That simplicity, however, conceals nuances that matter for foreign investors. Getting tax residency wrong, missing filing deadlines, or overlooking applicable exemption schemes can be costly. This guide covers Singapore's CIT rate, taxable income categories, residency rules, exemption schemes, filing obligations, and the new global minimum tax rules — with enough detail to orient any company entering the Singapore market.

Key Takeaways

- Singapore taxes company profits at a flat 17% rate on chargeable income — applicable to both resident and non-resident companies

- The one-tier tax system means dividends flow to shareholders tax-free once corporate tax is paid

- Start-up companies can claim up to SGD 125,000 in annual tax exemptions under the Start-Up Tax Exemption scheme

- Tax residency hinges on where control and management is exercised, not where the company is incorporated

- From 2025, multinationals with group revenues above EUR 750 million are subject to a 15% global minimum tax in Singapore

Singapore's Corporate Income Tax Rate and How the System Works

The Flat 17% Rate

IRAS confirms that Singapore applies a flat 17% CIT rate to chargeable income for both local and foreign companies. Chargeable income is not the same as revenue — it is profit after allowable deductions such as business expenses, capital allowances, and applicable exemptions.

A company turning over SGD 2 million but incurring SGD 1.5 million in allowable expenses has chargeable income of SGD 500,000, not SGD 2 million. The 17% applies to that SGD 500,000 figure.

The One-Tier System: No Double Taxation

Singapore operates a single-tier corporate tax system. Once a company pays CIT on its profits, those profits are effectively taxed once. Dividends distributed to shareholders — whether individuals or corporate entities — are exempt from further taxation in the shareholders' hands.

For foreign investors, this is a significant structural advantage: profits extracted from Singapore don't attract an additional layer of tax at the shareholder level.

Preceding-Year Basis of Assessment

CIT is assessed on a preceding-year basis. Income earned during financial year 2024 is assessed in Year of Assessment (YA) 2025, meaning the filing deadline falls in the year after your accounts close.

Example: A company with a financial year ending 31 December 2024 reports profits for that period. IRAS assesses those profits in YA 2025, and the tax return is due by 30 November 2025. A company with a March year-end (ending 31 March 2024) files under YA 2025 as well — because YA is determined by when the financial year ends, not calendar year.

YA 2026 CIT Rebate

For YA 2026, IRAS has announced an enhanced rebate:

- 50% rebate on corporate tax payable, capped at SGD 40,000 total benefit

- SGD 2,000 cash grant for active companies with CPF contributions to at least one local employee (excluding shareholder-directors) during calendar year 2025

These are Budget-linked measures, not permanent features of the tax code.

Capital Gains and Section 10L

Singapore generally does not tax capital gains — gains from selling fixed assets, for instance, are not taxable. However, from 1 January 2024, Section 10L introduced a targeted exception. Key points to understand:

- Gains from disposing of certain foreign assets received in Singapore may be taxable

- The exception applies where the entity lacks adequate economic substance in Singapore

- Adequate substance typically requires local staff, management decisions made in Singapore, and operating expenditure incurred here

- Holding companies with no genuine Singapore operations are most exposed to this rule

What Income Is Taxable Under Singapore's Corporate Income Tax

Singapore taxes income on a territorial and remittance basis:

- Singapore-sourced income is taxed when it arises

- Foreign-sourced income is taxed when it is received in Singapore (remitted, transmitted, or brought in), unless specifically exempted

Main Categories of Taxable Income

Within this framework, the following types of income are subject to corporate tax:

- Gains or profits from any trade or business

- Investment income — dividends, interest, and rental

- Royalties, premiums, and other profits from property

- Other gains of an income nature

Not all foreign income is taxable, however. Singapore tax resident companies can claim exemption on specific categories of foreign income received locally.

Exempt Foreign-Sourced Income

Singapore tax resident companies can claim exemption on three categories of foreign income received in Singapore, provided qualifying conditions are met:

- Foreign-sourced dividends

- Foreign branch profits

- Foreign-sourced service income

The key condition: the income must have been subject to tax in the foreign jurisdiction at a headline rate of at least 15%, and the Comptroller must be satisfied the exemption is beneficial. The IRAS foreign income page sets out the full qualifying conditions, including specific rules around the "subject to tax" requirement.

What Is Generally Not Taxable

- Capital gains on disposal of shares or assets (subject to Section 10L anti-avoidance rules, covered in the section on capital gains)

- Dividends received from Singapore-resident companies under the one-tier system

Tax Residency for Companies in Singapore

The Control and Management Test

IRAS determines a company's tax residency based on where its "control and management" is exercised — specifically, where the board of directors holds strategic meetings and makes key decisions on company policy and strategy. Incorporation jurisdiction is irrelevant to this test.

Practical consequences:

- A Singapore-incorporated company whose directors meet and make decisions from overseas may be treated as a non-resident

- A foreign-incorporated company whose board meets and makes decisions from Singapore could qualify as a Singapore tax resident

- A Singapore branch of a foreign company is generally treated as a non-resident, as it is controlled by its foreign parent

Why Residency Status Matters

Tax residency unlocks benefits that non-residents cannot access:

- Start-Up Tax Exemption (SUTE) and Partial Tax Exemption (PTE) schemes

- Double Tax Agreement (DTA) relief — Singapore has DTAs with around 100 jurisdictions per IRAS's DTA list, covering withholding tax reductions and tie-breaker residency rules

- Foreign-sourced income exemptions under Section 13(8)

These exemptions and treaty protections are only available to resident companies, which makes the control and management question consequential from day one. For businesses considering Singapore as a regional holding or treasury centre, retroactively relocating board decision-making is operationally complex and may attract IRAS scrutiny — getting the structure right at incorporation is significantly easier than correcting it later.

Tax Exemption Schemes and Incentives for Companies

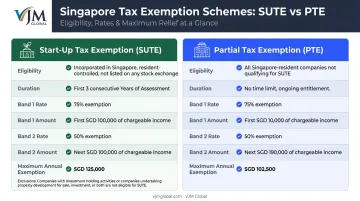

Start-Up Tax Exemption (SUTE) vs. Partial Tax Exemption (PTE)

Two core schemes reduce effective tax rates for most Singapore companies. The table below summarises the key differences:

| Feature | SUTE | PTE |

|---|---|---|

| Who qualifies | New qualifying companies | All companies not claiming SUTE |

| Duration | First 3 consecutive YAs | Every YA, no time limit |

| Exemption — Band 1 | 75% on first SGD 100,000 | 75% on first SGD 10,000 |

| Exemption — Band 2 | 50% on next SGD 100,000 | 50% on next SGD 190,000 |

| Maximum exemption | SGD 125,000 per YA | SGD 102,500 per YA |

| Exclusions | Investment holding companies; property developers | None specified |

SUTE in practice: A qualifying startup with SGD 200,000 of chargeable income in its first YA would receive SGD 125,000 in exemptions, leaving SGD 75,000 taxable — an effective rate well below 17% in those early years.

Other Tax Incentives Worth Knowing

Beyond SUTE and PTE, Singapore offers several targeted schemes for specific activities and sectors:

- Double Tax Deduction for Internationalisation (DTDi): 200% deduction on eligible expenses for overseas market expansion, covering qualifying expenditure through 31 December 2030

- Enterprise Innovation Scheme (EIS): 400% tax deductions on up to SGD 400,000 of qualifying expenditure per year (YA2024–YA2028) for R&D in Singapore, IP registration, and qualifying training

- Financial Sector Incentive (FSI): Concessionary tax rates of 5%–13.5% for licensed financial institutions on qualifying income

- Maritime Sector Incentive (MSI): Tax exemptions or concessionary treatment for qualifying shipping and maritime activities

Foreign companies and multinationals with cross-border operations — including those managing entities across Singapore and India — should assess scheme eligibility early. VJM Global's international tax advisory team regularly helps clients map incentive frameworks across jurisdictions to avoid missed deductions and compliance gaps.

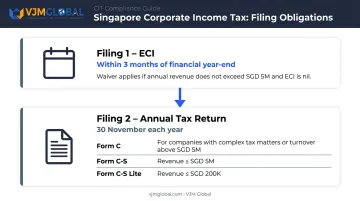

Corporate Income Tax Filing Obligations

Every Singapore company must meet two annual filing obligations with IRAS — the ECI filing and the annual tax return — regardless of whether it made profits or losses.

Two Required Filings

1. Estimated Chargeable Income (ECI)

- Filed within 3 months from the end of the company's financial year

- Declares the company's estimated taxable profit for that year

- Waiver available if annual revenue is SGD 5 million or below AND ECI is nil

2. Annual Corporate Income Tax Return

- Deadline: 30 November each year

- Three form options depending on company size:

| Form | Who Files It |

|---|---|

| Form C | Larger or more complex companies |

| Form C-S | Singapore-incorporated companies with annual revenue ≤ SGD 5 million meeting qualifying conditions |

| Form C-S (Lite) | Eligible companies with annual revenue ≤ SGD 200,000 |

All companies must file — even those in a loss position or with no income.

Penalties for Non-Compliance

Missing filing deadlines carries real consequences. Late or non-filing can result in:

- An estimated Notice of Assessment issued by IRAS

- A composition amount of up to SGD 5,000

- Court action, with conviction carrying fines of up to SGD 5,000

Beyond penalties, companies must also retain proper financial records and accounts for at least five years from the relevant Year of Assessment (YA) — a requirement that applies whether or not any issues arise.

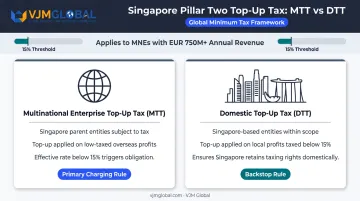

BEPS 2.0 and the Global Minimum Tax for Large MNEs

From 1 January 2025, Singapore implemented the OECD/G20 Pillar Two GloBE rules through the Multinational Enterprise (Minimum Tax) Act 2024. These rules apply to MNE groups with annual consolidated revenues of EUR 750 million or more in at least two of the four preceding fiscal years.

Two Components

Singapore's Pillar Two framework introduces two distinct top-up tax mechanisms:

- Multinational Enterprise Top-Up Tax (MTT): Singapore's Income Inclusion Rule. Singapore parent entities pay top-up tax on low-taxed profits earned by overseas constituent entities where the effective tax rate in those jurisdictions falls below 15%.

- Domestic Top-Up Tax (DTT): A qualified domestic minimum top-up tax that applies to constituent entities located in Singapore where the effective rate falls below 15% — letting Singapore collect the top-up tax before a foreign jurisdiction does.

Singapore has not adopted the Undertaxed Profits Rule (UTPR) at this stage; that remains under review.

For in-scope MNEs, Singapore's standard corporate tax rate of 17% generally keeps most Singapore entities above the 15% threshold. However, the DTT can still apply where specific incentives or deductions reduce the effective rate below that floor.

Frequently Asked Questions

How much is the corporate tax in Singapore?

Singapore levies a flat 17% rate on chargeable income for both resident and non-resident companies. Effective rates are often lower once tax exemptions (SUTE or PTE) and available rebates are applied.

What is the difference between income tax and corporate tax?

Corporate income tax applies specifically to a company's chargeable profits, while personal income tax applies to individual earnings. In Singapore, individuals are taxed at progressive rates up to 24%; companies pay a flat 17% CIT regardless of profit size.

Who is required to pay corporate income tax in Singapore?

Any company earning income sourced in Singapore is liable for CIT at 17%. Resident companies are also taxed on foreign-sourced income when it is received in Singapore. There is no minimum revenue threshold for liability.

What is the deadline for filing corporate income tax returns in Singapore?

The ECI must be filed within three months after the company's financial year-end. The annual Corporate Income Tax Return (Form C-S, C-S Lite, or C) must be filed by 30 November each year. Form C-S and C-S Lite apply to smaller companies with simpler tax profiles; Form C is for all others. All forms are due by 30 November each year.

Are dividends taxable under Singapore's corporate income tax?

Under Singapore's one-tier system, dividends paid by Singapore-resident companies are exempt from tax in shareholders' hands. The company pays CIT once on its profits, and no further tax is charged when those profits are distributed.

What is the Start-Up Tax Exemption scheme in Singapore?

The SUTE scheme gives qualifying new companies a 75% exemption on the first SGD 100,000 and a 50% exemption on the next SGD 100,000 of chargeable income for their first three consecutive Years of Assessment. Investment holding companies and property developers are excluded.