Introduction

Most GST compliance errors don't start at the filing stage — they start in the books. For GST-registered businesses in Singapore, every sale and purchase creates specific accounting obligations, and many finance teams struggle with translating those everyday transactions into the double-entry records that the Inland Revenue Authority of Singapore (IRAS) requires. Get the entries wrong, and errors ripple through every line of your quarterly GST F5 return.

GST accounting entries are the journal records that capture output tax collected from customers and input tax paid to suppliers. These entries feed into two dedicated control accounts in your general ledger: a GST Output Tax liability account and a GST Input Tax asset account. IRAS expects both accounts to reconcile perfectly with the figures in your F5 return.

Misclassify a transaction, fail to separate tax from revenue, or apply the wrong accounting basis, and you've created both a compliance gap and a potential audit trigger.

This guide walks business owners, finance teams, and foreign companies operating in Singapore through the full picture: how GST flows through the books, how to structure journal entries for standard sales and purchases, and how to handle trickier scenarios like mixed supplies, bad debt relief, and the reverse charge. Accurate bookkeeping is the first line of defense against IRAS compliance issues — and this guide shows you exactly how to build it.

Key Takeaways

- Singapore GST is currently 9% on most taxable supplies; businesses collect output tax on sales and claim input tax on qualifying purchases

- Every GST transaction requires a double-entry journal — output tax on sales creates a liability, input tax on purchases creates a recoverable asset

- At period-end, net output tax minus input tax determines whether you pay IRAS or claim a refund

- Special situations like customer accounting, reverse charge, credit notes, and imports each require distinct journal treatments

- Clean records are non-negotiable — every GST F5 return figure must trace back to a source document

What Are GST Accounting Entries in Singapore?

GST accounting entries are the systematic recording of GST-inclusive transactions in your general ledger, using two core control accounts:

- GST Output Tax (liability account) — tax collected from customers

- GST Input Tax (asset account) — tax paid to suppliers

These entries achieve one outcome: ensuring that the net GST payable or refundable is accurately computed at the end of each accounting period, and that every figure in the GST F5 return can be reconciled directly to the books.

Why GST Entries Differ from General Bookkeeping

Recording a $1,090 sale isn't just about crediting revenue. GST entries require:

- Separating the tax component ($90) from the transaction value ($1,000)

- Posting the tax to a dedicated GST control account (not revenue)

- Maintaining records that allow IRAS to trace every dollar reported in Box 6 (output tax) or Box 7 (input tax) back to source invoices

Most classification errors happen at step two. IRAS requires businesses to maintain accounting records for at least 5 years/basics-of-gst/invoicing-price-display-and-record-keeping/keeping-records), including general ledgers, a GST account summarising output and input tax, and sale/purchase listings. These records must separately identify output tax and input tax — IRAS treats this as a structural requirement.

The practical risk: if your chart of accounts treats GST as revenue or expense rather than as liability and asset accounts, your entire F5 return will be mathematically incorrect.

How GST Output Tax and Input Tax Are Recorded

Recording Output Tax on Sales

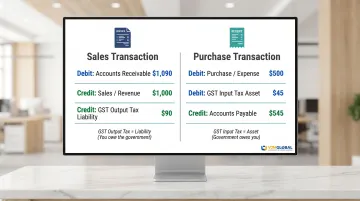

When you issue a tax invoice for a standard-rated sale, the full invoice amount flows through three accounts:

Example: $1,000 sale at 9% GST

| Account | Debit | Credit |

|---|---|---|

| Accounts Receivable (or Bank) | $1,090 | |

| Sales/Revenue | $1,000 | |

| GST Output Tax (liability) | $90 |

The $1,090 represents what the customer owes or has paid. The $1,000 is your actual revenue. The $90 is a liability — money you've collected on behalf of IRAS that you'll remit at period-end.

Recording Input Tax on Purchases

When you receive a tax invoice from a GST-registered supplier, the entry reverses:

Example: $500 purchase at 9% GST

| Account | Debit | Credit |

|---|---|---|

| Purchase/Expense | $500 | |

| GST Input Tax (asset) | $45 | |

| Accounts Payable (or Bank) | $545 |

The $545 is what you owe or paid the supplier. The $500 is your actual expense. The $45 is a recoverable asset — GST you'll claim back from IRAS in Box 7 of your return.

The Two Accounting Bases: Invoice vs. Cash

Under the invoice basis (the default), you record entries when the tax invoice is issued or received, regardless of payment. IRAS requires output tax to be accounted for at the earlier of (a) when an invoice is issued or (b) when payment is received.

Under the Cash Accounting Scheme, entries are only recorded when cash actually changes hands. This scheme is available to businesses with annual taxable turnover not exceeding S$1 million and requires a separate application to IRAS.

You must apply one basis consistently — switching methods mid-period creates reconciliation failures that are difficult to unwind.

Conditions for Claiming Input Tax

You can only record and claim input tax if all the following conditions are met:

- You hold a valid tax invoice addressed to your business

- The purchase is for business purposes

- The expense is not a disallowed claim under Regulations 26 and 27

- You pay your supplier within 12 months from the due date; if not, you must repay the input tax to IRAS

- Claims are made within five years from the end of the relevant accounting period

IRAS specifically blocks input tax claims on motor cars, club subscriptions, medical expenses (with limited exceptions), and family benefits. If you code these expenses with a debit to GST Input Tax, you've over-claimed — and audits target this error.

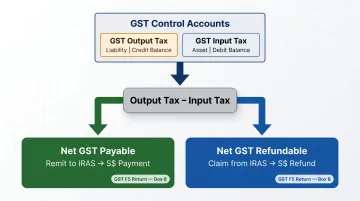

Period-End Settlement Entry

At the close of each GST accounting period, you offset the balances in your two control accounts:

If output tax exceeds input tax (net GST payable):

| Account | Debit | Credit |

|---|---|---|

| GST Output Tax | $X | |

| GST Input Tax | $Y | |

| GST Payable to IRAS | $(X – Y) |

If input tax exceeds output tax (net GST refundable):

| Account | Debit | Credit |

|---|---|---|

| GST Refund Receivable | $(Y – X) | |

| GST Input Tax | $Y | |

| GST Output Tax | $X |

The net figure from this entry flows into Box 8 of the GST F5 return. If GST is payable, payment is due by the filing deadline — typically one month after the end of your accounting period.

GST Journal Entries for Adjustments and Period-End Settlement

Credit Notes and Debit Notes

When you issue a credit note — for a sales return, discount, or billing error — you must reverse the original output tax entry proportionally:

Example: Credit note for $218 (GST-inclusive)

| Account | Debit | Credit |

|---|---|---|

| Sales/Revenue | $200 | |

| GST Output Tax | $18 | |

| Accounts Receivable | $218 |

Adjustments must be made in the GST F5 return for the accounting period in which the credit note is issued, not the period of the original sale. Missing this entry means you over-report output tax in Box 6.

Debit notes work in the opposite direction — they increase both the taxable value and the GST amount.

Bad Debt Relief

If a debt remains unpaid for more than 12 months and meets IRAS conditions, you can claim bad debt relief to recover the output tax previously paid:

Qualifying conditions:

- You've accounted for and paid GST on the supply

- The debt is written off in your accounts

- 12 months have elapsed from the date of supply, or the debtor has become insolvent

- You've taken reasonable steps to recover the debt

Journal entry to claim relief:

| Account | Debit | Credit |

|---|---|---|

| Bad Debt Expense | $X | |

| GST Output Tax (or Bad Debt Relief Receivable) | $Y | |

| Accounts Receivable | $(X + Y) |

The relief amount is reported in Box 7 (input tax and refunds claimed) and you must indicate "Yes" in Box 11. Claims must be made within 5 years from the date of supply.

If the customer subsequently pays, you must repay the relief by including the recovered GST in Box 6 in the period payment is received.

Importing Goods — Accounting for Import GST

GST on imports is paid to Singapore Customs at the point of importation, not to the supplier. The journal entry records this separately:

Standard import (GST paid at customs):

| Account | Debit | Credit |

|---|---|---|

| GST Input Tax | $X | |

| Bank (or Accrued Customs Duty) | $X |

Import GST Deferment Scheme (IGDS):

Approved businesses can defer import GST payments until their monthly GST returns are due, rather than paying at importation. Under IGDS, you account for deferred import GST and claim it as input tax in the same return — so the two entries offset each other with no upfront cash outlay. Goods imported under IGDS are reported in Box 9 of the F5 return.

IGDS participants must file on a monthly basis, not quarterly.

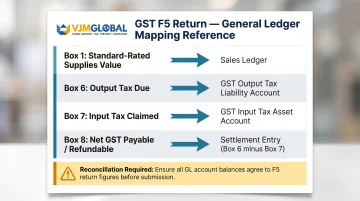

How GST F5 Return Boxes Map to Your Accounts

| F5 Box | Description | Source Account/GL Code |

|---|---|---|

| Box 1 | Total value of standard-rated supplies (excl. GST) | Sales ledger entries (taxable sales) |

| Box 6 | Output tax due | GST Output Tax liability account |

| Box 7 | Input tax and refunds claimed | GST Input Tax asset account |

| Box 8 | Net GST to be paid to / claimed from IRAS | Box 6 minus Box 7 (settlement entry) |

Inconsistent sales coding is the most common reason Box 1 fails to reconcile during audits. If input tax is claimed on blocked expenses, Box 7 will be overstated — both errors draw IRAS scrutiny.

Special GST Accounting Situations in Singapore

Customer Accounting for Prescribed Goods

For certain prescribed goods — mobile phones, memory cards, and off-the-shelf software above S$10,000 GST-exclusive per transaction — the supplier does NOT charge GST. Instead, the customer accounts for both output tax and input tax on the same transaction.

Example: Customer purchases mobile phones worth $11,000 (GST-exclusive)

The customer records:

| Account | Debit | Credit |

|---|---|---|

| Inventory/Purchases | $11,000 | |

| GST Output Tax | $990 | |

| GST Input Tax | $990 | |

| Accounts Payable | $11,000 |

The supplier reports the value in Box 1 but records $0 in Box 6. The customer simultaneously records $990 output tax (Box 6) and claims $990 input tax (Box 7) — netting to zero if fully entitled to input tax credit.

Incorrect treatment leads to under-reporting, because the supplier's return shows zero tax on a taxable supply.

Reverse Charge for Imported Services

From 1 January 2020, GST-registered businesses not entitled to full input tax credit/gst-and-digital-economy/local-businesses) must self-account for GST on services procured from overseas suppliers.

Example: Business imports consulting services worth $5,000 from an overseas provider

| Account | Debit | Credit |

|---|---|---|

| Consulting Expense | $5,000 | |

| GST Output Tax (reverse charge) | $450 | |

| GST Input Tax (partial claim) | $X | |

| Accounts Payable | $5,000 | |

| GST Payable to IRAS | $450 – X |

The business records output tax as if it were the supplier, then claims input tax to the extent it's entitled. If the business makes exempt supplies and can only recover 60% of input tax, the net GST cost is 40% of $450 = $180.

The value of imported services subject to reverse charge is reported in Box 14 of the F5 return.

Zero-Rated vs. Exempt Supplies

Zero-rated supplies (e.g., exports of goods) are taxable supplies charged at 0% GST. They generate no output tax entry, but you can claim full input tax on related costs:

| Account | Debit | Credit |

|---|---|---|

| Accounts Receivable | $1,000 | |

| Sales/Revenue | $1,000 |

Reported in Box 2 of the F5 return.

Exempt supplies (e.g., sale of residential property, financial services) also carry no GST, but you generally cannot claim input tax on attributable costs unless the De Minimis Rule is satisfied:

- Exempt supplies do not exceed an average of S$40,000 per month, AND

- Exempt supplies do not exceed 5% of total taxable and exempt supplies

If both conditions are met, all input tax may be claimed. If not, you must apportion input tax — only claiming the portion attributable to taxable supplies.

Reported in Box 3 of the F5 return.

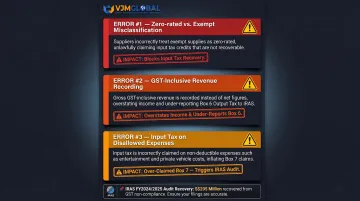

Misclassifying a zero-rated supply as exempt wrongly reduces input tax entitlement. Misclassifying an exempt supply as zero-rated results in over-claiming input tax.

When Complexity Requires Specialist Support

Businesses with mixed supply types, those running multiple IRAS schemes simultaneously (e.g., Major Exporter Scheme + Import GST Deferment Scheme), or foreign companies newly registering for GST in Singapore face real classification and reconciliation risks. Getting the entries wrong from the start compounds quickly across reporting periods.

VJM Global's accounting outsourcing services support foreign businesses navigating cross-border tax compliance, including GST structuring for international operations. With 30+ years of experience in tax and advisory services and a 95% client retention rate, the firm helps businesses establish correctly structured accounting processes from day one.

Common Errors and Misconceptions in GST Accounting Entries

Classification Errors That Distort Both P&L and GST Returns

The most frequent mistakes:

Coding a zero-rated sale as exempt (or vice versa): Both result in no GST charged to the customer. The difference is recoverability — zero-rated supplies preserve full input tax claims, while exempt supplies block them. Misclassifying a zero-rated export as exempt wrongly reduces your input tax claim.

Recording the full GST-inclusive value as revenue: A $1,090 sale should be split: $1,000 to revenue, $90 to GST Output Tax liability. Recording the full $1,090 as revenue overstates your income statement and under-reports output tax in Box 6.

Claiming input tax on disallowed expenses: IRAS blocks input tax on motor cars, club subscriptions, medical expenses (with limited exceptions), and family benefits. If you debit GST Input Tax on these items, you've over-claimed. IRAS audits specifically target this — in FY2024/2025, over 2,800 GST audits recovered S$205 million, with incorrect input tax claims as the most common finding.

Timing Errors That Trigger IRAS Queries

Recording GST in the wrong accounting period is a common trigger for IRAS queries. Two scenarios come up repeatedly:

- Invoice basis: Input tax must be recognised when the tax invoice is dated — not when payment is made. Posting a March invoice in April creates a mismatch between your books and the F5 return.

- Credit notes: GST must be adjusted in the period the credit note is issued, not the period of the original sale. Getting this wrong distorts both periods' returns simultaneously.

The Misconception That "GST Is an Expense"

Beyond timing and classification, a deeper misunderstanding affects how businesses set up their accounts entirely.

GST Output Tax is a liability owed to IRAS, not revenue. GST Input Tax is a recoverable asset, not a cost.

Only when input tax is non-claimable (e.g., on disallowed expenses like staff club memberships) does it become part of the expense. In those cases, the full GST-inclusive amount is coded to the expense account, with no entry to GST Input Tax.

The chart of accounts reflects this directly:

- GST Output Tax sits in liabilities

- GST Input Tax sits in current assets

- Only non-claimable GST flows to expense

Frequently Asked Questions

What are the GST accounting journal entries in Singapore?

On sales, debit Accounts Receivable and credit both Sales and GST Output Tax (a liability). On purchases, debit the relevant expense account and GST Input Tax (a recoverable asset) and credit Accounts Payable. At period-end, the net difference between output and input tax is settled to IRAS via a closing entry.

What are the two options for accounting for GST?

The invoice basis (default) records GST when the tax invoice is issued or received, regardless of payment. The cash accounting scheme records GST only when payment is received or made, and is available to businesses with annual taxable turnover not exceeding S$1 million.

How does GST work in Singapore?

GST is a consumption tax currently at 9%, collected by GST-registered businesses on taxable supplies (output tax) and recoverable on qualifying business purchases (input tax). The net amount is paid to or refunded by IRAS quarterly via the F5 return.

Is GST an expense account?

No. GST output tax is a liability (not revenue) and GST input tax is a recoverable asset (not an expense). It only becomes an expense when input tax is non-claimable — for example, on disallowed items like motor cars or staff entertainment.

Is GST the same as VAT in Singapore?

Yes. GST and VAT are functionally the same type of consumption tax, both levied on the value-add at each stage of the supply chain. Singapore's GST is modelled on New Zealand's GST and the UK's VAT legislation.

What is the format for GST in Singapore?

GST-registered businesses file the GST F5 return quarterly via IRAS's myTax Portal, within one month of the accounting period end. The return covers 15 boxes reporting standard-rated supplies, output tax, taxable purchases, and input tax — all in Singapore dollars.