Flipping houses can be a lucrative investment strategy, but many U.S. investors overlook one crucial aspect: accounting. Without proper financial management, profits can evaporate, and tax liabilities can spiral out of control.

As a house flipper, understanding how to track expenses and report profits is essential for maximizing your return on investment.

This guide will cover everything you need to know about accounting for flipping houses, from managing expenses to implementing key accounting strategies. Let’s get started.

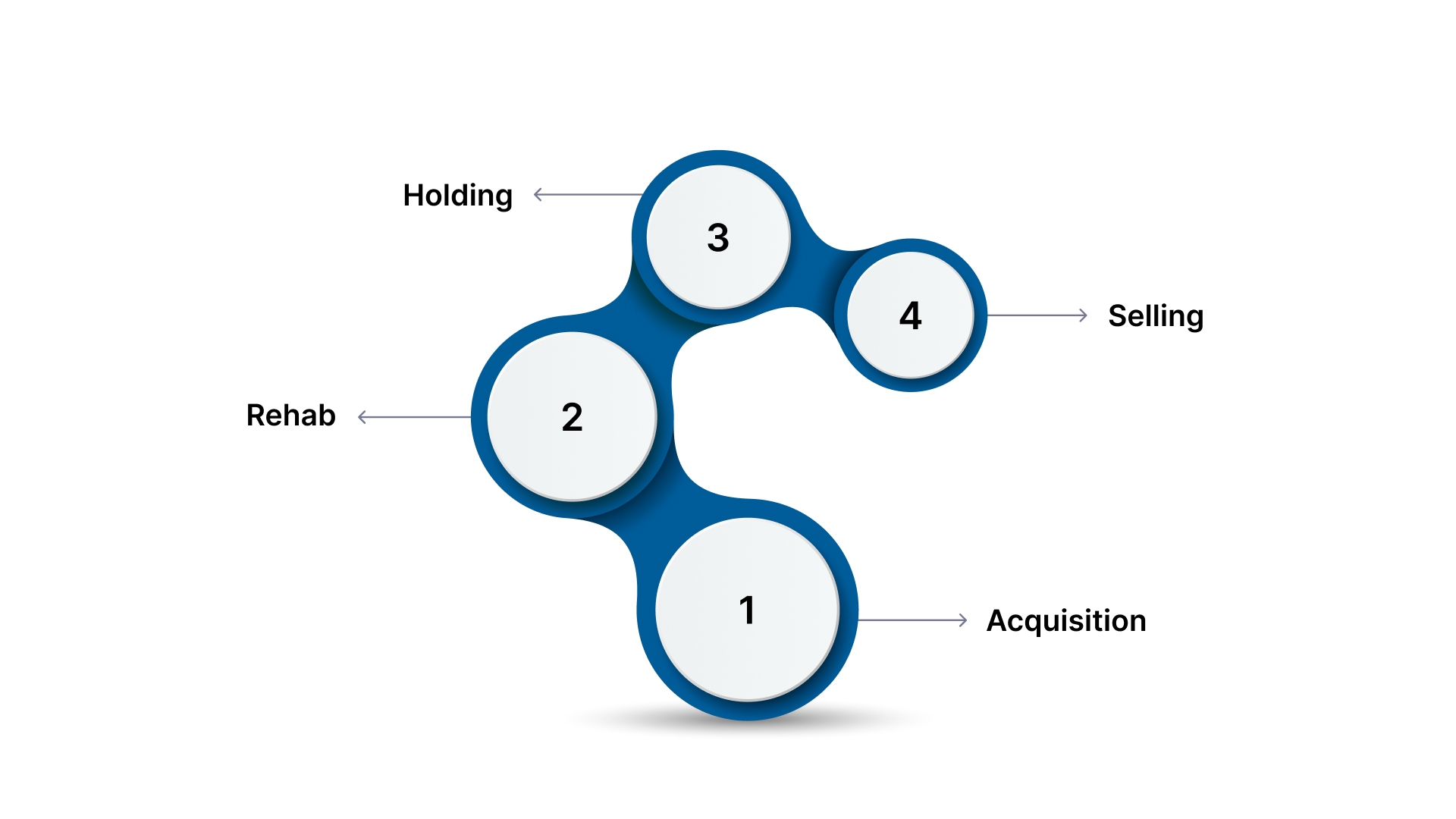

When flipping houses, it’s crucial to break down your investment into clear phases. Each phase has distinct costs and tax implications, so accurate tracking is essential.

The purchase price of the property is your starting point. This includes the home's price and any additional costs, such as closing fees, inspections, and agent commissions. These are direct costs that are factored into your total investment.

Rehab expenses include costs for renovating the property, such as labor, materials, permits, and design work. Keeping detailed records of these costs is essential, as they may be deductible and directly impact your taxable profits.

Holding costs include expenses you incur while waiting to sell, such as property taxes, insurance, utilities, and loan interest. These expenses can quickly add up, and proper categorization ensures they’re accounted for when calculating profit margins.

Selling costs cover agent commissions, advertising, and closing costs associated with the sale. These should be tracked and subtracted from your revenue to determine your final profit.

Accurately categorizing these costs is crucial for both accounting and taxes. From a tax perspective, improper categorization could lead to missed deductions or over‑reporting of taxable income. For example, rehab expenses may be deductible, reducing your taxable income, while holding costs impact the overall profitability of the flip.

Additionally, how long you hold onto the property before selling can affect whether your profits are taxed at short‑term or long‑term capital gains rates. Short‑term capital gains are taxed like regular income, which can be much higher, while long‑term gains may qualify for lower tax rates.

Properly categorizing these expenses and understanding their tax implications will ultimately help you maximize profits while minimizing taxes.

Now that you know how to categorize your costs, let’s explore why keeping track of these expenses is so important for your house flipping success.

Flipping houses without proper accounting can cause your profits to quickly slip away. Here’s why getting your finances right is essential:

Accounting practices minimize risks, support smarter decisions, and ultimately protect your profits throughout the entire house-flipping process.

VJM Global specializes in helping property flippers manage cash flow, track expenses, and handle tax planning. With our expert accounting services, you can stay on top of repairs, loans, and vendor payments while maximizing profits and minimizing tax risks. Get started today.

Also Read: Understanding Monthly Bookkeeping Costs and Services

With proper accounting in place, let’s look at some key accounting tips to ensure you stay on top of your finances throughout the flip.

Flipping houses can be incredibly profitable, but without strong accounting practices, it’s easy to miss out on potential savings. Here’s how you can stay on top of your finances throughout the entire flip:

Relying on "shoebox accounting" (throwing receipts and invoices into a box or folder) can lead to chaos when it's time to report expenses or file taxes. It's essential to have a system in place to track every receipt and categorize each expense.

This ensures you don’t miss deductions or create unnecessary stress when filing your taxes. Proper organization helps you stay in control of your budget and financials.

Your budget is the foundation of your entire project. Start by creating a comprehensive budget that includes buying costs, holding costs, selling costs, financing costs, and, of course, repair costs.

Once you have your budget, diligently track the actual expenses as they occur. Regularly compare the two to identify discrepancies early and adjust your approach to keep costs under control.

Start your budget early in the process during your due diligence phase. This involves planning for every cost involved in the flip. Break down your costs into four main categories: Buying Costs (title fees, appraisal), Holding Costs (insurance, utilities), Selling Costs (real estate commissions), and Financing Costs (loan fees, interest).

Then, get into the specifics of repairs by breaking them down into categories like exterior work, interior demolition, and systems like plumbing and electrical.

Once the project is underway, the most critical part is tracking every single expense. From large contractor invoices to small purchases, keeping a detailed record is crucial. Record each receipt as soon as you make a purchase.

For example, a Home Depot receipt might contain expenses for both plumbing and electrical supplies. If you lump them together, you won’t know exactly how much you spent on each category, making it harder to track your budget and compare actuals.

After the flip is complete, don’t forget to track your final sale price and calculate the net income from your flip. A clear, organized record helps with both profit tracking and tax filing. Properly categorizing your expenses and understanding deductible costs will ensure that your tax prep goes smoothly, helping you minimize taxable income.

For property flippers, understanding tax implications is critical, and having the right support is key. VJM Global offers specialized tax and accounting services tailored to the needs of house flippers. Our expert team helps you ensure proper expense classification and identifies valuable deductions to minimize your tax liability.

With our comprehensive services in bookkeeping, tax preparation, and financial reporting, you can focus on growing your business while we ensure your tax filings are accurate and compliant. Get started today.

Make sure you’re classifying your income and expenses correctly. For instance, repairs are typically deductible, while improvements need to be capitalized and added to the property’s basis. Also, distinguish between business and personal expenses by keeping separate bank accounts and credit cards for your flips.

Understand the tax implications of your financing choices, such as loan interest deductions, and keep thorough records. It’s essential to track all acquisition costs, renovations, utilities, insurance, and contractor fees, as many of these can be deducted. Being diligent with your record-keeping will ensure your tax filings are accurate and compliant.

Following these tips ensures your property-flipping projects remain financially healthy.

Also Read: Top Benefits of Outsourcing Accounting Services to India for US Small Businesses

If you're ready to simplify your accounting and stay compliant, expert support from VJM Global can help you avoid costly mistakes and keep your finances on track.

VJM Global is here to simplify the accounting process for house flippers. Our expert team provides the following tailored services to keep your business on track:

Let VJM Global handle your accounting so you can focus on turning properties into profits.

Flipping houses goes beyond finding the right property and handling renovations; it involves mastering the financial management that drives success. Without the right accounting practices, you risk running over budget, missing key tax deductions, or paying more than necessary come tax season.

House flipping requires careful planning, especially when it comes to managing finances. VJM Global provides expert accounting and tax services tailored specifically for U.S. property flippers, from creating detailed budgets to ensuring compliance.

Don’t let financial mismanagement derail your profits; let us guide you through every step. Reach out today and take control of your house flipping finances with confidence.

The key expenses to track include acquisition costs (purchase price, closing fees), rehab costs (materials, labor), holding costs (insurance, utilities), and selling costs (commissions, advertising).

Ensure that repairs are classified as deductible expenses, while improvements should be capitalized and added to the property’s basis. Using separate accounts for business and personal expenses helps.

Accounting software can help you track expenses, categorize transactions, generate financial reports, and keep an eye on your budget. It can also make tax filing easier by organizing your records.

You can claim deductions for costs like repairs, utilities, insurance, and loan interest. Keep detailed records of all expenses to ensure you maximize your deductions and minimize your tax liability.

VJM Global offers expert tax planning, bookkeeping, expense tracking, and financial reporting services tailored to house flippers. We help you stay compliant, maximize your profits, and minimize tax liabilities.