Introduction

Singapore's position as one of Asia's leading cross-border business hubs means companies here routinely make payments to non-resident entities—for IP licenses, consulting services, loan interest, or management fees. Every such payment carries a potential withholding tax (WHT) obligation under Section 45 of the Income Tax Act, requiring the local payer to deduct a specified percentage and remit it directly to IRAS.

Many finance teams know WHT exists but struggle with the mechanics: Is it a liability, an expense, or both? What if the contract requires the payer to "gross up" and bear the tax? Errors in recording WHT—or in the timing of recognition—can result in misstated liabilities, compliance penalties, and lost deductions.

Year-end accruals and deemed payment triggers add another layer of complexity that catches even experienced teams off guard.

This guide covers which payments trigger WHT, the correct journal entries, deductibility rules for payers and payees, and how DTA relief applies.

Key Takeaways

- WHT applies to specific cross-border payments (interest, royalties, technical fees, management fees) made to non-residents, with rates ranging from 10% to 24% depending on payment type.

- The payer is responsible for deducting WHT and remitting it to IRAS by the 15th of the second month following payment or deemed payment.

- In the payer's books, WHT is a liability (WHT Payable), not an expense—the full gross payment remains the deductible expense.

- WHT is a final tax for passive income (interest, royalties); for technical/management fees, it's non-final and the non-resident can file a return to claim deductions.

- Singapore's 80+ DTAs can reduce or eliminate WHT rates for qualifying residents holding a valid Certificate of Residence.

What Is Withholding Tax in Singapore?

Withholding tax is a source-based collection mechanism under Section 45 of the Income Tax Act that requires a Singapore payer to deduct a percentage of certain payments made to non-resident companies or individuals and remit that amount directly to IRAS. This ensures Singapore collects tax on income sourced locally, even when earned by overseas entities.

Final vs. Non-Final WHT

WHT treatment depends on the nature of the payment:

Final WHT applies to passive income when the non-resident operates entirely from overseas:

- Interest on loans or indebtedness: 15%

- Royalties for intellectual property use: 10%

- Rental of movable property: 15%

The non-resident has no further Singapore tax filing obligation: the WHT amount is the final, settled tax liability.

Non-final WHT applies to service-based payments physically performed in Singapore:

- Technical assistance and management fees: 17% (the prevailing corporate income tax rate)

Here, the non-resident can file a Singapore tax return (Form C) and claim deductions for expenses incurred in earning that income. If those expenses reduce net taxable income below the amount withheld, IRAS will issue a refund for the difference.

WHT vs. Singapore Corporate Income Tax

Singapore's corporate income tax rate is 17%. WHT is not an additional tax layer—it is a collection mechanism applied at the point of payment to non-residents. For Singapore-resident businesses, the accounting treatment differs: WHT is not the payer's own tax expense — it is a liability representing the non-resident's tax obligation, collected at source on their behalf.

Who Must Withhold Tax in Singapore?

The "Payer"

Any person or entity—individual, company, or partnership—resident in Singapore or operating through a Singapore branch must withhold tax on specified payments to non-residents. This includes the Singapore branch of a foreign company making payments to its own overseas head office, which can still trigger WHT obligations.

Defining "Non-Resident"

A payee qualifies as non-resident if they fall into one of these categories:

- Companies where control and management are exercised outside Singapore — IRAS applies this test based on where the board makes strategic decisions, not where the company is incorporated. A Singapore-incorporated company managed from overseas is still non-resident.

- Individuals physically present in Singapore for fewer than 183 days in a calendar year

- Independent professionals (contractors or consultants) who meet the same 183-day threshold

- Directors of Singapore companies who do not meet the residency threshold

Key Exemption: Singapore Branches

One important carve-out: payments made to the Singapore branch of a non-resident company are not subject to WHT. Because the branch must include this income in its own annual Corporate Income Tax Return filed with IRAS, separate withholding is unnecessary.

Payments Subject to Withholding Tax and Applicable Rates

Payment Categories Under Sections 12(6) and 12(7)

The following payments to non-resident companies, as defined under Sections 12(6) and 12(7) of the Income Tax Act, trigger WHT obligations:

- Interest, commissions, or fees on loans or indebtedness

- Royalties or payments for the use of intellectual property or movable property

- Technical assistance and service fees for work performed in Singapore

- Management fees for services rendered in Singapore

- Rent or payments for the use of movable property

- REIT distributions to non-resident non-individuals

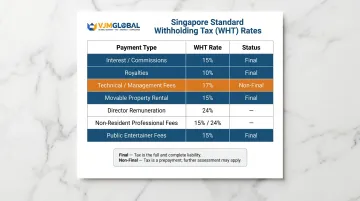

Standard WHT Rates (Non-Treaty)

| Payment Type | WHT Rate | Final/Non-Final |

|---|---|---|

| Interest, commissions, loan fees | 15% | Final |

| Royalties (IP, movable property use) | 10% | Final |

| Technical/Management service fees (work in Singapore) | 17% | Non-final |

| Rental of movable property | 15% | Final |

| Non-resident director remuneration | 24% | Varies |

| Non-resident professional fees | 15% on gross or 24% on net | Non-final |

| Public entertainer fees | 15% | Final |

Rights-Based Approach to Software Payments

In 2013, IRAS adopted a rights-based framework to characterize software and digital goods payments:

- "Copyright right" (WHT applies): The payer acquires rights to commercially exploit the software—e.g., reproduce, modify, distribute to customers. Treated as a royalty subject to 10% WHT.

- "Copyrighted article" (no WHT): The payer acquires software for internal business use only, such as off-the-shelf accounting software or shrink-wrapped licenses. Not treated as a royalty.

Example:

A Singapore retailer purchasing accounting software for internal bookkeeping pays no WHT. A Singapore company licensing CRM software to resell to its own clients pays 10% WHT on the license fee.

Apportionment Rule for Services

Beyond IP payments, service fees carry their own apportionment rules. Only the portion of fees attributable to work physically performed in Singapore is subject to WHT at 17%. Services rendered entirely from overseas via email, phone, or internet are not subject to WHT.

Example:

A consultant invoices SGD 100,000 for a project. If documentation shows 60% of work (man-days) was performed in Singapore and 40% overseas, WHT applies to SGD 60,000 at 17% = SGD 10,200.

Withdrawal of Cost Reimbursement Concession (November 2022)

This is a compliance update that caught many related-party arrangements off-guard. Effective 1 November 2022, the administrative concession that exempted cost reimbursements (accommodation, meals, transport) and cost-pooling arrangements between related parties was withdrawn. Any such reimbursements to a non-resident related party are now subject to WHT.

Withholding Tax Accounting Treatment in Singapore

Core Accounting Principle

For the payer, WHT is not an expense: it is a tax collected on behalf of IRAS from the non-resident payee. It is recorded as a current liability (WHT Payable) in the payer's balance sheet at the date of accrual and extinguished when remitted to IRAS. The gross expense (interest, royalties, service fees) is recognized at the full contractual amount.

Accounting Entry: Payer's Perspective

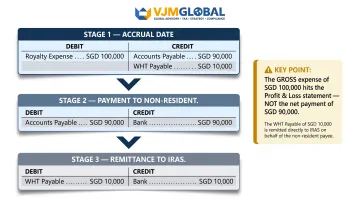

Consider a Singapore company accruing a royalty payment of SGD 100,000 to a non-resident company (non-treaty jurisdiction, 10% WHT rate):

At accrual date:

Dr: Royalty Expense SGD 100,000

Cr: Accounts Payable (to non-resident) SGD 90,000

Cr: WHT Payable (to IRAS) SGD 10,000

At payment to non-resident:

Dr: Accounts Payable SGD 90,000

Cr: Bank SGD 90,000

At remittance to IRAS:

Dr: WHT Payable SGD 10,000

Cr: Bank SGD 10,000

Critical point: The royalty expense in the profit & loss statement is SGD 100,000 (gross), not SGD 90,000. The WHT payable is a balance sheet liability, not a P&L expense.

Gross-Up Arrangements

When the payer contractually agrees to "gross up", the payer bears the WHT so the payee receives the full contracted amount. The additional WHT borne becomes an incremental cost.

Gross-up calculation:

If the payable to the non-resident is SGD 90,000 net (after 10% WHT):

Gross Amount = Net Amount ÷ (1 – WHT rate)

= SGD 90,000 ÷ 0.90

= SGD 100,000

WHT remitted to IRAS = SGD 10,000 (borne by payer)

Journal entry (gross-up scenario):

Dr: Royalty Expense SGD 100,000

Cr: Accounts Payable (to non-resident) SGD 90,000

Cr: WHT Payable (to IRAS) SGD 10,000

Note: this entry is structurally identical to the standard accrual above because the gross amount happens to equal SGD 100,000 in both scenarios. In practice, a gross-up on a SGD 90,000 net fee yields a higher gross base — the key difference is how that gross figure is derived, not how it is journaled. The payer cannot recover the WHT borne; it is an additional cost of obtaining the service.

Non-Resident Payee's Accounting

From the payee's side, the accounting treatment depends on whether the WHT is final or non-final. The non-resident records the gross income (SGD 100,000) as revenue. The WHT withheld (SGD 10,000) is treated as:

- For final WHT (interest, royalties): A prepayment or settled tax. No further Singapore filing required.

- For non-final WHT (technical/management fees): Tax paid on account. The non-resident files a Singapore tax return to claim deductible expenses and potentially recover excess WHT.

Timing of WHT Recognition and Deemed Payment

WHT becomes a liability at the earlier of:

- Date of actual cash payment to the non-resident

- Deemed payment: when the amount is credited to the payee's account or offset against an amount owed by the payee

Balance sheet implication: Companies with year-end accruals for non-resident fees must recognize the corresponding WHT liability even if cash has not yet been paid. This ensures compliance with the accrual concept under financial reporting standards.

Deferred Tax Considerations

WHT payable is a current liability with no deductibility timing differences for the payer: it is not the payer's own tax. Therefore, no deferred tax asset or liability is typically created in the payer's books for the WHT itself.

However, if a gross-up arrangement increases the payer's deductible expense, this may affect the payer's deferred tax calculation. Structures involving back-to-back arrangements, hybrid instruments, or variable royalty bases warrant separate tax advice.

Is Withholding Tax Expense Deductible in Singapore?

From the Payer's Perspective

The WHT remitted to IRAS is not deductible by the payer as a business expense—it is the non-resident's tax obligation, not the payer's own expense. The deductible amount for the payer is the full gross payment (interest, royalties, service fees), provided it meets the general deductibility conditions under Section 14 of the Income Tax Act: wholly and exclusively incurred in producing income.

Gross-Up Deductibility

When the payer contractually bears the WHT via a gross-up arrangement, the additional tax amount becomes an incremental cost of that service or payment. This additional amount is deductible as part of the total expense—but IRAS scrutinizes such arrangements to ensure they are at arm's length, particularly for related-party transactions.

Example:

A Singapore company pays SGD 110,000 total (SGD 100,000 net to consultant + SGD 10,000 WHT borne by payer). The deductible expense is SGD 110,000, subject to transfer pricing rules for related parties.

From the Non-Resident's Perspective

For non-final WHT (technical/management fees at 17%):

The non-resident can file a Singapore tax return and claim deductions for expenses incurred in deriving Singapore-sourced income. The net tax liability is assessed on net income, and any over-withheld amount is refunded by IRAS.

For final WHT (interest at 15%, royalties at 10%):

No expense deduction is available. The WHT is the full and final liability — no further deductions apply.

These distinctions matter for treaty planning, since DTA agreements can shift the economics of both scenarios.

DTA Impact on Deductibility Planning

Where a Double Tax Agreement (DTA) applies, reduced WHT rates lower gross-up costs for the payer. For example, a payer making royalty payments to a German non-resident benefits from a 5% DTA rate (reduced from the standard 10%), halving the WHT cost.

To qualify for treaty relief, companies should verify DTA availability and require the non-resident to provide a Certificate of Residence (COR) from their home tax authority before making payment. Applying the wrong rate — or missing the COR requirement entirely — can result in under-withholding, penalties, and interest charges from IRAS.

Filing, Payment, and DTA Relief for Withholding Tax

Filing and Payment Deadline

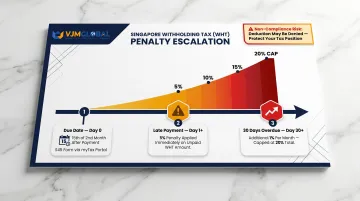

WHT must be filed and paid to IRAS by the 15th of the second month following the date of payment (or deemed payment) to the non-resident. Filing is done via the S45 Form on IRAS's myTax Portal.

Late payment penalty: 5% of the unpaid WHT amount. If payment remains outstanding 30 days after the due date, an additional penalty of 1% per month applies (up to a maximum total of 20%).

Non-compliance can also result in denial of the deduction for the payer's related expense — a separate cost that compounds the penalty exposure.

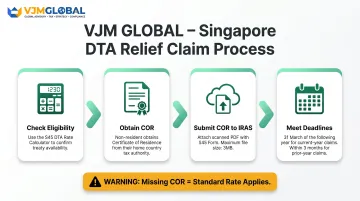

How to Claim DTA Relief

Singapore has over 80 comprehensive DTAs that can reduce applicable WHT rates. To apply treaty rates:

- Check eligibility using the S45 Double Taxation Relief Tax Rate Calculator

- Obtain a Certificate of Residence (COR) from the non-resident's home tax authority

- Submit the COR to IRAS together with the S45 Form (upload scanned PDF, max 3MB)

- COR submission deadlines:

- For claims in the current calendar year: by 31 March of the following year

- For prior year claims: within 3 months of the WHT submission date

The COR must be in English (or translated) and clearly state that the non-resident is a resident of that jurisdiction for DTA purposes.

If the COR is not submitted in time, the payer must withhold at the standard (higher) rate, and the non-resident must separately apply to IRAS for a refund of the excess tax withheld.

Common Compliance Errors to Avoid

- Withholding tax on services performed in Singapore even when the non-resident issues an overseas invoice — the trigger is where the services are performed, not where the invoice originates

- Applying reduced treaty rates without first obtaining a valid, current COR

- Overlooking the deemed payment trigger when fees are credited, offset, or set off rather than paid in cash

- Miscalculating gross-up amounts, resulting in under-withholding on payments where the payer absorbs the WHT

Foreign companies entering Singapore for the first time often encounter these errors simply because local WHT mechanics differ significantly from their home jurisdictions. Working with a Singapore-experienced tax compliance adviser from the outset is the most direct way to stay clean with IRAS.

Frequently Asked Questions

What is the accounting treatment for withholding tax?

The payer records the full gross payment as an expense (debit) and splits the credit between a net payable to the non-resident and a WHT Payable liability to IRAS. The WHT is not an expense of the payer—it is a liability representing the non-resident's tax collected at source.

Is withholding tax expense deductible in Singapore?

The WHT remitted to IRAS is not deductible as the payer's own expense. However, the full gross payment — interest, royalties, or service fees — remains deductible if it meets Singapore's general deductibility conditions. Where the payer bears WHT through a gross-up arrangement, that additional cost is also deductible as part of the total payment.

How does withholding tax work in Singapore?

A Singapore payer deducts a specified percentage (ranging from 10% to 24% depending on payment type) from payments made to non-resident companies or individuals, and remits that amount to IRAS by the 15th of the second month following payment. The non-resident receives only the net amount. For non-final WHT, they may file a Singapore tax return to recover any excess tax paid.

What is the deadline for filing and paying withholding tax in Singapore?

WHT must be filed and paid to IRAS by the 15th of the second month following the date of payment or deemed payment to the non-resident, using the S45 Form on the myTax Portal. Late payment attracts a 5% penalty on the outstanding amount.

Can a Double Tax Agreement reduce withholding tax obligations in Singapore?

Singapore's network of 80+ DTAs can reduce or eliminate WHT rates on interest, royalties, and certain service fees. The non-resident must provide a valid Certificate of Residence from their home tax authority to the Singapore payer for treaty rates to apply.

What happens if withholding tax is not paid on time in Singapore?

IRAS imposes a 5% late payment penalty on the unpaid WHT amount, plus an additional 1% per month if payment remains outstanding beyond 30 days (maximum total penalty: 20%). Continued non-compliance can lead to further penalties, and the payer may lose the right to deduct the related expense in their corporate tax computation.