Key Takeaways

- VAT returns and payments are due one calendar month and seven days after the end of each accounting period

- Most businesses file quarterly, but monthly and annual options exist under specific schemes

- All VAT-registered businesses must use MTD-compatible software — paper returns are no longer permitted

- Late submissions trigger a points-based penalty system, with a £200 penalty once the threshold is reached

- Payment must clear HMRC's account by the deadline — including when the due date falls on a weekend or bank holiday

What Is a UK VAT Return and Who Needs to File One?

A UK VAT return is a form submitted to HMRC that reports two figures: the VAT a business has charged its customers (output VAT) and the VAT it has paid to its suppliers (input VAT). The difference is either paid to HMRC or reclaimed from them.

Who Must Register

Businesses must register for VAT once their taxable turnover exceeds £90,000 in the previous 12 months, or if they expect to exceed that figure within the next 30 days. Once the threshold is crossed, registration must be completed within 30 days of the end of the month when it happened.

Voluntary registration is also available for businesses trading below £90,000 — useful if you want to reclaim input VAT on purchases. Check the current threshold on GOV.UK before registering, as HMRC updates this periodically.

Overseas businesses should note: HMRC VAT Notice 700/1 confirms that the standard registration threshold does not apply to non-established taxable persons (NETPs). Foreign companies making any taxable supplies in the UK must register regardless of turnover value.

Filing Obligations

- VAT-registered businesses must file a return for every accounting period, even if no VAT is owed or reclaimable — this is called a nil return

- Overseas businesses selling taxable goods or services in the UK may also need to register and file

- VAT returns have different deadlines and submission routes from Corporation Tax and Self-Assessment filings

UK VAT Return Deadlines Explained

The core rule is straightforward: both the VAT return submission and the payment are due one calendar month and seven days after the end of the VAT accounting period.

Example: If your quarter ends 31 March, the return and payment are due by 7 May.

Standard Quarterly VAT Deadlines

The table below applies HMRC's one month plus seven days rule to the four standard quarterly periods:

| Quarter End | Submission Deadline | Payment Due |

|---|---|---|

| 31 March | 7 May | 7 May |

| 30 June | 7 August | 7 August |

| 30 September | 7 November | 7 November |

| 31 December | 7 February (next year) | 7 February (next year) |

Critical: These dates do not shift for weekends or bank holidays. Payment must clear HMRC's account on or before the stated date.

Direct Debit Exception

Businesses paying by Direct Debit get an advantage over other payment methods. HMRC collects payment automatically — but three rules apply:

- Payment is collected three working days after the submission deadline on the return

- The Direct Debit must be set up at least three working days before you file

- If filed late, collection occurs three working days after that late filing date — this does not stop late submission penalty points from building up

Your Specific Quarter Dates

Beyond payment method, your actual quarter end dates may differ from the standard calendar above. Your VAT quarter start date depends on when you originally registered. Check your VAT online account to confirm your exact due dates.

Annual Accounting Scheme exception: Businesses on this scheme submit one return per year, with the return and balancing payment due two months after the end of the 12-month accounting period — not the standard one month plus seven days.

VAT Accounting Schemes and How They Affect Deadlines

Choosing the right scheme affects how often you file, how you calculate VAT, and how you plan cash flow around deadlines.

The Three Main Schemes

| Scheme | Filing Frequency | Deadline Rule | Eligibility (VAT Taxable Turnover) |

|---|---|---|---|

| Standard VAT Accounting | Quarterly | 1 month + 7 days after quarter end | No separate entry threshold; standard for all VAT-registered businesses |

| Annual Accounting Scheme | Annual (1 return per year) | 2 months after year-end | Up to £1.35M; must leave above £1.6M |

| Monthly VAT Returns | Monthly | 1 month + 7 days after month end | Available for businesses regularly receiving VAT repayments (for example, exporters) |

Under the Annual Accounting Scheme, businesses also make advance payments — either monthly or quarterly — throughout the year, with a final balancing payment submitted alongside the annual return.

Two Schemes That Affect Calculation, Not Frequency

- Cash Accounting Scheme (up to £1.35M turnover): VAT is recognised when customers pay you — not when you invoice. This eases cash flow without changing your filing frequency.

- Flat Rate Scheme (up to £150,000 VAT turnover; exit above £230,000): Pay a fixed percentage of gross turnover to HMRC instead of calculating output and input VAT separately. Input VAT is generally not reclaimable, except on capital assets over £2,000.

Switching schemes requires HMRC approval and resets your deadline dates — including your stagger group and quarter-end cycle. Check your VAT online account to confirm your new filing schedule before the change takes effect.

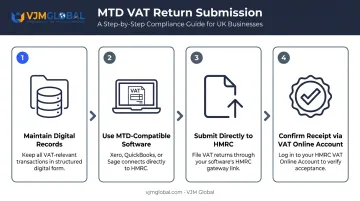

How to Submit a UK VAT Return Under Making Tax Digital

Since April 2022, all VAT-registered businesses must keep digital VAT records and submit returns using MTD-compatible software. This applies regardless of turnover. Paper returns and manual portal submissions are no longer an option for most businesses — check HMRC's exemption rules if you believe this may not apply to you.

Submission Process

- Maintain digital records of all VAT transactions throughout the accounting period — sales, purchases, and adjustments

- Use MTD-compatible software (such as Xero, QuickBooks, or Sage — see HMRC's official software list, last updated May 2025) to compile the return

- Submit directly to HMRC via the software before the deadline

- Confirm receipt through your VAT online account

What Goes Into the Return

Per HMRC VAT Notice 700/12, returns contain nine boxes:

| Box | What It Reports |

|---|---|

| 1 | VAT due on sales and other outputs |

| 2 | VAT due on acquisitions from EU member states (Northern Ireland only) |

| 3 | Total VAT due (Boxes 1 + 2) |

| 4 | VAT reclaimed on purchases and other inputs |

| 5 | Net VAT to pay or reclaim (Box 3 minus Box 4) |

| 6 | Total value of sales excluding VAT |

| 7 | Total value of purchases excluding VAT |

| 8 | Value of goods supplied to EU member states |

| 9 | Value of goods acquired from EU member states |

VAT Repayments

If your input VAT exceeds output VAT, HMRC will repay the difference. Repayments are usually made within 30 days of receiving the return. If HMRC opens a compliance check, repayment may be delayed. Exporters and businesses supplying zero-rated goods are most likely to receive regular repayments.

UK businesses with cross-border operations — particularly those trading between the UK and India — often outsource VAT return preparation to ensure MTD compliance and avoid missed deadlines. VJM Global has supported 250+ UK businesses with return preparation across Xero and QuickBooks.

Penalties for Late VAT Return Submission and Payment

Late Submission: The Points System

For VAT periods starting on or after 1 January 2023, HMRC operates a points-based system. Each missed submission earns one penalty point. Once you reach the threshold, HMRC issues a £200 financial penalty. Every subsequent late submission while at the threshold adds another £200.

| Filing Frequency | Penalty Threshold | Financial Penalty |

|---|---|---|

| Annual | 2 points | £200 |

| Quarterly | 4 points | £200 |

| Monthly | 5 points | £200 |

Points below the threshold expire after 24 months. Points at the threshold do not expire automatically. To reset them, you must complete a full compliance period — 24 months for annual filers, 12 months for quarterly, 6 months for monthly — and clear all outstanding returns.

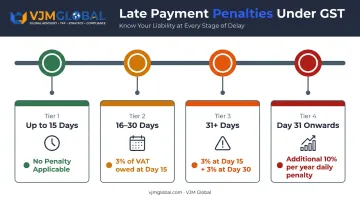

Late Payment Penalties and Interest

Missed submissions aren't the only risk. Late VAT payments for periods starting on or after 1 January 2023 trigger a separate penalty regime based on how long the balance remains unpaid:

| How Late | Penalty |

|---|---|

| Up to 15 days | No penalty if paid in full or Time to Pay agreed |

| 16–30 days | 3% of VAT owed at day 15 |

| 31+ days | 3% of amount outstanding at day 15 plus 3% at day 30 |

| Day 31 onwards | Additional daily penalty at 10% per year on the outstanding balance |

On top of penalties, HMRC charges late payment interest from the first day VAT is overdue until the balance is cleared. The current rate is the Bank of England base rate plus 4%.

How to Avoid Penalties

- Submit early — don't wait until the deadline day

- Set up a Direct Debit so payment is automated

- Check your VAT online account regularly to confirm returns have been received

- Contact HMRC to arrange a Time to Pay agreement before the deadline passes if you cannot pay on time

Frequently Asked Questions

What is the deadline for filing a VAT return?

The deadline is one calendar month and seven days after the end of the VAT accounting period. Both the return submission and the payment must reach HMRC by that date — even if it falls on a weekend or bank holiday.

Is the UK VAT return monthly or quarterly?

Most UK businesses file quarterly under the standard scheme. Monthly filing is available for businesses regularly expecting VAT repayments, such as exporters. Businesses with up to £1.35M taxable turnover may also qualify for the Annual Accounting Scheme, which allows a single annual return.

What happens if you miss the UK VAT return deadline?

Missing a deadline earns one penalty point. Quarterly filers who accumulate 4 points trigger a £200 penalty, with a further £200 charge for each subsequent late submission. Separate late payment penalties and interest apply to any VAT paid after the due date.

What is Making Tax Digital and does it apply to my VAT return?

MTD for VAT requires all VAT-registered businesses to keep digital records and submit returns using HMRC-approved compatible software. It has applied to all VAT-registered businesses since April 2022, regardless of turnover.

Can I reclaim VAT through my UK VAT return?

Yes. Input VAT paid on business purchases is offset against output VAT charged to customers via Box 5. If input VAT exceeds output VAT, HMRC will issue a refund through the same return.

What is the VAT registration threshold in the UK?

The current threshold is £90,000 in taxable turnover over the previous 12 months. You must register within 30 days of exceeding it. Voluntary registration is available below this figure and can be advantageous if you regularly incur VAT on purchases.