For Singapore investors, this guide addresses a critical knowledge gap. Despite strong India-Singapore trade ties anchored by the Comprehensive Economic Cooperation Agreement (CECA) and a bilateral tax treaty (DTAA), the subsidiary registration process involves multiple regulatory touchpoints across the Ministry of Corporate Affairs (MCA), Reserve Bank of India (RBI), and state-level authorities. Errors in sequencing, documentation, or post-incorporation filings remain the single biggest cause of delays and penalties for first-time India entrants.

Key Takeaways

- A Singapore parent can own 50–100% of an Indian private limited company under the automatic FDI route (no RBI pre-approval needed)

- Registration takes 15–25 working days via SPICe+ integrated filing, covering DIN, PAN, TAN, GST, and incorporation in one submission

- India-Singapore DTAA reduces withholding tax to 10% on dividends and royalties (vs. 20% domestic rate)

- Post-incorporation: FC-GPR filing is due within 30 days of equity remittance, plus annual transfer pricing documentation for intercompany transactions

- VJM Global handles incorporation and ongoing compliance for Singapore investors, with dedicated support at every regulatory step

What Is a Subsidiary Company in India?

Under Section 2(87) of the Companies Act, 2013, a subsidiary is a company where the holding company either controls the composition of the Board of Directors or exercises more than half the total voting power. The critical distinction: ownership exceeding 50% creates the parent-subsidiary relationship.

In practice, Singapore investors typically structure their India entities in two ways:

- Wholly owned subsidiary (WOS): 100% shareholding by the Singapore parent, permissible in most sectors under India's automatic FDI route

- Majority subsidiary: Singapore parent holds 50–100%, with balance held by Indian or other foreign partners

The private limited company structure dominates for operational flexibility. Unlike a liaison office (prohibited from earning revenue in India) or a branch office (restricted to specific activities and requiring RBI approval), a subsidiary is a full-fledged Indian legal entity.

As a standalone legal entity, a subsidiary can:

- Conduct any business activity permitted under its Memorandum of Association

- Raise local capital from Indian financial institutions

- Acquire property in India

- Participate in government tenders

These capabilities make the subsidiary structure the preferred choice for Singapore investors looking to scale operations in India's domestic market.

Why Singapore Companies Are Expanding into India via a Subsidiary

Singapore ranks 2nd among all FDI source countries, contributing cumulative equity inflows of USD 171.92 billion as of December 31, 2024—representing 23.87% of India's total FDI. This investment corridor reflects decades of bilateral trade frameworks and regulatory alignment.

Strategic advantages of the subsidiary structure for Singapore companies:

- Caps parent company exposure at the equity investment amount through limited liability protection

- Enables local hiring, INR contracts, and domestic supply chain access without foreign branch restrictions

- Qualifies for India-Singapore DTAA withholding tax relief on cross-border payments

- Unlocks PLI schemes, export subsidies, and sector-specific incentives that foreign branch offices cannot access

Singapore-specific regulatory advantage:

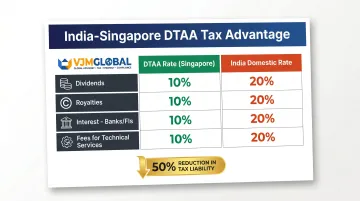

Of these benefits, the tax treaty advantage is the most consequential for cross-border cash flows. The India-Singapore DTAA (amended 2016) provides the following preferential withholding tax rates:

| Income Type | DTAA Rate | India Domestic Rate |

|---|---|---|

| Dividends | 10% | 20% |

| Royalties | 10% | 20% |

| Interest (banks/FIs) | 10% | 20% |

| Fees for Technical Services | 10% | 20% |

These rates apply when the Singapore parent is the beneficial owner of the income. The treaty's Limitation of Benefits (LOB) clause requires the Singapore parent to demonstrate economic substance—specifically, minimum annual expenditure of S$200,000 in Singapore—to access treaty benefits. Shell companies or mere holding entities may be denied treaty relief during Indian tax assessments.

Step-by-Step: How to Register a Subsidiary in India

The registration process runs through the MCA's online portal and typically completes within 15–25 working days from name reservation to Certificate of Incorporation. VJM Global manages this end-to-end for Singapore investors — handling document apostille, director compliance, and integrated filings so nothing slips through the cracks.

Step 1: Obtain Digital Signature Certificates (DSC)

All proposed directors must hold a Class 3 DSC to digitally sign incorporation forms. For Singapore-based directors, required documents include:

- Government-issued ID (passport)

- Proof of Singapore address (utility bill or bank statement)

- Passport-sized photograph

Critical for Singapore nationals: Documents originating outside India must be notarized and apostilled. Since Singapore acceded to the Hague Apostille Convention in September 2021, the Singapore Academy of Law (SAL) is the designated competent authority. SAL affixes an Apostille Certificate after notarization by a Singapore Notary Public. The apostille fee is S$87.20 (inclusive of GST). Apostilled documents are accepted in India without additional embassy legalization.

DSC issuance takes approximately 2 days once documents are verified.

Step 2: Apply for Director Identification Number (DIN)

Every director requires a unique DIN. The SPICe+ form allows up to 3 DIN applications to be processed simultaneously with incorporation. Directors beyond the first three must apply separately via Form DIR-3 after incorporation.

Mandatory resident director requirement: Section 149(3) of the Companies Act mandates at least one director who has stayed in India for 182+ days during the preceding financial year. Singapore investors typically appoint a local Indian resident director or engage professional nominee director services to satisfy this requirement.

Step 3: Reserve the Company Name

Part A of the SPICe+ form is used to reserve the company name. Key rules:

- Submit up to 2 name options in order of preference

- Name must reflect the nature of business (avoid generic or misleading names)

- If using the Singapore parent's brand name in India, attach a No Objection Certificate (NOC) from the parent company

- Approved name is reserved for 20 days (extendable to 60 days for existing companies)

Name approval typically takes 5 days. The SPICe+ Part B (incorporation filing) must be submitted within the 20-day reservation window.

Step 4: File the SPICe+ Form and Supporting Documents

Once the name is reserved, SPICe+ Part B must be filed within that 20-day window. This integrated form simultaneously processes:

- Company incorporation (Certificate of Incorporation)

- PAN (Permanent Account Number)

- TAN (Tax Deduction Account Number)

- GSTIN (optional, if applied for)

- EPFO (Employees' Provident Fund) registration

- ESIC (Employees' State Insurance) registration

- Professional Tax registration (in applicable states)

Required attachments include:

- INC-33: Memorandum of Association (MOA) — defines the company's objectives, authorized capital, and subscriber details (critical for FDI compliance, as it determines permissible business activities)

- INC-34: Articles of Association (AOA) — internal governance rules covering board meetings, share transfers, and dividend policy

- Agile Pro: Integrated application for PAN, TAN, and EPFO/ESIC

- INC-9: Declaration by professionals (CA/CS/CMA) certifying document compliance

Step 5: Obtain the Certificate of Incorporation (COI)

Once the Registrar of Companies (ROC) approves the SPICe+ filing, it issues:

- Certificate of Incorporation with Corporate Identification Number (CIN)

- PAN (for income tax purposes)

- TAN (for TDS deductions)

This marks the official creation of the Indian legal entity. That said, the company cannot begin operations immediately. It must first file Form INC-20A (Certificate of Commencement of Business) within 180 days of incorporation. This declaration confirms that all subscribers have paid for their shares.

Documents Required for Singapore Investors

Company-Related Documents (from Singapore Parent)

| Document | Apostille Required | Notes |

|---|---|---|

| Board resolution authorizing Indian subsidiary incorporation | Yes | Must be notarized by Singapore Notary Public, then apostilled by SAL |

| Certificate of Incorporation of Singapore parent company | Yes | Certified true copy required |

| Memorandum and Articles of Association (or Constitution) of parent company | Yes | Recent certified copy |

| Proof of registered office address for Indian subsidiary | No | Utility bill + NOC from property owner (must be in India) |

Director-Related Documents (for Singapore-National Directors)

- Government-issued ID and address proof (notarized and apostilled)

- Passport-sized photograph

- Form DIR-2: Consent to act as director

- Form MBP-1: Disclosure of interest in other entities

- DIN (if already obtained in a prior incorporation)

Apostille Process for Singapore Investors

Documents must first be notarized by a Singapore Notary Public, then submitted to the Singapore Academy of Law for apostille. India, as a Hague Convention member since 2005, accepts apostilled documents without embassy attestation — cutting processing time considerably compared to non-Convention countries.

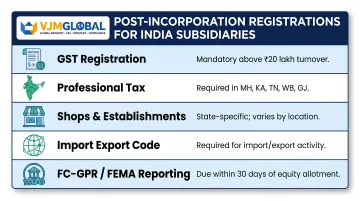

Post-Incorporation Registrations

Once your subsidiary is incorporated and documents are in order, several compliance registrations follow. Requirements vary by state and business activity:

- GST registration: Mandatory if aggregate turnover exceeds ₹20 lakh (₹10 lakh for special category states)

- Professional Tax registration: State-specific; required in Maharashtra, Karnataka, Tamil Nadu, West Bengal, Gujarat (not applicable in Delhi, Haryana, Punjab)

- Shops & Establishments registration: State-level labour compliance; varies by location

- Import Export Code (IEC): Required if the subsidiary will import goods or services

- FEMA reporting: FC-GPR filing required within 30 days of equity allotment

Post-Incorporation Compliance Requirements

Once incorporated, your Indian subsidiary immediately enters three overlapping compliance layers: corporate (MCA/ROC), foreign exchange (RBI/FEMA), and tax (Income Tax/GST). Each carries its own deadlines and penalties.

Statutory Corporate Compliance

Within 30 days of incorporation:

- Hold the first Board of Directors meeting (Section 173 mandates minimum 4 board meetings per year with maximum 120-day gap between meetings)

- Appoint the first statutory auditor (Section 139(6))

Within 60 days of incorporation:

- Issue share certificates to subscribers of the Memorandum (Section 56(4)(a))

Within 180 days of incorporation:

- File Form INC-20A (Certificate of Commencement of Business) with the ROC, declaring that subscribers have paid for their shares

Ongoing:

- Maintain statutory registers at the registered office (register of members, register of directors, register of charges)

- Directors must file Form MBP-1 disclosing interests in other entities

Annual Filings with the ROC

| Form | Purpose | Deadline |

|---|---|---|

| AOC-4 | Financial statements filing | Within 30 days of Annual General Meeting (AGM) |

| MGT-7 / MGT-7A | Annual return | Within 60 days of AGM |

Non-compliance attracts penalties under Section 92 (₹50,000 fine for company + ₹1,000 per day penalty for officers in default).

FEMA and RBI Obligations for Foreign-Owned Subsidiaries

FC-GPR Filing:

When the Singapore parent remits equity capital into the Indian subsidiary, the company must report the investment to RBI via Form FC-GPR (Foreign Currency - Gross Provisional Return) through the RBI FIRMS portal within 30 days of share allotment.

Required attachments:

- Foreign Inward Remittance Certificate (FIRC) from the Indian bank

- KYC report of foreign investor

- Board resolution approving share allotment

- Valuation certificate (from CA or SEBI-registered merchant banker)

- Company Secretary certificate

Late submission attracts a Late Submission Fee: ₹7,500 + (0.025% × Amount × Years of delay), capped at 100% of investment amount.

Automatic Route vs. Government Route:

Most sectors allow FDI under the automatic route—no prior RBI or government approval required. Singapore investors only need to file FC-GPR post-investment. Sectors requiring government route approval (via Foreign Investment Facilitation Portal) include:

- Defence (above 74% FDI)

- Multi-brand retail trading

- Print media (news/current affairs)

- Banking (public sector)

- Satellites establishment

Press Note 3 (2020) restrictions (requiring government approval for land-bordering countries like China) do not apply to Singapore.

Tax Compliance

Corporate Income Tax:

- Indian subsidiaries must file annual income tax returns

- Corporate tax rate: 25% (for companies with turnover up to ₹400 crore) or 30% (for larger companies), plus surcharge and cess

GST Compliance:

- Monthly/quarterly GST returns depending on turnover and registration type

- GSTR-1 (outward supplies), GSTR-3B (summary return), GSTR-9 (annual return)

Transfer Pricing Compliance (Critical for Singapore Parent-Subsidiary Transactions):

Sections 92-92F of the Income Tax Act mandate that all international transactions between the Indian subsidiary and its Singapore parent be conducted at arm's length price. This includes:

- Management fees

- Technical service fees

- Royalty payments for intellectual property

- Intercompany loans (interest must be at arm's length)

- Shared service charges

If aggregate international transactions exceed ₹1 crore, the Indian subsidiary must maintain a Transfer Pricing Study covering:

- Functional, Asset, and Risk (FAR) analysis

- Transfer pricing method selection (CUP, Resale Price, Cost Plus, TNMM, or Profit Split)

- Benchmarking study with comparable independent transactions

- Economic analysis justifying arm's length pricing

Form 3CEB filing: A Chartered Accountant must certify the transfer pricing documentation and file Form 3CEB by October 31 of the assessment year.

Important update: Under the new Income-tax Act, 2025 (effective April 1, 2026), Form 48 replaces Form 3CEB. Form 48 introduces enhanced structured, transaction-wise reporting with six parts covering taxpayer details, transaction summaries, associated enterprise information, arm's length price determination, and accountant certification.

Penalties for non-compliance:

- Failure to maintain transfer pricing documentation: 2% of transaction value (Section 271AA)

- Failure to file Form 3CEB: ₹100,000 (Section 271BA)

VJM Global handles transfer pricing study preparation, benchmarking analysis, intercompany agreement drafting, and Form 3CEB/Form 48 filing for Singapore-owned Indian subsidiaries.

Common Mistakes Singapore Investors Make

Underestimating State-Level Compliance Complexity

India's federal structure means compliance obligations vary significantly across states. Common oversights include:

- Professional Tax: Capped at ₹2,500 per person annually under Article 276 of the Constitution, but not levied uniformly. Maharashtra, Karnataka, Tamil Nadu, West Bengal, and Gujarat require registration. Delhi, Haryana, Punjab, and Rajasthan do not. Companies operating across multiple states need separate registrations in each state.

- Shops & Establishments Act: Every state has its own registration requirements, working hour limits, and leave policies. A subsidiary with offices in Mumbai and Bangalore must comply with both Maharashtra and Karnataka regulations.

- GST registration: If the subsidiary operates in multiple states (e.g., warehouse in Gujarat, sales office in Delhi), separate GST registrations are required for each state.

Singapore investors accustomed to Singapore's unified regulatory framework frequently assume India follows a similar model. This federal-state compliance gap is a leading cause of penalties during inspections.

Misunderstanding the "No Minimum Capital" Rule

India formally abolished the minimum paid-up capital requirement (previously ₹1 lakh for private companies) via the Companies (Amendment) Act, 2015. However, Singapore investors sometimes misinterpret this to mean they can defer equity remittance.

The reality: While there is no statutory minimum capital, the subsidiary must:

- Declare authorized capital in the MOA

- Allot shares to subscribers within a reasonable time

- Report all FDI inflows to RBI via FC-GPR within 30 days of allotment

- File Form INC-20A within 180 days, confirming subscribers have paid for shares

Failure to remit adequate working capital via the FDI route creates FEMA compliance risk. Indian banks typically require proof of minimum capitalization (often ₹1–2 lakh) to open a corporate bank account.

Ignoring Transfer Pricing Obligations

Singapore companies frequently underestimate the documentation burden for intercompany transactions. Common mistakes include:

- Relying on verbal agreements or email approvals for management fees and shared services — Indian rules require written agreements specifying pricing methodology, payment terms, and responsibilities

- Treating small intercompany charges as exempt: amounts of ₹10–20 lakh can aggregate past the ₹1 crore threshold, triggering a full transfer pricing study and Form 3CEB filing

- Reusing prior-year benchmarking studies without updating comparables and economic analysis — documentation must be refreshed annually

- Overlooking the Form 3CEB to Form 48 transition: the Income-tax Act, 2025 introduces Form 48 (effective April 1, 2026), requiring enhanced transaction-wise reporting that demands early advisor engagement

Inadequate transfer pricing documentation is one of the most common triggers for tax adjustments and penalties during audits. VJM Global's transfer pricing team works with Indian subsidiaries and their Singapore parents to prepare compliant documentation covering management fees, IP royalties, intercompany loans, and shared services.

Frequently Asked Questions

Does a subsidiary need to be 100% owned?

No. Under Section 2(87) of the Companies Act, a subsidiary only requires the parent company to hold more than 50% of voting shares. A wholly owned subsidiary (100% ownership) is permissible in sectors where 100% FDI is allowed under India's automatic route, which includes most industries.

Can a Singapore company set up a subsidiary in India without an Indian partner?

Yes. Most sectors allow a wholly owned subsidiary under the FDI automatic route, with no Indian partner required. One condition applies regardless of ownership structure: at least one Board director must be an Indian resident (182+ days in India in the preceding calendar year).

How long does it take to register a subsidiary in India?

The typical timeline is 15–25 working days from name reservation to Certificate of Incorporation, assuming documents are complete and apostilled. Common delays arise from name approval conflicts with existing entities and slower-than-expected apostille processing in Singapore.

What is the minimum capital required to register a subsidiary in India?

India abolished the minimum paid-up capital requirement in 2015. There is no statutory minimum. However, the Singapore parent must remit equity capital into India via banking channels and report it to RBI via FC-GPR within 30 days of share allotment. Practical considerations (bank account opening, working capital needs) typically result in initial capitalization of ₹1–10 lakh.

What is the difference between a branch office and a subsidiary in India?

A branch office is an extension of the foreign parent, not a separate Indian legal entity. It requires RBI approval and is limited to specific activities such as export/import, R&D, and consultancy. A subsidiary, by contrast, is an independent Indian entity that can conduct any permissible business, hire employees, own assets, and raise local capital without RBI pre-approval under the automatic route.

Do Singapore investors get tax benefits under the India-Singapore DTAA?

Yes. The India-Singapore DTAA reduces withholding tax rates on dividends, royalties, and technical service fees to 10% (against the 20% domestic rate), and interest to 10–15% depending on the lender type. To qualify, the Singapore parent must be the beneficial owner of the income and meet the Limitation of Benefits clause, which requires a minimum annual expenditure of S$200,000 in Singapore.

VJM Global supports Singapore investors with end-to-end subsidiary registration and compliance services, including document apostille coordination, SPICe+ filing, post-incorporation ROC compliance, GST and income tax return filing, FC-GPR and FEMA reporting, and transfer pricing documentation for intercompany transactions. Contact VJM Global at info@vjmglobal.com or +91 98915 76441 to streamline your India market entry.