.avif)

U.S. businesses handle millions in daily transactions. According to Deloitte’s 4Q 2024 CFO Signals survey, 42% of CFOs say enterprise risk management, including internal controls, is a top priority for 2025. Another 40% are focused on digitally transforming finance, where weak control structures often create costly vulnerabilities.

But how do companies make sure every dollar adds up, every record checks out, and no unauthorized access slips through? The answer lies in internal controls.

In a global environment where regulatory scrutiny intensifies and cyber threats become more sophisticated, internal controls are no longer optional; they're strategic. Modern businesses, particularly those expanding across borders or undergoing digital transformation, rely on strong internal control frameworks to maintain transparency, mitigate liability, and foster sustainable growth.

This article examines the role of internal controls in ensuring financial accuracy, mitigating risk, and maintaining operational consistency. You'll get a breakdown of control types, components, and limitations, along with practical reasons why internal control frameworks remain essential to modern business.

Internal controls are structured systems and policies that help protect assets, ensure accurate information, and support compliance with laws and regulations. These controls form the foundation of a company’s risk management strategy and are critical to the overall health and stability of the organization.

Internal controls are woven into nearly every business function. In finance, they help prevent errors and fraud in processes such as payroll, invoicing, and budgeting. In procurement, they ensure purchases are authorized and properly documented. In IT, they govern data access, user permissions, and cybersecurity protocols.

Internal controls act as checks and balances. They help reconcile statements, approve expenses, and assign duties to prevent misuse, detect issues, and ensure accountability.

When well-designed and properly implemented, internal controls help organizations operate efficiently, produce reliable financial statements, and avoid legal or regulatory trouble. They support sound decision-making and build trust with stakeholders, including employees, board members, investors, and regulators.

Internal controls are essential mechanisms within any organization, designed to safeguard assets, ensure the accuracy of financial information, and promote efficient operations. But what is the exact purpose of these controls?

Simply put, internal controls serve to prevent errors, detect fraud, and enhance operational efficiency. They act as a system of checks and balances, a set of guardrails that guide business activities and protect the company from risks.

Here’s a closer look at what internal controls help businesses achieve:

Accurate financial data forms the backbone of any business decision. Internal controls ensure that all transactions are accurately and consistently recorded, thereby reducing the likelihood of errors in bookkeeping, reporting, and tax filings. This accuracy enables management to make informed decisions and presents an accurate picture of the company’s financial health to investors and regulators.

Internal controls help prevent fraud, theft, and the misuse of company resources by establishing clear approval processes, segregating duties, and conducting regular reviews. When properly designed and implemented, these controls catch unauthorized or suspicious activities early, minimizing potential losses and reputational damage.

Standardized procedures reduce variability and errors in day-to-day operations. Controls enforce adherence to company policies and workflows, ensuring that employees follow best practices uniformly. This consistency not only streamlines operations but also improves productivity and reduces operational risks.

Many industries face strict compliance standards and external audits. Internal controls help businesses stay aligned with relevant laws, regulations, and accounting standards. By maintaining well-documented controls and records, companies can avoid penalties, fines, and legal complications and demonstrate accountability to auditors and regulators.

Investors, customers, employees, and partners all rely on the integrity and reliability of a business. Strong internal controls signal that a company is well-managed, transparent, and committed to protecting its assets. This trust can enhance a company’s reputation, attract investment, and foster long-term relationships.

Suggested Read: Understanding Company Audits: Key Processes and Types

The cost of weak oversight can be devastating for any organization. Financial misstatements, regulatory penalties, and internal theft cut into revenue. They also damage reputation and erode trust among investors, customers, and partners.

In today’s complex business environment, companies face constant pressure to maintain accurate financial records and comply with an ever-growing list of regulations. To meet these challenges, they rely on strong internal accounting controls.

Internal accounting controls serve as the company’s first line of defense against financial risks. By implementing these controls, businesses aim to prevent errors and fraud before they occur rather than simply reacting to problems after the fact. These controls provide a framework to ensure:

By maintaining strong internal accounting controls, companies not only protect their assets but also demonstrate their commitment to transparency, accountability, and adherence to compliance standards. This, in turn, builds confidence with stakeholders and supports long-term business success.

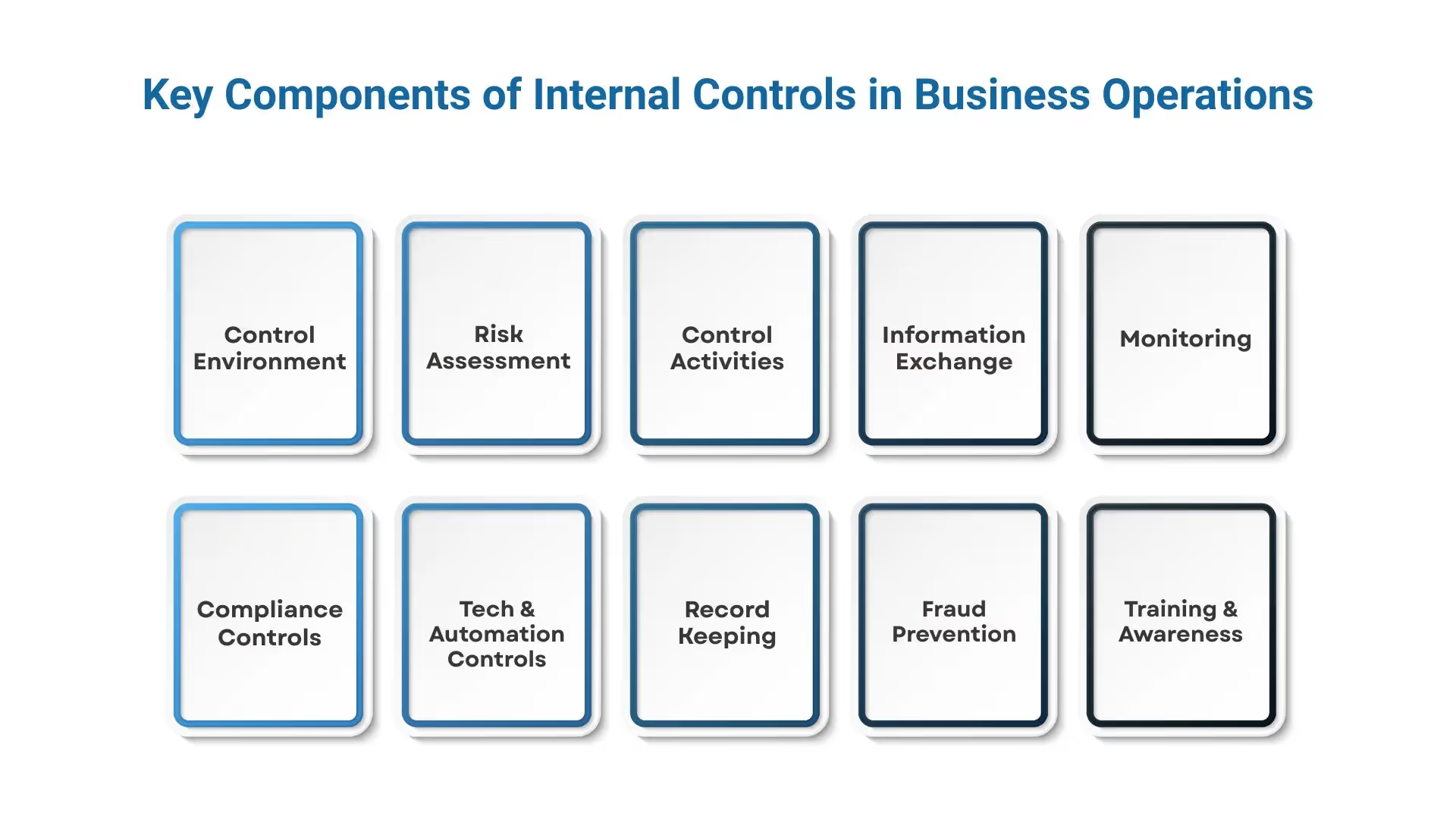

Internal controls are essential for safeguarding assets, ensuring accurate financial reporting, promoting operational efficiency, and maintaining compliance with laws and regulations. A strong system of internal controls helps prevent fraud, detect errors, and improve business processes.

The primary components of internal controls include:

Also Read: Corporate Tax Audit Guide for Businesses

Internal controls establish a structured approach to safeguard assets, ensure the accuracy of financial data, promote efficient operations, and guarantee compliance with laws and internal policies.

By categorizing these controls into distinct types, organizations can apply targeted measures to address different risks and challenges effectively:

1. Preventive Controls: Preventive controls are designed to stop errors, fraud, or unauthorized actions before they even happen. By establishing clear rules, barriers, and procedures, these controls reduce the risk of mistakes and misconduct at the earliest stage possible, often deterring potential issues before they arise.

Example: A company implements a policy requiring two separate employees to both authorize and approve any payment that exceeds $10,000. This segregation of duties ensures no single person has full control over disbursing funds, which helps prevent fraud or misappropriation of company money.

2. Detective Controls: Detective controls focus on identifying errors, fraud, or irregularities as soon as possible after they have occurred. These controls enable organizations to identify and address problems promptly, minimizing potential damage and enhancing accountability.

Example: Each month, the company performs detailed bank reconciliations that compare internal accounting records against the bank statements. Any discrepancies or unusual transactions uncovered during this process are thoroughly investigated and resolved to maintain accurate financial records.

3. Corrective Controls: Corrective controls come into effect after an issue has been identified by detective controls. Their purpose is to correct the problem and implement changes that prevent similar issues from occurring again, thus improving internal processes or strengthening system weaknesses.

Example: Following the detection of a cybersecurity breach, the company responds by upgrading its cybersecurity software and implementing multi-factor authentication. Additionally, employees receive training on creating strong passwords and recognizing phishing attempts, all aimed at preventing future security incidents.

4. Directive Controls: Directive controls provide employees with clear instructions, guidelines, and standards to ensure their activities comply with company policies and regulatory requirements. These controls foster consistent behavior, ethical conduct, and alignment with organizational goals.

Example: The company distributes a comprehensive code of conduct that outlines expected ethical behaviors and legal obligations. Quarterly training sessions are held to reinforce these standards, ensuring employees understand their responsibilities and how to apply the rules in daily operations.

5. Physical Controls: Physical controls focus on protecting tangible assets like cash, inventory, equipment, and sensitive documents from theft, damage, or unauthorized use. These controls typically involve securing physical spaces and limiting access to authorized personnel only.

Example: A warehouse facility employs multiple layers of physical security, including strategically placed security cameras to monitor key areas, high-quality locks on all doors, and a policy that requires all staff to wear ID badges that must be shown to enter restricted zones. This approach significantly reduces the risk of inventory theft or unauthorized access.

You Might Also Like To Read: Unlocking the Benefits of Internal Audit Outsourcing

Despite their importance, internal controls have inherent limitations that can affect their effectiveness. Understanding these limitations is critical for management, auditors, and stakeholders to set realistic expectations and implement complementary measures. The key limitations include:

强有力的内部控制是任何经营良好业务的支柱。它们降低财务风险,防止欺诈并确保合规性。这些控制措施对增长和投资者信心至关重要。在VJM Global,我们通过提供针对其特定需求量身定制的专业离岸会计支持,协助总部位于美国的注册会计师事务所和企业实施有效的内部控制系统。

方法如下 VJM Global 通过离岸人员配置支持更好的内部控制:

随着审计审查的加强以及远程环境中欺诈风险的增加,拥有强大的内部控制框架不再是可选的。VJM Global将专业知识、技术和人员灵活性完美结合,帮助注册会计师事务所和企业保持领先地位。

无论您是在为监管漏洞而苦苦挣扎,还是需要随着成长扩展控制系统,VJM Global都是您的离岸问责合作伙伴。

立即联系我们 了解我们如何支持您的内部控制策略,同时为您的公司节省时间和金钱。

A: 内部控制措施旨在保护公司资产,防止错误和欺诈,并确保准确、及时的财务报告。它们还通过促进业务一致性、问责制以及对法律和内部政策的遵守来支持战略决策。

A: 公司实施内部会计控制,以限制财务错报、挪用资金和运营中断的风险。这些控制措施有助于验证会计记录的完整性,执行职责分离,并为监管机构和利益相关者提供清晰的审计跟踪。

A: 内部控制建立在五个核心要素之上:

A: 没有哪个系统是万无一失的。尽管内部控制显著降低了欺诈风险,但它们无法完全消除欺诈风险,尤其是在存在串通或管理层超越的情况下。但是,精心设计的控制框架通过增加监督和问责层来提高侦查率并阻止不当行为。

A: 公司应至少每年对内部控制进行一次正式评估。但是,在快速增长、组织重组、系统升级或监管要求变化期间,应更加频繁地进行审查。持续的监控和定期审计有助于在控制漏洞升级为更大的风险之前识别出来。