The good news: you don't need to relocate. UK business owners can incorporate an Irish company remotely, and the process is more straightforward than most expect. There are, however, a handful of legal requirements that are specific to UK nationals post-Brexit — and getting them wrong delays registration.

This guide walks through every step, from name reservation to ongoing compliance, with the exact rules that apply to UK directors in 2024.

Key Takeaways

- UK citizens can incorporate an Irish company entirely from a distance — no physical move required

- Post-Brexit, UK directors must appoint an EEA-resident director or obtain a Section 137 bond (€25,000) before filing

- The Private Company Limited by Shares (LTD) is the right structure for most UK entrepreneurs

- Ireland's 12.5% corporation tax rate on trading income compares with the UK's 25% main rate

- The first CRO annual return is due six months after incorporation — late filing triggers penalties and loss of audit exemption

Why UK Businesses Are Setting Up in Ireland Post-Brexit

Brexit created a hard dividing line for UK companies serving EU clients. Goods now require customs declarations. Services face regulatory divergence. Contracts previously governed by harmonised EU rules need revisiting. For businesses with meaningful EU revenue, trading through a UK entity has become measurably more expensive and complex.

Ireland resolves most of this friction in one move. An Irish-incorporated company operates inside the EU single market from day one.

The Numbers Behind the Trend

The financial services sector tells the story most clearly. According to EY's Brexit tracker, 36 financial services firms had announced intentions to relocate UK operations or staff to Dublin by December 2021, with approximately 1,200 UK-based employees relocated or expected to follow.

A subsequent Irish Times report found 135 firms relocating financial services activities from the UK to Dublin, out of 440 firms identified as moving from the UK to the EU overall.

These figures cover financial services specifically — comprehensive all-sector data is not publicly available — but the direction of travel is clear. Ireland captured the largest share of Brexit-driven EU relocations, and that trend extends well beyond finance.

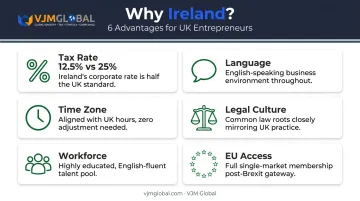

Why Ireland Works for UK Entrepreneurs

Several factors combine to make Ireland the default EU choice for UK-based founders:

- Tax rate: 12.5% on trading income, compared with the UK's 25% main rate for companies with profits over £250,000

- Language: English as the business language throughout, with legal and financial documentation in English

- Time zone: Same as the UK, meaning no adjustment to working hours or client communication

- Legal culture: Irish company law has strong historical parallels with UK practice, reducing the learning curve

- Workforce: A young, highly educated talent pool with strong tech and professional services sectors

- EU access: Full participation in the single market, including EU procurement frameworks and financial passporting

UK-Specific Requirements Before You Register

This is where UK entrepreneurs most often run into unexpected delays. Understanding these requirements before you approach the Companies Registration Office (CRO) saves significant time.

The Common Travel Area vs. Company Law

UK citizens retain the right to live and work in Ireland under the Common Travel Area (CTA) — no visa, no immigration barriers. This matters for individuals who plan to relocate personally. But it has no bearing on Irish company law.

The CTA is an immigration arrangement. The EEA-resident director rule is a statutory requirement under the Companies Act 2014. The two operate independently.

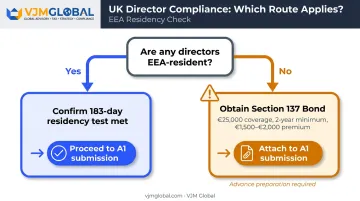

The EEA-Resident Director Requirement

Section 137 of the Companies Act 2014 states that at least one director must be resident in an EEA state. Since the UK left the EEA through Brexit, a UK-only board of directors no longer satisfies this requirement.

Residency under Section 141 is defined by day-count: 183 days or more in Ireland in a 12-month period, or 280 days or more across the current and preceding 12-month periods. Living in the UK — even with CTA rights — does not qualify as EEA residency.

The Section 137 Bond

If all your directors are UK (or otherwise non-EEA) residents, the company must obtain a Section 137 bond before the A1 incorporation form is submitted to the CRO. Key facts:

- Bond amount: €25,000 (set by statute)

- Duration: Minimum two years from the date of incorporation or director appointment

- Coverage: Specified fines and penalties under the Companies Act 2014 and the Taxes Consolidation Act 1997

- Commercial cost: The premium paid to an approved insurer typically runs €1,500–€2,000 including VAT — this is not an official CRO fee

This is the most common reason registrations stall — have the bond in place before you reach the A1 submission stage.

Company Secretary and Registered Address

Two additional requirements differ from UK practice:

- Company Secretary: Every Irish company must appoint a Company Secretary. If the company has only one director, the secretary must be a different person — this is a legal requirement, not optional. UK-based owners typically outsource this role to an Irish service provider.

- Registered Irish address: All Irish companies must maintain a verifiable physical Irish address on the CRO register. A PO Box does not qualify. Registered address services from Irish formation providers satisfy this requirement at low cost.

How to Set Up a Business in Ireland from the UK: Step-by-Step

Online registration through the CRO's CORE portal (Companies Online Registration Environment) typically processes in around three to five weeks based on current CRO workload — the CRO publishes daily processing updates on its website, so check current timelines before you plan.

Step 1: Check and Reserve Your Company Name

Search the CRO's CORE portal to confirm your preferred name is not already registered or deceptively similar to an existing Irish company. You can reserve the name for 28 days through CORE for €25.

Step 2: Prepare Constitutional Documents

For an LTD company, you'll need:

- Constitution — the single constitutional document for Irish LTD companies (replacing the older Memorandum and Articles of Association)

- A1 Form — the incorporation application, including details of all directors, the company secretary, registered address, and shareholder information

- Identity documents — directors must provide identity verification through the CRO's VIF (Verified Identity Form) process, which has been mandatory since April 2023 for directors without an Irish PPSN

Step 3: Arrange Your Bond or EEA Director

Complete this step before submitting your A1. If appointing an EEA-resident director, confirm they meet the day-count residency test under Section 141. If using the Section 137 bond route, source it from an approved insurer and have the bond documentation ready to attach to the A1.

Don't leave this step until last.

Step 4: Register with the CRO

Submit the completed A1 form and Constitution through CORE. The electronic filing fee is €50. On approval, the CRO issues a Certificate of Incorporation and a CRO registration number. Paper submissions are accepted but take longer.

Step 5: Register with Revenue and Open a Bank Account

After incorporation:

- Register for corporation tax with Irish Revenue Commissioners via the ROS (Revenue Online Service) portal or through eRegistration

- Assess your VAT position — current thresholds are €42,500 for services and €85,000 for goods (updated under Finance Act 2024). Businesses below these thresholds are not required to register immediately

- Open a business bank account capable of operating in EUR — many UK banks offer EUR business accounts, though an Irish bank often simplifies day-to-day local operations

Choosing the Right Business Structure

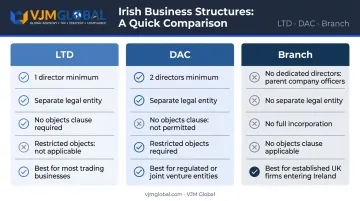

Most UK entrepreneurs will use one of three structures. Here's how to choose:

| Structure | Directors Required | Separate Legal Entity | Best For |

|---|---|---|---|

| LTD (Private Company Limited by Shares) | 1 minimum | Yes | Most trading businesses and subsidiaries |

| DAC (Designated Activity Company) | 2 minimum | Yes | Regulated activities, joint ventures, restricted-purpose entities |

| Branch Office | Parent company officers | No | Established UK firms testing the Irish market |

LTD vs. DAC

The LTD is the default for most UK entrepreneurs. It requires only one director, has no prescribed objects clause, and can be incorporated quickly. Limited liability is built in.

The DAC applies when business activities must be restricted to specific stated objects — regulated financial services, structured joint ventures, or entities where investors contractually require defined operational scope. The two-director minimum is also a practical factor when structuring the board.

Branch Office

A branch is not a separate Irish company. It is an extension of the existing UK entity registered in Ireland under Part 21 of the Companies Act 2014. This means:

- No separate Irish limited liability — the UK parent remains directly exposed

- Corporation tax treatment and filing obligations differ from an incorporated entity

- Suited to larger UK businesses wanting an Irish presence without full incorporation

For most UK entrepreneurs building a standalone EU presence, the LTD is the right answer. Those with regulatory constraints, restricted-activity requirements, or an existing UK entity to extend should assess the DAC or branch route before committing.

Tax and Ongoing Compliance Obligations

Irish Corporation Tax

Irish Revenue confirms two corporation tax rates: 12.5% on trading income and 25% on certain passive or non-trading income categories. For most UK entrepreneurs operating through an Irish trading company, the 12.5% rate applies.

Large multinational groups with consolidated global revenue exceeding €750 million are subject to the Pillar Two rules, which impose a minimum effective tax rate of 15%. This affects very few UK SMEs.

The Ireland-UK Double Taxation Agreement (DTA) covers corporation tax, income tax, and capital gains tax in both jurisdictions. A UK-resident director receiving salary or dividends from an Irish company will not pay tax on the same income in both countries. Credit mechanisms prevent double taxation, provided the treaty conditions are correctly applied.

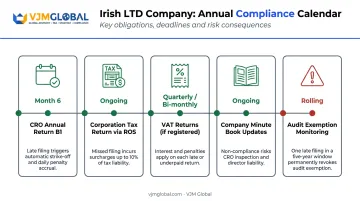

Annual Compliance Calendar

Running an Irish LTD creates obligations that run alongside (not instead of) any UK obligations you retain:

- CRO Annual Return (Form B1): First return is due six months after incorporation. Late filing triggers a €100 penalty from the day after the deadline, with additional daily charges potentially applying

- Audit exemption: From 16 July 2025, audit exemption is lost if an annual return is filed late more than once in any five-year period, a significant financial consequence for smaller companies

- Corporation tax return: Filed with Irish Revenue via ROS

- VAT returns: Quarterly or bi-monthly if VAT-registered

- Company minute book: Board decisions must be recorded. Irish company law requires this, and it's often overlooked by UK-based directors managing remotely

Common Compliance Mistakes

UK entrepreneurs frequently encounter these problems after incorporation:

- Annual Return Date: The six-month first return deadline catches many founders off guard

- UK accounting assumptions: Irish Revenue requirements and CRO financial statement formats follow specific rules that don't mirror UK practice

- Registered office gaps: Using a formation agent's address without confirming ongoing service arrangements creates compliance risk

- No company minute book: Easy to skip, but it surfaces as a problem during audit and due diligence

Managing Irish compliance alongside UK obligations is where specialist cross-border accounting support pays for itself. Working with advisors experienced in dual-entity accounting, tax treaty application, and cross-border compliance reduces the risk of costly filing errors on either side of the Irish Sea.

Frequently Asked Questions

Can a UK citizen set up a business in Ireland?

Yes. UK citizens face no visa or immigration barrier under the Common Travel Area. However, since the UK left the EEA, UK-resident directors must either appoint an EEA-resident director to the board or obtain a Section 137 bond before the company can be incorporated.

Do Ireland and the UK have a double taxation agreement?

Yes. The Ireland-UK DTA covers corporation tax, income tax, and capital gains tax in both countries. A UK resident directing an Irish company will not pay tax on the same income in both jurisdictions. The treaty provides credit mechanisms to prevent double taxation, provided the relevant conditions are met.

What is the 3-year residency rule in Ireland?

This rule applies to Irish citizenship by naturalisation, not to company registration. There is no minimum residency requirement for UK entrepreneurs incorporating an Irish company. The standard naturalisation route requires five years of reckonable residence, but that is irrelevant to business setup.

Do I need a bond or an EEA-resident director to incorporate an Irish company from the UK?

Yes, one or the other is required. Section 137 of the Companies Act 2014 requires at least one director to be resident in an EEA state. If your board consists entirely of UK (or other non-EEA) residents, a €25,000 Section 137 bond from an approved insurer must be in place before the A1 form is submitted.

How long does it take to register a company in Ireland?

Processing times vary — the CRO publishes daily updates on its website showing which submission dates are currently being processed. Budget several weeks for the full process. Delays are almost always caused by incomplete documentation or failure to arrange the Section 137 bond before submission.