Introduction

GST accounting entries are the debit and credit records a GST-registered Singapore business makes every time it buys or sells goods and services — separating the GST component from the base transaction so input tax and output tax can be tracked, settled, or claimed back from IRAS accurately.

This guide is written for business owners, finance managers, and accountants running GST-registered companies in Singapore who need to understand how GST moves through their books, not just their returns.

Many businesses grasp GST conceptually but make systematic errors in execution: recording the full invoice amount as revenue, claiming input tax on blocked expenses, or filing the GST F5 return without reconciling it against their accounting records. IRAS completed over 2,800 GST audits in FY2024/25 and recovered S$205 million in taxes and penalties — errors that are common and costly.

This guide covers:

- The correct journal entries for standard sales, purchases, and adjustments

- How to structure your GST ledger accounts for clean reconciliation

- The mistake patterns that most often trigger IRAS scrutiny

Key Takeaways

- GST-registered businesses need at least two control accounts: GST on Purchases (input tax) and GST on Sales (output tax)

- Singapore's current GST rate is 9% (effective 1 January 2024); net GST payable = Output Tax minus Input Tax

- If input tax exceeds output tax, IRAS refunds the difference — common for export-heavy businesses

- Zero-rated, exempt, and OVR transactions each require different treatment from standard purchase and sales entries

- All GST records must be retained for five years and reconciled with figures submitted in the GST F5 return

What Are GST Accounting Entries in Singapore?

GST accounting entries are the debit and credit records a GST-registered business makes on every purchase or sale. Each entry separates the GST component from the base transaction amount so the business can claim, remit, or settle the correct amount with IRAS.

Two flows run through every GST-registered set of books:

- Input tax — GST a business pays to its suppliers on eligible purchases, recorded as a recoverable asset

- Output tax — GST the business charges customers on taxable supplies, recorded as a liability owed to IRAS

At the end of each GST reporting period, these two figures are offset. If output tax exceeds input tax, the business remits the difference to IRAS. If input tax exceeds output tax, IRAS refunds the balance.

How Singapore's GST Structure Differs

Singapore runs a single-rate GST — businesses only need to distinguish between three supply categories:

| Supply Type | GST Rate | Input Tax Claimable? |

|---|---|---|

| Standard-rated | 9% | Yes |

| Zero-rated (exports, international services) | 0% | Yes |

| Exempt (residential property, financial services) | Nil | Generally No |

This is far simpler than multi-component systems like India's CGST/SGST/IGST. With only three supply categories and one rate to apply, the recording structure is straightforward — which is why getting the entries right from the start matters more than managing complexity.

GST Ledger Accounts Every Registered Business Must Maintain

Singapore's GST framework does not prescribe a universal chart of accounts, but IRAS expects records that can support GST declarations and withstand audit review. In practice, the minimum ledger structure looks like this:

| Account | Type | Purpose |

|---|---|---|

| GST on Purchases (Input Tax) | Current Asset | Accumulates recoverable GST paid to suppliers |

| GST on Sales (Output Tax) | Current Liability | Accumulates GST collected from customers, owed to IRAS |

| GST Payable / GST Receivable | Net Settlement | Records the balance due to or refundable from IRAS at period end |

Businesses making zero-rated supplies should also maintain a separate account to track zero-rated output. This is necessary for accurate completion of the GST F5 form, where standard-rated and zero-rated supplies are reported in separate boxes.

Balance Sheet Treatment

Throughout the period:

- Input tax accumulates as an asset (money IRAS owes you in recoverable tax)

- Output tax accumulates as a liability (money you owe IRAS on behalf of your customers)

At period end, the two accounts are offset. The net balance flows to either GST Payable (you owe IRAS) or GST Receivable (IRAS owes you).

IRAS requires GST records to be retained for at least five years/basics-of-gst/invoicing-price-display-and-record-keeping/keeping-records) from the date of the GST return, in physical or electronic format.

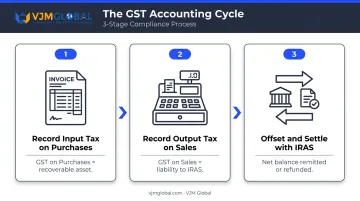

How to Record GST Accounting Entries: Step by Step

The GST accounting cycle runs in three stages:

- Record input tax on purchases throughout the period

- Record output tax on sales throughout the period

- Offset input against output at period end and settle the net balance with IRAS

Recording a Purchase — Input Tax Entry

Example: Purchase of office equipment for S$10,000 net, plus 9% GST (S$900). Total invoice: S$10,900.

| Account | Debit | Credit |

|---|---|---|

| Office Equipment (or Expense) | S$10,000 | |

| GST on Purchases (Input Tax) | S$900 | |

| Creditors / Accounts Payable | S$10,900 |

The S$900 debit to GST on Purchases is a recoverable asset : it represents tax you can offset against your output tax liability.

Input tax can only be claimed when:

- The purchase is for business purposes

- It is supported by a valid tax invoice from a GST-registered supplier

- It is claimed in the period corresponding to the tax invoice date

Once purchases are recorded correctly, the same discipline applies to the sales side of the ledger.

Recording a Sale — Output Tax Entry

Example: Sale of goods for S$20,000 net, plus 9% GST (S$1,800). Total invoice: S$21,800.

| Account | Debit | Credit |

|---|---|---|

| Debtors / Accounts Receivable | S$21,800 | |

| Sales / Revenue | S$20,000 | |

| GST on Sales (Output Tax) | S$1,800 |

The S$1,800 credit to GST on Sales is a liability — it belongs to IRAS, not to the business. It should never flow into revenue.

Period-End Settlement Entry

At period end, using the example figures above (Output Tax S$1,800, Input Tax S$900):

| Account | Debit | Credit |

|---|---|---|

| GST on Sales (Output Tax) | S$1,800 | |

| GST on Purchases (Input Tax) | S$900 | |

| GST Payable | S$900 |

Then, when the net amount is remitted to IRAS:

| Account | Debit | Credit |

|---|---|---|

| GST Payable | S$900 | |

| Bank | S$900 |

If input tax had exceeded output tax, the net balance would sit as GST Receivable (an asset) until IRAS processes the refund.

Filing deadline: GST returns and payment are due one month after the end of each accounting period.

Date and post period-end entries within the same reporting period to avoid discrepancies when submitting your F5 return (the standard GST filing form) to IRAS.

Special GST Transactions That Require Different Accounting Treatment

Zero-Rated Supplies

For exported goods and qualifying international services, the GST rate is 0%. The sales entry credits Revenue only — no GST on Sales credit arises because there is no output tax to collect.

Sales entry for zero-rated supply:

| Account | Debit | Credit |

|---|---|---|

| Debtors / Bank | S$20,000 | |

| Sales / Revenue | S$20,000 |

Input tax on purchases used to make those zero-rated supplies remains fully claimable. This is why export-heavy businesses frequently receive GST refunds from IRAS each period — their input tax accumulates with no offsetting output tax liability.

Exempt Supplies

Exempt supplies — including the sale or lease of residential properties and most financial services — are treated very differently:

- No GST is charged to customers

- Input tax on costs directly attributable to exempt supplies cannot be claimed

- Any such input GST must be expensed or added to the cost of the asset rather than posted to GST on Purchases

Businesses making both taxable and exempt supplies must apportion residual input tax using IRAS's partial exemption rules. The de minimis threshold allows full input tax recovery only if exempt supplies do not exceed an average of S$40,000 per month and 5% of total supplies.

Imports and the OVR Regime

For imported goods, GST is collected by Singapore Customs at the point of import. The entry records:

| Account | Debit | Credit |

|---|---|---|

| GST on Purchases (Input Tax) | GST amount | |

| GST Payable to Customs / Bank | GST amount |

For digital services and low-value goods purchased from overseas vendors registered under Singapore's Overseas Vendor Registration (OVR) regime, the GST is charged by the vendor and recorded identically to a standard purchase input tax entry.

The OVR regime expanded from 1 January 2023 to cover low-value goods. Overseas suppliers must register if their annual global turnover exceeds S$1 million and Singapore B2C sales exceed S$100,000.

Customer Accounting

Under customer accounting rules, certain prescribed goods (currently mobile phones, memory cards, and off-the-shelf software, where the GST-exclusive sale value exceeds S$10,000) require the buyer — not the seller — to account for output tax.

The buyer records:

| Account | Debit | Credit |

|---|---|---|

| GST on Purchases (Input Tax) | GST amount | |

| GST on Sales (Output Tax) | GST amount |

If the goods are used entirely for taxable business purposes, the net GST effect is zero in the same return period. Always verify the current IRAS list of prescribed goods before applying this treatment.

Credit and Debit Note Adjustments

Credit and debit note adjustments must be recorded promptly. When a credit note is issued for a return or discount, both the original sales value and the output tax must be reduced:

| Account | Debit | Credit |

|---|---|---|

| GST on Sales (Output Tax) | GST portion | |

| Sales / Revenue | Net value | |

| Debtors / Bank | Full credit note amount |

Missing these adjustments causes your GST F5 return to overstate or understate taxable supplies — a discrepancy IRAS may flag during a review.

Common GST Accounting Mistakes Singapore Businesses Make

Recording Full Invoice Amounts as Revenue

The most frequent error: posting the total invoice amount (including GST) to the revenue account instead of separating out the GST component.

Incorrect entry:

| Account | Debit | Credit |

|---|---|---|

| Debtors | S$21,800 | |

| Sales / Revenue | S$21,800 |

Correct entry:

| Account | Debit | Credit |

|---|---|---|

| Debtors | S$21,800 | |

| Sales / Revenue | S$20,000 | |

| GST on Sales (Output Tax) | S$1,800 |

The incorrect approach inflates reported sales, overstates income, and obscures the actual output tax liability owed to IRAS.

Claiming Input Tax on Blocked Items

Singapore's GST Act disallows input tax claims on specific categories, including:

- Club memberships and entrance fees

- Medical expenses for employees (with limited exceptions)

- Motor cars (unless used exclusively for commercial purposes such as taxis or driving instruction)

- Family benefits for employees

Businesses that post all supplier GST to GST on Purchases without reviewing eligibility will systematically overclaim input tax — one of the most common triggers for IRAS audit scrutiny. Reviewing each expense category before period-end is a compliance requirement — not a best-practice suggestion. Missing it carries direct penalty exposure.

Failing to Reconcile GST Control Accounts Against the F5 Return

Input tax errors rarely exist in isolation — they often surface during GST return reconciliation. Many businesses prepare their F5 from a summary report without tracing figures back to individual accounting entries. Any discrepancy between the sales figure in the GST return and the revenue figure in the profit and loss account will attract IRAS audit scrutiny, regardless of whether it can be explained.

Best practices to avoid this:

- Reconcile GST control accounts against source documents monthly, not just at filing time

- Retain all tax invoices and import permits for the mandatory five-year period

- Cross-check F5 Box 1 (total standard-rated supplies) and Box 6 (output tax due) directly against ledger totals before submission

IRAS warns that businesses may be penalised up to 200% of tax undercharged for submitting incorrect GST returns — making clean, reconcilable bookkeeping a financial risk management issue, not just an administrative one.

Frequently Asked Questions

What is the journal entry for GST?

On a purchase, debit GST on Purchases (input tax) and credit Creditors or Bank for the full invoice amount. On a sale, credit GST on Sales (output tax) and debit Debtors or Bank. At period end, debit GST on Sales and credit GST on Purchases to arrive at net GST payable to IRAS or receivable from IRAS.

What ledger accounts do Singapore GST-registered businesses need for GST?

At minimum, you need three accounts: GST on Purchases (current asset), GST on Sales (current liability), and a GST Payable or GST Receivable account for net settlement. Singapore's single-rate structure means no separate sub-accounts by tax type are required.

What is the difference between input tax and output tax in Singapore GST?

Input tax is the GST paid to suppliers on eligible purchases (recorded as a recoverable asset), while output tax is the GST collected from customers on taxable supplies (recorded as a liability to IRAS). The net difference determines what your business owes or is owed at period end.

How do you record GST accounting entries for zero-rated supplies?

The sales entry credits Revenue only with no output tax component, since the GST rate is 0%. However, input tax on related purchases remains fully claimable, which is why export-heavy businesses regularly receive GST refunds from IRAS.

When should GST accounting entries be recorded in Singapore?

Entries should be recorded at the time of the transaction or when the tax invoice is issued or received, whichever is earlier. Businesses approved under the Cash Accounting Scheme recognise GST only when payment is made or received, not at the invoice date.

How are GST accounting entries linked to the GST F5 return?

Each F5 box — Box 1 (standard-rated supplies), Box 6 (output tax due), Box 7 (input tax claimed) — pulls directly from your accounting entries for the period. Accurate bookkeeping and regular reconciliation of control accounts against the return keeps IRAS scrutiny at bay.