Introduction

Many UAE businesses trading with UK clients operate under a dangerous assumption: that being based outside the UK automatically shields them from UK VAT obligations. It does not.

UK VAT is determined by the nature and location of the supply — not the supplier's country of establishment. A UAE firm selling goods stored in a UK warehouse, or supplying digital services to UK consumers, carries the same VAT obligations as any UK-based business.

According to HMRC's VAT Notice 700/1, non-established taxable persons (NETPs) face no minimum registration threshold. Registration can apply from the very first £1 of taxable UK supply.

This article covers what UAE firms need to know: how UK VAT categories (exempt, zero-rated, and out of scope) apply to cross-border trade, which exemptions matter most for UAE businesses, when registration is required, and how place of supply rules affect UAE-UK transactions.

Key Takeaways

- UK VAT exemptions are defined by the type of supply, not the supplier's location — UAE firms follow the same rules as UK businesses.

- There are three distinct categories: VAT-exempt, zero-rated (0% but still taxable), and out of scope, each carrying different financial consequences.

- UAE firms making taxable UK supplies must register from £1 of supply — the £90,000 threshold only applies to UK-established businesses.

- Businesses making only exempt supplies cannot register for VAT and cannot reclaim UK input VAT.

- Most B2B services from UAE firms to UK-registered businesses fall under the reverse charge, which shifts VAT accounting to the UK customer.

UK VAT Categories: Exempt, Zero-Rated, and Out of Scope Explained

UAE firms trading into the UK face three distinct VAT categories — and the differences between them have direct consequences for cost recovery, registration obligations, and how supplies are structured.

Exempt vs. Zero-Rated: A Critical Distinction

Both exempt and zero-rated supplies result in £0 VAT charged to the customer. But that surface similarity hides a meaningful practical difference.

Zero-rated supplies are still taxable supplies under the VAT Act 1994. This means a business making zero-rated supplies can register for VAT and reclaim input VAT on its costs. Exempt supplies, by contrast, sit outside the taxable supply framework — HMRC permits no input VAT recovery on costs attributable to them.

For a UAE firm exporting goods to the UK or structuring service arrangements, being classified as zero-rated rather than exempt is considerably more advantageous.

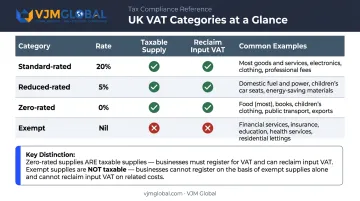

| VAT Category | Rate | Taxable Supply? | Reclaim Input VAT? | Common Examples |

|---|---|---|---|---|

| Standard-rated | 20% | Yes | Yes | Most goods and services |

| Reduced-rated | 5% | Yes | Yes | Home energy, children's car seats |

| Zero-rated | 0% | Yes | Yes | UK exports, most food, books |

| Exempt | Nil | No | No | Financial services, healthcare, insurance |

Out of Scope Supplies

Out-of-scope supplies are entirely outside the UK VAT system. They do not count toward taxable turnover and cannot carry VAT in either direction: no charging and no reclaiming.

This category is particularly relevant to UAE firms whose supply is physically or legally situated outside the UK. Services consumed entirely outside the UK, statutory fees, and non-business activities all fall here.

A UAE firm providing services to another UAE entity with no UK nexus would typically be supplying outside the scope of UK VAT altogether.

Which UK VAT Exemptions Are Most Relevant to UAE Firms?

UK VAT exemptions are defined under Schedule 9 of the VAT Act 1994. Several of these categories align closely with sectors where UAE firms are active in UK trade.

Financial and Insurance Services

Financial services (including loans, currency exchange, and certain investment management) and most insurance services are VAT-exempt under Schedule 9, Groups 2 and 5. UAE-based fintech firms, investment managers, or insurance intermediaries supplying these services into the UK market may qualify for this exemption, depending on how the supply is structured.

One critical caveat: HMRC Notice 701/49 makes clear that many services connected with finance are not exempt. Specifically excluded from exemption:

- Bookkeeping and accountancy services

- Investment, finance, and taxation advice

- Management consultancy

- Market research and advertising

- Mere collection or provision of financial information

The intermediary exemption is also conditional — a UAE firm must be genuinely bringing together parties to an exempt financial transaction, not simply providing advisory services around one. Active litigation in this area (including Target Group Ltd v HMRC) confirms that courts and HMRC interpret these boundaries narrowly.

Real Estate and Land

The sale or leasing of commercial land and buildings is generally VAT-exempt in the UK. This is directly relevant to UAE investors or property companies holding or transacting UK real estate.

However, sellers and landlords can opt to tax — formally electing to treat otherwise exempt supplies as taxable. This allows them to charge VAT on rents or sale proceeds and reclaim input VAT on construction, refurbishment, and other property costs.

For UAE property investors with significant UK development expenditure, the opt-to-tax decision can have a material impact on recoverable costs. It is not automatic and must be formally notified to HMRC.

Professional and Consultancy Services

Legal, accounting, and management consulting services are not VAT-exempt. They are standard-rated at 20%.

That said, place of supply rules change the picture for B2B transactions. When a UAE firm supplies these services to a UK VAT-registered business, the UAE firm does not charge UK VAT directly. Instead, the UK customer accounts for VAT via the reverse charge mechanism.

The practical effect resembles exemption from the UAE firm's perspective (no UK VAT on the invoice), but the legal mechanism is entirely different. UAE firms should not treat these two outcomes as interchangeable when assessing compliance obligations.

Education, Healthcare, and Other Categories

Other Schedule 9 exemptions relevant to UAE businesses include:

- Education and training: only by eligible bodies meeting HMRC's specific institutional criteria

- Healthcare and medical treatment: only by registered practitioners; not general health-related products or services

- Postal services: Royal Mail only; private couriers are not covered

- Betting and gaming: subject to specific conditions

Each exemption is defined narrowly. The sector a UAE firm operates in is only the starting point — HMRC looks at the specific nature and legal form of each supply when determining whether it qualifies. Misclassifying a taxable supply as exempt can trigger penalties, back-dated VAT assessments, and interest charges.

Does Your UAE Business Need to Register for UK VAT?

The rule that most surprises UAE firms: there is no minimum turnover threshold for non-UK-established businesses. Where a UAE firm makes any taxable supplies in the UK, registration is required from the first £1. This contrasts sharply with the £90,000 threshold that applies to UK-established businesses (effective from 1 April 2024).

When Registration Is Required

UK VAT registration is triggered for UAE firms in these scenarios:

- Goods located in the UK at point of sale — selling goods stored in a UK warehouse or fulfilment centre

- Importing goods into the UK for domestic sale — goods brought into the UK and sold to UK customers

- B2C digital services to UK consumers — streaming, software, apps, or other digital content supplied to UK individuals

- Construction or land-related services in the UK — services directly connected to UK-situated property, where the reverse charge does not apply

Note: supplying only exempt goods or services does not trigger registration — and a business making only exempt supplies cannot register even if it wants to.

When Registration Is Not Required

Two scenarios remove the registration obligation entirely:

- B2B services subject to reverse charge — if a UAE firm supplies general-rule services exclusively to UK VAT-registered businesses, the UK customer accounts for VAT via reverse charge. Under HMRC Notice 741A, overseas suppliers making only reverse-charged supplies are not entitled to register for UK VAT.

- All supplies are out of scope or exempt — no taxable UK supplies means no registration requirement.

Confirm Your Registration Position Before Supplying

Supply classification, place of supply rules, and business structure all interact when determining a UAE firm's UK VAT position. Getting this wrong at the outset creates costly correction work and potential HMRC penalties.

Assess your registration position before making any UK supplies. VJM Global has supported 250+ UK businesses and brings 30+ years of cross-border tax and compliance experience — helping international firms understand their obligations across jurisdictions before they become a problem.

UK VAT Rules for UAE-UK Cross-Border Transactions

Place of supply rules determine whether UK VAT applies to a transaction at all. The rules differ for goods and services, and within services, differ further for B2B versus B2C.

For goods: VAT is generally determined by where goods are located at the point of sale.

For services:

- B2B — place of supply is where the customer is established. A UAE firm supplying services to a UK VAT-registered business generally does not charge UK VAT; the UK customer self-accounts via reverse charge.

- B2C — place of supply is where the supplier is established (general rule), but digital services to UK consumers are supplied where the consumer is located — meaning the UAE firm must account for UK VAT.

Exporting Goods from the UK to the UAE

Goods exported from the UK to the UAE are zero-rated for UK VAT purposes. The UK supplier charges 0% VAT and can still reclaim input VAT on related costs.

The key condition: HMRC's VAT Notice 703 requires the supplier to obtain and retain valid proof of export within the required time limit — typically three months from the time of supply. Acceptable evidence includes:

- Official customs export documentation

- Authenticated waybills or bills of lading

- Supporting commercial evidence (contracts, payment records, transport documents)

Without this documentation, the zero-rating is lost and 20% VAT becomes chargeable. UAE importers purchasing from UK suppliers receive goods without UK VAT. The condition is straightforward: their UK supplier must meet the export evidence requirements above.

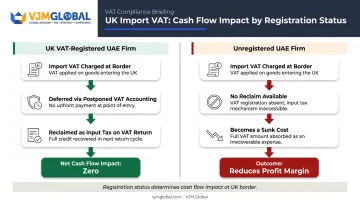

Importing Goods into the UK

UAE firms importing goods into the UK face import VAT at the point of entry, charged on the customs value of the goods. The VAT treatment then depends entirely on registration status:

- UK VAT-registered firms can use postponed VAT accounting to defer the import VAT charge and reclaim it as input tax on the VAT return — no cash flow impact at the border.

- Unregistered firms cannot reclaim import VAT. It becomes a sunk cost that directly reduces profit margins, and should factor into pricing decisions before entering the UK market.

Common UK VAT Compliance Mistakes UAE Firms Should Avoid

Mistake 1: Assuming the UAE base exempts all supplies from UK VAT

UK VAT follows the supply, not the supplier. A UAE firm with goods in a UK fulfilment centre, or supplying apps to UK consumers, is fully liable for UK VAT regardless of where its offices are located.

Mistake 2: Misclassifying exempt supplies as zero-rated — or vice versa

This is a costly error in both directions. A UAE firm incorrectly treating supplies as exempt (when they are zero-rated) forfeits input VAT recovery it was entitled to claim, inflating its cost base unnecessarily.

In financial services specifically, the boundary between taxable advisory services and exempt intermediary services is genuinely complex. HMRC's Notice 701/49 excludes a wide range of finance-adjacent services from exemption, and court disputes like Target Group Ltd v HMRC confirm that these lines are actively litigated.

Mistake 3: Poor documentation for cross-border transactions

UAE firms must maintain:

- Export evidence for zero-rated goods leaving the UK — within the required timeframe

- Reverse charge records for B2B services received from UK suppliers

- Separate accounting for exempt supplies, to correctly calculate partial input VAT recovery where a business makes both taxable and exempt supplies

Getting the accounting structure right from the outset avoids costly reconstruction later. VJM Global works with UAE-facing businesses to establish the correct compliance frameworks across all three areas: supply classification, documentation, and VAT return preparation.

Frequently Asked Questions

How do I get VAT exemption in the UK?

VAT exemption is not applied for in most cases — it applies automatically when a business supplies only goods or services listed as exempt under Schedule 9 of the VAT Act 1994 (such as financial services or healthcare). A business making only exempt supplies cannot register for VAT. If your supplies are mainly zero-rated, you can separately apply for exemption from registration via HMRC's Notice 700/1.

Do UAE businesses need to register for UK VAT?

A UAE firm must register for UK VAT if it makes any taxable supplies in the UK — there is no minimum threshold for non-established businesses, unlike the £90,000 threshold that applies to UK firms. If the UAE firm only supplies exempt goods or services, or B2B services subject to reverse charge, registration is not required.

Are services provided by a UAE firm to UK clients subject to UK VAT?

For B2B services, the place of supply is generally the customer's country, so the UK business client accounts for VAT via reverse charge — the UAE firm does not charge UK VAT. For B2C services supplied directly to UK consumers, the UAE firm may need to charge and account for UK VAT, particularly for digital services.

What is the difference between UK VAT exemption and zero-rating?

Both result in no VAT charged to the customer, but zero-rated supplies are still technically taxable — meaning the business can reclaim input VAT on related costs. Exempt supplies sit outside the VAT system entirely, and no input VAT can be reclaimed on costs attributable to those supplies.

Can a UAE company reclaim UK VAT it has paid?

UAE businesses not registered for UK VAT may reclaim UK VAT through the overseas refund scheme (VAT Notice 723A), provided the UAE allows equivalent arrangements for UK businesses — confirm eligibility with HMRC's Overseas Repayments Unit. UK VAT-registered UAE businesses reclaim input VAT through their standard VAT return.

What is the reverse charge, and how does it affect UAE firms?

Under the reverse charge, the UK business client self-accounts for VAT on services purchased from overseas suppliers — reporting both output and input VAT on its own return. The UAE firm therefore does not charge or collect UK VAT on those B2B services, removing a direct compliance obligation in the UK.