Introduction

India's appeal to Canadian-based entrepreneurs has never been stronger. India recorded USD 81.04 billion in total FDI inflows in FY2024-25, a 14% jump from the previous year — and the two-way Canada-India merchandise trade relationship stood at $10.9 billion in 2025.

The interest cuts across three distinct groups. Established Canadian business owners want a foothold in one of the world's fastest-expanding consumer markets. Members of the Indo-Canadian diaspora are looking to invest back home. And NRIs and OCIs with existing family or property ties to India are exploring formal business structures for the first time.

For most, the sticking point is the process itself. India's registration system is now largely digital, but it involves multiple regulatory bodies, sequential steps, and cross-border documentation requirements that trip up even well-prepared founders.

This guide walks through the legal process end-to-end: entity types, registration steps, FDI compliance, and what ongoing obligations look like once your Indian company is operational.

Key Takeaways

- Canadian investors can legally start a business in India through a Private Limited Company (WOS), LLP, Joint Venture, or Branch/Liaison Office

- Every foreign-owned Indian company must comply with the Companies Act 2013, FEMA regulations, and RBI reporting requirements

- NRIs and OCIs are treated differently from pure foreign nationals under Indian law, which directly affects ownership rights and repatriation options

- Registration is now online via the MCA's SPICe+ portal, but requires precise, sequenced documentation

- End-to-end setup typically takes several weeks to a few months, depending on documentation readiness

Why Canadian-Based Entrepreneurs Are Looking to India

India was the fastest-growing major economy at 6.5% growth in FY2024-25, according to the World Bank. That growth translates directly into expanding consumer demand, a young workforce, and sectoral opportunities across industries ranging from IT to clean energy.

The Canada-India trade relationship adds further momentum. Canada-India CEPA negotiations are actively underway, with public consultations completed in 2026 covering goods, services, investment, digital trade, and sustainable development. Improved trade terms, when finalized, could lower barriers for Canadian businesses entering India.

Where Canadian Entrepreneurs Are Finding Traction

DPIIT data shows the top FDI-receiving sectors in India by cumulative equity inflow are:

- Services — 16% of cumulative FDI equity inflow

- Computer Software and Hardware — 16%

- Trading — 6%

- Telecommunications — 5%

- Automobiles — 5%

These figures reflect India-wide FDI patterns, not a Canada-specific sector split. They are, however, a reliable signal of where market conditions, regulatory openness, and investor returns converge. For Canadian founders in IT services, professional services, or clean energy, India's market is deep, growing, and actively courting foreign capital.

What Canadians Need to Know Before Starting a Business in India

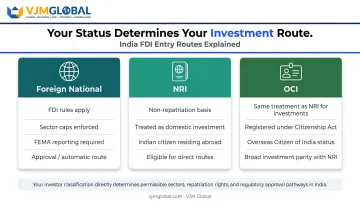

The NRI, OCI, and Foreign National Distinction

This distinction matters more than most Canadian founders expect. Under FEMA and Indian FDI policy:

- Foreign National — A Canadian citizen without Indian origin. Treated as a non-resident foreign investor under FDI rules. Subject to sector caps, the automatic or approval route, and full FEMA reporting obligations.

- NRI (Non-Resident Indian) — An individual resident outside India who is a citizen of India. NRI investment on a non-repatriation basis is deemed domestic investment and treated at par with resident investment.

- OCI (Overseas Citizen of India) — An individual registered as an OCI cardholder under Section 7A of the Citizenship Act, 1955. OCIs largely receive the same treatment as NRIs for investment purposes.

The practical implication: a Canadian citizen of Indian origin who holds OCI status has more flexibility — on repatriation, sector access, and investment basis — than a Canadian citizen with no Indian connection. Misclassifying your status at this stage can lock you into the wrong investment route and create repatriation complications that are difficult to unwind later.

Process Complexity Is Procedural, Not Just Paperwork

India's MCA portal has made registration primarily digital. The process still spans multiple regulatory bodies — MCA, RBI, GSTN, Income Tax — and each has its own timelines, forms, and documentation standards.

One requirement catches many founders off guard: at least one director must be an Indian resident, defined as someone present in India for at least 182 days during the preceding financial year. Canadian-based founders without a local director need to plan for this from day one, either by appointing a trusted individual in India or engaging a nominee director service.

Common Mistakes to Avoid

- Choosing an entity type based on familiarity rather than FDI eligibility and sector fit

- Not understanding FEMA's capital remittance requirements before wiring funds from Canada

- Treating India as a single uniform market — state-level tax, incentive, and registration requirements vary considerably

Choosing the Right Business Structure as a Canadian Investor

The choice of entity shapes tax liability, FDI eligibility, compliance burden, and exit options. Getting this right at incorporation is far cheaper than restructuring later.

VJM Global advises Canadian and other foreign clients through this exact decision as part of their India market entry advisory services, covering sector FDI routes, capital structure, operational requirements, and repatriation planning before a single form is filed.

Private Limited Company / Wholly Owned Subsidiary (WOS)

The most common structure for foreign investors. The parent company holds 100% of shares, creating a separate legal entity under the Companies Act 2013, eligible for most FDI under the automatic route.

Key requirements:

- Minimum 2 directors, at least 1 resident in India (182+ days per financial year)

- Minimum 2 shareholders

- No mandatory minimum authorized capital, but subscription amount must be paid before filing commencement of business

Limited Liability Partnership (LLP)

Well-suited for professional service firms and asset-light business models. Lower compliance burden than a private limited company, no minimum capital requirement, and a separate legal entity.

Important restriction: FDI in LLPs is permitted under the automatic route only in sectors where 100% FDI is permitted under the automatic route and there are no FDI-linked performance conditions. At least one designated partner must also be resident in India.

Joint Venture (JV)

A JV works best when an Indian partner brings something the foreign investor cannot easily replicate. Common scenarios include:

- Entering sectors with FDI caps that require local equity participation

- Accessing established distribution networks or regional relationships

- Sharing operational risk in a market the Canadian investor is still assessing

JVs can be incorporated (as a company or LLP) or structured contractually without forming a new entity. Whichever route you choose, a clear shareholder agreement and defined exit mechanism are non-negotiable — disputes over exit terms are among the most common failure points in foreign-Indian JV structures.

Branch Office / Liaison Office

Appropriate for testing the market or establishing a presence without full incorporation.

| Type | Can Generate Revenue? | RBI Requirements |

|---|---|---|

| Branch Office | Yes (limited permitted activities) | Parent: 5 years profitable, net worth USD 100,000+ |

| Liaison Office | No (representational only) | Parent: 3 years profitable, net worth USD 50,000+ |

Neither a Branch Office nor a Liaison Office is suitable for broad commercial operations; both serve a legitimate purpose for companies still at the market-assessment stage.

How to Legally Register Your Business in India from Canada — Step by Step

The registration sequence below applies primarily to a Private Limited Company, the most common structure for Canadian investors. Complete each step in order — skipping ahead causes filing delays that can set the process back by weeks.

Step 1 — Obtain a Digital Signature Certificate (DSC) and Director Identification Number (DIN)

All proposed directors must obtain a DSC before any MCA filing can proceed. The MCA requires Class-II or above DSCs for e-filings on the MCA21 portal.

For foreign nationals and NRIs based in Canada, DSC documentation typically requires:

- Notarized and apostilled copy of passport

- Address proof

- Contact details

Canada acceded to the Apostille Convention on May 12, 2023, with the convention entering into force on January 11, 2024. Canadian documents can now be apostilled domestically rather than going through consular legalization — cutting weeks off the document preparation timeline.

DINs for all directors who don't already have one can be applied for through the SPICe+ portal simultaneously with the name reservation step.

Step 2 — Reserve the Company Name via the MCA Portal

Name reservation uses the SPICe+ Part A form (or RUN service for LLPs). The name must be unique and must not conflict with existing trademarks or registered companies.

If the foreign parent company wants to use its own name in India, it must provide a board resolution and NOC — both apostilled. Once approved, the name is reserved for 20 days, during which Part B of the incorporation form must be completed.

Step 3 — File for Incorporation via SPICe+ Part B

SPICe+ Part B is the core incorporation form. It covers company incorporation, DIN allotment, PAN and TAN issuance, GST registration (optional at this stage), EPFO/ESIC registration, and bank account pre-selection — all through a single integrated form, accompanied by AGILE-PRO-S.

Canadian-based applicants will need to compile the following documents before filing:

- Apostilled board resolution of the foreign holding company (specifying the authorized representative, proposed capital structure, and director/subscriber details)

- Apostilled MOA and Certificate of Registration of the foreign parent

- ID and address proofs of all directors

- Memorandum and Articles of Association

- Proof of India registered office address (rent agreement or NOC from the property owner)

Step 4 — Complete RBI/FDI Compliance After Receiving Capital

Once the company is registered and the Canadian investor remits capital via SWIFT to the Indian entity's bank account:

- Obtain a Foreign Inward Remittance Certificate (FIRC) and KYC documents from the remitter's bank

- File Form FC-GPR with the RBI through the Authorized Dealer (AD) bank within 30 days of allotting shares to the foreign investor

Under the FEM (Non-Debt Instruments) Rules, 2019, capital instruments must be issued within 60 days of receiving the inward remittance. If shares are not issued within that window, the funds must be refunded within the following 15 days. Confirm the current deadline with your AD bank before initiating the transfer.

Step 5 — Complete Post-Incorporation Registrations and First Compliances

Take these actions immediately after incorporation:

- File Form INC-20A (Declaration of Commencement of Business) with the ROC within 180 days of incorporation

- Hold first board meeting within 30 days

- Appoint first statutory auditor within 30 days

- Issue share certificates

- Affix company name board at the registered office

Before starting operations, you'll also need the following registrations depending on your business activities:

- GST registration — mandatory if annual aggregate turnover exceeds INR 20 lakh (INR 10 lakh in certain special-category states); INR 40 lakh for exclusive goods suppliers in most states

- Professional Tax (state-specific; mandatory through AGILE-PRO-S for companies in Maharashtra, Karnataka, and West Bengal)

- Shop and Establishment Act registration

- Importer Exporter Code (IEC) if the business involves cross-border trade

Ongoing Compliance After Registration

Annual Corporate Filings

A foreign-owned Indian company must meet these recurring obligations:

- Annual Return — Prepared and filed within 60 days from the AGM (Section 92, Companies Act 2013)

- Financial Statements — Filed with the Registrar within 30 days of the AGM (Section 137)

- Annual General Meeting — Must be held annually

- Statutory Audit — Annual audit required; financial records must be audit-ready throughout the year

- Income Tax Return — Filed annually in conformance with the Income Tax Act, 1961

Non-compliance attracts penalties under the Companies Act 2013. VJM Global supports foreign-owned Indian businesses with ongoing accounting, audit, and compliance management — covering secretarial filings, annual audits, and tax returns so Canadian founders can focus on operations rather than regulatory calendars.

FEMA and RBI Ongoing Compliance

Beyond the initial registration, the Canadian parent and Indian subsidiary must keep the RBI informed of ongoing cross-border activity. Key reporting and compliance obligations include:

- Capital infusions — Each subsequent investment must be reported to the RBI via the AD bank

- Inter-company transactions — Loans, royalties, and service fees between parent and subsidiary require RBI reporting

- Profit repatriation — Profits can be freely repatriated once all Indian tax obligations are cleared; the India-Canada DTAA governs withholding tax on dividends and can reduce the overall repatriation tax cost when applied correctly

GST Compliance

GST is a separate compliance stream from corporate filings. A typical foreign-owned company registered for GST will need to manage:

- GSTR-1 — Monthly or quarterly outward supplies return

- GSTR-3B — Monthly self-declaration and net liability payment

- GSTR-9 — Annual return (mandatory; GSTR-9C reconciliation statement required if turnover exceeds INR 2 crore)

ITC mismatches, reverse charge mechanism errors, and place-of-supply issues are among the most common GST pain points for foreign-owned companies without dedicated local accounting support.

Frequently Asked Questions

Can a foreigner start a business in India?

Yes. Foreign nationals can establish a business in India under the Companies Act 2013 and India's FDI policy. Most sectors are open under the automatic route, but some require prior government approval. At least one director must be an Indian resident.

How much money is required to start a business in India?

There is no mandatory minimum authorized capital for a Private Limited Company or LLP. However, government filing fees, state stamp duty, and professional service costs apply and vary by state and authorized capital amount. Foreign founders also incur notarization, apostille, and courier costs for Canadian-origin documents. Use the MCA's fee calculator for a state-specific estimate before committing to a structure.

Can a Canadian NRI or OCI start a business in India?

Yes, and with more flexibility than a pure foreign national. NRI and OCI investment on a non-repatriation basis is treated as domestic investment at par with resident investment. Repatriation-basis investment follows standard FDI rules — confirm your specific status with a qualified advisor before choosing a structure.

Do I need to be physically present in India to register a company there?

No. The registration process is online via the MCA portal and can be completed from Canada. However, documents including passports and board resolutions must be notarized and apostilled, and at least one director must be an Indian resident throughout the company's existence.

What is the best business structure for a Canadian entering the Indian market?

A Private Limited Company (Wholly Owned Subsidiary) is the most common choice for full operational control and FDI eligibility. An LLP suits professional services businesses operating in sectors with 100% automatic-route FDI. A JV makes sense when a local partner provides strategic or regulatory access. The right structure depends on your sector, intended scale, and exit horizon.

How long does it take to register a company in India from Canada?

The MCA portal typically responds to SPICe+ submissions within 48–72 hours. The full process — covering DSC/DIN procurement, name reservation, document apostille, MCA filing, and RBI compliance — realistically takes several weeks to a few months, depending on documentation readiness and whether the ROC requests clarifications.

Conclusion

Starting a business in India from Canada is legally accessible — but it rewards founders who treat the setup phase as seriously as the business plan itself. The right entity type, properly apostilled documentation, sequential MCA and RBI filings, and a resident director in place before day one: these are the foundation the entire operation runs on — not bureaucratic formalities.

The most common failure points aren't insufficient capital or a weak business model. They're procedural:

- Wrong entity type chosen for the intended FDI structure

- FEMA reporting deadlines missed after capital inflow

- Operations launched before commencement of business is formally declared

Professional advisory at the outset — covering entity structuring, FDI compliance, and ongoing regulatory obligations — typically recovers its cost well before the first year of operations closes. For Canadian founders managing Indian corporate law, FDI policy, and cross-border tax obligations at the same time, VJM Global's team of Chartered Accountants and business setup specialists brings 30+ years of experience navigating exactly this terrain — turning a complex multi-step process into a structured, predictable setup.