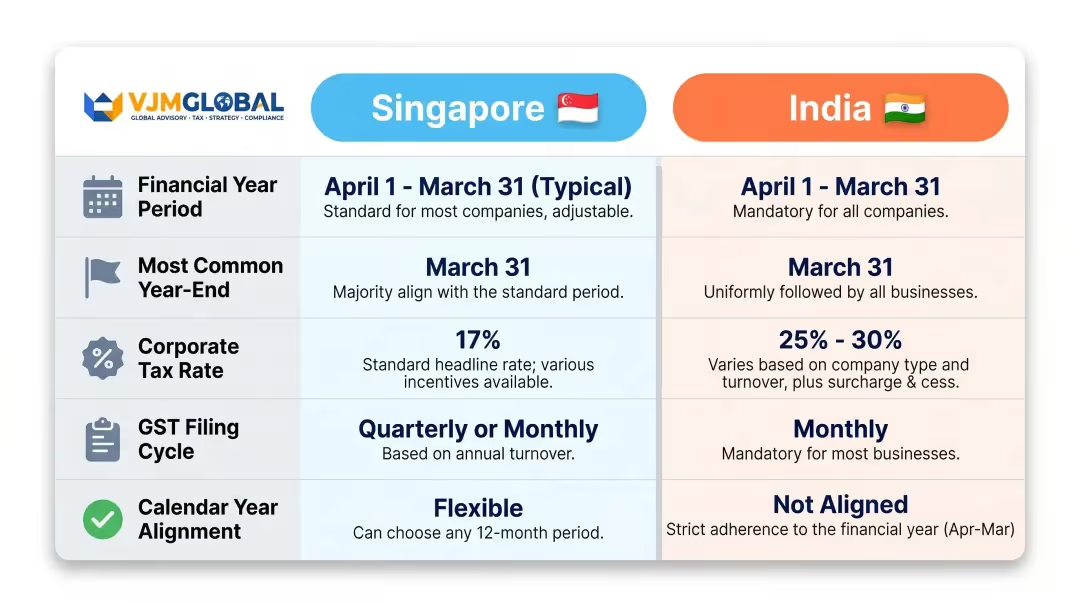

新加坡企业在印度拓展业务时,会立即遇到一个监管障碍:印度的财政年度是从4月1日到次年3月31日,而非大多数新加坡公司所采用的1月至12月日历年。这种差异不仅造成日程安排上的不便,更带来了实际的合规难题。

当您的新加坡母公司在12月31日结账,而您的印度子公司却采用4月至3月的周期时,您将面临三个月的报告滞后和不一致的税务截止日期。公司间对账、合并报告和法定申报都需要在两个司法管辖区之间进行仔细协调。

本指南将详细解读印度的会计期间规定,它们与新加坡框架的对比,以及您的财务团队从一开始就需要了解如何管理这种双重报告的现实。

印度的财政年度(也称为会计年度或 财年)是一个为期12个月的期间,从4月1日开始,到次年3月31日结束。例如,2025-26财年是从2025年4月1日到2026年3月31日。

根据2013年《公司法》第2(41)条的规定,该周期是法定强制性的,该条款将“财政年度”定义为每年3月31日结束的期间。1961年《所得税法》通过其对“前一年度”和“评估年度”的定义进一步强化了这一点。

印度的税收系统使用了两个不同的概念,这些概念经常让新加坡的财务团队感到困惑:

例如,在2025-26财年(前一年度)获得的收入,将在2026-27评税年度(评估年度)进行评估和征税。这种滞后与新加坡的制度截然不同,新加坡的收入是在赚取当年进行评估的。

4月至3月的周期可追溯到1867年,当时英国殖民政府将印度的财政日历与英国财政部的会计期间对齐。这一时间点也恰逢印度的农业收获季节——收获期从10月持续到次年3月,这使得政府能在4月前对收入情况有更清晰的了解。印度在独立后保留了这一周期,因为行政和预算系统已经围绕它建立起来。

尽管大多数印度公司遵循4月至3月的财年,但历史上存在有限的例外情况。《2013年公司法》通过强制所有注册公司采用统一的财年,大大缩小了这些例外范围。

例外情况的关键点:

理解这一框架后,还有一个关键要素:联邦预算。印度政府在财年开始前的2月公布预算,这意味着税收变化会在您的规划周期结束前生效。

预算中公布的税率调整、折旧规定和合规要求通常从4月1日起适用。对于新加坡企业而言,这意味着2月份的预算公告可能会在约六周的通知期内,改变您在印度的税务风险、转让定价假设或申报截止日期。将预算监控步骤纳入您的第一季度日程安排是值得的。

新加坡母公司若拥有印度子公司,其财年结账日期的差异不仅会带来行政上的挑战,更会造成实际的合并报表和报告难题。

一家在12月31日结账的新加坡控股公司,必须合并一家仅在3月31日结账的印度子公司,这造成了三个月的报告期差异。

根据国际财务报告准则第10号(IFRS 10)和新加坡财务报告准则(国际)第10号(SFRS(I) 10),这三个月的差异是合并报表目的所允许的最大期限。公司通常通过以下方式处理:

无论采用哪种方法,两家实体的会计政策都必须保持一致,并且必须识别并调整两个财年结账日之间发生的任何重大交易,将其反映在合并报表中。

新加坡没有单独的“评估年度”概念。收入在其赚取的当年进行评估。而在印度, 上一个年度/评估年度 这种区分意味着一家公司在2025-26财年赚取的收入,其税务评估要到2026-27评估年度才会进行。

新加坡财务团队在审查公司间账目中的印度税务准备金时,需要考虑这种滞后性——若未能做到,可能导致税务负债被错误归属到不正确的期间,从而扭曲准备金和公司间对账。

新加坡的消费税申报通常是按季度进行的。而印度的消费税要求:

印度的商品及服务税(GST)日历与财政年度并非完全吻合——申报周期横跨日历月,这为新加坡企业带来了全年无休的合规义务,需要持续投入人力。

印度商品及服务税申报的频率也对转让 定价文件产生影响,因为用于这些申报的内部公司发票必须全年保持一致的定价。

当新加坡实体与印度子公司进行交易时,印度的转让定价文件必须涵盖4月至3月的财政年度。而新加坡的转让定价文件则遵循新加坡的财政年度。

新加坡企业必须确保其 内部公司定价政策 和文件涵盖这两个时期并进行核对——尤其是在定价或利润率在年内发生变化的情况下。印度转让定价审计报告Form 3CEB的截止日期为评估年度的10月31日,涵盖印度财政年度。

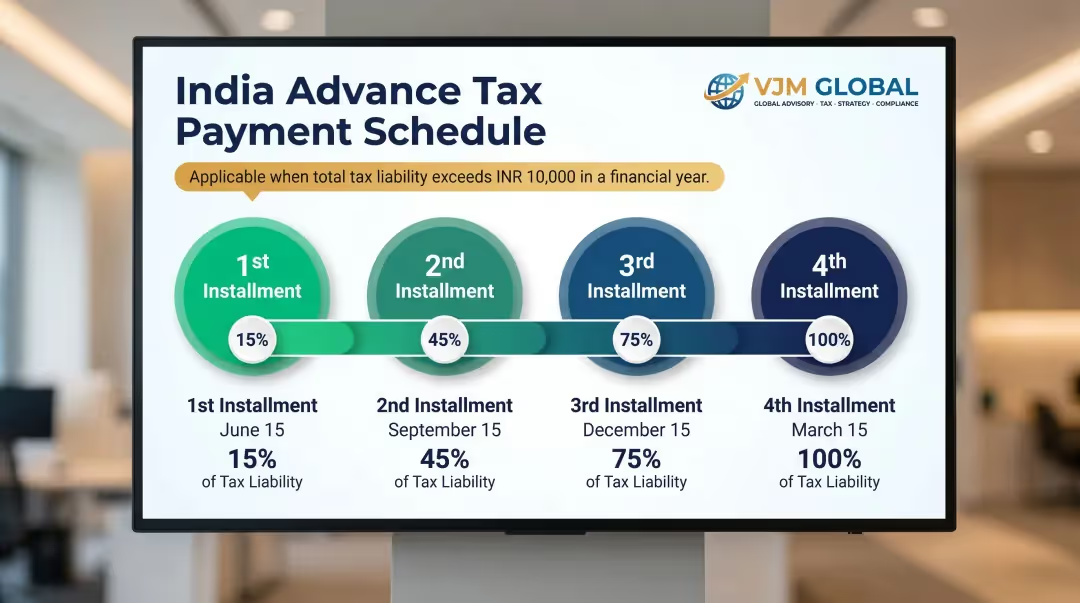

如果年度应纳税总额超过10,000印度卢比,公司必须支付 预缴税款 ,分四期按季度支付:

未能按时支付这些款项,将根据《所得税法》第234B和234C条规定,每月加收1%的利息。这与新加坡的评估时征税模式不同,许多新加坡企业首次进入印度时对此措手不及。

季度TDS申报截止日期:

适用表格包括24Q表(工资TDS)、26Q表(非工资支付)和27Q表(向非居民支付)。

印度子公司必须提交 年度申报表、财务报表和董事会决议至公司事务部:

逾期提交AOC-4和MGT-7将面临每日100印度卢比的罚款,且不设上限,此外,根据第450条,对于持续违规行为还将处以额外罚款。

对于通过分支机构或联络处(而非注册子公司)运营的新加坡公司:

另一个值得注意的合规方面是:印度现在通过数字化方式进行税务评估,不设现场听证会。新加坡企业应:

印度子公司的独立财务报表采用4月至3月的财年,而新加坡母公司的合并集团账目通常采用1月至12月的财年。这种不匹配并非印度独有——英国和澳大利亚也使用非1月开始的财年——但这需要结构化的内部流程。

新加坡集团审计师将要求在合并账目中披露不同的财年——这种不匹配也会影响您的规划周期。

当新加坡企业以1月至12月为基础进行预算时,印度子公司的计划将跨越两个印度财年:1月至3月结束一个财年,4月至12月开启下一个财年。印度管理团队以4月至3月的周期进行规划和激励,这可能导致当地优先事项与集团目标不同步。

通过以下方式有意识地管理这一差距:

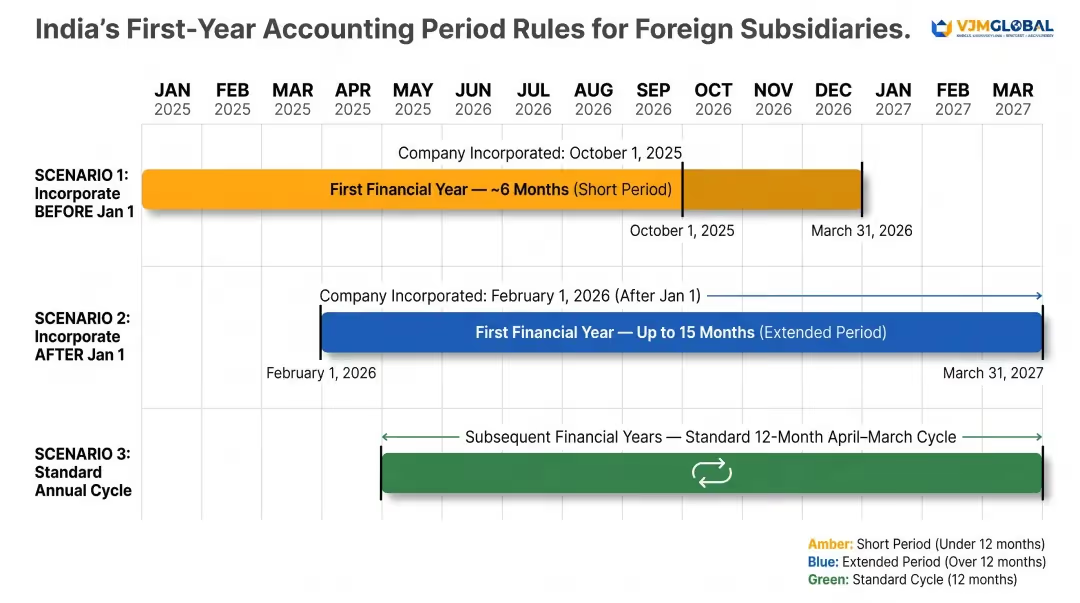

当外国公司在印度设立子公司时,第一个财年可以短于或长于12个月,但必须在3月31日结束。

根据2013年《公司法》第2(41)条:

这意味着印度第一份经审计的账目可能涵盖不足12个月,这一点必须明确告知新加坡母公司的利益相关者。

通过联络处或项目办事处(非注册实体)运营的外国公司,根据《外汇管理法》(FEMA)和印度储备银行(RBI)的规定,有单独的会计和报告要求:

第2(41)条规定了一项有限的例外:作为外国注册实体的控股公司、子公司或联营公司的公司,可以向区域总监申请采用不同的财政年度以进行合并。

适用此规定的两种具体情况:

实际上,大多数新加坡所有的印度子公司都将采用标准的4月至3月周期。

印度储备银行(RBI)历史上曾采用7月至6月的会计年度。自2021年4月1日起,印度储备银行已调整为4月至3月,以与政府的财政年度保持一致。对于新加坡企业而言,这种调整意味着您的印度子公司的财政年度、政府的财政日历以及印度储备银行的银行周期现在都遵循相同的4月至3月时间表——从而减少了一层对账的复杂性。

12个月的会计期间通常被称为“财政年度”或“会计年度”。在印度,该期间特指从4月1日到3月31日,在所得税术语中也称为“上一年度”。

2025-26财年(FY 2025-26)从2025年4月1日开始,到2026年3月31日结束。相应的评估年度是2026-27评估年度(AY 2026-27),届时将对2025-26财年期间的收入进行评估和征税。

2024-25财年(通常称为25财年)于2024年4月1日开始,并于2025年3月31日结束。“25财年”这个术语可能会因采用起始年份还是结束年份的惯例而引起混淆。

否。新加坡并未强制规定特定的财政年度——在新加坡注册成立的公司可以选择任何12个月的期间作为其财政年度。许多公司采用1月1日至12月31日,这与印度强制性的4月1日至3月31日周期不同,从而为在印度设有子公司的加坡企业造成了报告不匹配的问题。

根据2013年《公司法》,在印度注册的公司——包括外国公司的子公司——都必须遵循4月1日至3月31日的财政年度。对于国际金融服务中心(IFSC)公司等特定实体类型存在有限的例外情况,但灵活性非常受限。

需要关注的主要截止日期:

错过这些截止日期将导致每月1%的利息以及累积罚款。

需要专家支持以应对印度的会计期间和合规要求吗? VJM Global 专注于帮助新加坡企业在印度设立并运营。凭借30多年的经验,我们提供全面的企业设立、税务合规、双日历管理报告以及为跨境运营量身定制的持续会计服务。请通过以下方式联系我们: info@vjmglobal.com 或 +91 98915 76441 讨论我们如何帮助您的新加坡企业在印度取得成功。