling, leasing, or letting commercial property (subject to "option to tax")

Source: HMRC Exemption Guidance

Worth noting: Both exempt and zero-rated result in no VAT charged to customers — but they behave very differently behind the scenes. Zero-rated supplies are taxable, so you reclaim input VAT on related costs. Exempt supplies are not, so that input VAT becomes an unrecoverable cost. Getting this wrong can mean losing thousands in legitimate VAT recovery.

Reduced Rate (5% — Code R or T5)

Specific goods and services qualify for the 5% rate:

- Domestic energy (gas, electricity)

- Children's car seats

- Smoking cessation products

- Certain mobility aids

Singapore businesses importing or distributing these product types in the UK should confirm whether the reduced rate applies before setting prices.

Outside the Scope (Code T9 or No VAT)

Transactions outside the scope of VAT are not reported on a VAT return at all. These include:

- Non-business transactions (gifts, personal expenses)

- Statutory fees and charges

- Wages and dividends

- Supplies made before VAT registration

Outside-scope is not the same as zero-rated: zero-rated transactions sit within the VAT system at 0%, while outside-scope transactions fall entirely outside it and carry no VAT reporting obligation whatsoever.

Reverse Charge (Code RC SG or T20)

The reverse charge mechanism shifts VAT accounting from the supplier to the recipient. When a Singapore business receives services from a UK supplier, the Singapore business (if UK VAT-registered) must self-account using reverse charge codes.

How it works:

- Calculate VAT on the service value (usually 20%)

- Report it as output VAT in Box 1

- Simultaneously claim it as input VAT in Box 4 (if you're fully taxable)

- Include the net value in both Box 6 (as deemed supplier) and Box 7 (as purchaser)

For fully taxable businesses, the net effect is nil: Box 1 and Box 4 cancel out. Partially exempt businesses face a different outcome — they may not recover all the input VAT, which becomes a genuine cash cost rather than a paper entry.

Source: HMRC Place of Supply of Services Notice 741A

How UK VAT Codes Apply to Singapore–UK Trade

Exporting Goods from Singapore to the UK

When a Singapore business ships physical goods into the UK for sale, import VAT is triggered at UK customs clearance. If you're the importer of record, you may need UK VAT registration and will use relevant purchase codes to reclaim import VAT.

Incoterms matter:

- DDP (Delivered Duty Paid): The Singapore seller acts as importer of record, bears UK import VAT and duty obligations, and may trigger mandatory UK VAT registration

- DAP (Delivered At Place): The UK buyer is the importer of record and handles import VAT — the Singapore seller's UK VAT exposure is more limited

HMRC Customs Valuation Guidance

UK Businesses Selling to Singapore Buyers

UK-registered businesses exporting goods to Singapore customers typically zero-rate those sales (0% Z code) since Singapore is outside the UK. The UK exporter must maintain proof of export — official or commercial documentation confirming the goods left the UK.

HMRC VAT Notice 703

Singapore businesses receiving UK invoices should expect zero-rated treatment, not 20% VAT.

Selling Digital Services to UK Consumers from Singapore

Singapore businesses providing digital services (software, streaming, online content) to UK private consumers (B2C) must charge UK VAT at 20% and register with HMRC regardless of turnover. There is no registration threshold for overseas suppliers of digital services to UK consumers.

The reverse charge does not apply in B2C scenarios. You must charge, collect, and remit UK VAT directly.

HMRC Digital Services VAT Rules

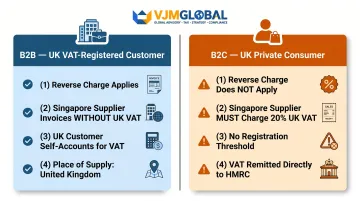

B2B Services from Singapore to UK Businesses

When a Singapore business provides services to a UK VAT-registered business, the place of supply is where the customer belongs — the UK. The reverse charge applies, meaning the UK customer self-accounts for VAT. The Singapore supplier issues an invoice without UK VAT.

This applies to most B2B services, even where the Singapore supplier holds a UK VAT number, provided they "belong" outside the UK.

The treatment differs sharply depending on the customer type:

- B2B (UK VAT-registered customer): Reverse charge applies — Singapore supplier invoices without UK VAT

- B2C (UK private consumer): Singapore supplier must charge and remit UK VAT at 20%

Holding Inventory in the UK (Amazon FBA, 3PL Warehouses)

A Singapore e-commerce business storing goods in a UK fulfilment centre is considered to be making UK domestic supplies and must register for VAT, apply standard VAT codes on UK sales, and file regular VAT returns.

HMRC confirms: "If you are an overseas seller who owns goods of any value that are located in the UK at the point of sale you must register and account for VAT on any sales you make directly to customers in Great Britain or Northern Ireland."

HMRC Overseas Goods Guidance

Singapore sellers using FBA or 3PL warehouses who overlook this rule face retrospective VAT assessments, interest, and penalties — registration is required before the first UK sale, not after.

Registering for UK VAT as a Singapore Business

NETP (Non-Established Taxable Person) Rule

Unlike UK-resident businesses which only register when taxable turnover exceeds £90,000, Singapore businesses operating as NETPs have no registration threshold — they must register from the very first taxable supply made in the UK.

A business is an NETP if it has no UK establishment. To qualify as a UK establishment, a business needs either:

- A place where essential management decisions are made, or

- A permanent physical presence with human and technical resources to make or receive taxable supplies

A registered, serviced, or virtual office alone does not meet this threshold.

Source: HMRC VAT Notice 700/1

Registration Process and Documentation

Overseas businesses register via the Government Gateway online portal. You'll need:

- Legal entity and business details including overseas address

- Details of expected UK sales activity and supply chains

- Storage/warehousing arrangements if goods are held in the UK

- Identity verification documents (passport copies or official ID for directors/owners)

- Official documentation confirming the business is registered in its home country

- Confirmation of MTD-compatible accounting software

Most UK VAT registrations are processed within 4–6 weeks, though overseas applications may take longer due to additional verification requirements.

VAT Number Format and Post-Registration Obligations

The UK VAT number format is "GB" followed by 9 digits (e.g., GB123456789). Branch traders may have 12 digits, and Northern Ireland uses the "XI" prefix for EU trading purposes.

Once registered, your ongoing obligations include:

- Filing quarterly VAT returns

- Issuing VAT-compliant invoices

- Maintaining digital records under Making Tax Digital (MTD) for VAT

- Paying VAT by the statutory deadline

HMRC confirms: "All VAT registered businesses should now be signed up for Making Tax Digital for VAT." This applies universally to all VAT-registered entities, including Singapore businesses.

Source: HMRC Making Tax Digital

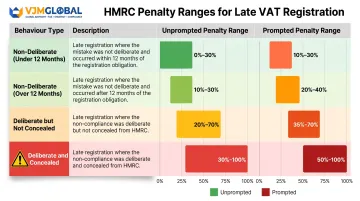

Penalties for Late or Missed Registration

The current penalty regime is governed by Schedule 41, Finance Act 2008. Penalties are calculated as a percentage of Potential Lost Revenue (PLR) — the VAT due from the date registration was required to the date of notification:

| Behaviour | Unprompted | Prompted |

|---|---|---|

| Non-deliberate (within 12 months) | 0% – 30% | 10% – 30% |

| Non-deliberate (over 12 months) | 10% – 30% | 20% – 30% |

| Deliberate but not concealed | 20% – 70% | 35% – 70% |

| Deliberate and concealed | 30% – 100% | 50% – 100% |

HMRC may reduce penalties to 0% where a reasonable excuse exists and the taxpayer notified HMRC promptly after the excuse ended. The exact percentage depends on the quality of disclosure.

Source: HMRC VATREG26050

⚠️ Note: Invoicing VAT before receiving a VAT number can attract a separate 100% penalty — so avoid charging VAT to customers until your registration is confirmed.

Common Mistakes Singapore Businesses Make with UK VAT Codes

Treating Zero-Rated and Exempt as the Same

Both result in no VAT being charged to the customer, but the reporting and reclaim implications are completely different:

Zero-rated supplies:

- Taxable at 0%

- Reported in Box 6

- Input VAT is reclaimable

Exempt supplies:

- Not taxable at all

- Not reported on VAT return

- Input VAT cannot be reclaimed

Misclassification directly affects what you can reclaim and how your return is prepared. If you treat a zero-rated supply as exempt, you understate Box 6 and may fail to reclaim legitimate input VAT.

Assuming the £90,000 Threshold Applies

The domestic VAT registration threshold only applies to UK-established businesses. Singapore businesses (as NETPs) must register immediately upon making any taxable supply in the UK — an error that triggers immediate registration liability for first-time exporters and e-commerce sellers.

Ignoring the Reverse Charge on Purchased Services

The reverse charge must be applied when a UK VAT-registered Singapore business purchases services from UK suppliers — marketing agencies, software providers, and consultants are common examples. Failing to do so creates underreported output VAT and Box 1 errors, exposing the business to HMRC penalties even when the net tax effect is nil.

Common reverse charge errors include:

- Not recording the reverse charge in Box 1 (output VAT) and Box 4 (input VAT)

- Treating purchased UK services as outside the scope of VAT entirely

- Omitting reverse charge transactions from the VAT return altogether

Frequently Asked Questions

What is a VAT code?

A VAT code is a short identifier used in accounting systems and VAT returns to classify the tax treatment of a transaction — such as standard-rated, zero-rated, exempt, or outside scope. Different codes determine which boxes on the HMRC VAT return the amounts flow into.

What are the VAT codes in the UK?

The main UK VAT codes are Standard Rate (20%), Zero Rate (0%), Reduced Rate (5%), Exempt, Outside the Scope, and Reverse Charge. Accounting software may label these differently (for example, T1, T0, T5 in Sage; S, Z, R in QuickBooks) but the underlying classifications remain consistent.

What is the difference between T0 and T9 VAT codes?

T0 (zero rate) applies to taxable supplies at 0% that are still reported on a VAT return (included in Box 6). T9 (outside the scope) applies to transactions not subject to VAT at all and not included in the VAT return. This distinction is critical for accurate reporting.

How does a UK VAT number look?

A UK VAT number begins with the country prefix "GB" followed by 9 digits (for example, GB123456789). Branch traders may have 12 digits, and Northern Ireland uses the "XI" prefix for EU trading purposes.

How do I find a UK VAT number?

Use the HMRC VAT checker tool, which confirms whether a VAT number is valid and returns the registered business name and address. This is essential for Singapore businesses verifying UK supplier invoices.

Can a Singapore company have a UK VAT number?

Yes. A Singapore company can and in many cases must register for UK VAT. As a Non-Established Taxable Person, a Singapore business making taxable supplies in the UK must register from the first supply, regardless of turnover, and will receive a standard GB-prefixed VAT number.

Need support navigating international tax obligations? VJM Global has 30+ years of experience helping businesses across the UK, USA, Australia, and Asia manage cross-border accounting and tax compliance. For UK VAT registration and ongoing compliance, our team can help you identify the right obligations and connect you with the appropriate HMRC-qualified specialists — so your Singapore business stays fully compliant from day one. Contact us at info@vjmglobal.com to get started.