Introduction

FRS 115 is Singapore's Financial Reporting Standard 115, issued by the Accounting Standards Council (ASC). It governs how companies must recognise revenue from contracts with customers.

For Singapore-incorporated companies, foreign businesses operating in Singapore, and finance professionals, this standard directly shapes what gets reported in financial statements — affecting compliance, audit outcomes, and investor confidence.

Many businesses struggle with revenue recognition compliance, particularly when applying judgment to complex contracts. ACRA has completed 194 financial statement reviews over the past decade, and revenue recognition remains one of the most frequently flagged areas of material non-compliance.

The consequences are real. In one documented case, a property developer's inconsistent application of FRS 115 resulted in ACRA enforcement action — a reminder that misapplication carries more than accounting risk.

This article explains what FRS 115 is, why it replaced earlier standards, how the five-step model works in practice, and where businesses commonly go wrong.

Key Takeaways

- FRS 115 replaced six legacy standards from 1 January 2018, creating a single principles-based framework

- All revenue must follow a five-step model: identify contract → identify obligations → determine price → allocate price → recognise when satisfied

- Recognition turns on transfer of control to the customer — not invoicing date or cash collection

- Key judgment areas include variable consideration, principal vs agent assessment, and over-time vs point-in-time recognition

- ACRA enforces compliance actively — penalties reach S$50,000, and listed companies have faced documented restatements

What Is FRS 115?

FRS 115, Revenue from Contracts with Customers, was issued by the ASC on 19 November 2014 and became effective for annual periods beginning on or after 1 January 2018. It is Singapore's equivalent of IFRS 15 issued by the International Accounting Standards Board (IASB).

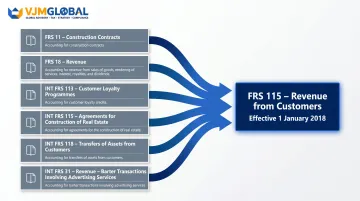

Standards Replaced by FRS 115

The standard consolidated six legacy standards and interpretations:

- FRS 11 (Construction Contracts)

- FRS 18 (Revenue)

- INT FRS 113 (Customer Loyalty Programmes)

- INT FRS 115 (Agreements for Construction of Real Estate)

- INT FRS 118 (Transfers of Assets from Customers)

- INT FRS 31 (Revenue - Barter Transactions)

This consolidation was necessary because the fragmented standards created inconsistencies across industries. Construction companies followed different rules than retailers, and technology firms applied different principles than service providers. Cross-industry comparability suffered, and auditors faced genuine uncertainty about which framework applied in mixed-contract scenarios.

Core Objective

FRS 115 establishes a single, principles-based framework for revenue recognition. Under this framework, revenue is recognised when — and to the extent that — goods or services are actually transferred to the customer. The amount recorded must reflect what the entity expects to receive in exchange for those goods or services.

Why FRS 115 Matters for Businesses in Singapore

Compliance Is Mandatory

All Singapore-incorporated companies preparing financial statements under Singapore Financial Reporting Standards must follow FRS 115. Non-compliance is subject to scrutiny by ACRA, which has enforcement powers including:

- Financial penalties up to S$50,000

- Mandatory restatement of past financial statements

- Warning letters to directors

- Prosecution (up to S$100,000 and 3 years imprisonment for fraud)

Listed companies that transitioned to SFRS(I) also adopted SFRS(I) 15, the IFRS equivalent. Both standards are substantively the same — ACRA's enforcement approach applies equally to listed and non-listed companies.

Business Impact Beyond Compliance

Incorrect revenue recognition doesn't just create audit issues—it distorts reported financial performance, affecting:

- Lending covenants and credit facility terms

- Tax computations and cash flow planning

- Earn-out arrangements in M&A transactions

- Investor valuations and equity pricing

In the 2020-2022 FRSP cycle, three listed companies restated comparatives and five listed companies plus one non-listed company had past financial statements re-audited.pdf). Four directors received warnings. These weren't accounting technicalities—they were material misstatements with real personal consequences.

Critical for Foreign Companies

Those enforcement outcomes are especially relevant for foreign entrants. Businesses from the UK, USA, Australia, or other markets setting up in Singapore must ensure their accounting policies align with FRS 115 from the moment they begin contracting with customers.

Home-country revenue policies rarely transfer without adjustment. Singapore's standard requires specific judgment on:

- Contract enforceability under Singapore law

- Currency and foreign exchange considerations

- Industry-specific applications (particularly property development, construction, and technology)

Getting this right from day one matters — misapplied policies discovered later can trigger restatements, re-audits, and the same director-level consequences documented in ACRA's enforcement cycles.

How FRS 115 Works: The Five-Step Revenue Recognition Model

Under FRS 115, revenue is recognised only when an entity satisfies a performance obligation — that is, when control of a promised good or service transfers to the customer. The standard establishes a five-step model that applies consistently to every contract, regardless of industry or transaction type.

Step 1: Identify the Contract with a Customer

A contract must meet five criteria simultaneously:

| Criterion | Description |

|---|---|

| Approval and commitment | Both parties have approved the contract and are committed to perform |

| Rights identified | Each party's rights regarding goods or services are identifiable |

| Payment terms identified | Payment terms are clearly established |

| Commercial substance | The contract changes the risk, timing, or amount of future cash flows |

| Collectability probable | It is probable the entity will collect the consideration |

Key point: Oral and implied contracts may qualify. Contracts can be combined or modified, and need reassessment at each reporting date.

Step 2: Identify the Performance Obligations in the Contract

A performance obligation is a distinct promise to transfer a good or service. Distinct means:

- The customer can benefit from it on its own or with readily available resources

- It is separately identifiable from other promises in the contract

Bundled arrangements — software plus implementation plus support, for example — must be separated if the elements are distinct. In technology and professional services contracts, this separation requires careful analysis: determining whether each element has standalone value or whether the components are so interdependent that they form a single obligation.

Step 3: Determine the Transaction Price

The transaction price is the consideration an entity expects to receive, accounting for:

- Variable consideration — discounts, rebates, bonuses, and refunds

- Significant financing components — the time value of money when payment timing differs substantially from performance

- Non-cash consideration — measured at the fair value of goods or services received

- Amounts payable to the customer — credits, vouchers, or rebates returned to them

Critical constraint: Variable consideration is included in the transaction price only to the extent it is highly probable that a significant reversal of cumulative revenue will not subsequently occur. This requires reassessment at every reporting date.

Step 4: Allocate the Transaction Price to Performance Obligations

Once the transaction price is determined, allocate it across each performance obligation in proportion to its relative standalone selling price.

Estimation approaches when standalone prices aren't observable:

- Adjusted market assessment — estimate what customers in that market would pay

- Expected cost plus margin — project costs and add an appropriate profit margin

- Residual approach — subtract the observable prices of other items from the total contract price

Step 5: Recognise Revenue When (or As) Performance Obligations Are Satisfied

With the price allocated, the final step determines when that revenue enters the books. Recognition happens either:

At a point in time — when control transfers to the customer (typically on delivery of goods)

Over time — when one of three criteria is met:

- Customer simultaneously receives and consumes the benefit as the entity performs

- Entity's performance creates or enhances an asset the customer controls

- Entity has no alternative use for the asset and has an enforceable right to payment for performance completed to date

For over-time recognition, select an appropriate progress measure and apply it consistently:

- Input methods — costs incurred, labour hours, time elapsed

- Output methods — milestones achieved, units delivered, surveys of performance

Complex Areas That Require Judgment Under FRS 115

Variable Consideration and the Constraint

Estimating the transaction price for contracts with bonuses, penalties, volume discounts, or refund rights requires either:

- Expected value method – probability-weighted sum of possible amounts (suitable for many similar contracts)

- Most likely amount method – single most likely amount (suitable for two possible outcomes)

The constraint means entities often cannot recognise the full estimated variable amount upfront. This is a departure from the simpler "probable and measurable" threshold under old FRS 18, requiring more rigorous assessment and reassessment at every reporting date.

Principal Versus Agent

When a third party is involved in delivering goods or services, determine whether the entity is:

- Principal – controls the specified good or service before transfer (records gross revenue)

- Agent – merely arranges for another party to provide it (records net commission)

Three indicators guide this assessment:

- Primary responsibility for fulfilling the contract with the customer

- Inventory risk before or after the customer places an order

- Discretion in establishing the price charged to the customer

These indicators inform — but do not override — the fundamental control principle. ACRA and international regulators frequently scrutinize this area during reviews.

Contract Costs

Once the entity's role is established, the next question is how to treat costs incurred to win and fulfill that contract.

Costs to obtain a contract (sales commissions, for example):

- Capitalise as an asset if incremental and expected to be recovered

- Amortise over the expected customer relationship period

Costs to fulfil a contract:

- Capitalise only if they generate or enhance resources used to satisfy future performance obligations and are expected to be recovered

- Expense all other costs as incurred

This differs from previous practice under FRS 11, where most contract costs were capitalised as work-in-progress.

Percentage of Completion for Long-Term Contracts

For performance obligations satisfied over time — common in construction, IT projects, and managed services — entities must select and consistently apply a measure of progress.

Method choice has real P&L consequences:

- Input method: periodic margin tends to be stable across reporting periods

- Output method: margins can fluctuate significantly based on milestone achievement

ISCA guidance is clear on one point: progress payments claimed are not an appropriate measure of completion. Entities must assess actual performance, not billing activity.

Contract Modifications and Variable Pricing

When a contract is modified (scope change, price variation), assess whether it represents:

- A new separate contract (additional goods/services at standalone selling prices)

- A modification of the existing contract (requires adjustment to revenue recognition)

This applies most often in construction and technology sectors, where change orders and scope variations are routine.

Common Misconceptions About FRS 115

Misconception: Revenue Can Be Recognised When Invoiced or Cash Received

In practice, FRS 115 is entirely control-based — not cash- or invoice-based. Many businesses, especially smaller ones, incorrectly assume their billing cycle determines revenue timing. Revenue is recognised when the performance obligation is satisfied, which may occur before, at, or after invoicing or cash receipt.

Misconception: FRS 115 Only Affects Construction or Long-Term Contract Businesses

The standard applies to all industries and all contract types, including:

- Retail sales (warranties, loyalty programmes)

- SaaS subscriptions (upfront fees, implementation services)

- Professional services (retainers, milestone billing)

- Licensing arrangements (intellectual property transfers)

- Franchising agreements (initial fees versus ongoing royalties)

Every entity with customer contracts must apply the five-step model regardless of contract length or complexity.

Even businesses already familiar with FRS 115's scope often underestimate the standard's ongoing demands.

Misconception: FRS 115 Was a One-Time Implementation Exercise

The standard requires active judgment at every reporting period, including:

- Reassessing variable consideration estimates

- Reviewing contract modifications

- Updating progress measures for over-time recognition

- Testing capitalised contract costs for impairment

- Evaluating new contract types against the five-step model

It is a continuous process, not a one-time implementation exercise.

Conclusion

FRS 115 replaces fragmented legacy standards with a single, principles-based five-step model that ensures revenue is recognised in a way that faithfully reflects how goods and services are transferred to customers. This standardisation improves comparability across industries and jurisdictions, but it also requires rigorous, ongoing judgment.

Misapplication of FRS 115 affects financial reporting accuracy, regulatory compliance, and business credibility — and ACRA's active enforcement programme demonstrates that non-compliance has real consequences, from financial penalties to director warnings and mandatory restatements.

For foreign companies operating in Singapore, getting this right from the outset is essential. Firms that already manage cross-border accounting obligations — including those working with advisors like VJM Global, who support foreign companies with full-cycle financial reporting across multiple jurisdictions — benefit from pairing local Singapore expertise with a compliance partner who understands international reporting frameworks end to end.

Frequently Asked Questions

What is the accounting standard for revenue recognition in Singapore?

FRS 115, Revenue from Contracts with Customers, is the governing standard for revenue recognition in Singapore. Issued by the Accounting Standards Council, it has been effective from 1 January 2018 for all annual reporting periods.

What standards did FRS 115 replace in Singapore?

FRS 115 replaced FRS 11 (Construction Contracts), FRS 18 (Revenue), and several related interpretations including INT FRS 113, INT FRS 115, INT FRS 118, and INT FRS 31. This brought previously fragmented industry-specific guidance under a single, consistent framework.

Does FRS 115 apply to all companies in Singapore?

FRS 115 applies to all Singapore-incorporated companies preparing financial statements under Singapore FRS. Key exceptions include lease contracts (FRS 116), insurance contracts, and financial instruments — each governed by their own dedicated standards.

When is revenue recognised over time versus at a point in time under FRS 115?

Revenue is recognised over time if any one of three conditions is met: the customer simultaneously receives and consumes the benefit, the customer controls the asset as it is created, or the entity has an enforceable right to payment for work with no alternative use. If none of these apply, revenue is recognised at the point control transfers.

How does FRS 115 treat variable consideration such as discounts or performance bonuses?

Entities estimate variable consideration using either the expected value or most likely amount method. It can only be included in the transaction price when it is highly probable that a significant revenue reversal will not occur later.

What is SFRS(I) 15 and how does it relate to FRS 115?

SFRS(I) 15 is the IFRS-identical equivalent of FRS 115, applicable to Singapore-listed companies that adopted the IFRS-aligned framework from 1 January 2018. The requirements are identical in practice to both FRS 115 and IFRS 15.