Introduction

Missteps in Singapore compliance can cost UK businesses up to S$5,000 (Singapore dollars) in penalties — and that's before the reputational damage that strains banking relationships and investor confidence.

A compliance audit for Singapore SMEs is an independent review of a company's financial records to verify accuracy and regulatory adherence. It sits under Singapore's Companies Act, with reporting obligations to both ACRA (Accounting and Corporate Regulatory Authority) and IRAS (Inland Revenue Authority of Singapore).

For UK businesses, this means running a compliance framework entirely separate from Companies House and HMRC. Total UK-Singapore trade in goods and services reached £26.7 billion in the four quarters to Q3 2025, driven in part by the UK-Singapore Free Trade Agreement signed in December 2020. As more UK SMEs expand into Singapore, understanding local audit requirements is no longer optional.

Key Takeaways

- Singapore compliance is governed primarily by the Companies Act 1967, with ACRA and IRAS as the two key regulatory bodies

- Financial filings must follow Singapore's own accounting standards (SFRS) in XBRL format — distinct from UK requirements

- Audit exemption is available to SMEs meeting two of three thresholds: revenue ≤S$10M, assets ≤S$10M, or employees ≤50

- UK businesses must manage dual compliance obligations simultaneously — both in the UK and Singapore

- Missing ACRA filing deadlines carries late penalties starting at S$300 — knowing the full audit timeline is non-negotiable

What Is a Compliance Audit for Singapore SMEs?

A compliance audit in Singapore is an independent examination of a company's financial statements, accounting records, and corporate filings. Its purpose is to verify accuracy under the Singapore Financial Reporting Standards (SFRS) and the Companies Act (Cap. 50).

The audit gives stakeholders, regulators, and investors verified assurance that a company's financials are free from material misstatements and meet local statutory requirements.

Statutory vs. Voluntary Audits

Singapore distinguishes between two types of audits:

- Statutory audit — legally required for companies that do not qualify for exemption under Sections 205B or 205C of the Companies Act

- Voluntary audit — chosen by exempt companies for credibility, investor confidence, or lending purposes

Both types follow the same SFRS standards. Under Singapore Standards on Auditing (SSA 700 Revised and SSA 705 Revised), auditors issue one of four possible opinions on the financial statements:

- Unqualified (Clean) Opinion — financial statements present a true and fair view

- Qualified Opinion — material misstatement or limitation, but not pervasive

- Adverse Opinion — material and pervasive misstatement

- Disclaimer of Opinion — inability to obtain sufficient appropriate evidence

Singapore Financial Reporting Frameworks

The Accounting Standards Council (ASC) prescribes three frameworks, and which one applies to your Singapore entity depends on how it's classified:

| Framework | Applicable To | Basis |

|---|---|---|

| SFRS(I) | Listed companies on SGX (mandatory) | Fully converged with IFRS |

| FRS | Non-listed companies (default) | Closely aligned with IFRS |

| SFRS for Small Entities | Eligible small private companies (optional) | Based on IFRS for SMEs |

Companies may use SFRS for Small Entities if they meet at least two of three criteria across two consecutive financial years: total annual revenue ≤S$10 million, total assets ≤S$10 million, and total employees ≤50.

Why Singapore Compliance Audits Matter for UK Businesses

The Dual Compliance Burden

UK companies with Singapore subsidiaries or branches face simultaneous obligations in two jurisdictions:

UK obligations:

- Companies House annual filings

- HMRC tax returns

- UK GAAP or IFRS financial reporting

Singapore obligations:

- ACRA annual returns (within 7 months of financial year-end for non-listed companies)

- IRAS Estimated Chargeable Income (ECI) filing (within 3 months of financial year-end)

- GST returns filed quarterly if turnover exceeds S$1 million

Missing a filing in either jurisdiction — or conflating one regime's rules with the other's — leads to penalties that compound quickly. The UK-Singapore Free Trade Agreement, which entered into force on 11 February 2021, has drawn more UK SMEs into Singapore, and full exposure to Singapore's compliance regime begins on day one.

Singapore's Regulatory Demands

ACRA requirements:

- Financial statements in XBRL format for most companies (mandatory from 1 May 2021)

- Appointment of ACRA-registered public accountants for statutory audits

- Maintenance of statutory records for minimum 5 years

IRAS requirements:

- ECI filing within 3 months of financial year-end

- Corporate Income Tax return (Form C or Form C-S for smaller companies) by 30 November each year

- GST registration and quarterly filing once turnover exceeds S$1 million

Financial Consequences of Non-Compliance

Singapore imposes specific penalty amounts for late or failed filings:

| Offence | Penalty |

|---|---|

| Late annual return filing (within 3 months) | S$300 |

| Late annual return filing (beyond 3 months) | S$600 |

| Late/non-filing of CIT return (composition) | Up to S$5,000 per offence |

| Non-filing for 2+ years | 2× tax assessed plus S$5,000 fine |

| Failure to maintain accounting records | Up to S$10,000 or 12 months imprisonment |

IRAS may impose composition amounts of up to S$5,000, and persistent non-compliance can lead to court summons or ACRA-initiated enforcement action.

How Singapore's Standards Differ from UK Norms

Those penalties matter most to UK owners who assume Singapore mirrors familiar UK processes. It doesn't. Four differences catch businesses out repeatedly:

| Area | UK Practice | Singapore Requirement |

|---|---|---|

| Financial year-end | Fixed to UK calendar | Chosen freely upon incorporation |

| Financial statement format | PDF submission to Companies House | XBRL format (mandatory for most companies) |

| Auditor qualifications | Any qualified UK accountant | Must be ACRA-registered public accountant |

| Accounting standards | UK GAAP or FRS 102 | Singapore Financial Reporting Standards (SFRS) |

How the Compliance Audit Process Works in Singapore

A Singapore SME audit spans several months and should start well before the financial year-end. It moves through three distinct phases: pre-audit preparation, auditor engagement and examination, and post-audit regulatory filing.

Step 1: Pre-Audit Preparation

Before the audit begins, UK-owned SMEs must organise comprehensive financial records:

Essential documents:

- General ledger and trial balance

- Bank reconciliations for all accounts

- Payroll records including CPF contribution records (for Singapore citizens and PRs)

- GST returns and supporting schedules

- Accounts receivable/payable ageing reports

- Fixed asset registers

- Board minutes and shareholder resolutions

Confirm your company's financial year-end date and identify which accounting standard applies — SFRS (full) or SFRS for Small Entities. Disorganised records are the leading cause of audit delays and inflated auditor fees.

Step 2: Engaging an ACRA-Registered Auditor and the Examination

Only public accountants registered with ACRA under the Accountants Act may conduct statutory audits in Singapore. PAs must practise within an ACRA-registered accounting entity. Requirements include ISCA membership and at least 2,500 hours of qualifying audit experience.

The auditor's role includes:

- Examining financial statements against SFRS requirements

- Testing transactions for accuracy and proper authorisation

- Reviewing internal controls and identifying weaknesses

- Assessing compliance with Companies Act provisions

- Issuing an audit opinion

The audit opinion has direct implications for the company's credibility with banks, investors, and government grant applications. An unqualified opinion signals robust financial controls; a qualified or adverse opinion raises red flags.

Step 3: Post-Audit Filing with ACRA and IRAS

After the audit, three key filings must be completed:

1. ACRA Annual Return (XBRL format):

ACRA requires most Singapore-incorporated companies to file financial statements in XBRL format. Companies use the BizFinx Preparation Tool to create Inline XBRL (iXBRL) files that are both human-readable and machine-readable. Two main filing formats exist:

- Full XBRL — approximately 210 data elements for most companies

- Simplified XBRL — approximately 120 elements for smaller companies

Exemptions apply to solvent Exempt Private Companies, dormant companies, and companies limited by guarantee.

2. IRAS ECI Filing:

Submit Estimated Chargeable Income within 3 months of financial year-end. An ECI filing waiver applies where annual revenue is S$5 million or below AND ECI is nil for the year of assessment.

3. Corporate Income Tax Return:

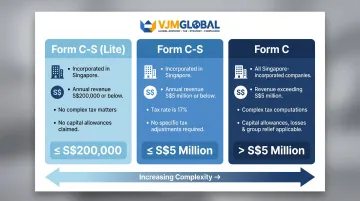

File Form C-S, Form C-S (Lite), or Form C by 30 November:

| Form | Qualifying Companies | Revenue Threshold |

|---|---|---|

| Form C-S (Lite) | Singapore-incorporated; no capital allowances, losses, or complex deductions | ≤S$200,000 |

| Form C-S | Singapore-incorporated, taxed at 17% only | ≤S$5 million |

| Form C | All companies not qualifying for C-S or C-S (Lite) | No limit |

Unlike the narrative accounts submitted to Companies House, XBRL requires structured, tagged data — plan for additional preparation time or engage a local accountant with BizFinx experience before your first filing deadline.

Key Compliance Areas UK Businesses Must Cover

Corporate and Accounting Compliance

Singapore's corporate compliance requirements differ in scope from equivalent UK Companies House obligations:

Singapore requirements:

- Annual return filing with ACRA within 7 months of financial year-end

- Financial statements prepared under SFRS (not UK GAAP or FRS 102)

- Auditor appointed within 3 months of incorporation

- Statutory records maintained for minimum 5 years (vs. 3 years in UK for some records)

- XBRL format for financial statement filing (not PDF)

UK requirements:

- Annual confirmation statement to Companies House

- Financial statements prepared under UK GAAP or IFRS

- Auditor appointed (if applicable)

- Records maintained for 3-6 years depending on document type

- PDF or paper filing accepted

Company Secretary and Corporate Governance

Section 171 of the Companies Act 1967 requires every company to appoint a resident company secretary within 6 months of incorporation. This is a distinct legal role from a UK company secretary, and UK businesses frequently overlook it — risking non-compliance from day one.

Key requirements for this role:

- Must be a natural person ordinarily resident in Singapore

- Cannot be the sole director of the company

- The office must not remain vacant for more than 6 months at any time

- Failure to appoint carries financial penalties under the Companies Act

Tax Compliance

Singapore taxes companies at a flat 17% rate of chargeable income, applying to both local and foreign companies. Three main tax obligations apply:

1. Corporate Income Tax with Start-Up Exemption:

New companies may qualify for the Start-Up Tax Exemption (SUTE) scheme:

- Eligibility: Incorporated in Singapore, tax resident, no more than 20 shareholders (at least one individual holding ≥10% ordinary shares)

- Exemption (first 3 consecutive Years of Assessment):

- 75% exemption on first S$100,000 of chargeable income

- 50% exemption on next S$100,000 of chargeable income

- Maximum exemption per YA: S$125,000

Property development and investment holding companies are excluded.

2. GST Registration and Filing:

Businesses must register for GST if taxable turnover exceeds S$1 million/gst-registration-deregistration/do-i-need-to-register-for-gst):

- Retrospective basis: more than S$1 million at the end of any calendar year

- Prospective basis: expected to exceed S$1 million in the next 12 months

Failure to register on time can result in backdated tax liabilities, fines of up to S$10,000, and a 10% penalty on tax due.

3. Transfer Pricing Documentation:

Under Section 34F of the Income Tax Act 1947, contemporaneous transfer pricing documentation is mandatory if:

- Gross revenue from trade or business exceeds S$10 million for the basis period; OR

- Related party transactions exceed S$15 million for the basis period

IRAS scrutinises cross-border transactions, and this applies directly to UK parent-Singapore subsidiary structures involving management fees, IP licensing, or intercompany services.

Employment and Data Protection

CPF Contributions:

Employers must make CPF contributions for employees who are Singapore citizens and permanent residents. CPF is not applicable to foreign workers on work permits, S Passes, or Employment Passes.

Fair Consideration Framework:

Before submitting Employment Pass or S Pass applications, employers must advertise job vacancies on the MyCareersFuture.gov.sg portal for at least 14 calendar days to ensure fair consideration of the local workforce.

Personal Data Protection Act (PDPA):

The PDPA imposes 11 key obligations on organisations handling personal data, including accountability, consent, notification, purpose limitation, accuracy, protection, retention limitation, transfer limitation, access and correction, data breach notification, and data portability.

UK GDPR experience helps, but Singapore's PDPA has distinct requirements — notably around data breach notification thresholds and consent mechanisms.

Common Mistakes and Audit Exemptions for UK-Owned Singapore SMEs

Understanding the SME Audit Exemption

Under Section 205C of the Companies Act 1967, a Singapore private company qualifies as a "small company" exempt from statutory audit if it meets at least two of three criteria for two consecutive financial years:

- Total annual revenue ≤S$10 million

- Total assets ≤S$10 million

- No more than 50 full-time employees

Comparison with UK audit exemption thresholds:

| Criterion | Singapore | UK |

|---|---|---|

| Turnover/Revenue | ≤S$10 million (~£5.8M) | ≤£10.2 million |

| Total Assets | ≤S$10 million (~£5.8M) | ≤£5.1 million |

| Employees | ≤50 | ≤50 |

Singapore's revenue threshold is significantly narrower than the UK's SME definition (up to 250 employees, turnover up to £36M for Companies Act purposes). UK businesses should not assume their UK "SME" status transfers to Singapore.

If the company is a parent or subsidiary, the entire group must also qualify as a "small group" on a consolidated basis using the same thresholds.

The Audit Exemption Misconception

The most common mistake UK businesses make is assuming audit exemption means no compliance obligations. This is false.

Audit-exempt companies still must:

- Prepare financial statements under SFRS

- File annual returns with ACRA within prescribed deadlines

- Meet all IRAS tax filing deadlines (ECI, Form C-S/Form C, GST returns if registered)

- Retain accounting records for not less than 5 years

Exemption only removes the mandatory external audit requirement, not the underlying reporting framework.

Additional Common Mistakes

1. Reactive rather than proactive compliance:

Waiting until the financial year-end to begin compliance preparations rather than building a year-round compliance calendar. This creates rushed filings, errors, and penalty risk.

2. Using UK-based accountants unfamiliar with Singapore requirements:

A UK-based accountant unfamiliar with SFRS and ACRA requirements will frequently produce errors, restatements, and regulator queries. Only ACRA-registered public accountants can conduct statutory audits in Singapore. UK businesses should engage Singapore-registered professionals with demonstrated cross-border experience in both jurisdictions.

Strategic Value Beyond Compliance

Beyond avoiding penalties, compliance audits build financial credibility with local banks, investors, and government agencies. For UK businesses in Singapore, voluntary audits — even when exempt — often pay off strategically, particularly when:

- Seeking bank financing or credit facilities

- Applying for government grants or incentives

- Preparing for equity fundraising

- Building investor confidence in governance

- Establishing credibility with local partners

Frequently Asked Questions

What qualifies as an SME in Singapore for audit purposes?

Singapore does not have a single universal "SME" definition, but for audit purposes, a company qualifies as a "small company" if it is a private company meeting at least two of three thresholds for two consecutive financial years: annual revenue ≤S$10M, total assets ≤S$10M, and no more than 50 full-time employees.

What are the key steps in an SME audit?

An SME audit follows three broad stages:

- Pre-audit preparation: Organising financial records and appointing an ACRA-registered auditor

- Audit examination: Reviewing financial statements, transactions, and internal controls

- Post-audit filing: Submitting audited statements to ACRA via XBRL and filing tax returns with IRAS

Is a UK company's Singapore subsidiary required to file annual returns with ACRA?

Yes. All Singapore-incorporated companies — including subsidiaries of UK parent companies — must file annual returns with ACRA within 7 months of the financial year-end (for non-listed companies). This obligation applies regardless of the parent company's filing requirements with Companies House in the UK.

What happens if an SME in Singapore misses its compliance filing deadline?

Late annual return filings attract penalties of S$300–S$600, while late or non-filing of corporate income tax returns can result in fines of up to S$5,000. Persistent non-compliance may trigger court summons or ACRA enforcement action, so maintaining a compliance calendar is strongly recommended.

Do audit-exempt SMEs in Singapore still need to maintain financial records?

Yes. Audit exemption does not remove the obligation to maintain accurate financial records. Companies must still prepare financial statements under SFRS, retain accounting records for at least five years, and meet all ACRA and IRAS filing requirements.

What accounting standards must Singapore SMEs follow?

Singapore companies follow the Singapore Financial Reporting Standards (SFRS), which are based on IFRS. Smaller companies may use the simplified SFRS for Small Entities. Both are governed by the Accounting Standards Council (ASC) and differ in scope and presentation from UK GAAP or FRS 102.