Many businesses know about revocation via Form GST REG-21, but the formal appeal mechanism — Form GST APL-01 — is frequently overlooked. This matters because revocation has a 90-day window and can itself be rejected. When that happens, APL-01 is your only structured legal recourse. This guide walks through the entire process: who can file, valid grounds, the step-by-step portal procedure, common mistakes, and what happens after you submit.

Key Takeaways

- Form GST APL-01 is the formal appeal filed with the First Appellate Authority against a registration cancellation order

- This route applies only when the officer cancelled registration on their own motion — not when the taxpayer voluntarily cancelled

- File within 3 months of receiving the cancellation order; the authority can condone delays of up to one additional month

- Companies and LLPs must use DSC; EVC is available for other entity types

- Outcomes include registration restoration or further escalation to the GST Appellate Tribunal (GSTAT) or High Court

What Is an Appeal Against GST Registration Cancellation?

If your GST registration has been cancelled and you disagree with the order, Section 107(1) of the CGST Act gives you the right to appeal to the prescribed Appellate Authority within three months of the order being communicated. A registration cancellation order is fully covered under this provision.

Who you appeal to depends on the rank of the officer who issued the cancellation order:

- Order by Additional or Joint Commissioner → appeal to the Commissioner (Appeals)

- Order by Deputy/Assistant Commissioner or Superintendent → appeal to an officer not below the rank of Joint Commissioner (Appeals)

How This Differs from Revocation

Before filing a formal appeal, it's worth confirming which route applies to your situation. Revocation (GST REG-21 under Section 30) and a formal appeal (GST APL-01) serve different purposes and operate at different levels:

| Feature | Revocation (REG-21) | Formal Appeal (APL-01) |

|---|---|---|

| Forum | Same officer who cancelled | Higher appellate authority |

| Time limit | 90 days from cancellation order | 3 months from communication |

| Availability | Only when officer cancelled suo motu | When revocation rejected or window passed |

| Complexity | Simpler administrative process | Formal legal proceeding |

Orders Against Which an Appeal Can Be Filed

The GST portal FAQ lists these registration orders as appealable:

- GST REG-05 — Order of Rejection of Application for Registration/Amendment/Cancellation

- GST REG-19 — Order for Cancellation of Registration

- GST REG-28 — Order for Cancellation of Provisional Registration

- GST REG-08 — Order of Cancellation of Registration as Tax Deductor/Collector at Source

Appeal vs. Revocation: Choosing the Right Legal Path

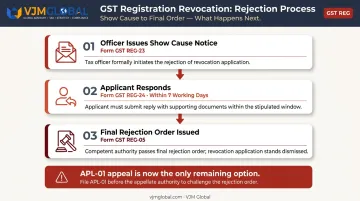

Revocation is the faster, simpler route — with one hard deadline. Under Rule 23(1), a GST REG-21 application must be filed within 90 days from service of the cancellation order. The same officer reviews it and, if satisfied, restores registration via Form GST REG-22.

When the officer is not satisfied, the process follows a fixed sequence before a final decision is made:

- The officer issues a show cause notice in Form GST REG-23

- The applicant responds in Form REG-24 within seven working days

- If the officer still rejects the application, the final order is issued in Form GST REG-05

Once REG-05 is issued, filing a formal appeal using APL-01 is the only remaining option.

When APL-01 Becomes the Only Path

File a formal appeal when:

- The revocation application was rejected via GST REG-05

- The 90-day revocation window has already passed

- The taxpayer disputes the cancellation on legal or procedural grounds (natural justice violations, factual errors)

- The cancellation involved fraud or misstatement allegations and the taxpayer has evidence to counter the department's findings

- The cancellation order is linked to non-filing of returns where the taxpayer can now demonstrate compliance

One important note: Neither revocation nor formal appeal applies when the taxpayer voluntarily cancelled their own registration under Section 29. The revocation provisions under Section 30 and Rule 23 only apply to cancellations initiated by the proper officer on their own motion. For self-cancelled registrations, a fresh GST registration application is the route forward.

Eligibility, Grounds, and Time Limits for Filing an Appeal

Who Can File

Any registered taxpayer or unregistered individual aggrieved by an adjudicating authority's order on GST registration matters is eligible. Those who are not eligible include:

- UIN holders (UN bodies, embassies) for most registration disputes

- GST Practitioners filing on their own behalf

- Taxpayers who voluntarily cancelled their own registration

Authentication method matters: Rule 26(1) of the CGST Rules requires DSC for persons registered under the Companies Act, 2013. Official form instructions also include LLPs in the DSC-mandatory category. All other entity types can use EVC (OTP verification).

Valid Grounds for Appeal

Specific, well-documented grounds are critical to getting an appeal admitted. Accepted grounds include:

- Cancellation without proper notice or hearing (violation of natural justice principles)

- Factually incorrect reasons cited in the cancellation order

- Pending returns that have since been filed and dues cleared

- Procedural errors in the cancellation proceedings

- Cancellation despite the business being operational and compliant with GST requirements

Courts have supported taxpayers on natural justice grounds. In Aggarwal Dyeing and Printing Works v. State of Gujarat (Gujarat High Court, February 2022), the court quashed vague show-cause notices and non-speaking cancellation orders. The ruling left room for fresh, lawful cancellation proceedings to follow.

Time Limits

- Standard deadline: 3 months from the date the cancellation order was communicated (not necessarily the date printed on the order)

- Condonation: Section 107(4) permits the Appellate Authority to allow filing within one additional month if sufficient cause is shown — the statute grants no wider discretion beyond this total four-month window

Delay beyond the total four-month window cannot be condoned under any circumstances.

How to File an Appeal Against GST Registration Cancellation Order

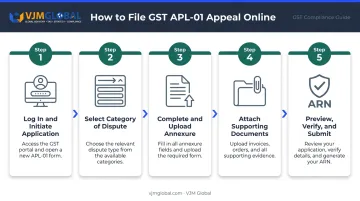

The official portal manual outlines a five-step process. Here is the complete procedure.

Step 1: Log In and Initiate a New Application

- Log in to www.gst.gov.in with valid credentials

- Navigate to Services → User Services → My Applications

- Select "Appeal to Appellate Authority" as the Application Type

- Click "New Application"

- Select Order Type: Registration Order

- Enter the Order Number and click Search to auto-populate order details

Step 2: Select the Category of Dispute

- From the "Category of Case Under Dispute" drop-down, select the appropriate category (e.g., cancellation of registration)

- Click Add — multiple categories can be added if applicable

- Edit the date of communication and period of dispute fields as needed

Step 3: Complete and Upload the Annexure to GST APL-01

This is the most critical step — the Annexure is where you lay out the legal and factual case for reversing the cancellation.

- Click "Click Here" to download the Annexure template

- Open in Microsoft Word, enable editing, and fill in detailed grounds of appeal

- Address the officer's original reasons for cancellation point by point with legal references and documentary support

- Save as PDF (maximum 5 MB) and upload

Vague grounds are the most common reason appeals fail at admission. The Annexure must cite specific CGST Act provisions, respond directly to departmental findings, and attach supporting evidence. VJM & Associates LLP helps clients draft legally sound grounds that address each departmental objection precisely.

Step 4: Attach Supporting Documents

Up to 4 supporting documents can be uploaded in PDF or JPEG format, maximum 5 MB each. Typical documents include:

- Original cancellation order

- Copies of pending GST returns now filed

- Tax payment challans and outstanding dues clearance proof

- Bank statements and business operation evidence

- Correspondence with the GST department

Additional documents can be submitted in hard copy to the Appellate Authority's office.

Step 5: Preview, Verify, and Submit

- Use the Preview button to review the complete application as PDF

- Select the Verification checkbox

- Choose the Authorized Signatory from the drop-down

- Enter the place of filing

- Click "Proceed to File" → "Proceed"

- Submit using DSC (mandatory for companies/LLPs) or EVC (OTP on registered mobile/email)

- An ARN (Acknowledgement Reference Number) is generated — download the acknowledgement immediately

Critical note on hard copies (Rule 108, Notification 26/2022-Central Tax, December 26, 2022):

| Scenario | Requirement | Filing Date |

|---|---|---|

| Cancellation order uploaded on portal | No hard copy needed | Date of online submission |

| Order not uploaded on portal | Self-certified copy within 7 days of online filing | Date of online submission |

| Hard copy submitted after 7 days | Self-certified copy required | Date hard copy is received — may trigger limitation issues |

Common Mistakes That Lead to GST Appeal Rejection

Weak or Generic Grounds in the Annexure

Broad statements without legal backing are the leading cause of admission failure. The Annexure must:

- Cite specific CGST Act provisions

- Address each departmental reason for cancellation individually

- Attach documentary evidence supporting every factual claim

- Be drafted with precision, not as a general complaint narrative

Procedural Errors That Invalidate Filings

- Missing the deadline: The combined four-month window (3 months + 1 month condonation) is absolute. Courts have refused to entertain appeals filed beyond this period

- Hard copy timing (where applicable): When the cancellation order is not on the portal, failing to submit self-certified copies within 7 days shifts your legally recognised filing date forward — potentially making a timely appeal appear late

- Wrong authentication method: Using EVC when DSC is mandatory (for companies and LLPs) will invalidate the filing

- File format or size errors: Documents must be PDF or JPEG, maximum 5 MB each

Misunderstanding the Dues Clearance Requirement

Beyond procedural errors, a common source of confusion is the dues clearance requirement. Rule 23 (revocation under REG-21) requires pending returns and outstanding amounts to be cleared in non-filing cases. That condition is specific to revocation — not to APL-01 appeals.

For APL-01 appeals involving a pure registration cancellation with no monetary demand, Section 107(6)'s pre-deposit requirement is demand-linked and may not apply. That said, clearing any pending returns before filing strengthens the appeal's credibility before the Appellate Authority.

What Happens After You File: Appeal Outcomes and Next Steps

After submission, the appeal status on the GST portal progresses through these stages:

| Status | What It Means |

|---|---|

| Appeal Submitted | Application received by the system |

| Appeal Admitted | Authority has admitted the appeal for hearing |

| Hearing Notice Issued | Formal notice of hearing date sent |

| Reply Submitted | Counter-reply submitted by the taxpayer |

| Show Cause Notice Issued | Authority raised additional queries |

| Appeal Order Passed | Final decision issued |

| Appeal Rejected | Appeal dismissed |

| Adjournment Granted | Hearing postponed |

Outcome Scenarios

Each appeal concludes in one of four ways:

- Approved — GST registration is restored. Resume all compliance obligations immediately: filing returns, paying taxes, and maintaining required records.

- Modified — Comply with the revised conditions specified in the appellate order.

- Rejected at admission stage — Re-file using the same Order ID before the limitation period expires.

- Rejected on merits — Escalate to the GST Appellate Tribunal (GSTAT) under Section 112 of the CGST Act, or approach the High Court under Article 226 of the Constitution for jurisdictional errors, natural justice violations, or fundamental rights issues. Note that courts expect taxpayers to exhaust statutory remedies first.

In Tvl. Suguna Cutpiece Center v. Appellate Deputy Commissioner (Madras High Court, January 2022), the court granted conditional restoration even after Section 107 appeals had been dismissed as time-barred. The condition: file all pending returns and pay statutory dues. This confirms that courts retain jurisdiction in appropriate cases even after an appeal rejection.

Frequently Asked Questions

How to file an appeal against cancellation of GST registration?

The appeal is filed online using Form GST APL-01 on the GST portal by navigating to Services → User Services → My Applications → Appeal to Appellate Authority. Upload the completed Annexure with grounds of appeal and supporting documents, then submit via DSC or EVC within 3 months of the cancellation order being communicated.

What is the time limit for GST cancellation appeal?

Under Section 107 of the CGST Act, the appeal must be filed within 3 months of the date the cancellation order was communicated. The Appellate Authority may condone a delay of up to 1 additional month on sufficient cause shown. No extension beyond this four-month total is permitted.

Can I revoke my cancelled GST registration?

Revocation via Form GST REG-21 is available within 90 days if the cancellation was initiated by the tax officer (not voluntarily by the taxpayer). If revocation is rejected via REG-05 or the 90-day window has passed, a formal appeal via Form GST APL-01 before the Appellate Authority is the appropriate next step.

Is GST registration cancellation upheld after appeal?

If the Appellate Authority upholds the cancellation, the registration remains cancelled. Options then include escalating to the GST Appellate Tribunal (Section 112), approaching the High Court under Article 226, or applying for fresh GST registration.

What documents are needed to file an appeal against GST cancellation?

Key documents include the original cancellation order, the completed Annexure to GST APL-01 (grounds of appeal), proof of filed GST returns and tax payments, business operation evidence (bank statements, invoices), and any relevant correspondence with the GST department.

What happens if the Appellate Authority rejects my GST appeal?

If rejected at the admission stage, you can re-file using the same Order ID before the limitation period expires. If rejected after a hearing on merits, the next appeal option is the GST Appellate Tribunal (GSTAT) under Section 112, and beyond that, the High Court under Article 226.