Expanding a US business into India involves far more than hiring teams and setting up local operations. One area that demands close attention from the start is payroll, especially when payroll liabilities must be calculated, recorded, and cleared across two statutory systems.

For firms moving employees, contractors, or finance processes from the US to India, payroll operations include cross-border withholding rules, country-specific employer charges, and strict deposit cycles that directly affect payroll liabilities every month. These requirements apply whether you are building a local team, shifting back-office work, or establishing a long-term presence in India.

This blog gives US companies a clear view of how payroll liabilities work during a US to India transition, with practical steps, compliance details, and record-keeping methods required to keep payroll accurate throughout expansion.

Key Takeaways

US payroll uses IRS, state, and local rules, while India uses Section 192 and TDS, creating separate liability calculations for each employee.

IRS, state, TDS, PF, and ESIC must have distinct ledger accounts to prevent merged balances on the payroll liabilities balance sheet.

A payroll liability clears only when matched with the exact receipt, EFTPS ID, state confirmation, OLTAS challan, PF ECR, or ESIC challan.

Employee-level deduction codes such as FIT, SIT, FICA, TDS, PF, and ESIC must match ledger entries to avoid misclassification.

Returned payments, reversals, and incorrect postings must be reviewed weekly so unresolved items do not inflate payroll liability totals.

What Are Payroll Liabilities?

Payroll liabilities are short-term amounts a company owes after running payroll but before clearing statutory deductions, benefit commitments, and employer-side contributions.

In the US-to-India expansion, these liabilities include federal and state withholdings, Indian social security-linked deductions, and unpaid employer charges tied to dual-country hiring. Each item remains on the payroll liabilities balance sheet until settled with the respective authority or vendor.

Why This Matters

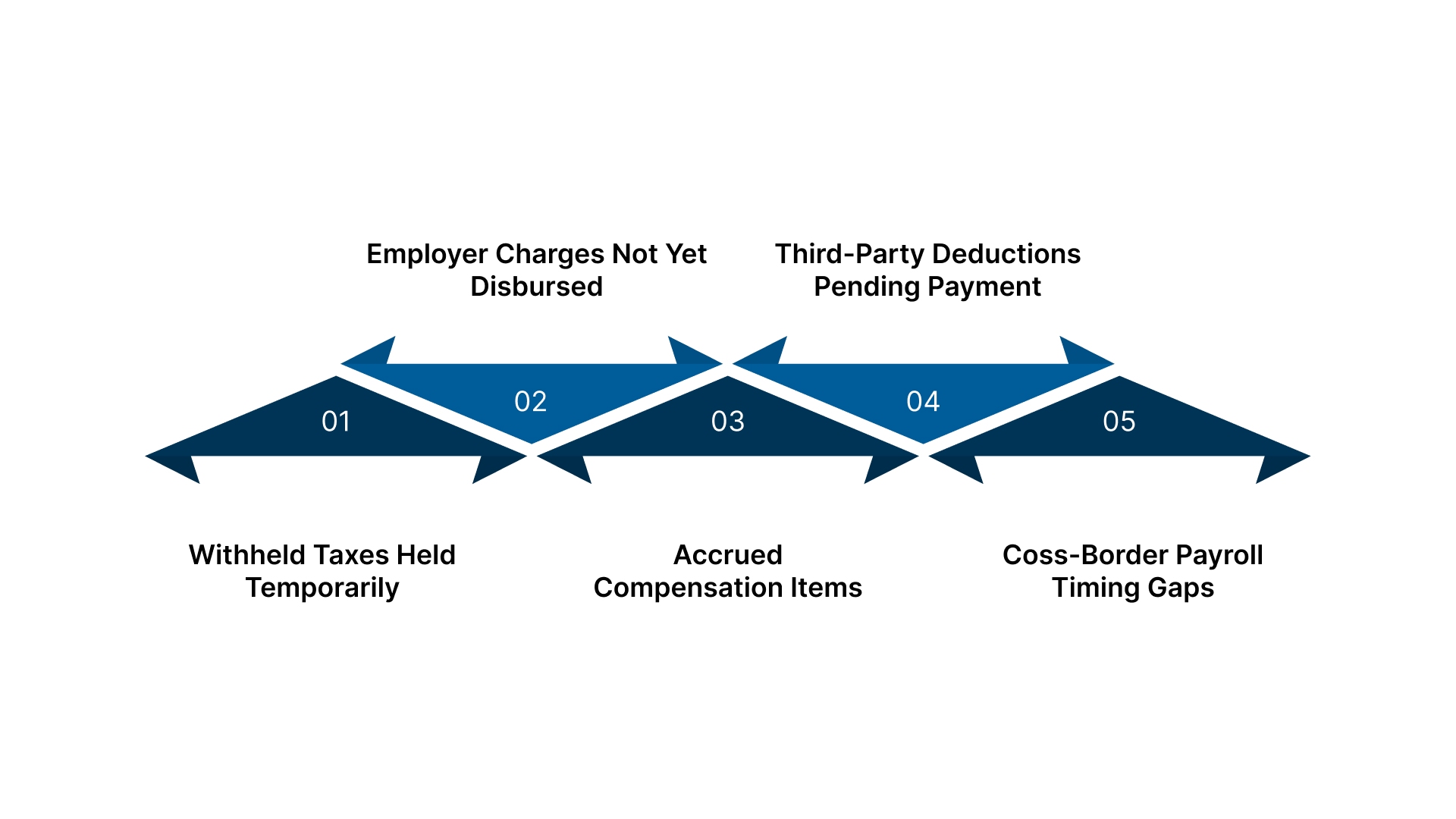

Withheld Taxes Held Temporarily: Payroll taxes are recorded as liabilities until cleared with agencies such as the IRS, state departments, the Income Tax Department, EPFO, or ESIC.

Employer Charges Not Yet Disbursed: Amounts owed for US FICA components or Indian employer contributions (PF, ESIC, labor welfare funds) remain unpaid liabilities until transferred.

Accrued Compensation Items: Unpaid bonuses, overtime dues, leave encashment, and incentives become payroll liability entries until processed in the next payroll cycle.

Third-Party Deductions Pending Payment: Unremitted health plan premiums, retirement plan deductions, or local Indian statutory funds are carried as liabilities until deposited.

Cross-Border Payroll Timing Gaps: US deposit schedules (semi-weekly or monthly) and Indian deadlines (PF by the 15th, TDS by the 7th) create temporary liability periods across two systems.

To manage payroll liabilities correctly, companies must track the exact statutory categories generated across both payroll systems.

Key Payroll Liability Types for US to India Operations

Each payroll liability type follows its own statutory calculation method and deposit workflow under US and India rules. These categories form the core structure used in cross-border payroll liability registers.

Federal Income Tax (US) and TDS on Salary (India): Amounts withheld from employee pay that remain unpaid until deposited with the IRS or the Income Tax Department. US deposits follow semi-weekly or monthly cycles; India requires a TDS deposit by the 7th of the following month.

FICA: Social Security and Medicare (US): Employee share plus employer share withheld but not yet transferred to the IRS. Calculated on taxable wages up to annual wage caps for Social Security; Medicare has no wage cap.

State Income Tax and Local Tax Withholdings (US): Amounts withheld under state tax codes (e.g., California PIT, New York SIT) and local taxes where applicable. Due dates vary by state, but remain payroll liability items until the agency deposit is complete.

Provident Fund (EPF) Contributions (India): Employee and employer shares are recorded as liabilities until deposited with the EPFO. Deposit due by the 15th of the following month; the employer share includes pension and PF segments.

ESIC Contributions (India): Employee and employer portions due under the Employees’ State Insurance Act. Submission must be completed by the 15th of the month for all employees within ESIC wage limits.

Health, Dental, Retirement, and Other Benefit Deductions (US & India): Amounts withheld for medical plans, 401(k) contributions, NPS, term insurance, or cafeteria plan deductions. Entries remain recorded as payroll liabilities until remitted to the plan provider.

Accrued Wages and Unpaid Earnings: Wages earned but not yet paid at the period close, including overtime or shift earnings. Recorded as a payroll liability at month-end until released in the next payroll run.

Bonuses, Incentives, and Variable Pay Accruals: Approved but unpaid bonuses, commissions, or retention payouts. Appear under payroll liability ledgers only when authorised and accrued, not during estimation.

Wage Garnishments and Court-Ordered Deductions: Amounts withheld under garnishment orders, child support directives, or recovery proceedings. Must be remitted exactly as stated in the order; remain liabilities until the transfer is completed.

Payroll Clearing, Reversals, and Pending Adjustments: Transactions held temporarily due to bank returns, incorrect employee bank details, or pending corrections. These appear in payroll liability clearing accounts until fully reconciled.

These liability categories form the basis for the calculation and tracking steps required during a US-to-India payroll shift.

From bookkeeping to audit prep, we handle it all. Discover how outsourcing can work for you.

How Companies Calculate and Track Payroll Liabilities When Moving From the US to India

US and India payroll systems follow different rules for withholding, posting, and confirming liability deposits. The steps below outline how companies manage these processes across both jurisdictions.

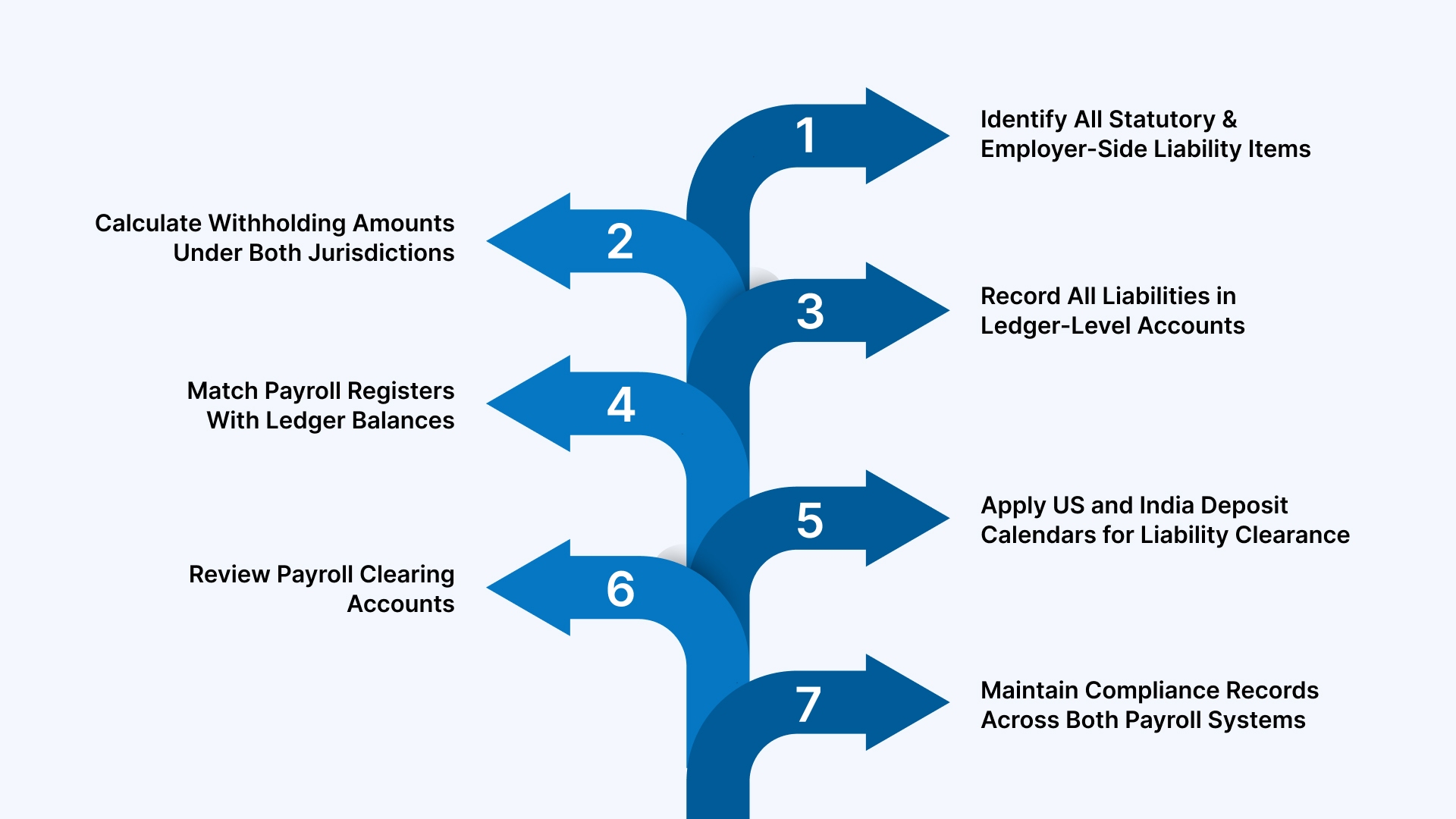

Step 1: Identify All Statutory and Employer-Side Liability Items

Compile a checklist of every legally required withholding and every employer contribution that can generate a payroll liability in either country. Map each item to its filing instrument, deposit channel, and ledger control account.

Key Details

Withholding Categories: Federal income tax withholding recorded under Form 941 family; state withholding and local taxes tied to state/local deposit systems; India TDS recorded under TAN and reported via Form 24Q.

Employer Charge Categories: US employer obligations include FICA employer share, FUTA (Form 940), and state unemployment deposits; India employer obligations include EPF employer share filed via EPFO ECR portals and ESIC deposits via the ESIC challan.

Accrual Categories: Accrued salary, unpaid overtime, earned leave encashment, and unpaid commissions are logged as payroll liabilities until paid; advances, payroll reversals, and suspense items must have a designated clearing account.

Step 2: Calculate Withholding Amounts Under Both Jurisdictions

Withholding must follow the exact rules issued by the US federal and state authorities and India’s income-tax provisions. Each calculated amount is recorded as a payroll liability until the corresponding agency confirms receipt. VJM Global often supports companies in validating these cross-border calculations during payroll consolidation.

Key Details

US Federal and State Rules: Federal income tax withholding follows IRS Publication 15 (current year tables) and Form W-4 data. State calculations depend on individual state rate tables and state-specific certificates, such as DE-4 (California). FICA is calculated on taxable wages using Social Security and Medicare rules.

Indian TDS Rules: TDS on salary follows Section 192, based on taxable income after exemptions and deductions claimed via declarations. Monthly TDS is linked to the TAN registration and must match the statements uploaded in Form 24Q.

Liability Status: All withheld amounts remain recorded as payroll liability entries until the deposit challan or agency acknowledgment appears in payroll records, IRS receipt, state confirmation number, or India’s OLTAS/EPFO/ESIC acknowledgment.

Step 3: Record All Liabilities in Ledger-Level Accounts

Each calculated item is posted to a mapped liability account, so the payroll liabilities balance sheet reflects pending US and India statutory dues clearly. This structure prevents overlap between jurisdictions and keeps audit trails clean.

Key Details

Separate Control Accounts: Dedicated liability accounts are created for IRS withholding, state taxes, FICA, TDS, PF, and ESIC, so each item is tracked without merging categories.

Accrual Entries: Unpaid earnings such as overtime, commissions, or leave payouts are posted to short-term payroll liability accounts until released in the next cycle.

Clear Posting Rules: Only validated payroll data is posted; any adjustment, reversal, or correction is routed through a separate payroll clearing account before final entry.

Step 4: Match Payroll Registers With Ledger Balances

The payroll register serves as the line-level source for confirming that every withholding, contribution, and accrual appears in the correct payroll liability account. This step helps maintain accurate links between processed payroll, statutory records, and ledger entries across US and India operations.

Key Details

Register Matching: Employee-level tax, benefit, and contribution figures in the payroll register must correspond to the liability amounts posted for IRS, state authorities, TDS, PF, and ESIC.

Variance Tracking: Any difference between register totals and ledger balances is investigated before month-end to avoid incorrect liability positions.

Supporting Documents: Payslips, W-4 and state certificates, TDS workings, and PF/ESIC computation sheets serve as validation for each posted liability.

Step 5: Apply US and India Deposit Calendars for Liability Clearance

Each payroll liability follows a fixed deposit schedule set by US federal/state agencies and Indian statutory bodies. These timelines determine when a liability can be cleared from the payroll liabilities balance sheet after payment acknowledgement.

Key Details

US Timelines: Federal income tax and FICA follow IRS deposit schedules, which may be semi-weekly or monthly, depending on the employer’s lookback period. State deposits follow state-issued calendars.

India Timelines: TDS deposits follow monthly due dates through OLTAS, while PF and ESIC payments follow their respective statutory deadlines for the following month.

Liability Closure: A payroll liability is cleared only after deposit confirmation, such as an IRS receipt, state confirmation ID, OLTAS challan, PF ECR receipt, or ESIC challan.

Step 6: Review Payroll Clearing Accounts

Payroll clearing accounts capture temporary payroll items that arise from corrections, reversals, or payment returns. For US-to-India operations, reviewing these accounts prevents unresolved entries from appearing as payroll liabilities at period close.

Key Details

Adjustment Identification: Items such as returned payments, incorrect tax postings, or duplicate entries are isolated in the clearing account until corrected.

Timeline Review: Only unresolved items remain in the clearing account; once validated, they shift to the appropriate payroll liability or expense account.

Correct Reclassification: After confirming the correction source, the entry is posted to the correct statutory liability, IRS, state, TDS, PF, or ESIC, before closing the period.

Step 7: Maintain Compliance Records Across Both Payroll Systems

Every payroll liability must be supported with clear deposit proof and computation records from both the US and Indian systems. These documents confirm that payroll taxes are recorded as liabilities only until cleared, and they form part of audit-ready files used during internal checks or external reviews. VJM Global often assists companies in organising these records across jurisdictions.

Key Details

Deposit Receipts: Agency acknowledgments such as IRS deposit confirmations, state payment IDs, OLTAS challans, PF ECR receipts, and ESIC challans verify liability clearance.

Employee-Level Records: Payslips, W-4 and state forms, TDS data, and PF/ESIC computation sheets confirm that individual deductions match posted payroll liabilities.

Audit Readiness: Copies of deposit reports, reconciliation files, and ledger extracts support internal reviews and help maintain clear records for cross-border audit teams.

Once the calculation and tracking steps are in place, the next priority is distinguishing which payroll amounts sit as liabilities and which move to expenses.

Partner with VJM Global for cross-border payroll support that covers withholding calculations, liability tracking, deposit confirmations, and audit-ready documentation across both jurisdictions.

Payroll Liabilities vs Payroll Expenses in a US to India Setup

Payroll items follow different accounting paths depending on whether they remain unpaid statutory amounts or are completed payroll costs. The table below outlines how these classifications operate across the US and India systems.

Paid salaries, employer FICA share, employer PF share, employer ESIC share, and released bonuses.

Posting Timing

Recorded when processed, but remain open until agency or fund receipt is confirmed.

Recorded once payment to employees or authorities is completed.

Clearance Method

Cleared after deposit proof such as IRS receipt, state confirmation ID, OLTAS challan, PF ECR receipt, or ESIC challan.

Cleared instantly once payment is made with no pending statutory confirmation.

Balance Sheet Impact

Appears under current liabilities on the payroll liabilities balance sheet.

Appears under payroll-related expenses in the income statement.

Control Accounts

Uses liability accounts for IRS, state bodies, TDS, PF, ESIC, and other deductions.

Uses expense accounts tied to employer contributions and paid compensation.

US–India Considerations

Dual deposit calendars create separate liability windows in both jurisdictions.

Posting remains country-specific and tied only to actual disbursement.

Once payroll items are separated into liabilities and expenses, the remaining challenge is managing how each liability behaves across the US and India systems.

Outsource your bookkeeping and save time without compromising accuracy. Let us handle the books.

Challenges and Practical Steps for Payroll Liabilities From the US to India

Liability discrepancies often arise because US payroll rules and India’s statutory workflows follow separate calculation and clearance paths. The challenges below reflect the exact points where these paths diverge.

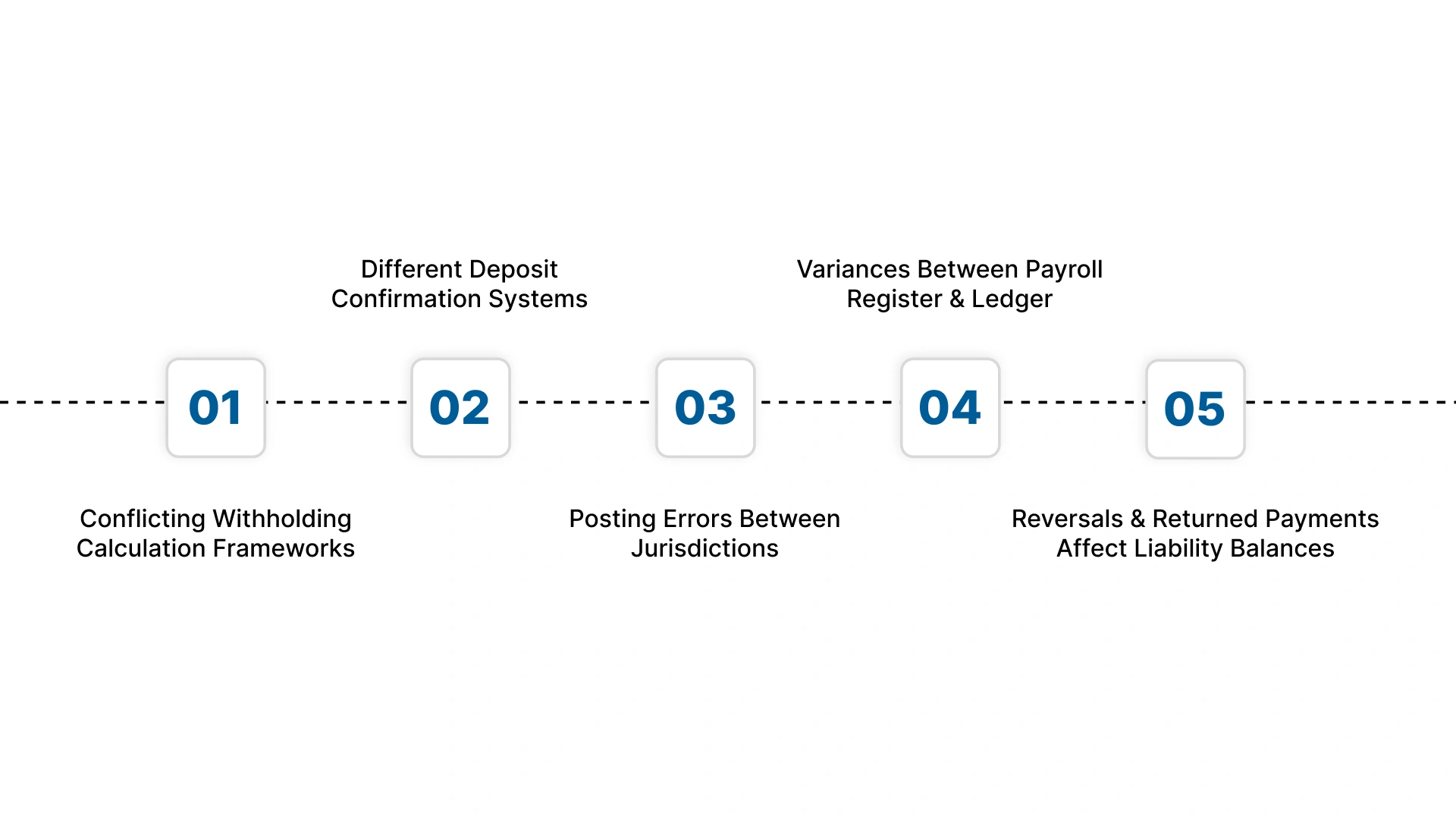

US withholding uses IRS Publication 15, Form W-4 data, and state certificates; India uses Section 192 and monthly TDS workings.

Practical Step: Create separate computation sheets for IRS, each state, and TDS to avoid merging US federal/state rules with Indian slabs.

Challenge 2: Different Deposit Confirmation Systems

US confirmations rely on EFTPS/agency IDs; India uses OLTAS challans, PF ECR receipts, and ESIC challans.

Practical Step: Map each liability to its corresponding confirmation document so clearance happens only when the correct receipt is logged.

Challenge 3: Posting Errors Between Jurisdictions

US liability entries (Federal Withholding, FICA, state withholding) and Indian entries (TDS, PF, ESIC) can be posted into the wrong control account.

Practical Step: Maintain distinct control accounts for IRS, each state, TDS, PF, and ESIC instead of using a pooled “tax liability” account.

Challenge 4: Variances Between Payroll Register and Ledger

Employee-level US withholdings and India TDS or PF values may not match posted ledger figures during the month-end.

Practical Step: Run a register-to-ledger match for every employee using payroll deduction codes (US: FIT, SIT, FICA; India: TDS, PF, ESIC).

Challenge 5: Reversals and Returned Payments Affect Liability Balances

Returned salary payments, incorrect tax postings, or PF/ESIC deposit failures hold amounts in liability status longer than intended.

Practical Step: Review payroll clearing accounts weekly and reclassify each unresolved entry to the correct liability or adjustment category.

These operational challenges highlight where expert cross-border support becomes necessary for accurate payroll liability control.

How VJM Global Supports Payroll Liability Management From the US to India

VJM Global assists companies shifting payroll work from the US to India by building accurate liability structures, aligning statutory requirements across jurisdictions, and maintaining clean records for audits. Their team manages cross-border withholding calculations, statutory deposits, ledger postings, and payroll liability reconciliation so pending amounts are recorded correctly on the payroll liabilities balance sheet.

Cross-Border Withholding Accuracy: VJM Global prepares US federal/state and India TDS computations with matching statutory worksheets to prevent incorrect liability values across jurisdictions.

Mapped Liability Control Accounts: They create and maintain distinct ledger accounts for IRS, state authorities, TDS, PF, and ESIC so payroll taxes are recorded as liabilities without overlap.

Deposit Tracking Across Two Systems: US deposits are tracked through EFTPS and state portals; Indian deposits through OLTAS, PF ECR, and ESIC challans to confirm liability clearance.

Register-to-Ledger Reconciliation: Employee-level deductions from US and India payroll registers are matched with posted payroll liability accounts to prevent month-end misclassification.

Clearing of Adjustments and Reversals: Returned payments, reversals, and late adjustments are reviewed and reclassified, preventing inflated payroll liability balances.

Audit Support for Dual Jurisdictions: VJM Global compiles IRS receipts, state payment IDs, TDS data, PF ECR files, and ESIC challans into audit-ready documentation sets.

VJM Global supports firms in keeping payroll liabilities precise and well-documented across both payroll systems.

Conclusion

Managing payroll liabilities across the US and India requires close attention to withholding methods, deposit cycles, and cross-border statutory records. When each liability item is calculated correctly and supported with the right documentation, companies reduce errors in payroll ledgers and avoid compliance gaps during expansion.

VJM Global supports US businesses moving operations to India by handling federal and state withholding work, India TDS calculations, PF and ESIC entries, deposit tracking, and payroll liability reconciliation. Their team prepares accurate records for the IRS, state agencies, OLTAS, PF, and ESIC so every payroll liability stays current and verifiable across both systems.

Contact VJM Global to keep your payroll liabilities organised, compliant, and ready for audits as you expand from the US to India.

FAQs About Payroll Liabilities

1. Can payroll liabilities include items that are not tied to employee wages?

Yes. A payroll liability can include unpaid employer-side charges such as the US employer FICA portion or India’s PF/ESIC employer share, even when wages are already paid.

2. Why are payroll taxes recorded as liabilities before they appear in statutory filings?

Payroll taxes are recorded as liabilities because the amounts are owed to agencies like the IRS, state departments, or India’s Income Tax Department, but remain unpaid until the deposit is completed.

3. Does the payroll liabilities balance sheet change when a deposit is initiated but not yet confirmed?

No. The payroll liabilities balance sheet updates only after official confirmation, such as an EFTPS ID, state receipt, OLTAS challan, PF ECR, or ESIC challan.

4. Can payroll liabilities remain open even if the payroll run is fully processed?

Yes. Items such as garnishments, PF arrears, state withholding catch-up entries, or cross-border reversals can remain as open payroll liabilities until the matching deposit or correction is posted.

5. Do US-to-India payroll transitions create temporary payroll liability categories not seen in single-country operations?

They can. For example, FX timing differences, cross-border clearing entries, or dual withholding adjustments may appear as temporary payroll liability items until reconciled.