The result? Silent liabilities that accumulate across every untaxed vendor purchase, often undetected until a state auditor requests your accounts payable records. At that point, back taxes, interest, and penalties have already compounded the problem.

This guide breaks down why use tax non-compliance happens, what it actually costs, and how to build a compliance process that holds up under audit scrutiny — including options for resolving historical exposure before a state comes knocking.

Key Takeaways

- Use tax is self-assessed by the buyer — the seller's failure to collect it does not eliminate your obligation

- Vertex tracks 12,414 U.S. tax jurisdictions, making manual compliance at scale nearly impossible

- Unresolved liabilities attract state penalties of up to 10% in California and New York, plus compounding interest

- Voluntary Disclosure Agreements (VDAs) can reduce penalties and limit lookback periods — but only before a state audit begins

- Sustainable compliance depends on clear internal ownership, documented processes, and either automation or dedicated professional support — without these, exposure compounds over time

Common Challenges Behind Use Tax Non-Compliance

Use tax non-compliance is rarely intentional. It stems from gaps in awareness, organizational structure, and process that let liabilities accumulate unnoticed across every purchasing cycle. Each gap below points to a specific, fixable problem.

Lack of Awareness About Self-Assessment Obligations

Sales tax is visible: the seller charges it, collects it, and remits it. Use tax works the opposite way. When a seller doesn't charge tax — often because they lack nexus in your state — the buyer becomes solely responsible for assessing and remitting that tax independently.

Many businesses, especially smaller ones, treat this obligation as optional or don't know it exists.

A common example: a business buys office equipment from an out-of-state vendor that charges no sales tax. The invoice clears accounts payable, the equipment gets deployed, and no one records a use tax liability — leaving an unacknowledged exposure in the general ledger.

Washington State's Department of Revenue puts it plainly: use tax is the buyer's responsibility when sales tax was not paid at purchase.

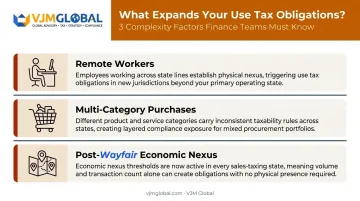

Multi-Jurisdictional Complexity

Vertex's 2025 compliance report tracks 12,414 distinct U.S. tax jurisdictions — states, counties, cities, and special districts — each with its own rates, taxability rules, and filing deadlines. Manual tracking across that landscape isn't practical for most finance teams.

The complexity compounds quickly:

- Remote workers can create physical nexus in states where the business has no formal presence

- Out-of-state purchases span multiple product categories with different taxability rules per state

- Post-Wayfair economic nexus thresholds now apply in every sales-taxing state, expanding where obligations exist

For foreign companies entering the U.S. market — a scenario VJM Global's advisory team regularly encounters — this jurisdictional complexity hits immediately upon crossing economic nexus thresholds in states like California ($500,000 in sales), New York ($500,000 and 100+ transactions), or Florida ($100,000).

No Internal Ownership of Use Tax

Sales tax has a natural owner: whoever manages customer invoicing and payments. Use tax doesn't.

It lands inside accounts payable — where the focus is payment processing, not tax assessment. Without explicit ownership, every vendor invoice becomes a potential unaccrued liability.

Staff turnover makes this worse. When institutional knowledge walks out the door, the next person in the AP seat has no documented procedure to follow. Accruals become inconsistent, filings get missed, and exposure grows.

Misclassification of Products and Exemptions

Product taxability rules differ by state and by category. Some common misclassification patterns:

- Manufacturing equipment: Texas and Washington limit exemptions to machinery used directly in qualifying manufacturing — nonqualifying purchases are fully taxable

- Digital goods and SaaS: New York taxes prewritten software regardless of delivery method; California generally exempts electronically delivered software; Washington taxes all digital products

- Construction materials: New York contractors generally owe sales tax on materials purchased; Washington's construction tax matrix confirms contractors owe sales/use tax on materials they consume

- Reseller permit misuse: Washington notes that use tax applies when equipment is purchased under a reseller permit but consumed by the business rather than resold

Expired or invalid exemption certificates create a related problem. If a certificate is missing or lapsed at the time of audit, the exempt purchase retroactively becomes taxable.

What Happens When Use Tax Is Ignored

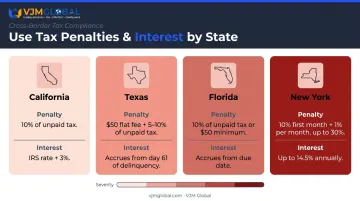

The consequences of unaddressed use tax liabilities aren't theoretical — they're documented in state penalty schedules that don't leave much room for interpretation.

State penalty and interest exposure:

| State | Late Filing Penalty | Interest |

|---|---|---|

| California | 10% for late filing or payment | IRS rate + 3%, adjusted twice yearly |

| Texas | $50 flat + 5% (1-30 days late) or 10% (30+ days) | Begins 61 days after due date |

| Florida | 10% of tax owed, minimum $50 | Accrues from due date |

| New York | 10% first month + 1% per additional month, up to 30% | Greater of 14.5% or Commissioner's rate for fraud |

Those penalties compound quickly — and audits do happen. California's CDTFA reported nearly $755.2 million in net audit deficiencies in FY 2022-23 for combined sales and use tax, auditing approximately 1% of active accounts annually. Auditors focus on accounts payable records and capital expenditure purchases precisely because those transactions are large and easy to trace — making under-reported use tax straightforward to surface.

Warning Signs Your Business Has a Use Tax Problem

Use tax exposure is often invisible until an auditor surfaces it. These operational indicators suggest liabilities are building:

- Out-of-state or online vendor purchases appear in your AP records with no corresponding use tax accrual

- Exemption certificates on file are expired, incomplete, or missing for purchases claimed as tax-exempt

- Your business has expanded into new states, hired remote workers, or opened new locations without reassessing where use tax obligations apply

If any of these apply, a voluntary disclosure or internal use tax review is worth prioritizing before an auditor does it for you.

How to Achieve Use Tax Compliance: A Step-by-Step Approach

Use tax compliance is a structured process with three distinct phases: understand your exposure, remediate what's accumulated, then build systems that prevent the problem from recurring.

Map Nexus and Determine Filing Obligations

The first step is establishing where your business has a tax presence. Physical nexus triggers include employees working in a state, inventory storage, and representative activities. Economic nexus applies when sales cross state-specific thresholds — and every sales-taxing state has now adopted economic nexus rules following South Dakota v. Wayfair.

For foreign companies entering the U.S. market, this step is non-negotiable. A UK or Australian business selling into California owes California use tax obligations once it crosses that state's $500,000 threshold, even without a physical office there.

When to act: Immediately upon expanding to a new state, hiring your first remote worker in any jurisdiction, or crossing an economic nexus threshold.

Audit Purchasing Records and Quantify Historical Exposure

Before building a forward-looking compliance process, businesses need to understand what's already accumulated. This means:

- Pull all vendor purchase records for the applicable lookback period

- Identify transactions where no sales tax was charged

- Determine taxability of each purchase in the destination state

- Estimate total use tax liability, including interest

If the exposure is significant, a Voluntary Disclosure Agreement (VDA) may be the most cost-effective path forward. The Multistate Tax Commission administers a national VDA program covering participating states, offering penalty waivers and limited lookback periods for businesses that come forward proactively. Washington, for example, limits the lookback to four prior years and can waive up to 39% in potential penalties.

The critical requirement: the business must initiate the VDA before the state makes contact. Once an audit is opened, VDA protections no longer apply.

Establish a Use Tax Accrual Process Within Accounts Payable

A formal accrual process means every vendor invoice goes through a defined review before payment:

- Was sales tax charged by the vendor?

- If not, is the purchase taxable in the state where the goods will be used or stored?

- If taxable, accrue the use tax liability and schedule remittance

This process needs explicit ownership. Assign it to the AP team with documented checklists (not institutional memory) to ensure it survives personnel changes and keeps pace with transaction volume.

Tax compliance advisors help design this process correctly from the start. VJM Global's CPAs and Chartered Accountants work with businesses across industries to build AP-integrated use tax workflows that hold up under audit scrutiny.

Implement Tax Automation and Maintain Exemption Certificates

Manual use tax calculation across thousands of jurisdictions is error-prone. Tax automation platforms (Avalara's AvaTax for Accounts Payable, Vertex Consumer Use Tax, and Thomson Reuters ONESOURCE) integrate directly with ERP and AP systems to calculate, accrue, and report use tax automatically. A Forrester TEI study commissioned by Thomson Reuters found 120% ROI and invoice error-rate reduction of more than 75% from indirect tax automation (note: this is a vendor-commissioned study covering the broader ONESOURCE platform).

Exemption certificates require equal attention. Collect them at the time of purchase, validate completeness, and maintain them with expiration tracking. An expired or incomplete certificate offers no protection during an audit — the exempt transaction becomes taxable retroactively.

Tips for Long-Term Use Tax Compliance Control

Moving from reactive to proactive means embedding use tax into your day-to-day operations:

- Conduct annual purchasing reviews — revisit vendor records, identify new taxable product categories, and reassess jurisdictions where your economic footprint has changed

- Train AP and procurement staff — document use tax accrual procedures and taxability rules for key states so the process doesn't depend on any one person

- Monitor rate changes and deadlines automatically — whether through compliance software or outsourced support, tracking registration requirements across active jurisdictions keeps the business current without adding ongoing burden to internal teams

The real goal is a documented, repeatable process — one that reduces exposure and shows good-faith compliance effort when an audit comes around.

Frequently Asked Questions

What does use tax compliance include?

Use tax compliance covers self-assessing whether untaxed purchases are subject to use tax, accruing the correct amount, remitting it to the relevant state authority, maintaining purchase records and valid exemption certificates, and filing use tax returns on the required schedule — either separately or as part of combined sales and use tax filings.

How do I know if I owe use tax in California?

A business owes California use tax if it purchased taxable goods for use in California and the seller did not collect California sales tax — including purchases from out-of-state or online vendors. The obligation applies regardless of whether the seller had California nexus, since the buyer is responsible for self-assessment; the CDTFA administers all California use tax filings.

What is the difference between sales tax and use tax?

Sales tax is collected by the seller at the point of sale and remitted to the state. Use tax is owed by the buyer when the seller did not collect sales tax on a taxable transaction. Both taxes apply to the same underlying purchases — the difference is which party is responsible for remitting them.

What happens if a business does not pay use tax?

Unpaid use tax accrues back taxes, interest, and penalties — up to 10% in California, Texas, Florida, and New York, with additional monthly charges in some states. Auditors routinely target accounts payable and capital expenditure records, making non-compliance a material financial and legal risk.

Which industries face the highest use tax compliance risk?

Manufacturing, construction, retail, distribution, and hospitality carry elevated risk due to high-volume out-of-state purchasing, complex taxability rules for equipment and materials, and frequent inventory withdrawals for internal use.

Can a Voluntary Disclosure Agreement (VDA) help resolve past use tax liabilities?

VDAs allow businesses to voluntarily disclose unpaid use tax in exchange for reduced or waived penalties and a limited lookback period — typically two to four years depending on the state. The agreement's protections only apply if the business initiates the process before the state opens an audit or makes enforcement contact.