.avif)

Are you a US business owner trying to figure out how to settle your tax debt? You’re not alone. In fiscal year 2024, the IRS collected nearly $77.6 billion in unpaid taxes from individuals and businesses through its collection efforts.

For small to mid-sized companies, tax debt problems can create cash flow bottlenecks, increase financial stress, and distract you from running your business. That’s where debt tax relief options come in.

From IRS settlement programs and professional tax debt services to options like an Offer in Compromise, choosing the proper relief solution can make all the difference for your business.

In this guide, you’ll learn practical ways to settle tax debts so you can put IRS notices behind you. By exploring these options, you’ll be able to address overdue liabilities, safeguard daily operations, and restore financial stability with confidence.

Tax debt arises when your business fails to pay taxes in full or on time. Common triggers include cash flow challenges, accounting mistakes, or unexpected financial setbacks. Once payments are delayed, the IRS begins adding interest and penalties, which can quickly escalate into a significant liability for small businesses.

The impact goes far beyond late fees. Outstanding tax debt can strain your finances, limit access to credit, and hurt your business reputation. The IRS has strong enforcement powers and can:

Stay ahead of these IRS penalties with VJM Global’s tax planning support. Prevent them before they hit your business.

Also Read: Corporate Tax Audit Guide for Businesses

While tax debt can feel overwhelming, you do have options. The IRS provides several tax debt settlement programs with which your business can take structured steps to resolve outstanding liabilities. Let’s look at the most practical ways to settle your tax debt and move toward financial stability.

For small and mid-sized businesses in the US, unpaid taxes can quickly spiral into a significant problem. Fortunately, the IRS provides several tax debt relief options designed to help you get back on track. Let’s explore them.

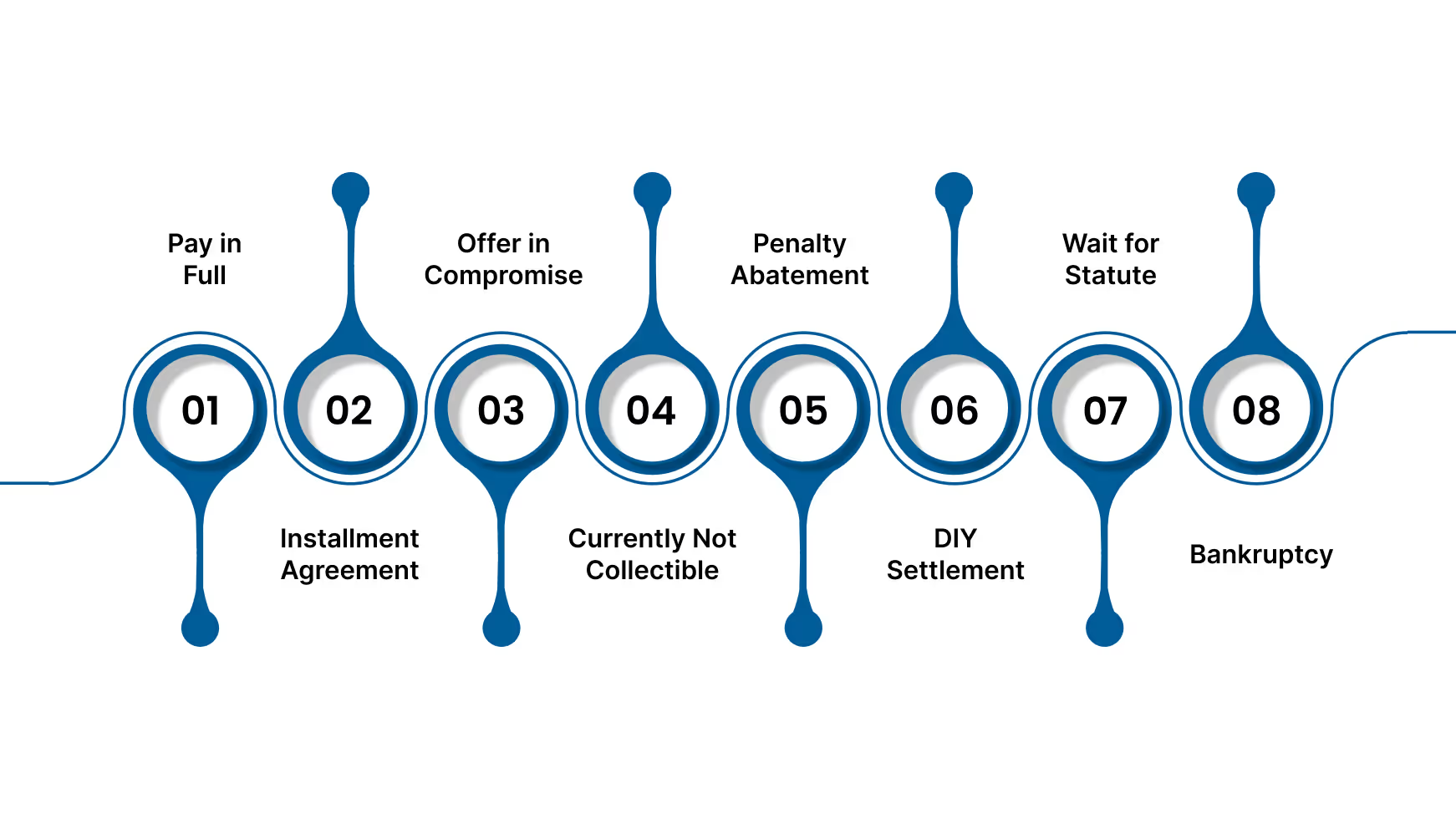

The most straightforward tax debt solution is paying the entire balance at once. While challenging for many small businesses, it’s the fastest way to close the case, avoid future IRS collection actions, and stop additional interest or penalties.

Best For: Businesses with access to cash reserves or financing

Why is it beneficial?

Limitations:

When paying in full isn’t realistic, an installment agreement allows you to spread payments out over time in monthly installments instead of one lump sum.

Best for: Businesses with stable cash flow but unable to pay in a single instance.

Two common types:

Pro Tip: Even if you enter into an installment agreement, try to make higher monthly payments than the minimum to cut down on long-term interest costs.

If your business cannot reasonably pay the full debt, an Offer in Compromise may enable you to settle for less than what you owe. This IRS program is selective but can be a lifeline for companies facing overwhelming financial hardship.

Best for: Businesses at risk of shutting down if forced to pay their full tax debt.

Considerations:

Key Insights:

If your business is in severe financial distress, the CNC status puts IRS collection activity on hold. While interest and penalties continue to add up, it gives you time to regroup and focus on stabilizing operations.

Best for: Businesses experiencing severe financial hardship.

What it means:

Why it matters:

Pro Tip: Use the CNC period to prepare a repayment or restructuring plan. Treat it as a pause, not a permanent solution.

Also Read: Understanding the Three Financial Statements and Their Connections

If penalties make up a large portion of your tax debt, you may qualify for penalty abatement. It removes or reduces penalties but not the tax itself or interest.

Best for: Businesses where penalties are the most significant driver of tax debt.

Common options:

Example: A small design agency in New York faces $12,000 in penalties due to late filings. By applying for a first-time abatement, they can have the penalties waived, leaving only the tax and interest.

Some small business owners choose to negotiate directly with the IRS instead of using outside tax debt services. This “DIY” route can work if your debt is relatively manageable and you’re confident in handling the paperwork and communication yourself.

How it works:

Pros:

Cons:

The IRS generally has up to 10 years to recover unpaid taxes. Once this statute of limitations ends, the debt is cleared, and any liens or levies tied to it are released.

However, in rare cases, businesses attempt to let this window run out. While the debt technically expires, this option exposes you to years of aggressive collection activity and risks damaging your business reputation.

Why businesses avoid this option: This is not a proactive solution. You’re chased by the IRS for constant repayment during the tenure, making financing and growth impossible. Moreover, there are risks of criminal charges for willful nonpayment.

Bankruptcy can sometimes wipe out older income tax debts and stop IRS collection efforts. While it may provide a reset, it comes with significant long-term financial consequences and should only be considered after other options fail.

Best for: Businesses with overwhelming debt where other options have failed.

Key Takeaways:

Risks:

Note: Bankruptcy should only be considered after professional tax debt relief services confirm that no other solutions fit.

Knowing your tax debt relief options is only half the battle. The next step is to choose a trusted service and avoid costly scams.

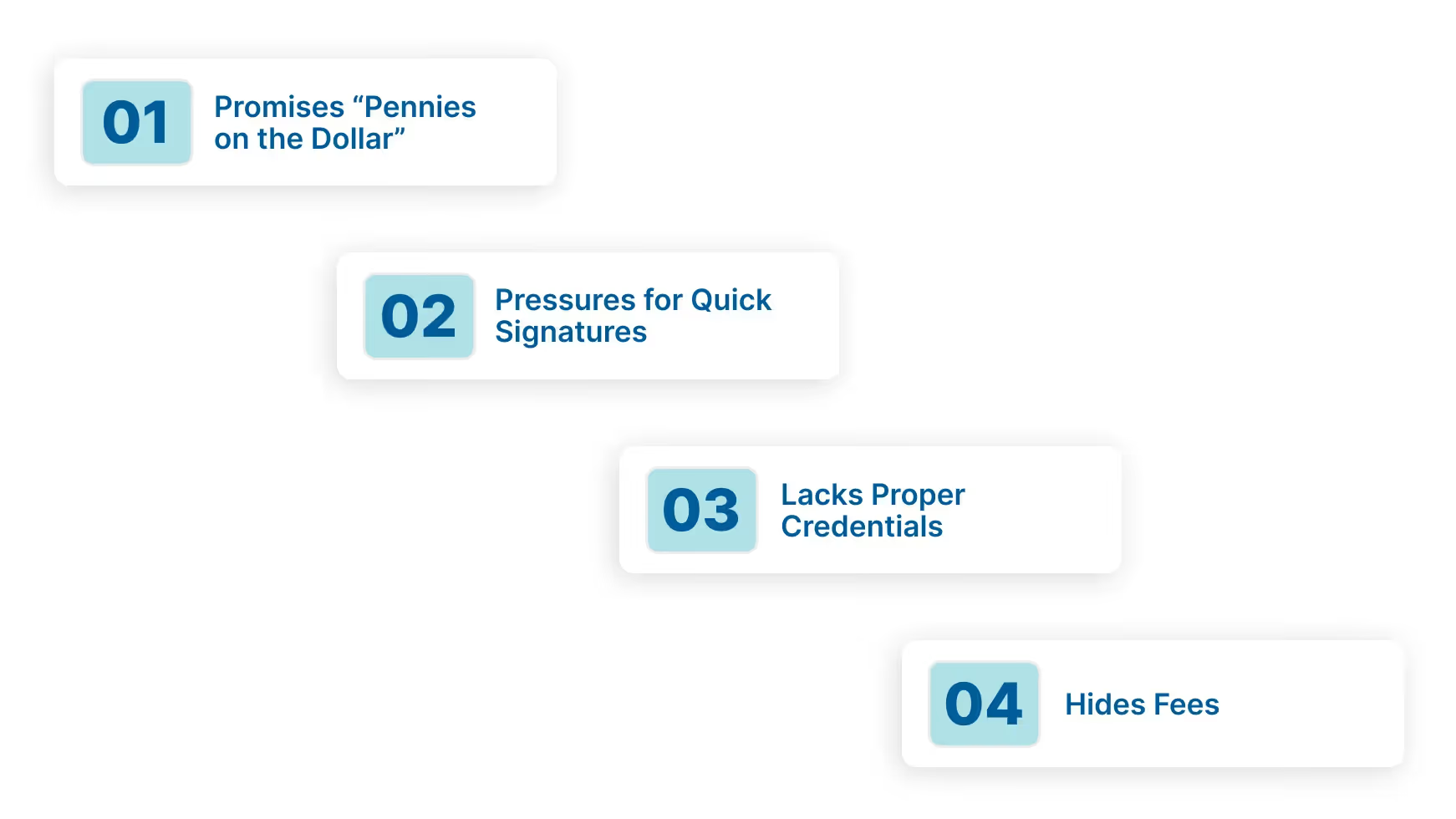

Not all tax debt relief services are created equal. While some provide genuine help, others prey on businesses under stress, making promises they can’t deliver. Knowing what to look out for helps you avoid scams and choose a reliable partner.

Be cautious if a company:

Why it matters: Many small businesses end up paying more in service fees than their actual tax debt, while still facing IRS penalties.

To avoid these costly mistakes and protect your business, check for:

Pro Tip: Always request a free initial consultation. This gives you a sense of whether the company focuses on education and problem-solving, or just aggressive sales tactics.

Also Read: Strategic Tax Planning Services for Businesses

Tax debt can disrupt cash flow, damage credibility, and expose your business to aggressive IRS enforcement. As we’ve covered, options such as installment agreements, Offers in Compromise, penalty abatement, and temporary hardship status give you different ways to settle overdue liabilities. Choosing the right path depends on your financial capacity and how quickly you need relief.

However, long-term stability comes from preventing these issues in the first place. Many businesses fall into tax problems because of irregular cash flow, accounting errors, or missed filings. Strong financial management, including accurate bookkeeping, timely reconciliations, payroll oversight, and proactive tax planning, keeps your operations compliant and future-ready.

This is where VJM Global supports you directly. By outsourcing your accounting and bookkeeping to an Indian team that understands US accounting standards and regulations, you reduce overhead costs. You also maintain compliance with IRS requirements and gain real-time visibility into your financials.

Tired of tax debt pulling focus from your business goals? Let VJM Global take charge of your accounting and compliance, so you can protect cash flow, stay IRS-compliant, and get back to growing your business. Book a consultation today.

Small businesses can qualify for IRS payment plans lasting up to 72 months and sometimes even 84 months. This allows them to spread tax debt repayment over years while keeping operations financially stable.

If your business misses tax deadlines, the IRS charges a 5% monthly penalty for late filing, 0.5% monthly for late payment, plus daily compounding interest. This rapidly escalates your total debt burden.

Tax debt settlement is an arrangement with the IRS that lets you resolve what you owe through programs like payment plans, penalty relief, reduced payoff offers, and more. It helps your business manage debt without crippling operations.

If your business misses payroll tax payments, the IRS can impose the Trust Fund Recovery Penalty. This makes you personally liable, even as an LLC or corporation, and lets the IRS pursue your assets to recover unpaid taxes.

A lien is the IRS’s legal claim against your business property when you owe taxes, affecting credit and financing. A levy is more severe, where the IRS actually seizes funds or assets to cover your tax debt.

Gather tax returns, bank statements, profit-and-loss reports, payroll records, and details of assets and debts. The IRS uses this information to determine eligibility for installment agreements, Offers in Compromise, or CNC status.