Introduction

Institutions of a Public Character (IPCs) in Singapore operate under a privileged framework established by the Charities Act, granting them the authority to issue tax-deductible receipts for donations. This status makes IPCs highly attractive to major donors and corporate giving programs. That privilege, however, comes with rigorous audit and governance obligations that every governing board must understand and fulfill.

IPC administrators routinely wrestle with the same questions: Which audit thresholds apply? What do auditors actually examine? What happens when something goes wrong?

According to the Commissioner of Charities Annual Report 2023, while 97% of charities submit their annual returns on time, the remaining 3% face escalating enforcement actions — from formal warnings to potential revocation of IPC status. For charity leaders and finance teams, the cost of not knowing the rules is simply too high.

This guide walks through IPC audit thresholds, what auditors examine, how to choose a qualified auditor, and the penalties for getting it wrong.

Key Takeaways

- All IPCs must use COC-approved public accountants registered with ACRA, regardless of income level

- Large IPCs ($10M+ receipts, 2 consecutive years) require 10+ board members and mandatory auditor rotation

- Audits verify financial accuracy, the 80% donation spending rule, and Code of Governance adherence

- Annual submissions are due within 6 months of financial year-end; late filing risks fines up to $10,000

- Auditor rotation applies to all IPCs every 5 years and requires prior COC/Sector Administrator approval

What Is an IPC in Singapore?

An Institution of a Public Character (IPC) is a status granted by the Commissioner of Charities (COC) under Section 40 of the Charities Act 1994 to eligible registered charities. The Charity Portal defines IPC as "a status accorded to a registered charity or an exempt charity for a period of time," distinguishing it from permanent registration.

Key Characteristics:

- Operate across social services, healthcare, education, arts and heritage, sports, environment, and religious sectors

- Must exclusively benefit the local Singapore community — benefits cannot be confined to sectional interests based on race, belief, or religion (unless a ministerial waiver is granted)

- Strictly prohibited from conducting activities that benefit overseas communities

The primary privilege distinguishing IPCs from regular charities is the ability to issue tax-deductible donation receipts. IRAS confirms that qualifying donations to approved IPCs receive a 250% (2.5x) tax deduction, extended until 31 December 2026. This means for every S$1 donated, S$2.50 can be deducted from taxable income — making IPCs highly attractive to corporate and individual donors.

IPC Status Is Not Permanent:

IPC status must be renewed periodically. The Sector Administrator determines renewal length based on the IPC's compliance with the Code of Governance for Charities and IPCs. IPCs with Governance Evaluation Checklist (GEC) scores above 80% (minimum 61 points) receive more favorable renewal terms.

As of 31 December 2023, approximately 647–649 IPCs operate within Singapore's charity sector of 2,331 registered charities.

Who Must Comply with IPC Audit Requirements in Singapore?

Universal Audit Requirement for All IPCs

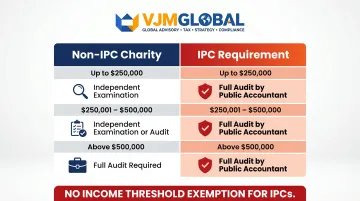

Unlike non-IPC charities, ALL IPCs must have their financial statements audited by a public accountant, regardless of income level. The standard $500,000 threshold that determines audit requirements for non-IPC charities does not apply to IPCs.

Audit Requirements by Entity Type:

| Gross Income/Expenditure | Non-IPC Charity | IPC Requirement |

|---|---|---|

| Up to $250,000 | Independent examination | Full audit by public accountant |

| $250,001 - $500,000 | ISCA member examination | Full audit by public accountant |

| Above $500,000 | Full audit | Full audit by public accountant |

This universal audit requirement applies to all IPCs, as confirmed by Regulation 17(1) of the Charities (IPC) Regulations.

Large IPC Classification and Additional Requirements

A "large charity/IPC" is defined as one with gross annual receipts of not less than $10 million in each of the last 2 financial years immediately preceding the current financial year. Gross annual receipts include all income, grants, donations, and sponsorships.

Three Additional Obligations for Large IPCs:

- Board Size Floor: Maintain at least 10 governing board members — if headcount drops below this, notify the Sector Administrator immediately and restore the count within 6 months

- Approved Auditor Pool Only: Appoint auditors from those specifically approved by the Commissioner of Charities or the relevant Sector Administrator — not all licensed public accountants qualify

- Mandatory Rotation Deadline: Switch audit firms at least once every 5 years; approval must be obtained through the Charity Portal before the new appointment takes effect

One of these obligations — the 5-year rotation — extends beyond large IPCs and applies to every IPC.

Critical Clarification: 5-Year Rotation Applies to ALL IPCs

The MCCY Charities Unit confirms that "a large charity or an Institution of a Public Character (IPC) must change its auditor at least once every 5 years." Despite the wording, this 5-year rotation requirement applies to ALL IPCs — not just large ones. Every IPC must track and act on this deadline, which means:

- Tracking auditor tenure from appointment date

- Submitting the Auditor Declaration Form via Charity Portal before the 5-year deadline

- Obtaining COC or Sector Administrator approval before the new appointment takes effect

Annual Filing Obligations

All IPCs must file their annual submissions through the Charity Portal within 6 months of their financial year-end. Required documents include:

- Annual Report (including audited financial statements)

- Governance Evaluation Checklist (GEC)

- Online Financial Summary (OFS)

- Tax-deductible donation details (filed with IRAS by 31 January annually)

Non-compliance can trigger regulatory penalties or suspension of IPC status — both of which directly affect an organization's ability to issue tax-deductible receipts to donors.

Key IPC Audit Requirements Under Singapore Law

Compliance with Charities Accounting Standards (CAS)

The Charities Accounting Standard (CAS) was issued by the Accounting Standards Council (ASC) in 2011 as an alternative financial reporting framework specifically developed for charities. IPCs may choose between CAS and Singapore Financial Reporting Standards (SFRS) based on their size and complexity.

Framework Selection:

- Smaller IPCs: May apply CAS, a simplified standard tailored to charity circumstances with focus on fund accounting and resource management

- Large IPCs ($10M+ threshold): Must use full SFRS(I) under Regulation 20(1) of the Charities (IPC) Regulations, ensuring compliance with the Accounting Standards Act 2007

Auditor Approval and Rotation Rules

The COC or Sector Administrator must approve the auditor appointed by an IPC before the appointment takes effect. IPCs cannot unilaterally appoint any registered public accountant without this prior approval — a safeguard that protects against conflicts of interest in the charity sector.

Application Process:

- Log in to the Charity Portal at www.charities.gov.sg

- Click "Update Charity Profile"

- Download the "Auditor Declaration Form" under "Appointment of Auditor (for IPCs or Large Charities)"

- Complete and submit the form via the Portal

- Await COC/SA review and approval notification

5-Year Rotation in Practice:

Per Section 5(2) of the Charities (Large Charities) Regulations, IPCs must change their auditor at least once every 5 years. The rotation can occur within the same audit firm (changing the individual auditor) or to a different audit firm. Either way, COC/SA approval must be secured before the new auditor begins work. Start succession planning at least 6 months before the deadline — approval processing takes time, and gaps in audit coverage can create compliance risk.

Annual Submission Deadlines

Annual submissions must be filed within 6 months from the end of each financial year. All documents are published on the Charity Portal for public viewing to promote transparency.

Penalties for Non-Compliance:

Contravention is an offence punishable by:

- Fine of up to $10,000

- Imprisonment of up to 3 years

- Or both

Persistent non-compliance can also trigger suspension or revocation of IPC status under Regulation 6 of the Charities (IPC) Regulations, exposing the IPC to both criminal prosecution and loss of tax-deductible donation status.

Set an internal filing deadline at least 2 months ahead of the 6-month cutoff to leave room for auditor queries, document preparation, and portal submission.

What Does an IPC Audit Cover?

An IPC audit covers far more than standard financial statement verification. It spans financial accuracy, governance compliance, donation management, and fund usage — each area tied to the IPC's specific obligations to the public and regulators.

Financial Statements and Fund Usage

Auditors examine the full financial picture, including:

- Verification of all income sources (donations, grants, fundraising receipts, program fees)

- Examination of expenditures, assets, and liabilities

- Tracing restricted versus unrestricted fund usage to ensure donor intent is honored

- Confirmation that funds are deployed exclusively for charitable purposes in Singapore

The CAS framework requires clear distinction between restricted, unrestricted, and designated funds. Auditors verify that donor-imposed conditions are respected and that the IPC's governing instruments are followed.

Where donations cannot be used for their intended purpose, charities face a 4-year refund requirement — or must seek Sector Administrator approval to redirect those funds.

Governance and Donation Compliance

The governance review covers:

- Adherence to the Code of Governance for Charities and IPCs (all IPCs classified as Tier 2)

- Board composition and minimum membership requirements

- Review of board meeting minutes and documentation

- Verification that the IPC is not in breach of any conditions attached to its IPC approval

- Conflict-of-interest declarations and documentation

- Board tenure compliance (members exceeding 10 years require justification)

On the donations side, auditors confirm that:

- Tax-deductible receipts contain all required information

- Donation records are complete, accurate, and properly maintained

- The IPC complies with the 80% spending rule

The 80% Spending Rule

Regulation 11(2) of the Charities (IPC) Regulations requires that an IPC must ensure at least 80% of donations received are spent on its charitable objects in Singapore within its financial year, or such other period as the Sector Administrator may allow.

A related rule applies to fundraising costs. Regulation 15(1) stipulates that total expenses incurred in a fundraising appeal must not exceed 30% of total receipts from that appeal. IPCs accumulating reserves or requiring extensions should seek Sector Administrator approval and document their reserves policy clearly.

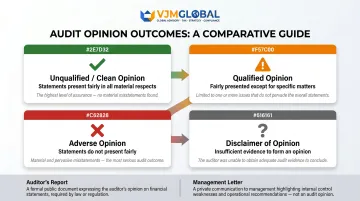

Audit Deliverables

Independent Auditor's Report — the formal opinion submitted to the COC. There are four possible outcomes:

- Unqualified (clean): Financial statements present fairly in all material respects

- Qualified: Except for specific matters, statements are fairly presented

- Adverse: Statements do not present fairly

- Disclaimer: Auditor unable to obtain sufficient evidence to form an opinion

Management Letter — documents internal control weaknesses and governance gaps for board action. Unlike the auditor's report, this letter is forward-looking: it gives the board a concrete list of issues to address before the next audit cycle.

How to Choose an Auditor for Your IPC

Primary Registration Requirement

The auditor must be a public accountant registered with the Accounting and Corporate Regulatory Authority (ACRA) under the Accountants Act. ACRA maintains the official register of public accountants, which can be verified at www.acra.gov.sg.

Prior approval from the COC or relevant Sector Administrator must be obtained before the auditor appointment takes effect. Meeting the registration threshold is the baseline — what separates a capable IPC auditor from a compliant one comes down to sector-specific experience.

Qualities That Make an Auditor Suitable for IPC Work

Beyond Technical Registration:

- Familiar with the Charities Accounting Standard (CAS) and all 6 principles of the Code of Governance for Charities and IPCs

- Has prior audit engagements with charitable or nonprofit organizations

- Delivers actionable management letter insights — not just compliance sign-offs

- Experienced with restricted vs. unrestricted fund tracking and donor-imposed conditions

- Aware of COC enforcement priorities and common compliance failure patterns

Planning for the 5-Year Rotation

Given the mandatory 5-year rotation rule, IPCs should plan ahead when their current auditor approaches the end of their permitted tenure. Allow sufficient lead time to:

- Identify potential replacement firms with charity sector experience

- Evaluate their qualifications and service approach

- Obtain COC/SA approval through the Charity Portal

- Transition engagement smoothly without disrupting annual filing deadlines

Starting this process 6–12 months before the rotation deadline gives your IPC enough time to vet candidates and secure approval without pressure. Advisory firms with cross-border compliance experience — such as VJM Global, a member of EAI International — can support the selection and approval process when internal resources are limited.

Common IPC Audit Compliance Mistakes to Avoid

Incomplete Documentation

The most frequent failure flagged during audits is missing or incomplete governance and training records:

- Board meeting minutes lacking required detail

- Conflict-of-interest declarations not documented or filed

- Donation register logs with gaps or missing information

- Fundraising appeal expense documentation incomplete

Even when practices themselves are solid, documentation gaps create audit qualifications and draw regulatory scrutiny.

Auditor Approval and Rotation Failures

Procedural missteps here are more common than most IPCs expect:

- Appointing or retaining an auditor without obtaining COC/SA approval first

- Failing to initiate the rotation process before the 5-year limit expires

- Not tracking auditor tenure from initial appointment date

- Assuming rotation only applies to large IPCs

These failures trigger regulatory scrutiny and can delay annual submission timelines, leading to follow-up reviews and submission backlogs.

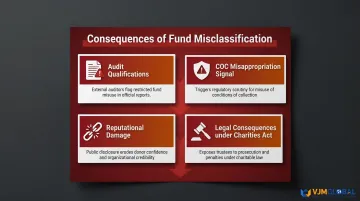

Misclassification of Restricted and Unrestricted Funds

Beyond process failures, financial reporting errors carry their own consequences. Incorrectly classifying funds in financial statements causes:

- Audit qualifications that require explanation to donors and regulators

- Potential signals of donation misappropriation to the COC

- Reputational damage if publicly disclosed

- Legal consequences under the Charities Act

IPCs must maintain clear fund accounting systems that track donor-imposed restrictions and demonstrate compliance with the 80% spending rule. This matters most for organizations managing multiple programs or multi-year grants.

Frequently Asked Questions

What is an IPC in Singapore?

An IPC (Institution of a Public Character) is a status granted by the Commissioner of Charities to eligible registered charities in Singapore under the Charities Act. It allows them to issue tax-deductible donation receipts, and is subject to strict governance and audit obligations that must be renewed periodically.

When is an IPC required to have its accounts audited?

All IPCs must have their accounts audited annually by a COC-approved public accountant registered with ACRA, regardless of income level. The $500,000 threshold that applies to non-IPC charities does not exempt smaller IPCs from the audit requirement.

How often must an IPC change its auditor in Singapore?

Under Singapore's Charities Act regulations, all IPCs must rotate their audit firm at least once every 5 years. The new appointment requires prior approval from the COC or relevant Sector Administrator via the Charity Portal before the auditor can commence work.

What documents are required for an IPC audit in Singapore?

Key documents include:

- Financial statements and bank records with reconciliations

- Donation registers and tax-deductible receipt logs

- Board meeting minutes

- Grant agreements and fund-use records

- Governance documentation (conflict-of-interest declarations, reserves policy)

- Fundraising appeal expense documentation

What happens if an IPC fails to submit its audited financial statements on time?

Late or missing annual submissions can result in:

- Fines up to S$10,000

- Imprisonment up to 3 years

- Suspension or revocation of IPC status

- Public disclosure of non-compliance by the COC

Who can conduct an IPC audit in Singapore?

The auditor must be a public accountant registered with ACRA and must be specifically approved by the COC or relevant Sector Administrator before being appointed. IPCs cannot unilaterally appoint any public accountant without this prior approval obtained through the Charity Portal.