Introduction

For UK businesses looking to enter Southeast Asia, Singapore stands out as the most practical starting point. With bilateral trade totalling approximately $10.59 billion USD in 2025, the city-state combines a familiar English-speaking legal environment with strong commercial ties to the UK — reinforced by the UK-Singapore Free Trade Agreement, which entered into force on 1 January 2021.

The UK-Singapore Digital Economy Agreement, signed in February 2022, further supports cross-border data flows and digital trade — a significant advantage for UK firms in financial services, technology, and professional services.

When setting up operations in Singapore, UK businesses typically consider three routes: a branch office, a subsidiary (Private Limited Company), or a representative office. Each carries different legal, tax, and operational implications. This guide focuses on the branch office route — what it involves, what UK companies must prepare, and how to work through the registration process.

Key Takeaways

- A Singapore branch is a legal extension of your UK parent company—not a separate entity—with the parent retaining full liability

- Registration requires a licensed Corporate Service Provider (CSP) and a Singapore-resident authorised representative

- Required documents include a certified Certificate of Incorporation, Articles of Association, audited accounts, and director register

- Branch offices are non-resident for Singapore tax purposes, losing access to start-up exemptions and full DTA benefits

- Registration completes in 1–3 business days; ongoing obligations cover ACRA filings, tax returns, GST, and CPF

What Is a Branch Office in Singapore?

A Singapore branch office is a registered extension of your UK parent company that operates under the same legal identity. It shares the same name, is bound by the same constitution, and cannot conduct business activities outside the scope of your parent company's operations. Under the Singapore Companies Act 1967, any foreign company establishing a place of business in Singapore must register with the Accounting and Corporate Regulatory Authority (ACRA) before commencing operations.

Unlike a subsidiary—a separate Singapore-incorporated entity with its own shareholders and limited liability—a branch office is wholly tied to the UK parent. There are no separate shareholders, and the parent company bears full liability for any contracts, debts, or legal claims arising from the Singapore operation.

This structure suits large multinationals and regulated industries where direct parent accountability is required. At a glance, the two structures differ in three key ways:

- Legal identity: A branch shares the parent's identity; a subsidiary is independent

- Liability: The UK parent is fully liable for branch obligations; subsidiary liability is ring-fenced

- Scope: Branch activities cannot exceed the parent company's permitted operations

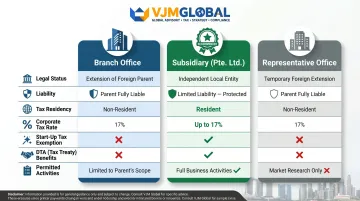

Branch Office vs. Subsidiary vs. Representative Office: What UK Businesses Should Know

Each structure carries distinct legal, tax, and operational consequences. UK businesses that default to "branch office" without comparing the alternatives often encounter avoidable liability exposure or missed tax advantages. The table below breaks down the key differences:

| Feature | Branch Office | Subsidiary (Pte. Ltd.) | Representative Office |

|---|---|---|---|

| Legal status | Extension of parent | Separate legal entity | No legal status; temporary |

| Liability | Parent bears full liability | Limited to subsidiary's assets | Parent bears liability |

| Tax residency | Non-resident | Singapore tax resident | Not applicable |

| Corporate tax rate | 17% on SG-source income | 17% on chargeable income | None (cannot earn revenue) |

| Start-up tax exemption | ✗ Not eligible | ✓ Eligible (first 3 years) | N/A |

| Partial tax exemption | ✓ Eligible | ✓ Eligible | N/A |

| DTA benefits | Limited (PE provisions apply) | ✓ Full treaty benefits | N/A |

| Permitted activities | Commercial operations | Any lawful activity | Market research, liaison only |

The DTA Limitation for UK Businesses

The UK and Singapore have a Double Taxation Agreement in place. While a branch constitutes a permanent establishment (PE) under the treaty, the branch itself is classified as a non-resident entity and cannot claim relief in the same way a Singapore-incorporated subsidiary can. UK businesses should therefore assess whether Singapore-sourced profits could face dual tax exposure when repatriated — a risk that a Pte. Ltd. subsidiary largely avoids.

When a branch office is the right choice:

- Large multinationals operating across multiple jurisdictions

- Regulated industries (banking, insurance, legal services, energy) where regulators require direct parent accountability

- Situations where the UK parent needs to contract and invoice under its established global brand identity rather than a new local entity

If a branch office fits your situation, the next step is understanding exactly what the registration process involves — and where delays typically occur.

Key Requirements and Documents UK Companies Need

Four Non-Negotiable Requirements

Before you can register a branch office in Singapore, you must meet these conditions:

- The UK parent company must be validly incorporated and in good standing

- The branch must register under the same name as the UK parent

- A Singapore-resident authorised representative must be appointed

- A local registered office address in Singapore must be provided

The authorised representative must be ordinarily resident in Singapore (a Singapore citizen, Permanent Resident, or Employment Pass holder). This individual bears personal responsibility if the branch fails to meet its legal obligations, making this selection a serious decision.

Required Documents

UK companies must prepare and certify the following documents:

- Certificate of Incorporation from Companies House

- Articles of Association — the UK equivalent of a company constitution

- Latest audited financial statements (or a declaration if newly incorporated)

- Register of directors of the UK parent company

- Consent form and personal particulars of the appointed authorised representative

Certification Requirements

UK-origin documents must typically be certified as true copies. Since the UK is a signatory to the Hague Apostille Convention, UK documents require only an apostille from the UK Foreign, Commonwealth & Development Office (FCDO) Legalisation Office—no additional consular legalisation is needed.

Engaging a Corporate Service Provider

UK companies cannot file directly with ACRA. You must engage a licensed Corporate Service Provider (CSP) or registered filing agent in Singapore to submit the application through the BizFile+ portal on your behalf. Your CSP handles document preparation, manages the filing, and liaises with ACRA throughout the process.

Fees

According to ACRA:

- Name reservation: SGD 15

- Branch registration: SGD 300

Total first-year costs will be higher once you factor in CSP service fees, registered office costs, and accounting setup. Once your documents are in order and a CSP is engaged, the registration itself typically moves quickly.

Step-by-Step: How to Register a Branch Office in Singapore

For UK businesses, document certification and apostille processing are the most common sources of delay. Start gathering paperwork well before your target registration date — ideally 4–6 weeks ahead.

Step 1 – Reserve a Business Name

Before filing the registration application, your UK parent company's name must be reserved through BizFile+. The Singapore branch must use the same name as the UK parent. ACRA will reject names that conflict with existing registered entities in Singapore. If your exact UK company name is already taken or restricted, seek legal advice before proceeding.

Name reservations are typically approved within one working day and remain valid for 60 days (extendable for another 60 days).

Step 2 – Engage a Licensed Corporate Service Provider

Your CSP will submit the registration on your behalf through BizFile+. They will also have their own internal document and KYC (Know Your Customer) requirements to fulfil before filing.

Step 3 – Prepare and Certify All Required Documents

This is typically the most time-consuming step for UK companies. You'll need certified copies of:

- Companies House records

- Articles of Association

- Financial statements

- Director particulars

Allow adequate time for apostille certification through the UK Foreign, Commonwealth & Development Office (FCDO) process.

Step 4 – Submit Application via BizFile+ and Appoint the Authorised Representative

Your CSP will log in to BizFile+ and file the full registration package, entering the Singapore branch's details, registered office address, business activities, and all position holder information — including the locally resident authorised representative.

Most straightforward applications are approved within 1–3 business days. Applications requiring referral to a sector-specific regulator, such as MAS for financial services, can take 14–60 days.

Step 5 – Receive UEN and Begin Operations

Upon approval, ACRA issues the branch's Unique Entity Number (UEN) — the identifier used for all government agency interactions in Singapore. The branch can now legally commence operations.

The UEN does not mean the branch can immediately trade in all regulated sectors. Sector-specific licences (such as those for financial services, healthcare, or food and beverage) must be applied for separately through the GoBusiness portal.

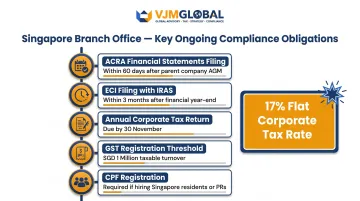

Post-Registration Compliance and Tax Obligations for UK Businesses

Ongoing Compliance Requirements

UK companies must maintain several key annual obligations for their Singapore branch:

- File audited Singapore branch financial statements with ACRA within 60 days of the UK parent's AGM

- File Estimated Chargeable Income (ECI) with IRAS within 3 months of the branch's financial year-end

- File annual corporate income tax return with IRAS by 30 November

- Register for GST if annual taxable turnover exceeds SGD 1 million

- Register for CPF if employing Singapore citizens or Permanent Residents

Managing these from the UK typically requires a local accounting partner or a retainer with a Singapore-based compliance firm.

Singapore Financial Reporting Standards

Branches must prepare financial statements under Singapore Financial Reporting Standards (SFRS), even if the UK parent reports under UK GAAP or IFRS. In practice, this means maintaining a completely separate set of accounts to Singapore standards — additional bookkeeping work that adds to ongoing operating costs UK businesses should budget for from day one.

Tax Implications Specific to UK Companies

Branch offices are taxed on Singapore-sourced income at the flat corporate tax rate of 17%.

Unlike a Singapore-incorporated subsidiary, a branch:

- Cannot access Singapore's start-up tax exemption scheme

- Can access the partial tax exemption (PTE) for resident and non-resident companies

- Cannot access most government grants or investment incentives offered by EDB and other agencies

Important tax note: The UK-Singapore Double Taxation Agreement applies to branches as permanent establishments under Article 7. However, the branch is treated as a non-resident entity — which limits its ability to claim treaty benefits that require Singapore tax residency. UK businesses should take qualified tax advice on profit repatriation and any dual taxation exposure before structuring their operations.

Frequently Asked Questions

Can a foreigner open a business in Singapore?

Yes, foreigners can open a business in Singapore, but they must appoint a locally resident director or authorised representative (depending on the entity type), engage a licensed Corporate Service Provider to file with ACRA, and meet the relevant documentation requirements.

What is a branch office in Singapore?

A Singapore branch office is a registered extension of a foreign parent company—not a separate legal entity. It operates under the same name, constitution, and legal identity as its overseas head office, with the parent company remaining fully liable for all branch obligations.

Is a branch office better than a subsidiary for a UK company expanding to Singapore?

For most small-to-mid-size UK businesses, a subsidiary (Private Limited Company) is the better choice — it offers limited liability, Singapore tax residency, and access to local incentives and DTA benefits. A branch suits large multinationals or regulated industries where direct parent accountability is required.

What documents does a UK company need to register a branch office in Singapore?

Required documents include a certified copy of the UK Certificate of Incorporation, Articles of Association, latest audited financial statements, register of directors, and details of the Singapore-resident authorised representative. All UK documents typically require apostille certification via the FCDO.

Can a UK company claim Singapore double tax treaty benefits through a branch office?

A branch is treated as a non-resident entity, so while the UK-Singapore DTA applies to it as a permanent establishment under Article 7, it cannot access treaty benefits requiring Singapore tax residency—such as reduced withholding tax rates on outbound payments.

How long does it take to register a branch office in Singapore?

Once all documents are prepared and certified, registration through ACRA via BizFile+ typically takes 1–3 business days for standard applications. However, applications in regulated sectors that require referral to a government agency (such as MAS) can take between 14 and 60 days.