Introduction

Canada has more than 4,000 publicly listed companies across its exchanges. From Royal Bank of Canada to Shopify, the markets span banking, energy, mining, and technology — covering nearly every major sector of the economy.

For investors, entrepreneurs, and foreign businesses considering Canadian market entry, "public company" carries specific legal weight. The regulatory framework is layered and provincially driven, with real consequences: tax treatment under the Income Tax Act, continuous disclosure obligations, and securities rules that vary by province.

This article covers what public companies are under Canadian law, how they differ from private companies, what the process of going public actually involves, and who the major players are.

Key Takeaways

- A public company in Canada trades shares on a recognized exchange (such as the TSX) and must meet strict financial reporting and governance obligations.

- Under the Income Tax Act, a company qualifies as a "public corporation" once its shares are listed on a designated Canadian stock exchange.

- Continuous disclosure obligations under NI 51-102 require IFRS financials, annual MD&A, AIFs, and material change reports.

- Listing on a public exchange opens access to broader capital markets while raising regulatory costs and shareholder scrutiny.

- Canada's two primary exchanges — the TSX and TSXV — together list over 3,400 issuers as of 2024.

What Is a Public Company in Canada?

A public company is a corporation whose shares are listed and traded on a recognized stock exchange, allowing any member of the public to buy or sell ownership stakes through the open market.

The Legal Definition

Under subsection 89(1) of the Income Tax Act, a corporation resident in Canada qualifies as a "public corporation" when a class of its shares is listed on a designated stock exchange in Canada. The current list of designated exchanges, per the Department of Finance Canada, includes:

- Toronto Stock Exchange (TSX)

- TSX Venture Exchange (TSXV), Tiers 1 and 2

- Montreal Exchange

- Canadian Securities Exchange (CSE)

- Cboe Canada (formerly NEO Exchange)

This definition matters most in tax-sensitive transactions. During going-private or M&A deals, the exact timing of a company's delisting determines when it loses public corporation status, affecting tax treatment on dividends, capital gains, and other corporate events.

The terms "public company" and "public corporation" are used interchangeably in most contexts, but the Income Tax Act assigns distinct implications to each. In tax-sensitive transactions, that distinction matters — consult qualified legal or tax counsel before assuming they're equivalent.

How Companies Become Public

The primary route is an Initial Public Offering (IPO), where a company sells shares to the public for the first time and applies to list on an exchange. This opens access to both equity and debt capital markets.

In Canada, listings occur primarily on exchanges operated by TMX Group:

| Exchange | Purpose | Listed Issuers (2024) |

|---|---|---|

| TSX | Established, large-cap companies | 1,823 |

| TSXV | Emerging and early-stage companies | 1,597 |

| Combined Total | — | 3,417 |

Key Characteristics of a Canadian Public Company

Financial Reporting Obligations

Public companies in Canada prepare financial statements under International Financial Reporting Standards (IFRS), specifically Canadian GAAP applicable to publicly accountable enterprises. This requires:

- An unreserved statement of compliance with IFRS in annual financials

- IAS 34 compliance for interim financial reports

- Independent audits by external auditors appointed by the board

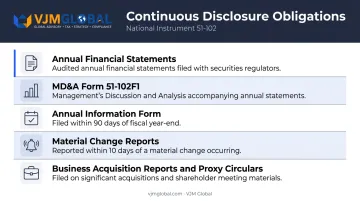

Continuous Disclosure Requirements

National Instrument 51-102 (Continuous Disclosure Obligations) governs what public companies must file and when. Key requirements include:

- Annual financial statements with comparative figures

- MD&A (Management Discussion and Analysis) using Form 51-102F1

- Annual Information Form (AIF) (required for non-venture issuers within 90 days of year-end)

- Material change reports (news release plus Form 51-102F3, due within 10 days of a material change)

- Business acquisition reports and proxy circulars

Regulatory Oversight

Securities regulation in Canada is provincial and territorial, not federal. The Canadian Securities Administrators (CSA) coordinates Canada's 10 provincial and 3 territorial regulators — including the Ontario Securities Commission (OSC) and the British Columbia Securities Commission (BCSC) — to harmonize national policy.

This decentralized structure means a company listed on the TSX must navigate the rules of both its exchange and its home province's securities commission.

Shareholder Rights and Governance

Public companies must:

- Hold annual general meetings (AGMs)

- Allow shareholders to elect directors and vote on major transactions

- Maintain a board with at least two independent directors

- Appoint a CEO, CFO (separate from the CEO), and corporate secretary

Foreign businesses with subsidiaries listed on Canadian exchanges often face the added complexity of aligning these requirements with their home-country reporting standards. VJM Global works with multinational companies on cross-border financial reporting, helping reconcile IFRS obligations with the accounting and compliance frameworks of other jurisdictions.

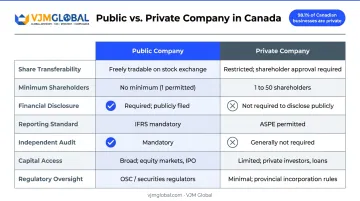

Public Companies vs. Private Companies in Canada

Private companies in Canada are corporations whose shares are not traded on public exchanges. Ownership is typically concentrated among founders, private equity, or a small investor group, and share transfers are restricted — a defining feature under National Instrument 45-106, which limits private issuers to no more than 50 beneficial security holders (excluding employees).

The two structures differ across several key dimensions:

| Dimension | Public Company | Private Company |

|---|---|---|

| Share transferability | Freely tradeable on exchange | Restricted by shareholder agreement |

| Minimum shareholders | 300+ public holders (TSX) | Up to 50 beneficial holders (NI 45-106) |

| Financial disclosure | Full public disclosure required | No public disclosure obligation |

| Reporting standard | IFRS mandatory | Accounting standards flexible |

| Independent audit | Mandatory | Not required |

| Capital access | Broad public and institutional markets | Private equity, VC, debt, retained earnings |

| Regulatory oversight | CSA, OSC, exchange rules | Minimal securities regulation |

Canada had 1.10 million employer businesses as of December 2023, with 98.1% classified as small businesses. Public companies represent a tiny fraction of that total — yet the TSX and TSXV alone listed over 3,800 companies with a combined market capitalization exceeding CAD $4 trillion, concentrating significant economic weight in comparatively few hands.

Benefits and Drawbacks of Going Public in Canada

Benefits of Going Public

Access to capital is the most compelling reason. TSX and TSXV issuers raised a combined C$20.9 billion in 2024, with 224 new listings across both exchanges. The TSX alone accounted for C$16.2 billion of that total.

Additional benefits include:

- Signals financial accountability to customers, partners, and talent through public-market transparency

- Attracts senior executives and key employees with stock-based equity incentives

- Gives founders and early backers a clear path to monetise their holdings through the open market

- Improves borrowing terms, as listed companies typically negotiate better rates with lenders

Drawbacks of Going Public

The benefits come with a real price tag — both upfront and recurring year after year.

Upfront listing costs on the TSX alone include:

- Original listing fees: C$10,000 to C$200,000

- Legal fees: C$400,000 to C$750,000

- Sponsorship fees: C$15,000 to C$50,000

- First audit costs: C$12,000 to C$80,000

Beyond costs, consider the structural trade-offs:

- Major decisions require shareholder approval, and quarterly earnings pressure can push management toward short-term thinking over long-term strategy

- Continuous reporting obligations — financial statements, material change disclosures, management circulars — consume significant time and resources

- Share price swings affect employee morale, acquisition currency, and market perception, even when operations are performing well

How Does a Company Go Public in Canada?

Canadian securities law gives companies several routes to a public listing — each with different disclosure requirements, timelines, and cost profiles. The path you choose depends on your company's size, sector, and readiness for public markets.

The IPO Process

A company going public through an IPO typically follows this sequence:

- Engage underwriters — investment banks advise on pricing, structure the offering, and manage investor roadshows

- File a prospectus — the primary disclosure document under National Instrument 41-101, filed with the relevant provincial securities regulator; covers financials, risk factors, and use of proceeds

- Apply to list — submit to TSX or TSXV and satisfy exchange-specific requirements

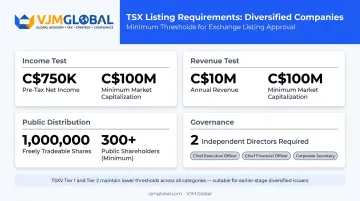

TSX Listing Requirements (Diversified Companies)

The TSX applies multiple listing tests. Key thresholds include:

- Income Test: C$750,000 annual audited pre-tax net income; C$100 million market capitalisation

- Revenue Test: C$10 million annual audited revenue; C$100 million market capitalisation

- Public distribution: Minimum 1,000,000 freely tradeable securities held by at least 300 public holders

- Governance: At least two independent directors; CEO, CFO, and corporate secretary in place

TSXV thresholds are lower. For technology, life sciences, and industrial issuers, Tier 1 requires C$5 million net tangible assets or C$5 million revenue; Tier 2 drops to C$750,000 net tangible assets.

Alternatives to a Traditional IPO

Not every company lists through a conventional IPO. Common alternatives include:

- Reverse Takeover (RTO) — a private company merges with an already-listed shell, effectively "back-door listing" without a full prospectus process. This route is especially common on the TSXV for resource-sector issuers

- SPAC (Special Purpose Acquisition Company) — a TSX-specific vehicle that raises capital with no commercial operations, then acquires a target within 36 months

- Capital Pool Company (CPC) — a TSXV program using a two-step shell company and qualifying transaction route, designed specifically for early-stage companies not yet ready for a full IPO

- Direct listing — companies already listed on recognized exchanges may transfer their listing to TSX or TSXV if they meet the applicable standards

Notable Public Companies in Canada

Canada's public market depth becomes clear when you look at what's listed. According to TMX Group's World Federation of Exchanges data, TMX had 3,569 listed companies with a domestic market capitalisation of approximately US$3.55 trillion as of December 2024.

A few flagship names illustrate the market's range:

| Company | Exchange | Sector | Market Cap (CAD, 2026) |

|---|---|---|---|

| Royal Bank of Canada (RY) | TSX | Banking | ~C$410 billion |

| Shopify Inc. (SHOP) | TSX | Technology | ~C$212 billion |

| Enbridge Inc. (ENB) | TSX | Energy | ~C$168 billion |

| Barrick Mining Corporation (ABX) | TSX | Mining | ~C$87 billion |

Canada's public market has a particularly distinctive strength in resources. Approximately 40% of the world's public mining companies are listed on TSX/TSXV. In 2025 alone, mining companies on these exchanges raised C$16 billion in equity capital and reached a combined market capitalisation of C$1.1 trillion.

Three sectors define the TSX's character:

- Resources — mining and energy companies dominate listings and equity issuance

- Financial services — Canada's five major banks account for roughly 20–25% of the S&P/TSX Composite Index by weight

- Technology — the fastest-growing segment by market cap over the past decade, anchored by Shopify's climb from startup to a C$200+ billion company in under 15 years

Frequently Asked Questions

What is a public company in Canada?

A public company in Canada is a corporation whose shares are listed and traded on a recognized stock exchange such as the TSX. Any member of the public can buy or sell shares, and the company must meet strict financial reporting and governance obligations under securities law and the Income Tax Act.

Is there a Canadian version of an LLC?

Canada does not have a direct equivalent to the U.S. LLC. The closest structures are the Canadian corporation (incorporated federally under the CBCA or provincially) and the limited partnership. Most businesses choose corporate incorporation for limited liability combined with operational flexibility.

What are the benefits of a limited company in Canada?

A Canadian limited company offers several core advantages:

- Limited liability protection for shareholders

- Access to lower corporate tax rates

- Ability to raise capital and attract investors

- Perpetual legal existence independent of ownership changes

- For public companies: direct access to equity markets through stock exchange listings

What is the difference between a public and private company in Canada?

Public companies trade on exchanges and must disclose financials publicly, maintain IFRS-compliant reports, and submit to ongoing regulatory oversight. Private companies face no public disclosure obligations and restrict share transfers — the core structural and regulatory divide.

What stock exchanges do public companies list on in Canada?

The two primary exchanges are the TSX (for established, larger companies) and the TSXV (for smaller and emerging businesses), both operated by TMX Group. The Canadian Securities Exchange (CSE) is also a designated exchange, with approximately 735 listed securities as of early 2026.

What are the reporting requirements for public companies in Canada?

Public companies must prepare IFRS-compliant financial statements and file continuous disclosure documents with provincial securities regulators under NI 51-102. These filings include annual MD&A, AIFs, and material change reports. Financials must also be independently audited on an annual basis.