Introduction

If you're running a Dubai operation from Singapore, the UAE's federal corporate tax regime now applies to you — and many businesses are still catching up. Since Federal Decree-Law No. 47 of 2022 took effect in June 2023, Singapore businesses with mainland subsidiaries, free zone entities, or permanent establishments in the UAE face mandatory filing obligations they cannot afford to overlook.

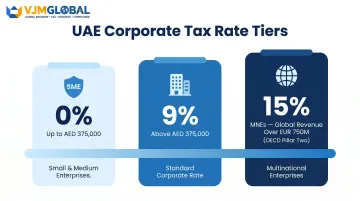

Many Singapore business owners wrongly assume their UAE entities are automatically exempt, or that Singapore's tax framework covers their Dubai operations. It doesn't. UAE corporate tax applies at 0% on taxable income up to AED 375,000 and 9% above that threshold. Filing is mandatory even if you owe zero tax.

This guide walks Singapore businesses through who is liable, the step-by-step filing process on the EmaraTax portal, essential documents, critical deadlines, and common mistakes that trigger penalties from AED 10,000 upward.

Key Takeaways

- UAE corporate tax became effective for financial years starting on or after 1 June 2023, with rates of 0% up to AED 375,000 and 9% above

- Singapore businesses with any UAE presence — subsidiary, branch, or free zone entity — must register for UAE CT and file returns electronically

- Returns must be filed via EmaraTax within 9 months of financial year-end, including nil-income returns

- The UAE-Singapore Double Tax Agreement reduces double taxation but does not eliminate your UAE filing obligation

- Late registration carries an AED 10,000 penalty; late filing incurs AED 500/month, rising to AED 1,000 after the first year

What Is UAE Corporate Tax and Who Does It Apply To?

UAE corporate tax is a federal direct tax levied on the net profits of businesses operating in the UAE. Introduced under Federal Decree-Law No. 47 of 2022 and administered by the Federal Tax Authority (FTA), it became effective for financial years starting on or after 1 June 2023.

The tax applies at three rates:

- 0%: Taxable income up to AED 375,000 (designed to protect SMEs)

- 9%: Taxable income above AED 375,000

- 15%: Large multinationals meeting OECD Pillar Two thresholds (consolidated global revenue exceeding EUR 750 million)

Dubai's 9% rate compares favorably to Singapore's 17% corporate tax rate — but compliance is mandatory regardless of which bracket applies to your business.

Who must register and comply:

- UAE-incorporated companies and juridical persons (legal entities such as partnerships and foundations) effectively managed in the UAE

- Foreign entities with a Permanent Establishment (PE) in the UAE

- Free zone entities (who may qualify for 0% on Qualifying Income if specific FTA conditions are met)

Entities automatically exempt from UAE corporate tax:

- Government entities and government-controlled entities

- Qualifying public benefit entities

- Certain qualifying investment funds

- Extractive businesses subject to Emirate-level taxation

- Public or private pension and social security funds

Most commercial entities operating in the UAE do not fall under any exemption category. Singapore businesses should confirm their status early — before registration deadlines apply.

Do Singapore Businesses Need to File UAE Corporate Tax?

Permanent Establishment Creates Filing Obligations

A Singapore company conducting business in the UAE on an ongoing basis may be treated as having a Permanent Establishment (PE), triggering CT registration and filing obligations even without a formal UAE legal entity.

PE exists when you have:

- Fixed Place PE: Any branch, office, factory, workshop, or construction site lasting more than 6 months through which business is conducted

- Agency PE: A dependent agent who habitually concludes contracts on your behalf in the UAE

Even a senior employee based in Dubai negotiating contracts can create PE status for your Singapore parent company.

Free Zone Entities Are NOT Automatically Exempt

Many Singapore businesses establish UAE free zone companies believing they're fully exempt from tax. This is incorrect.

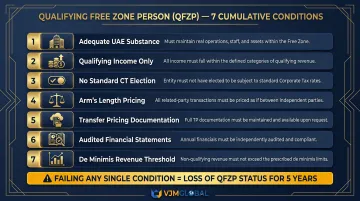

Free zone entities are within the scope of UAE CT as Taxable Persons and must register and file. Qualifying Free Zone Persons (QFZPs) can benefit from a 0% rate on Qualifying Income, but only if they meet all seven cumulative conditions:

- Maintain adequate substance in the UAE (employees, assets, core income-generating activities in the Free Zone)

- Derive only Qualifying Income (as defined by Ministerial Decision)

- Not elect to be subject to standard CT rates

- Comply with the Arm's Length Principle for related-party transactions

- Maintain transfer pricing documentation

- Prepare and maintain audited financial statements

- Ensure non-qualifying revenue doesn't exceed the de minimis threshold (5% of total revenue or AED 5 million)

Failing any single condition means losing QFZP status for that tax period and the subsequent four tax periods — a five-year penalty.

Mainland UAE Subsidiaries Must File and Pay

The free zone rules only apply to free zone entities. A Singapore company with a UAE LLC or mainland subsidiary operates under a different set of rules entirely.

A Singapore company with a UAE LLC or mainland subsidiary must register for UAE CT, file returns, and pay 9% tax on profits above AED 375,000. There is no exemption simply because the parent is based in Singapore.

How the UAE-Singapore Double Tax Agreement Fits In

The UAE-Singapore DTA, in force since 1996, can prevent double taxation by allowing Singapore to grant foreign tax credits for UAE CT paid. It does not, however, remove your obligation to file a UAE CT return.

Under Article 66 of the CT Law, the DTA takes precedence only where an inconsistency exists. One practical example: the DTA sets a 9-month construction PE threshold, while the CT Law uses 6 months. Once a PE or nexus exists under either definition, self-assessment filing remains mandatory under Articles 48 and 53.

Nil Returns Are Still Mandatory

Even if your taxable income falls in the 0% bracket, you must register and file a nil return. Missing the registration deadline is a separate offence — the FTA imposes an AED 10,000 fine.

Step-by-Step: How to File UAE Corporate Tax as a Singapore Business

UAE corporate tax operates on a self-assessment basis via the EmaraTax portal. Singapore businesses should begin preparing well before their financial year ends—not in the final weeks before the 9-month deadline.

Step 1: Register for UAE Corporate Tax

Every taxable person must electronically register with the FTA to obtain a Corporate Tax Registration Number (CT TRN), which is separate from a VAT TRN.

Registration process:

- Access the EmaraTax portal using UAEPass or email/phone account

- Select "Register for Corporate Tax" (even if you already have a VAT TRN)

- Provide trade licence details, entity information, and financial year dates

- Processing takes around 20 business days

Registration deadlines vary by entity type:

- UAE entity established before 1 March 2024: deadline based on month of earliest licence issuance

- UAE entity established on/after 1 March 2024: within 3 months of incorporation

- Non-resident with PE established before 1 March 2024: 9 months from PE establishment

- Non-resident with PE established on/after 1 March 2024: 6 months from PE establishment

Singapore businesses using a UAE-based tax agent can authorise the agent on the portal to handle registration and filing.

Step 2: Determine Your Tax Period and Taxable Income

Your tax period is your entity's financial year (typically 12 months). Taxable income starts from accounting income—net profit/loss before tax per IFRS-compliant financial statements—and then requires specific adjustments:

Required adjustments:

- Add back non-deductible expenses

- Exclude exempt income

- Apply reliefs such as carried-forward losses

- Make transfer pricing adjustments for intercompany transactions

Singapore parent company recharges and intercompany transactions require arm's length pricing adjustments and supporting documentation. Penalties for non-compliance can be substantial, so this area warrants early attention before preparing the return.

Step 3: Prepare Financial Statements and Supporting Records

Accounting standards requirement:

- Financial statements must be prepared under IFRS (International Financial Reporting Standards)

- Entities with revenue not exceeding AED 50 million may use IFRS for SMEs

Audit requirements:

- Audit mandatory if revenue exceeds AED 50 million during the tax period

- Audit mandatory for all Qualifying Free Zone Persons regardless of revenue

- Audit must be conducted by a UAE-licensed auditor

Small Business Relief:

- Entities with revenue of AED 3 million or less may elect Small Business Relief, treating taxable income as zero

- Available for tax periods ending on or before 31 December 2026

- Not available to QFZPs or financial institutions

Singapore businesses often use accounting systems not aligned with UAE requirements. Engaging a UAE-registered accountant or advisory firm well ahead of the deadline avoids last-minute gaps and reconciliation issues.

Step 4: Complete and Submit the CT Return via EmaraTax

The CT return is filed electronically on the EmaraTax portal no later than 9 months from the end of the tax period. For example, a 31 December year-end means a 30 September filing deadline.

Key return sections include:

- Income adjustments and reconciliation

- Exempt income declarations

- Transfer pricing disclosures

- Any elections made (e.g., Small Business Relief, tax group treatment)

Only one return is required per tax period regardless of the number of UAE entities (unless part of a tax group).

Step 5: Pay Any UAE CT Due

UAE CT payment is due on the same date as the return submission—within 9 months from financial year-end. Payment is made via the EmaraTax portal.

Accepted payment methods:

- GIBAN (bank transfer): UAE Funds Transfer System (beneficiary setup required in payer's bank)

- MagnatiPay: Accepts Visa or Mastercard prepaid, debit, or credit cards

Note: eDirham is no longer accepted as a payment method.

There is no separate advance payment or instalment system currently. Payment and filing fall on the same deadline date.

Step 6: Retain Records for Seven Years

All financial records must be retained for a minimum of 7 years from the end of the relevant tax period, as required under Article 56 of the Corporate Tax Law.

Required records include:

- Financial statements and general ledger

- Contracts, invoices, and bank statements

- Transfer pricing documentation

- Supporting schedules and reconciliations

Singapore businesses holding records in Singapore-based systems must ensure UAE-accessible copies are maintained. VJM Global's accounting and compliance teams can help Singapore businesses structure their record-keeping systems to meet both UAE and Singapore regulatory requirements.

Key Documents and Deadlines Singapore Businesses Must Know

Essential Documents for UAE CT Filing

- CT Registration Certificate (CT TRN)

- IFRS-compliant financial statements (audited if revenue exceeds AED 50 million)

- General ledger and trial balance

- Bank statements for all UAE business accounts

- Revenue and expense records (invoices, contracts, payroll)

- Fixed asset register with depreciation schedules

- VAT records (if VAT-registered)

- Transfer pricing documentation for Singapore-Dubai intercompany transactions

Critical Deadlines

| Obligation | Deadline |

|---|---|

| CT registration | As soon as entity becomes taxable (see Step 1 for specific timelines) |

| CT return filing | Within 9 months of financial year-end |

| CT payment | Same date as return filing |

| Record retention | 7 years from end of tax period |

Beyond the standard filing deadlines, transfer pricing adds a separate documentation layer that catches many Singapore businesses off guard.

Transfer Pricing Documentation Requirements

Transactions between a Singapore parent and UAE subsidiary must be at arm's length and documented. The UAE CT Law and OECD guidelines both apply.

Documentation thresholds:

| Document Type | Threshold |

|---|---|

| Transfer Pricing Disclosure Form | All taxable persons with related-party transactions above materiality threshold |

| Local File | Entity revenue ≥ AED 200 million |

| Master File | Entity revenue ≥ AED 200 million OR part of MNE group with consolidated revenue ≥ AED 3.15 billion |

| Country-by-Country Report | MNE group consolidated revenue ≥ AED 3.15 billion |

Documentation must be provided within 30 days of an FTA request. Singapore businesses often underestimate this exposure: management fees, royalties, and intercompany loans each require separate arm's length pricing support.

Common Mistakes Singapore Businesses Make When Filing UAE CT

Assuming Free Zone Status Equals Automatic Exemption

Many Singapore businesses set up UAE free zones specifically to avoid tax, but fail to understand that QFZP status requires meeting strict ongoing conditions.

Qualifying Income definition:

- Income from transactions with other Free Zone Persons

- Income from Qualifying Activities (manufacturing, trading qualifying commodities, holding shares, ship ownership, reinsurance, fund management, headquarter services to related parties, aircraft financing, logistics in Designated Zones)

- Ownership or exploitation of Qualifying Intellectual Property

Excluded from Qualifying Income (taxed at 9%):

- Income from a foreign or domestic Permanent Establishment

- Income from immovable property (with limited exceptions)

- Transactions with natural persons (with exceptions)

- Banking and insurance activities (except reinsurance)

Losing QFZP status retroactively triggers CT liabilities going back five years. Maintaining adequate substance in the Free Zone—employees, assets, and core income-generating activities physically on-site—is what keeps that status intact.

Missing the Registration Deadline or Conflating VAT TRN with CT TRN

Singapore businesses already VAT-registered in the UAE often assume they are also CT-registered. These are entirely separate obligations with separate registration numbers and separate deadlines.

Two facts to keep clear:

- Separate registration required: Holding a VAT TRN does not constitute CT registration — you must register independently on the EmaraTax portal to obtain a CT TRN

- Penalty for non-compliance: Failing to register for CT carries an AED 10,000 penalty, regardless of your VAT status

Underestimating Intercompany Complexity

Management service agreements, IP licences, and shareholder loans between a Singapore parent and Dubai entity must be documented at arm's length prices for UAE CT purposes. Without this, you face both a CT underpayment risk and an audit flag.

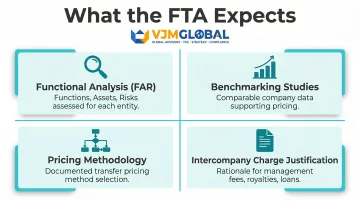

The FTA expects transfer pricing documentation aligned with OECD principles, including:

- Functional analysis (FAR: Functions performed, Assets employed, Risks assumed)

- Benchmarking studies using comparable companies

- Documentation of pricing methodology

- Justification of intercompany charges

Preparing this documentation before filing — not after receiving an FTA query — is the difference between a clean audit response and a 30-day scramble.

Frequently Asked Questions

Are corporate tax returns required to be filed in the UAE?

Yes. All taxable persons, including free zone entities, must file a UAE CT return for each tax period within 9 months of financial year-end. Even if your taxable income falls in the 0% bracket, filing a nil return is mandatory.

How do you file corporate tax in Dubai?

UAE CT is filed electronically via the FTA's EmaraTax portal. Businesses must first register to obtain a CT TRN, prepare IFRS-based financial statements, complete the return online, and submit with any tax payment due—all within 9 months of financial year-end.

Are there corporate taxes in Dubai?

Yes. The UAE (including Dubai) introduced federal corporate tax effective 1 June 2023. The rate is 0% on taxable income up to AED 375,000 and 9% above that threshold. Dubai itself does not levy a separate city-level tax.

Do Singapore companies need to register for UAE corporate tax?

Yes. Any Singapore company with a UAE subsidiary, branch, free zone entity, or Permanent Establishment in the UAE must register for UAE CT with the FTA. Failure to register carries a AED 10,000 penalty regardless of whether any tax is ultimately owed.

How does the UAE-Singapore Double Tax Agreement affect CT filing?

The UAE and Singapore have a Double Tax Agreement that can prevent the same income from being taxed in both jurisdictions. The DTA does not eliminate the UAE CT filing obligation. Singapore businesses must still file a UAE CT return and can claim a foreign tax credit in Singapore for any UAE CT paid.

What are the penalties for missing the UAE corporate tax filing deadline?

Key penalties under Cabinet Decision No. 75 of 2023 include:

- Late filing: AED 500/month for year one, rising to AED 1,000/month after that

- Failure to register: AED 10,000 one-time penalty

- Late payment: 14% per annum interest, calculated monthly

Final word: UAE corporate tax carries real consequences for Singapore businesses that miss registration, filing, or payment deadlines. Whether you're managing a mainland subsidiary, assessing QFZP status in a free zone, or determining PE exposure, the stakes are too high to navigate alone. VJM Global's international tax specialists work across UAE and Singapore obligations—handling return preparation, FTA registration, and cross-border documentation so nothing falls through the cracks.